MNI ASIA OPEN: Tsy Borrow Reqs Low-Side of Expectations

EXECUTIVE SUMMARY

- MNI FED: Gov Cook: December Is A Live Meeting, Noting Downside Employment Risks

- MNI BOC: Macklem: Policy Rates At Low End Of Neutral Range Providing Some Stimulus

- MNI US TSYS/SUPPLY: Treasury Borrowing Requirements Come In On Low Side Of Expected

- MNI US DATA: PMIs Point To Robust Manufacturing As Inventories Climb

- MNI US DATA: A Broadly Disappointing ISM Manufacturing Survey For October

US

MNI FED: Gov Cook: December Is A Live Meeting, Noting Downside Employment Risks

Fed Gov Cook says in a speech Monday that she viewed the decision to cut rates in October "as appropriate, because I believe that the downside risks to employment are greater than the upside risks to inflation", while noting that this cut was "another gradual step toward normalization" keeping rates "modestly restrictive, which is appropriate given that inflation remains somewhat above our 2 percent target." We continue to believe Gov Cook had 75bp of 2025 cuts penciled into her September Dot Plot, alongside most of the Fed Board, and is probably leaning toward a December cut.

MNI BRIEF: Fed’s Cook Says Policy Not On Preset Course

Federal Reserve policy is not on a preset course as the economy faces elevated risks of both higher inflation and elevated unemployment, Fed Governor Lisa Cook said Monday. “Looking ahead, policy is not on a predetermined path. We are at a moment when risks to both sides of the dual mandate are elevated,” she said in prepared remarks to the Brookings Institution.

NEWS

MNI BOC: Macklem: Policy Rates At Low End Of Neutral Range Providing Some Stimulus

BOC Gov Macklem is asked in an event Monday about why the Bank signaled last week that it wouldn't cut rates further (the actual Q from the host: "you said pretty clearly that this is it, you're done, unless things get way off course, you need to stop there. Why?") Macklem doesn't push back against the premise of the question, saying that there are limits to what monetary policy can do to mitigate the economic damage from the US-Canada trade conflict.

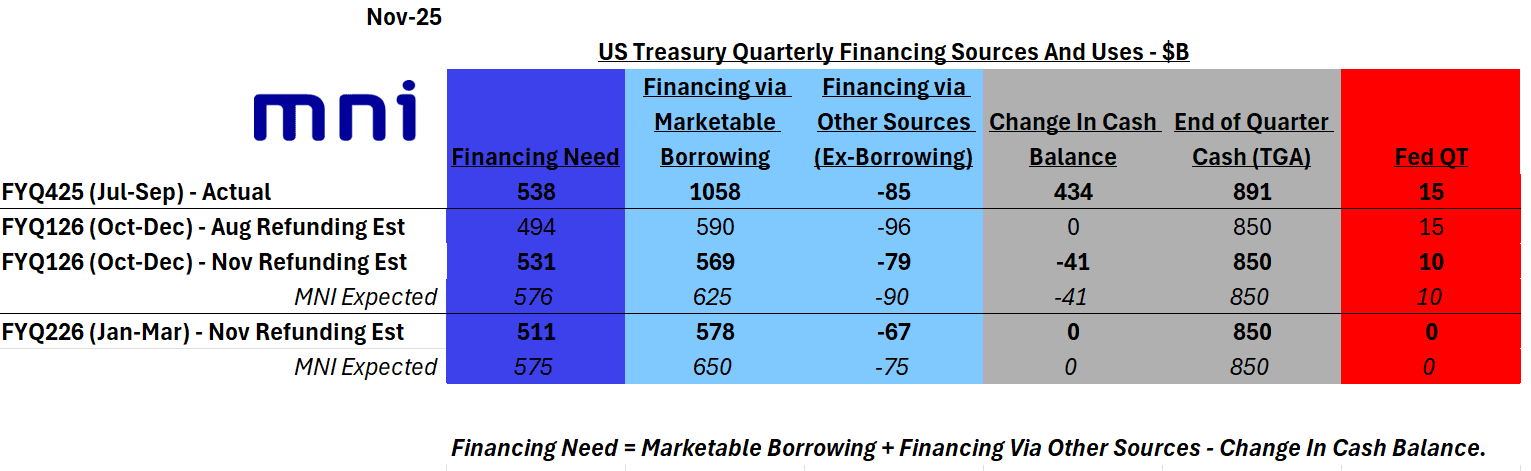

MNI US TSYS/SUPPLY: Treasury Borrowing Requirements Come In On Low Side Of Expected

Treasury's borrowing / financing estimates (Hidden PDF) for the current and next quarters are in the table below. Main takeaways:

- The current quarter's borrowing requirements were lowered to $569B from August's $590B estimate. For the initial estimate of Jan-Mar requirements, a slight further uptick to $578B is seen. These borrowing estimates are below MNI's expectations and are at the lower end of most estimates we'd seen.

- Oct-Dec borrowing estimates ranged from $525B to a high end of $710B (when adjusting for analysts' TGA assumptions).

- For Jan-Mar estimates ranged from $387B to as high as $795B.

- End-quarter cash targets are unchanged at $850B. Some risk had been seen of an upward revision to $900B or higher, which would have upped the borrowing requirements.

BBG: Thune Says Not Enough GOP Votes to End the Senate Filibuster: Senate Majority Leader John Thune says there aren’t enough Republican votes to end the filibuster rule in the upper chamber.

US TSYS

MNI US TSYS: Fed Gov Cook: Dec Meeting Live; Tsy Borrow Reqs Lowered

- Treasuries look to finish steady (10s) to mixed, curves steeper (2s10s curve +.423 at 50.602) with the short end outperforming after the bell.

- Treasuries extended early lows after unexpectedly large corporate bond issuance announced ($40.5B with Alphabet making up $17.5B over 8 tranches) - only to gap back to pre-open level after lower than expected ISM Mfg & Prices paid data, undershooting implications from regional Fed surveys, MNI Chicago PMI and more optimistic S&P Global PMI.

- Fed Gov Cook says in a speech Monday that she viewed the decision to cut rates in October "as appropriate, because I believe that the downside risks to employment are greater than the upside risks to inflation", while noting that this cut was "another gradual step toward normalization" keeping rates "modestly restrictive, which is appropriate given that inflation remains somewhat above our 2 percent target."

- Currently, the 10Y holds steady at 112-21.5, 10Y yield 4.1065% (+.0291). The contract has traded through the 50-day EMA, at 112-26+, highlighting potential for a deeper retracement near-term. A continuation lower would open 112-06, the Sep 25 low and the next key support. On the upside, the contract needs to trade above 113-18+, the Oct 28 high to signal a possible bullish reversal. Key resistance and the bull trigger is at 114-02, the Oct 17 high.

- The current quarter's borrowing requirements were lowered to $569B from August's $590B estimate. For the initial estimate of Jan-Mar requirements, a slight further uptick to $578B is seen. These borrowing estimates are below MNI's expectations and are at the lower end of most estimates we'd seen.

- Despite the greenback making initial further progress on Monday, the USD index rally has stalled just ahead of the psychological 100 mark, and the August highs at 100.25.

OVERNIGHT DATA

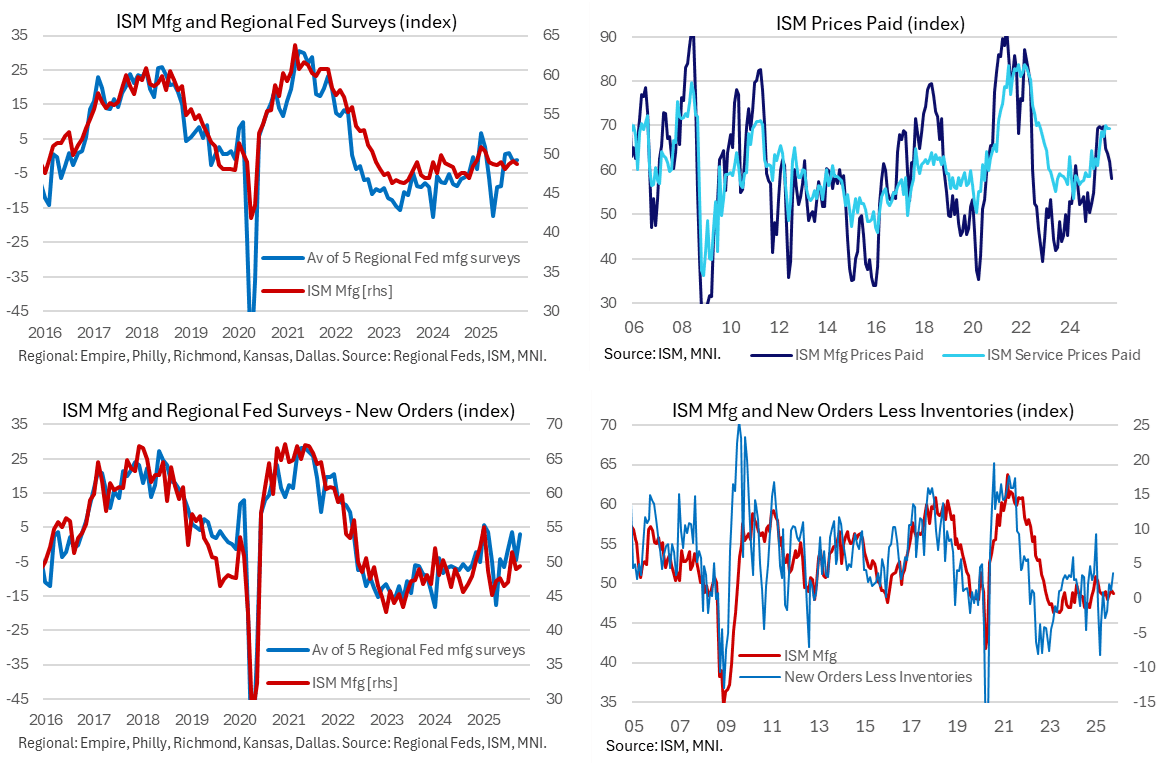

MNI US DATA: A Broadly Disappointing ISM Manufacturing Survey For October

The ISM manufacturing survey for October underwhelmed across the board, undershooting implications from regional Fed surveys, the MNI Chicago PMI and what continues to be a much more optimistic S&P Global PMI. New orders disappointed a bounce seen elsewhere and prices paid fell to the lowest since January, although new orders less inventories did at least point to upside for manufacturing activity ahead.

- ISM manufacturing: 48.7 in Oct (cons 49.5) after 49.1 in Sep

- New orders: 49.4 in Oct after 48.9 in Sep. The small 0.5pt increase after the -2.5 drop in September is disappointing considering the regional Fed surveys along with the MNI Chicago PMI had pointed to a solid bounce in new orders.

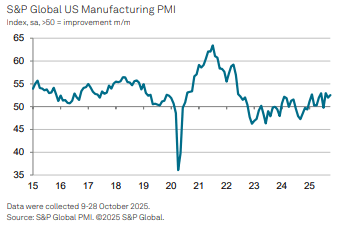

MNI US DATA: PMIs Point To Robust Manufacturing As Inventories Climb

The manufacturing PMI was revised higher in the final October print to 52.5, leaving a larger increase from 52.0 in September but still below the 3+ year high of 53.0 in August. Finished goods inventories increased at their fastest since the data began in 2007, hinting at further volatility within national account data details ahead, whilst input cost inflation confirmed its softest since February. S&P Global US Mfg PMI: 52.5 (cons & flash 52.2) in Oct after 52.0 in September.

Construction Spending data from the US Census Bureau suspended due to ongoing US Gov shutdown.

MARKETS SNAPSHOT

Key market levels of markets in late NY trade:

DJIA down 237.78 points (-0.5%) at 47328.44

S&P E-Mini Future up 4.5 points (0.07%) at 6879.75

Nasdaq up 92.6 points (0.4%) at 23821.79

US 10-Yr yield is up 2.9 bps at 4.1065%

US Dec 10-Yr futures are down 0.5/32 at 112-21

EURUSD down 0.0017 (-0.15%) at 1.152

USDJPY up 0.22 (0.14%) at 154.21

WTI Crude Oil (front-month) up $0.01 (0.02%) at $60.99

Gold is up $7.14 (0.18%) at $4010.11

European bourses closing levels:

EuroStoxx 50 up 17.21 points (0.3%) at 5679.25

FTSE 100 down 15.88 points (-0.16%) at 9701.37

German DAX up 174.11 points (0.73%) at 24132.41

French CAC 40 down 11.28 points (-0.14%) at 8109.79

US TREASURY FUTURES CLOSE

3M10Y -1.958, 22.621 (L: 21.2 / H: 27.656)

2Y10Y +0.434, 50.613 (L: 49.735 / H: 51.458)

2Y30Y +1.496, 109.042 (L: 107.296 / H: 109.853)

5Y30Y +1.02, 97.248 (L: 96.298 / H: 98.213)

Current futures levels:

Dec 2-Yr futures up 0.375/32 at 104-4.25 (L: 104-03.5 / H: 104-06)

Dec 5-Yr futures down 0.25/32 at 109-6.5 (L: 109-05 / H: 109-11.25)

Dec 10-Yr futures down 0.5/32 at 112-21 (L: 112-18.5 / H: 112-27)

Dec 30-Yr futures down 6/32 at 117-4 (L: 116-29 / H: 117-18)

Dec Ultra futures down 12/32 at 120-29 (L: 120-21 / H: 121-22)

MNI US 10YR FUTURE TECHS: (Z5) Key Support Remains Exposed

- RES 4: 114-02 High Oct 17 and the bull trigger

- RES 3: 113-29 High Oct 22

- RES 2: 113-18+ High Oct 28

- RES 1: 113-06 20-day EMA

- PRICE: 112-20+ @ 1311 ET Nov 3

- SUP 1: 112-16 Low Oct 30

- SUP 2: 112-14 Low Oct 9

- SUP 3: 112-06 Low Sep 25 and a reversal trigger

- SUP 4: 111-30 Trendline support drawn from the May 22 low

Recent weakness in Treasuries undermines a bullish theme. The contract has traded through the 50-day EMA, at 112-26+, highlighting potential for a deeper retracement near-term. A continuation lower would open 112-06, the Sep 25 low and the next key support. On the upside, the contract needs to trade above 113-18+, the Oct 28 high to signal a possible bullish reversal. Key resistance and the bull trigger is at 114-02, the Oct 17 high.

SOFR FUTURES CLOSE

Current White pack (Dec 25-Sep 26):

Dec 25 +0.010 at 96.235

Mar 26 +0.010 at 96.415

Jun 26 +0.010 at 96.650

Sep 26 steady00 at 96.805

Red Pack (Dec 26-Sep 27) -0.01 to -0.005

Green Pack (Dec 27-Sep 28) -0.01 to -0.005

Blue Pack (Dec 28-Sep 29) -0.005 to steady

Gold Pack (Dec 29-Sep 30) -0.005 to steady

REFERENCE RATES

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.22% (+0.18), volume: $3.211T

- Broad General Collateral Rate (BGCR): 4.15% (+0.16), volume: $1.153T

- Tri-Party General Collateral Rate (TCR): 4.15% (+0.16), volume: $1.117T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 3.86% (-0.01), volume: $107B

- Daily Overnight Bank Funding Rate: 3.86% (-0.01), volume: $195B

FED Reverse Repo Operation

RRP usage retreats to $23.792B with 18 counterparties going into month end - from $51.802B Friday. Compares to $2.435B on October 24 (lowest level since mid-March 2021) and the year's highest usage of $460.731B on June 30.

MNI PIPELINE: Corporate Bond Roundup: Over $40B to Price Monday

November kicks off with $40.25B corporate debt to price Monday, $17.5B Alphabet 8pt leading:

- Date $MM Issuer (Priced *, Launch #)

- 11/03 $17.5B #Alphabet: $1B 3Y +30, $500M 3Y SOFR+52, $2.5B +5Y +40, $1.25B 7Y +50, $3.5B 10Y +62, $2B 20Y +72, $4B 30Y +82, $2.75B 50Y +107 (massive debt issuance includes $6.5B over 6 tranches: 3Y, 6Y, 7Y, 13Y, 19Y and 39Y).

- 11/03 $6B #Novartis Capital: $700M 3Y +30, $800M 3Y SOFR+52, $1.75B 5Y +45, $925M 7Y +50, $925M 10Y +55, $350M 20Y +55, $550M 30Y +65

- 11/03 $4B #Qatar $1B 3Y +15, $3B 10Y Sukuk +20

- 11/03 $3.25B #UBS $2B 8NC7 +95, $1.25B 21.5NC20.5 +87.5

- 11/03 $2.35B #Shell $1B 5Y +50, $350M 5Y SOFR+78, $1B +10Y +67

- 11/03 $2B Tenet 7NC3 5.5%, 8NC3 6.0%

- 11/03 $1B #EBAY $600M 3Y +65, $400M 10Y +103

- 11/03 $1B #Nisource 30.7NC5.5 5.75%

- 11/03 $1B Neptune Bidco 5.5NC2

- 11/03 $600M #WEC Energy 30.5NC5.25 5.625%

- 11/03 $550M *EPR Properties 5Y +130

- 11/03 $500M *Lincoln National 10Y +125

- 11/03 $500M #Howmet Aerospace WNG 7Y +65

MNI EGB BONDS: EGBs-GILTS CASH CLOSE: Bunds Underperform Amid Light Bear Steepening

European curve bear steepened modestly Monday, with Bunds underperforming.

- Global core FI was under pressure through much of the session due to large US corporate issuance.

- A softer-than-expected US ISM Manufacturing report triggered a relief rally in Treasuries that spilled over the Atlantic.

- However most of the session's damage was done toward the cash close though as EGB futures were sold in size, despite no obvious headline trigger for the move.

- In data, Spanish and Italian manufacturing PMIs improved more than expected in October.

- The UK and German curves each bear steepened very slightly, with Bunds slightly underperforming on the day. Periphery/semi-core EGB spreads tightened modestly.

- Tuesday's data schedule is light, with French budget data and Spanish labour market data, alongside several ECB speakers (including Lagarde and Rehn) and BOE's Breeden. In the UK, focus remains on pre-Budget fiscal speculation and setup ahead of this week's BoE decision.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 3bps at 1.998%, 5-Yr is up 3.5bps at 2.268%, 10-Yr is up 3.4bps at 2.667%, and 30-Yr is up 4bps at 3.251%.

- UK: The 2-Yr yield is up 2.4bps at 3.795%, 5-Yr is up 2.5bps at 3.907%, 10-Yr is up 2.6bps at 4.435%, and 30-Yr is up 3bps at 5.208%.

- Italian BTP spread down 0.8bps at 74.3bps / French OAT down 0.4bps at 77.8bps

MNI FOREX: August Highs Cap DXY Topside for Now, CHF & CAD Weakest in G10

- Despite the greenback making initial further progress on Monday, the USD index rally has stalled just ahead of the psychological 100 mark, and the August highs at 100.25. Additionally, weaker-than-expected ISM manufacturing and prices paid data have provided a moderate dollar headwind, especially against a backdrop of relatively few US data releases in recent weeks.

- Softer-than-expected CPI data in Switzerland this morning has resulted in the Swiss Franc being the weakest currency across the G10 today. EURCHF (+0.28%) held a significant medium-term support last week, and spot is now operating roughly 100 pips above the key 0.9206 level. A break back above 50-day EMA resistance at 0.9308 would be a bullish development, likely allowing the cross to re-establish the 0.93-0.94 range that was broadly in place between May/September.

- USDCAD's +0.30% Monday rally puts the pair on course for a third consecutive higher daily close but, more importantly, the pair is on course to test and break 1.4080 resistance to clear to the best levels since mid-April's Liberation Day. Tomorrow's Federal Budget in Canada remains a key risk with some analysts touting risks of a "significantly more expansionary than previous" annual budget. The next topside level would be 1.4111, the Apr 10 high.

- There was a slight divergence between the antipodeans to start the week, with AUDNZD trading to a fresh cycle high of 1.1461. Solid demand was found beneath 1.13 and the latest strength further narrows the gap towards the 2022 highs at 1.1491. A break of this level would place the cross at its highest point since 2013. The RBA decision highlights the APAC calendar on Tuesday, and NZ employment data is scheduled Wednesday.

- Other central bank decisions due later in the week include the Riksbank, Norges Bank and the Bank of England.

TUESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 04/11/2025 | 0740/0840 | ECB Lagarde Keynote Speech At Bulgarian National Bank | ||

| 04/11/2025 | 0745/0845 | Budget Balance | ||

| 04/11/2025 | 0945/1045 | ECB Lagarde At Bulgarian National Bank Press Conference | ||

| 04/11/2025 | 1000/1000 | ** | Gilt Outright Auction Result | |

| 04/11/2025 | 1135/0635 | Fed Vice Chair Michelle Bowman | ||

| 04/11/2025 | 1140/1140 | BOE Breeden at International Banking Conference | ||

| 04/11/2025 | 1330/0830 | ** | Trade Balance | |

| 04/11/2025 | 1330/0830 | ** | Trade Balance | |

| 04/11/2025 | 1355/0855 | ** | Redbook Retail Sales Index | |

| 04/11/2025 | 1500/1000 | ** | Factory New Orders | |

| 04/11/2025 | 1500/1000 | *** | JOLTS jobs opening level | |

| 04/11/2025 | 1500/1000 | *** | JOLTS quits Rate | |

| 04/11/2025 | 1500/1000 | ** | Factory New Orders | |

| 04/11/2025 | 2100/1600 | Canada federal budget, release expected just after 4pm EST | ||

| 05/11/2025 | 2200/0900 | * | S&P Global Final Australia Services PMI | |

| 05/11/2025 | 2200/0900 | ** | S&P Global Final Australia Composite PMI | |

| 05/11/2025 | - | Riksbank Meeting | ||

| 05/11/2025 | 0145/0945 | ** | S&P Global Final China Services PMI | |

| 05/11/2025 | 0145/0945 | ** | S&P Global Final China Composite PMI |