MNI ASIA OPEN: Trump Considers Joining Strikes on Iran

EXECUTIVE SUMMARY

- MNI FED: FOMC Meeting Expectations: Patience Mostly Seen In New Projections

- MNI US DATA: Import Prices Show Most Exporters Didn’t Take Tariff “Hit” In Apr/May

- MNI US DATA: Control Group Flatters Mixed Retail Sales Report

- MNI US DATA: Industrial Output Continues To Stutter After Pre-Tariff Burst

US

MNI FED: FOMC Meeting Expectations: Patience Mostly Seen In New Projections

We expect that the June meeting communications will reflect an increasingly patient attitude since May and certainly since March’s projections. Our full meeting preview, including analyst expectations, is Hidden PDF

- With the Statement in need of only mark-to-market edits, and Chair Powell’s commentary unlikely to be much different from May’s press conference, this patience will be mostly reflected in the new SEP. There is a fairly low bar to the 2025 rate median to shift up to show 1 cut instead of March’ 2, and that seems like the most likely outcome.

- Overall despite its patience, the FOMC’s easing bias remains, perhaps aided to some extent by recent inflation data coming in softer than feared. This will be reflected in the 2026-27 dots which will show that the destination remains more or less the same, just with a delay.

NEWS

MNI SECURITY: Tensions Rise In MidEast As Trump Considers Joining Strikes On Iran

Media reports in the past minutes point to an intensification of hostilities between Iran and Israel, as US President Donald Trump meets his national security team at the White House to consider joining Israeli strikes on Iran. Iran will soon launch a 'punitive' operation against Israel, per Iran’s Chief of Staff of Armed Forces on Operations. Video statement here, per Iran Nuances on X.

MNI SECURITY: Trump To Decide On Iran Strategy In NatSec Meeting Underway Shortly

Bloomberg reporting that German Chancellor Friedrich Merz, speaking at the G7 Leaders’ Summit in Canada, said the US will decide today "whether to join Iran conflict,” noting the US decision “depends on whether Iran negotiates.” The comments are the latest in a series of hawkish remarks from Merz that have aligned Berlin firmly with Israel’s operation against Iran.

MNI SECURITY: Trump Threatens Iranian Supreme Leader, Iran Alleges Cyber Attack

US President Donald Trump has escalated his rhetoric towards Iran with a statement on Truth Social calling Iran's Supreme Leader Ayatollah Ali Khamenei an "easy target", but stating the US won't eliminate him "for now". Trump: "We know exactly where the so-called “Supreme Leader” is hiding. He is an easy target, but is safe there - We are not going to take him out (kill!), at least not for now. But we don’t want missiles shot at civilians, or American soldiers. Our patience is wearing thin. Thank you for your attention to this matter!"

- Trump followed the message with a second Truth saying: "UNCONDITIONAL SURRENDER!" The statement appears to be the clearest threat yet from the White House that the US will join Israeli airstrikes on Iran if Tehran doesn't immediately submit to a ceasefire on US terms.

MNI SECURITY: Trump Appears To Hint At Deeper US Involvement In Iran Conflict

US President Donald issued the following statement on Truth Social: "We now have complete and total control of the skies over Iran. Iran had good sky trackers and other defensive equipment, and plenty of it, but it doesn’t compare to American made, conceived, and manufactured “stuff.” Nobody does it better than the good ol’ USA."

MNI G7: Trump Departure Leaves Outreach Partners Out In Cold, Risks US Isolation

The G7 summit in Kananaskis, Alb. concludes later today after working sessions on support for Ukraine and energy security. The notable absence of US President Donald Trump will inevitably limit the ability of G7 leaders and those from the 'outreach partners' attending to achieve their main aims from the summit, given that it is with the US that so many countries are looking to either mitigate the impact of tariffs, ensure continued backing for Kyiv, or looking to influence a de-escalation in the Middle East.

MNI CRYPTO: US Senate Vote On Landmark Crypto Regulation Bill Expected At 17:00 ET

The United States Senate is poised to pass the GENIUS Act, a landmark crypto bill to create a regulatory framework for stablecoins, which are pegged to the value of the dollar. Craig Caplan at CSPAN notes that a final vote on the floor is expected at around 17:00 ET 22:00 BST.

US TSYS

MNI US TSYS: Safe Haven Raises Rates in Lead-Up to FOMC Policy Annc

- Rising Middle East tensions included chances the US will join the war lent to the second half risk-off support for Treasuries Tuesday. Otherwise, markets await Wednesday's FOMC policy announcement including a Summary of Economic Projections (Dots).

- Pres Trump: "We know exactly where the so-called “Supreme Leader” is hiding. He is an easy target, but is safe there - We are not going to take him out (kill!), at least not for now. But we don’t want missiles shot at civilians, or American soldiers. Our patience is wearing thin. Thank you for your attention to this matter!"

- We expect that the June FOMC meeting communications will reflect an increasingly patient attitude since May and certainly since March’s projections.

- Cross asset update: stocks ebbed in the second half (SPX eminis -44.75 at 6045.0), West Texas crude climbed to early July 2024 highs (WTI +3.39 at 75.16), while Bbg US$ index climbed to June 11 highs (BBDXY +6.43 at 1209.02).

- Tsy Sep'25 10Y futures trades +12.5 at 110-28 vs. 111-00 high, below key resistance and its recent high of 111-14+, a Fibonacci retracement and the Jun 5 high. Clearance of this hurdle would be bullish and highlight a stronger reversal. This would open 111-30, a Fibonacci retracement.

- Curves flatter, 2s10s -4.250 at 43.309, 5s30s -1.837 at 90.209. 10Y yield at 4.3849% vs. 4.3770% low.

OVERNIGHT DATA

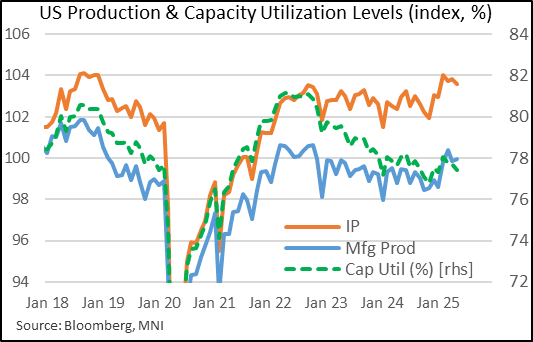

MNI US DATA: Industrial Output Continues To Stutter After Pre-Tariff Burst

Industrial production unexpectedly contracted in May, falling 0.2% M/M vs a consensus for +0.1%, though this was partially offset by an upward revision to April (0.1% vs 0.0%). Manufacturing production growth was in-line with 0.1% growth, though April was revised a bit lower (-0.5% after -0.4%). That meant utilities were the primary reason overall IP fell, with a decline of 2.9% M/M following a strong April (+4.9%, upward rev from +3.3%), looking largely weather related (electric utilities -3.6% M/M, vs natural gas +2.7%).

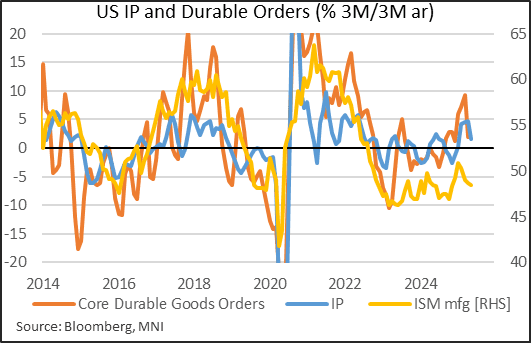

- Overall, US industrial output looks to have peaked in Q1 for the time being, reflecting some pulling forward in production and demand ahead of tariff impacts. Most indicators, including durable goods orders and surveys such as ISM Manufacturing, have pointed to a pullback in Q2 in industrial output which looks to be borne out in the data so far.

- Manufacturing output rose at a 39-month best 5.5% 3M/3M SAAR pace in April largely reflecting a breakneck Feb/Mar, but this has started to pull back to 3.9%. On a Y/Y basis, manufacturing levels are up just 0.5%.

- Also reflecting the pullback, the level of the IP index is below its February level, and up just 0.6% Y/Y, the slowest since December (and 1.5% 3M/3M SAAR). Overall capacity utilization fell 0.3pp to a 4-month low 77.4%.

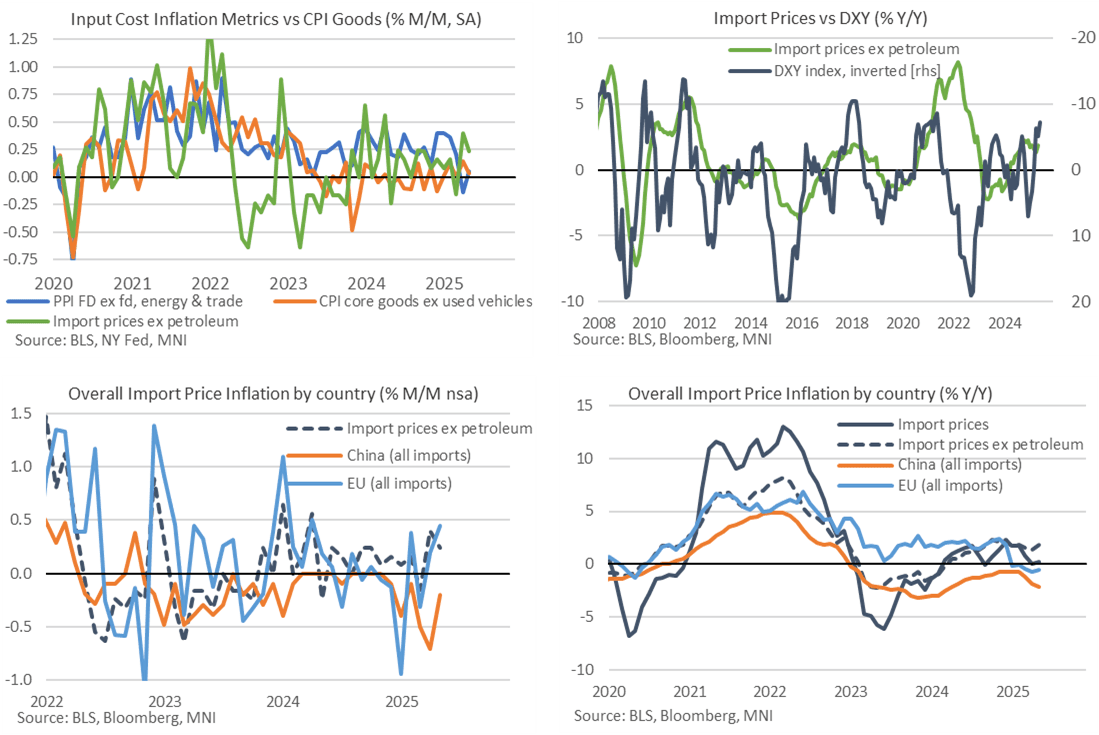

MNI US DATA: Import Prices Show Most Exporters Didn’t Take Tariff “Hit” In Apr/May

- Import prices were a little stronger than expected in May at 0.0% M/M (cons -0.2) after 0.1% in April whilst ex petroleum prices increased 0.2% M/M (cons 0.1) after 0.4% in April.

- For ex-petroleum prices, it’s a solid increase after the 0.4% in April was its strongest in twelve months. It saw the Y/Y accelerate from 1.36% to 1.8% Y/Y for its highest since February and with some further increases possible judging by USD weakness - see charts below.

- Whilst these data do not take account of tariffs (which are considered taxes in the national accounts), they importantly point to little sign of exporters taking part of the “hit” of US tariffs in the form of lowering their prices to remain more competitive against countries with lower tariff rates.

- That’s on a widespread basis, and likely a factor of the baseline ‘reciprocal’ 10% tariff rates seen for many countries during the current 90-day pause. There are however signs of some discounting from those that have been targeted more heavily, with China a clear standout.

- For example, overall import prices from China fell -0.2% M/M in May after a heavy -0.7% M/M in April whereas prices from the EU increased 0.4% M/M after 0.2% M/M.

- Overall declines in Canada (-1.0%) and Mexico (-0.3%) have to be taken with caution, as this was driven by fuel prices, with non-manufacturing import prices +0.7% M/M from Canada and 0.0% M/M from Mexico.

- China import price inflation stands at -2.1% Y/Y (weakest since Apr 2024) whilst EU import price inflation lifted from -0.8% to -0.5% Y/Y after what had been its weakest since May 2020.

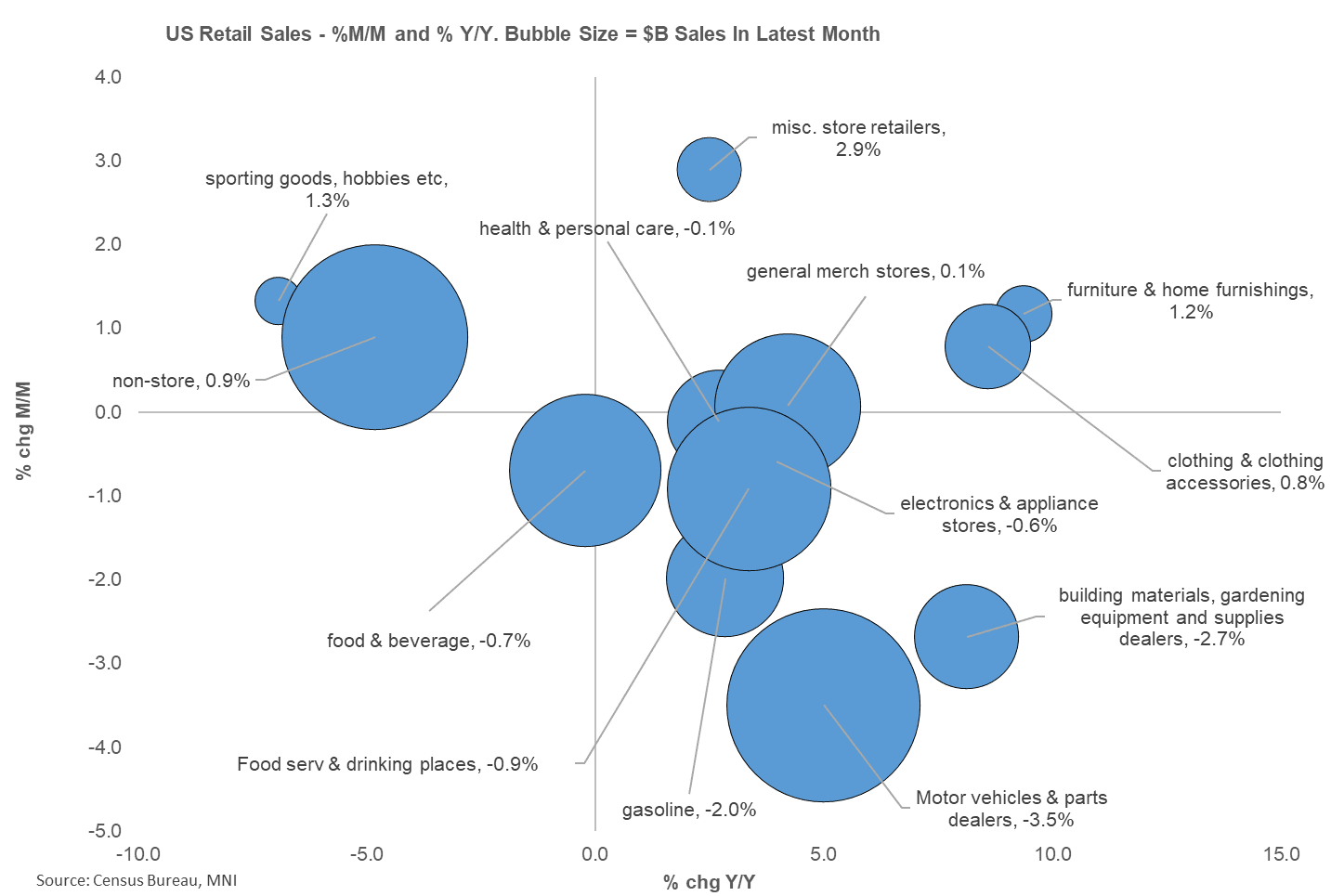

MNI US DATA: Control Group Flatters Mixed Retail Sales Report

May saw the biggest month-to-month drop in retail sales (-0.91% M/M SA unrounded, vs -0.6% consensus and -0.1% April rev from +0.1%) since March 2023, with ex-autos/gas weaker than expected (-0.1% vs +0.3%) and surprisingly decelerating from April (0.1%, rev down from 0.2%). Likewise, ex-auto sales unexpectedly fell, by 0.3% (+0.2% expected, 0.0% prior rev down from 0.1%).

- Bucking the trend was the closely-watched Control Group, which rose more than expected at 0.4% (0.3% consensus), with prior revised up (April -0.1%, from -0.2%).

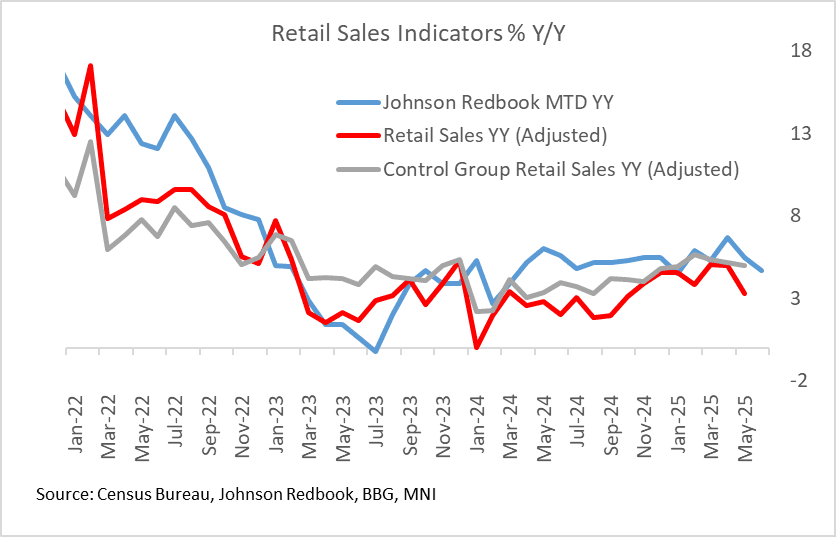

MNI US DATA: Redbook Sales Continue To Suggest Steady Slowdown In Core Retail

Johnson Redbook's retail sales index showed a 5.2% Y/Y rise in the week ending Jun 14, up from 4.7% prior and bringing June-to-date sales to 5.0% Y/Y.

MNI CANADA DATA: StatsCan Boosts CPI Weight Of Food, Lowers Housing

- StatsCan's annual re-weighting of CPI basket Tues increases share for food to 16.9% from 16.7% last year, and up from 16.2% in 2020.

- Shelter increases to 29.4% from 29.2%, but below 30% in 2020.

- Transportation unchanged at 16.9%, up from 16% in 2020.

- Overall services basket has climbed to 55.6% from 51.2% in 2020; goods declines to 44.5% from 48.8%.

- Reweighting comes at a time when BOC has been more concerned about elevated core inflation.

MARKETS SNAPSHOT

Key market levels of markets in late NY trade:

DJIA down 329.6 points (-0.78%) at 42187.53

S&P E-Mini Future down 50.75 points (-0.83%) at 6039.75

Nasdaq down 168.4 points (-0.9%) at 19533.57

US 10-Yr yield is down 5.7 bps at 4.3888%

US Sep 10-Yr futures are up 11.5/32 at 110-27

EURUSD down 0.0076 (-0.66%) at 1.1485

USDJPY up 0.52 (0.36%) at 145.27

WTI Crude Oil (front-month) up $3.1 (4.32%) at $74.89

Gold is down $0.39 (-0.01%) at $3384.80

European bourses closing levels:

EuroStoxx 50 down 50.89 points (-0.95%) at 5288.68

FTSE 100 down 41.19 points (-0.46%) at 8834.03

German DAX down 264.47 points (-1.12%) at 23434.65

French CAC 40 down 58.51 points (-0.76%) at 7683.73

US TREASURY FUTURES CLOSE

3M10Y -1.906, 6.618 (L: 4.139 / H: 11.764)

2Y10Y -4.065, 43.494 (L: 43.099 / H: 48.885)

2Y30Y -4.775, 93.68 (L: 93.179 / H: 100.557)

5Y30Y -1.884, 90.162 (L: 89.378 / H: 94.146)

Current futures levels:

Sep 2-Yr futures up 1.25/32 at 103-19.875 (L: 103-18.125 / H: 103-22.5)

Sep 5-Yr futures up 6.5/32 at 108-4 (L: 107-29.25 / H: 108-08)

Sep 10-Yr futures up 11.5/32 at 110-27 (L: 110-15.5 / H: 111-00)

Sep 30-Yr futures up 1-00/32 at 113-21 (L: 112-21 / H: 113-26)

Sep Ultra futures up 1-09/32 at 116-28 (L: 115-19 / H: 117-04)

MNI US 10YR FUTURE TECHS: (U5) Monitoring Resistance

- RES 4: 111-30 76.4% retracement of the May 1 - 22 downleg

- RES 3: 111-21 1.0% 10-dma envelope

- RES 2: 111-14+ High Jun 5 & 61.8% of the May 1 - 22 downleg

- RES 1: 111-13 High Jun 13

- PRICE: 110-17 @ 1015 ET Jun 17

- SUP 1: 109-28 Low Jun 6 / 11

- SUP 2: 109-12+ Low May 22 and the bear trigger

- SUP 3: 109-09+ Low Apr 11 and key support

- SUP 4: 108-25+ 0.764 proj of the Apr 7 - 11 - May 1 price swing

Treasury futures continue to trade below key resistance and its recent high of 111-14+, a Fibonacci retracement and the Jun 5 high. Clearance of this hurdle would be bullish and highlight a stronger reversal. This would open 111-30, a Fibonacci retracement. On the downside, support to watch lies at 109-28, the Jun 6 / 11 low. Clearance of this level would be bearish and open the bear trigger at 109-12+, the May 22 low.

SOFR FUTURES CLOSE

Jun 25 -0.003 at 95.668

Sep 25 -0.015 at 95.855

Dec 25 -0.025 at 96.090

Mar 26 -0.005 at 96.320

Red Pack (Jun 26-Mar 27) +0.010 to +0.050

Green Pack (Jun 27-Mar 28) +0.055 to +0.065

Blue Pack (Jun 28-Mar 29) +0.065 to +0.070

Gold Pack (Jun 29-Mar 30) +0.065 to +0.065

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.32% (+0.04), volume: $2.697T

- Broad General Collateral Rate (BGCR): 4.30% (+0.03), volume: $1.090T

- Tri-Party General Collateral Rate (TCR): 4.30% (+0.03), volume: $1.065T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $101B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $273B

FED Reverse Repo Operation

RRP usage bounces to $168.939B this afternoon from $140.759B yesterday, total number of counterparties at 37. Usage had fallen to $54.772B on Wednesday, April 16 -- lowest level since April 2021. Conversely, usage had surged to the highest level since December 31, 2024 on Monday, March 31: $399.167B.

MNI PIPELINE: Corporate Bond Update: Over $18.7B Debt to Price Tuesday

- Date $MM Issuer (Priced *, Launch #)

- $18.767B To price Tuesday, $32.717B/wk

- 06/17 $5B *EIB 7Y SOFR+50

- 06/17 $3.5B #Hyundai Cap AM: $1B 2Y +93, $400M 2Y SOFR+112, $1B 3Y +103, $600M 5Y +112, $500M 7Y +127

- 06/17 $3B #UnitedHealth $500M 3Y +52, $750M +5Y +70, $1B 10Y +92, $750M 30Y +112

- 06/17 $3B *KFW 2Y SOFR+26

- 06/17 $2B #Enterprise Products $500M 3Y +45, $750M +5Y +65, $750M +10Y +85

- 06/17 $1.2B *Islamic Development Bank Sukuk 5Y SOFR+57

- 06/17 $1.067B #The Bahamas 11Y 8.25%

MNI BONDS: EGBs-GILTS CASH CLOSE: Flatter Curves With Geopolitics Front Of Mind

European yields rose modestly Tuesday, with curves mostly flattening.

- Yields gapped higher on the open, catching up with the weakness in global bonds after Monday's cash close. Geopolitical and related inflation (energy)-related risk weighed on sentiment throughout amid the ongoing Israel-Iran conflict.

- Yields moved lower and hit session lows in a safe haven bid as the Israeli Defence Minister pointed to further attacks on Iran, a move that extended after weaker-than-expected US retail sales data.

- Core EGBs and Gilts would pull back again over the afternoon, with oil and gas prices moving higher, and some consideration given to robust US core retail data and firm import prices.

- German ZEW expectations jumped in June, with current conditions also improving.

- The German curve twist flattened, with the 2Y-5Y segment underperforming the UK which saw bear steepening and longer-end underperformance ahead of Wednesday's UK CPI data.

- Periphery / semi-core EGB spreads widened steadily through a broadly risk-off session.

- MNI's Markets Team sees downside risks to the headline UK CPI and services readings Wednesday - Hidden PDF.

MNI FOREX: USD Strength Extending as Middle-East Tensions Rise

- Headlines surrounding the Israel-Iran conflict, paired with President’s Trump escalatory rhetoric, have dented risk sentiment in currency markets, which has filtered through into a steady move higher for the US dollar across the US session.

- GBPUSD is notably underperforming in G10 as the pair currently tracks 0.87% lower on the session as we approach the APAC crossover, comfortably back below the 1.35 mark.

- This has coincided with a breach of the 20-day exponential moving average, of which spot has not closed below since May 12. A sustained break would be a bearish development, signalling scope for a deeper retracement below 1.3456 (Jun 10 low) and targeting the 50-day EMA at 1.3346.

- The likes of EUR, AUD and NZD have fallen over half a percent against the greenback. Price action has seen EURUSD slip back below 1.15, in what is deemed as a corrective selloff for now.

- USDJPY has risen 0.3%, evidence of the broad dollar strength on display. The pair is narrowing the gap to last week’s highs at 145.46. Key short-term resistance remains further out at 146.28, the May 29 high.

- Wednesday’s data calendar kicks off with UK CPI. US jobless claims & housing starts will precede the June FOMC decision later in the session.

WEDNESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 18/06/2025 | 0600/0700 | *** | Consumer inflation report | |

| 18/06/2025 | 0730/0930 | *** | Riksbank Interest Rate Decison | |

| 18/06/2025 | 0730/0930 | ECB Elderson At SRB Legal Conference 2025 | ||

| 18/06/2025 | 0800/1000 | ** | EZ Current Account | |

| 18/06/2025 | 0900/1100 | *** | HICP (f) | |

| 18/06/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 18/06/2025 | 1230/0830 | *** | Housing Starts | |

| 18/06/2025 | 1230/0830 | *** | Jobless Claims | |

| 18/06/2025 | 1230/0830 | *** | Housing Starts | |

| 18/06/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 18/06/2025 | 1500/1700 | ECB Lane At Macroprudential Conference | ||

| 18/06/2025 | 1515/1115 | BOC Governor speaks in Newfoundland. | ||

| 18/06/2025 | 1600/1200 | ** | Natural Gas Stocks | |

| 18/06/2025 | 1800/1400 | *** | FOMC Statement | |

| 18/06/2025 | 1800/2000 | ECB de Guindos at Osservatorio Permanente Giovani-Editori | ||

| 18/06/2025 | 2000/1600 | ** | TICS | |

| 19/06/2025 | 2245/1045 | *** | GDP | |

| 19/06/2025 | - | NorgesBank Meeting | ||

| 19/06/2025 | - | Swiss National Bank Meeting | ||

| 19/06/2025 | 0130/1130 | *** | Labor Force Survey |