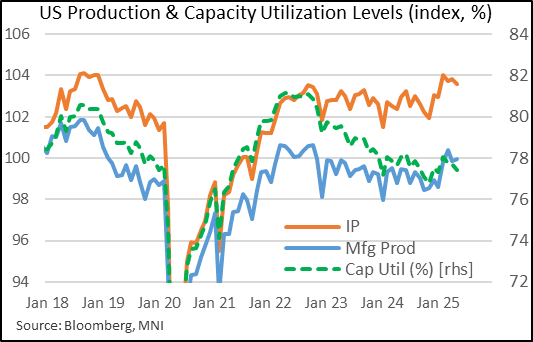

US DATA: Industrial Output Continues To Stutter After Pre-Tariff Burst

Industrial production unexpectedly contracted in May, falling 0.2% M/M vs a consensus for +0.1%, though this was partially offset by an upward revision to April (0.1% vs 0.0%). Manufacturing production growth was in-line with 0.1% growth, though April was revised a bit lower (-0.5% after -0.4%).

- That meant utilities were the primary reason overall IP fell, with a decline of 2.9% M/M following a strong April (+4.9%, upward rev from +3.3%), looking largely weather related (electric utilities -3.6% M/M, vs natural gas +2.7%).

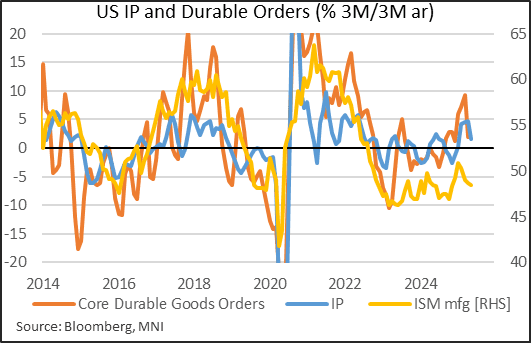

- Overall, US industrial output looks to have peaked in Q1 for the time being, reflecting some pulling forward in production and demand ahead of tariff impacts. Most indicators, including durable goods orders and surveys such as ISM Manufacturing, have pointed to a pullback in Q2 in industrial output which looks to be borne out in the data so far.

- Manufacturing output rose at a 39-month best 5.5% 3M/3M SAAR pace in April largely reflecting a breakneck Feb/Mar, but this has started to pull back to 3.9%. On a Y/Y basis, manufacturing levels are up just 0.5%.

- Also reflecting the pullback, the level of the IP index is below its February level, and up just 0.6% Y/Y, the slowest since December (and 1.5% 3M/3M SAAR). Overall capacity utilization fell 0.3pp to a 4-month low 77.4%.

- Major market groups were mixed, though likewise paint a picture of pre-/post-tariff dynamics: consumer goods production fell for a 3rd consecutive month (-0.2%) after a strong burst in February (+1.1%), with the level of production below end-2024 levels. Construction/non-industrial and materials production also continued to struggle.

- On a more positive note: motor vehicle assemblies soared 7.2% in May, to 11.19M, most since March 2024, with overall automotive product production up 3.9% (albeit merely rebounding from -2.9% in April), helping durables offset nondurable weakness in consumer goods output. And the solid 0.8% M/M rise in business equipment production which continues to be the best performing major market group category, albeit this has cooled significantly from late 2024/early 2025.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EURUSD TECHS: Support Remains Intact

- RES 4: 1.1625 1.500 proj of the Feb 28 - Mar 18 - 27 price swing

- RES 3: 1.1608 High Nov 9 2021

- RES 2: 1.1440/1573 High Apr 23 / 21 and the bull trigger

- RES 1: 1.1266/1381 High May 14 / High May 2 - 6

- PRICE: 1.1144 @ 19:09 BST May 16

- SUP 1: 1.1094/65 50-day EMA and a pivot level / Low May 12

- SUP 2: 1.1026 38.2% retracement of the Feb 3 - Apr 21 bull cycle

- SUP 3: 1.0943 Low Apr 10

- SUP 4: 1.0857 50.0% retracement of the Feb 3 - Apr 21 bull cycle

EURUSD continues to trade above last week’s low. Recent weakness appears corrective and key trend signals highlight an uptrend. Note that a key support at the 50-day EMA, at 1.1094, remains intact. A clean break of this average would undermine the uptrend. A key resistance to watch is 1.1381, the May 2 - 6 high. Clearance of this level would signal the end of the correction and highlight a bullish break.

RATINGS: Moody's Downgrades US's AAA Rating As Deficits Seen Ballooning

Moody's has downgraded the US's long-term credit rating to Aa1 trom Aaa. The move may not have been fully expected today. But it was the last holdout among they S&P and Fitch to demote the USA from the top rating, and they placed negative outlook on the US last year (now stable). Fiscal deterioration, both past and anticipated as Congress wrangles with the Republican fiscal bill, is cited as the key factor. From the release (link):

- “While we recognize the US’ significant economic and financial strengths, we believe these no longer fully counterbalance the decline in fiscal metrics."

- "This one-notch downgrade on our 21-notch rating scale reflects the increase over more than a decade in government debt and interest payment ratios to levels that are significantly higher than similarly rated sovereigns...We do not believe that material multi-year reductions in mandatory spending and deficits will result from current fiscal proposals under consideration."

- "If the 2017 Tax Cuts and Jobs Act is extended, which is our base case, it will add around $4 trillion to the federal fiscal primary (excluding interest payments) deficit over the next decade. As a result, we expect federal deficits to widen, reaching nearly 9% of GDP by 2035, up from 6.4% in 2024, driven mainly by increased interest payments on debt, rising entitlement spending, and relatively low revenue generation."

- "We anticipate that the federal debt burden will rise to about 134% of GDP by 2035, compared to 98% in 2024."

- "Federal interest payments are likely to absorb around 30% of revenue by 2035, up from about 18% in 2024 and 9% in 2021. The US general government interest burden, which takes into account federal, state and local debt, absorbed 12% of revenue in 2024, compared to 1.6% for Aaa-rated sovereigns."

US FISCAL: "Extraordinary Measures" Continue To Dwindle Amid Debt Impasse

The "extraordinary measures" available to Treasury to stave off a debt default were down to $82B as of May 14, per a Treasury Department release today.

- That compares unfavorably with a high of $335B in January when the debt limit impasse began. Combined with $562B in Treasury cash on hand, though, after April's large tax intakes, that makes for around $644B in available resources before the "x-date" is reached.

- Resources are gradually being eroded since reaching nearly $800B in mid-April.

- Per Tsy Sec Bessent's letter to Congress last week, "after reviewing receipts from the recent April tax filing season, there is a reasonable probability that the federal government's cash and extraordinary measures will be exhausted in August while Congress is scheduled to be in recess. Therefore, I respectfully urge Congress to increase or suspend the debt limit by mid-July, before its scheduled break, to protect the full faith and credit of the United States."