MNI ASIA OPEN: Rate Cut Pricing Consolidates On Strong US Data

EXECUTIVE SUMMARY

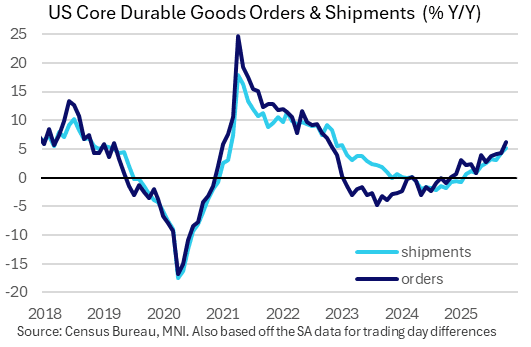

- MNI US DATA: Core Durable Goods Momentum Picking Up

- MNI US-CHINA: USTR Defers Chip Tariffs In Effort To Maintain Recent Sino-US Calm

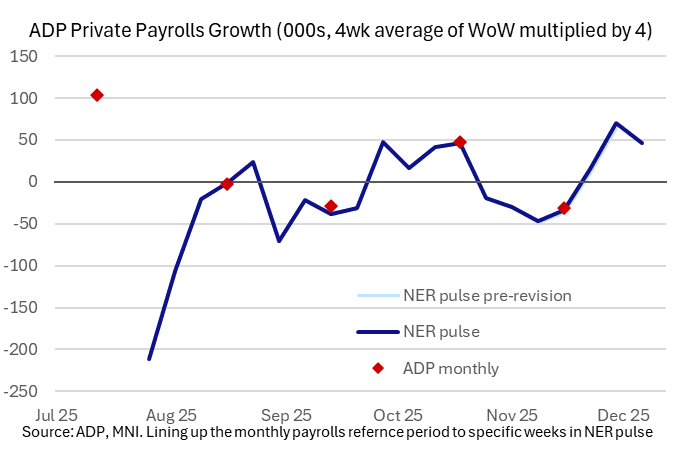

- MNI US DATA: Weekly ADP Continues To Hint At Return To Limited Job Creation

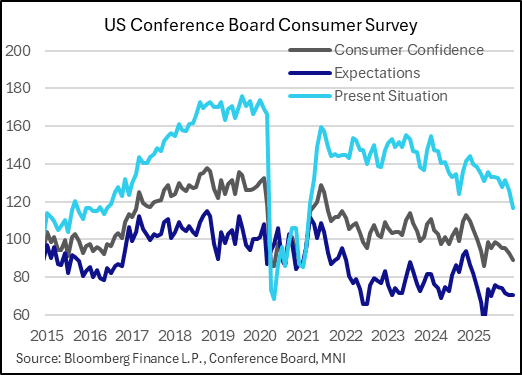

- MNI US DATA: Weak Conference Board Consumer Survey Bodes Ill For Labor Market

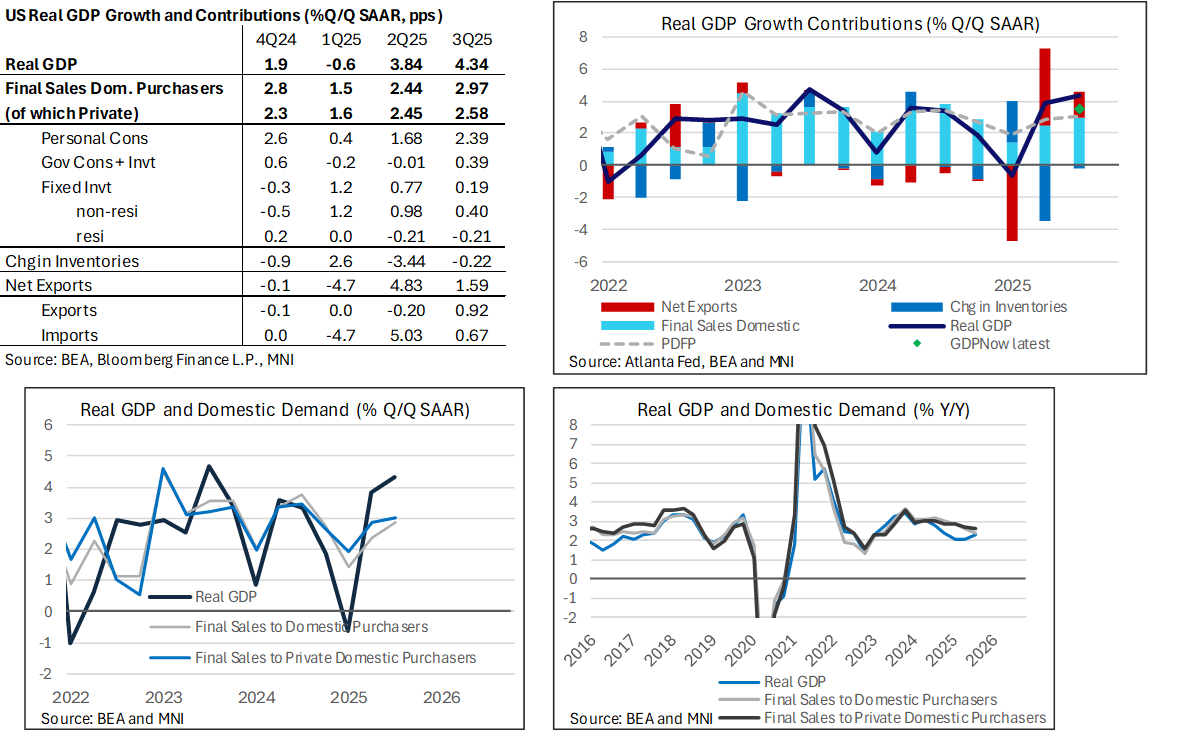

- MNI US DATA: Consumption Drives Surprisingly Strong Q3 GDP With Help From Trade

NEWS

WSJ: "U.S. Moves Troops and Additional Special- Operations Aircraft Into Caribbean -- The U.S. moved a large number of special-operations aircraft and multiple cargo planes filled with troops and equipment into the Caribbean area this week, giving the U.S. additional options for possible military action in the region, according to U.S. officials and open source flight-tracking data."

MNI US-CHINA: USTR Defers Chip Tariffs In Effort To Maintain Recent Sino-US Calm

The office of US Trade Representative Jamieson Greer has confirmed in a filing to the Federal Register that, under Section 301 of the Trade Act of 1974, the imposition of additional tariffs on the import of Chinese semiconductors is appropriate. The document does not confirm the level of tariffs, but does say the additional tariffs will remain at zero until June 2027, at which point they will be imposed. In its reasoning, the filing claims that "China’s targeting of the semiconductor industry for dominance is unreasonable and burdens or restricts U.S. commerce and thus is actionable."

MNI POLITICAL RISK: Greenland Issue Re-Emerges As Threat To US-EU Relations

Earlier on 23 Dec, French President Emmanuel Macron posted (in English) on X, "In Nuuk, I reaffirmed France’s unwavering support for the sovereignty and territorial integrity of Denmark and Greenland. Greenland belongs to its people. Denmark stands as its guarantor. I join my voice to that of Europeans in expressing our full solidarity." The French president's call for European solidarity comes amid a re-escalation in transatlantic tensions between the Trump administration and the gov't of Denmark over the future of Greenland.

US TSYS

MNI US TSYS: Strong Data Weighs on Rate Cut Pricing, Curves Twist Flatter

- Treasuries look to finish mixed, curves twist flatter (2s10s -1.733 at 63.666) with 2s-10s weaker vs. modest gains in Bonds. Futures gapped lower after stronger than expected economic data while projected rate cut pricing in-turn consolidated with the June '26 now the first FOMC date to price in a 25bp cut.

- Real GDP growth was clearly stronger than most expected in the “initial” Q3 release, with the largest upside coming from personal consumption but also with a larger than expected boost from net exports that was only partly offset by a larger than expected drag from inventories. Real GDP increased a strong 4.3% whilst PDFP was also solid at 3.0%.

- ADP employment saw an average week-on-week increase of 11.5k in the four weeks to Dec 6, a moderation after the upward revised 17.5k (initial 16.25k) in the four weeks to Nov 29.

- Durable goods orders fell more than expected in October, but as is often the case the headline reading was distorted by aircraft orders. Not only did core readings beat expectations, but priors were revised up, making for an overall solid report. In this shutdown-delayed report, headline durables orders fell 2.2% M/M (1.5% fall expected, but prior rev up 0.2pp to 0.7%), but fared better ex-transportation (up 0.2% vs the 0.3% expected, with an upward 0.1pp revision to prior to 0.7%).

- Information Technology and Communication Services sector shares continued to lead advances in the second half, chip makers buoyed after the Trump administration announced a tariff delay on China until 2027.

- Markets close early (1315ET) Wednesday for Christmas eve, re-open for electronic trade Thursday evening for Friday's order of business. Tomorrow's shortened session sees MBA Mortgage Applications (0700ET) and Weekly Jobless Claims (0830ET). Followed by US Treasury supply: US Tsy 4W & 8W bill auctions (1000ET), $44B 7Y Note (91282CPQ8) & 17W bill auctions at 1130ET.

OVERNIGHT DATA

MNI US DATA: Weak Conference Board Consumer Survey Bodes Ill For Labor Market

The December Conference Board consumer survey was weak, echoing its UMichigan counterpart in portraying a deterioration in sentiment at the close of 2025. While the Expectations index was steady at 70.7 (having been upwardly revised from 63.2), the Composite fell to an 8-month low 89.1 from 92.9 prior (upward rev from 88.7) as consumers' Present Situation fell to 116.8 from 126.3 (downwardly revised from 126.9). That's easily the weakest reading for the latter since February 2021, and outside of the pandemic, since 2016.

MNI US DATA: Consumption Drives Surprisingly Strong Q3 GDP With Help From Trade

Real GDP growth was clearly stronger than most expected in the “initial” Q3 release, with the largest upside coming from personal consumption but also with a larger than expected boost from net exports that was only partly offset by a larger than expected drag from inventories. Real GDP increased a strong 4.3% whilst PDFP was also solid at 3.0%.

- Real GDP was stronger than most expected in the first look at Q3 data, rising 4.3% annualized vs 3.5% in Atlanta Fed’s GDPNow and 3.3% for Bloomberg consensus. That said, the Dallas Fed’s weekly economic index had been pointing to a 4+% increase. Personal consumption saw an impressive beat at 3.5%, considering September PCE data released on Dec 5 had implied a 2.7% increase, which unsurprisingly had fed into both GDPNow and consensus. It saw PCE add 2.4pp to annualized GDP growth vs the 1.84pp estimated by GDPNow.

MNI US DATA: Core Durable Goods Momentum Picking Up

Durable goods orders fell more than expected in October, but as is often the case the headline reading was distorted by aircraft orders. Not only did core readings beat expectations, but priors were revised up, making for an overall solid report. In this shutdown-delayed report, headline durables orders fell 2.2% M/M (1.5% fall expected, but prior rev up 0.2pp to 0.7%), but fared better ex-transportation (up 0.2% vs the 0.3% expected, with an upward 0.1pp revision to prior to 0.7%).

- The key category though is nondefense capital goods ex-aircraft orders, which rose 0.5% M/M after 1.1% (which was an upward rev from 0.9%), note that the volatile categories of nondefense aircraft orders fell 20% (after -7%) and defense aircraft orders plunged 32% (after +34%). Core shipments rose 0.7% after 1.2%, beating expectations too. This left core orders on growth rates of 6.2% Y/Y and 8.4% 3M/3M, respectively 36-month and 7-month highs.

MNI US DATA: Weekly ADP Continues To Hint At Return To Limited Job Creation

ADP employment saw an average week-on-week increase of 11.5k in the four weeks to Dec 6, a moderation after the upward revised 17.5k (initial 16.25k) in the four weeks to Nov 29.

- Prior revisions were generally upward although they don’t materially change the recent story: there has been some improvement in the second half of November, which has since continued into December, after a return to negative -31k in the monthly ADP report (based off its reference period including the 12th of the month). The latest rate is equivalent to a 46k monthly increase as it starts to give a better idea of potential readings ahead of the December ADP report released on Jan 7.

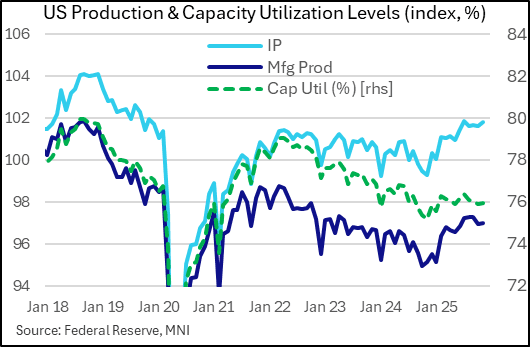

MNI US DATA: Flat Industrial Production Momentum, Though Prospects Look Better

Industrial production barely grew on net over the October/November period vs September, with a 0.12% 2-month rise implied by the Oct (-0.06% M/M) and Nov (+0.17%) readings. The broader picture is that while core durable goods orders suggest a potential pickup ahead, especially given the bounceback in November, actual industrial production momentum has shown signs of slowing through the first 2 months of Q4, with manufacturing showing notable weakness.

- Capacity utilization was steady over the 2-month period (76.0%). The monthly reports were, unusually, combined and delayed due to the government shutdown, as the Fed was unable to get some of the underlying data necessary to produce the production indices. But overall, unlike the October durable goods report which looked quite solid and suggest a pickup lies ahead, this report offered a more cautionary portrayal.

MNI US DATA: Redbook Sales Jump In Key Week, Point To Solid End To Retail Year

Retail sales remain on pace to post a joint 8-month high growth pace in December, per the Johnson Redbook Retail Sales Index which rose 7.2% in the week ending Dec 20 (6.2% prior). This brought month-to-date gains to 6.4% (retailers target a 6.5% rise), which would be a pickup from the 6.2% month-to-date pace through the prior week (and match November's 6.4% gain). While like most retail sales series this is in nominal terms, it suggests continued strong control group sales through year-end (after Q3's real goods consumption growth of 3.1% Q/Q SAAR).

MARKETS SNAPSHOT

DJIA up 77.59 points (0.16%) at 48440.18

S&P E-Mini Future up 30.75 points (0.44%) at 6960.75

Nasdaq up 125.3 points (0.5%) at 23554.75

US 10-Yr yield is up 0.2 bps at 4.1648%

US Mar 10-Yr futures are down 1/32 at 112-10

EURUSD up 0.0032 (0.27%) at 1.1794

USDJPY down 0.81 (-0.52%) at 156.24

WTI Crude Oil (front-month) up $0.46 (0.79%) at $58.47

Gold is up $47.51 (1.07%) at $4490.45

European bourses closing levels:

EuroStoxx 50 up 5.59 points (0.1%) at 5749.28

FTSE 100 up 23.25 points (0.24%) at 9889.22

German DAX up 56.09 points (0.23%) at 24340.06

French CAC 40 down 17.22 points (-0.21%) at 8103.85

US TREASURY FUTURES CLOSE

Curve update:

3M10Y +2.306, 56.089(L: 50.031 / H: 57.555)

2Y10Y -1.928, 63.471 (L: 62.449 / H: 65.974)

2Y30Y -3.043, 129.72 (L: 128.393 / H: 133.397)

5Y30Y -3.035, 109.161 (L: 108.661 / H: 112.593)

Current futures levels:

Mar 2-Yr futures down 1.75/32 at 104-9.375 (L: 104-07.5 / H: 104-11.75)

Mar 5-Yr futures down 2.5/32 at 109-5 (L: 109-00 / H: 109-10)

Mar 10-Yr futures down 1.5/32 at 112-9.5 (L: 112-01.5 / H: 112-17)

Mar 30-Yr futures up 7/32 at 115-11 (L: 114-24 / H: 115-20)

Mar Ultra futures up 10/32 at 118-2 (L: 117-11 / H: 118-14)

MNI US 10YR FUTURE TECHS: (H6) Opens Gap With Resistance

- RES 4: 113-09 76.4% retracement of the Nov 25 - Dec 10 bear leg

- RES 3: 113-07 H igh Dec 3

- RES 2: 112-31/113-00+ High Dec 18 / 61.8% of Nov 25 - Dec 10 leg

- RES 1: 112-21+ 50-day EMA

- PRICE: 112-07 @ 15:57 GMT Dec 23

- SUP 1: 112-01+/111-29 Low Dec 23 / 10 and the bear trigger

- SUP 2: 111-19 1.236 proj of the Oct 17 - Nov 5 - 25 price swing

- SUP 3: 111-11 1.382 proj of the Oct 17 - Nov 5 - 25 price swing

- SUP 4: 111-00 Round number support

Treasuries fell sharply on the back of the stronger-than-expected US GDP print, opening a sizeable gap with key short-term resistance into 112-31, the Dec 18 high. Renewed weakness here would refocus attention on 111-29, the Dec 10 low and a key short-term support. A breach of this support resumes the bear cycle that started Oct 17. Instead, clearance higher would signal scope for a stronger corrective phase and open 113-00 initially, a Fibonacci retracement point.

SOFR FUTURES CLOSE

Current White pack (Mar 26-Dec 26):

Mar 26 -0.025 at 96.460

Jun 26 -0.035 at 96.655

Sep 26 -0.040 at 96.795

Dec 26 -0.040 at 96.840

Red Pack (Mar 27-Dec 27) -0.035 to -0.02

Green Pack (Mar 28-Dec 28) -0.02 to -0.01

Blue Pack (Mar 29-Dec 29) -0.01 to -0.005

Gold Pack (Mar 30-Dec 30) steadysteady0 to +0.005

REFERENCE RATES

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 3.68% (+0.02), volume: $3.253T

- Broad General Collateral Rate (BGCR): 3.66% (+0.03), volume: $1.326T

- Tri-Party General Collateral Rate (TCR): 3.66% (+0.03), volume: $1.292T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 3.64% (+0.00), volume: $87B

- Daily Overnight Bank Funding Rate: 3.64% (+0.00), volume: $171B

FED Reverse Repo Operation

RRP usage rebounds to $5.893B with 14 counterparties this afternoon vs. Monday's $1.523B. Compares to December 12 low of $0.838B (lowest level since mid-March 2021); this years highest excess liquidity measure: $460.731B on June 30.

MNI BONDS: EGBs-GILTS CASH CLOSE: Pre-Holiday Bull Flattening

European curves bull flattened Tuesday ahead of the holiday period.

- Bunds modestly outperformed Gilts, with some spillover from late Monday's dovishly-received comments on rate hike prospects from ECB's Schnabel, as well as an overnight bounce in JGBs from oversold conditions.

- The rally was interrupted in early afternoon by stronger than expected US Q3 GDP data, but a subsequent recovery into the cash close would ensure bull flattening on the day.

- Periphery/semi-core EGB spreads tightened slightly, as European stocks rallied to/near historic highs in a broader risk-on move.

- A reminder that Wednesday sees a shortened session for Gilts and options/futures contracts and an EGB cash holiday due to Christmas Eve, with the 25th and 26th full day holidays. Normal trade resumes on Monday.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 0.6bps at 2.142%, 5-Yr is down 2.1bps at 2.464%, 10-Yr is down 3.5bps at 2.862%, and 30-Yr is down 4.4bps at 3.488%.

- UK: The 2-Yr yield is down 0.3bps at 3.742%, 5-Yr is down 1bps at 3.966%, 10-Yr is down 2.7bps at 4.509%, and 30-Yr is down 3.3bps at 5.238%.

- Italian BTP spread down 1.1bps at 69.1bps / French OAT down 1.1bps at 70.4bps

MNI FOREX: US GDP Prompts Limited Dollar Rebound

- After steadily weakening from the open this week, a much firmer-than-expected US GDP print has stalled the greenback’s downside momentum. Following the USD index printing a fresh pullback low at 97.85 in early trade, the data has sparked only a moderate rebound (owing to some question marks over the release), with the DXY operating around 98.05 as we approach the APAC crossover. Dollar dynamics did produce a notable pullback for spot gold, which had a near $70 pullback to $4,430/oz.

- Across the G10, it was JPY volatility that stole the show once again. Both the finance minister comments on potential intervention and a responsible tone from PM Takaichi provided a supportive backdrop early Tuesday. USDJPY extended its pull lower this week to erase the entirety of the post BOJ rally from Friday. This resulted in session lows of 155.65, before recovering around 85 pips following the US growth figures. Short-term technical parameters are well defined at 154.40 (50-day EMA) and 157.89 (key resistance and bull trigger).

- Continued positive sentiment for equity markets has underpinned solid gains for both AUD and NZD, which top the G10 leaderboard. AUDUSD has traded to within 7 pips of the key 0.6707 level, the Sep 17 high.

- Elsewhere, USDCAD also gathered downside momentum this morning. A break of multiple daily lows at 1.3727 is noteworthy, placing USDCAD at the lowest level since late July with prints below 1.3700. Overall, USDCAD has now extended its one-month selloff to around 3%, with the breach of the bull channel in early December exacerbating declines.

- Both EURUSD and GBPUSD had attempts at breaking the 1.18 and 1.35 levels respectively, although topside momentum certainly dissipated across the US session.

- US jobless claims are scheduled tomorrow, although market liquidity is likely to be heavily impacted by the upcoming holiday period.

WEDNESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 24/12/2025 | 1200/0700 | ** | MBA Weekly Applications Index | |

| 24/12/2025 | 1330/0830 | *** | Jobless Claims | |

| 24/12/2025 | 1530/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 24/12/2025 | 1530/1030 | ** | US DOE Petroleum Supply | |

| 24/12/2025 | 1630/1130 | ** | US Treasury Auction Result for 7 Year Note | |

| 24/12/2025 | 1700/1200 | ** | Natural Gas Stocks |