MNI ASIA OPEN: Massive Fed Fund Sales, Focus on Jobs, SCOTUS

EXECUTIVE SUMMARY

- MNI FED: Richmond's Barkin: Economy Resilient, Policy Now Within Neutral Ranges

- MNI TARIFFS: US Supreme Court Could Rule On Tariff Legality On Friday

- MNI POLITICAL RISK: Congressional Briefings On Venezuela Op. Set For Weds. Morning

- MNI US: Majority Whip Confirms Death Of GOP California Rep. LaMalfa

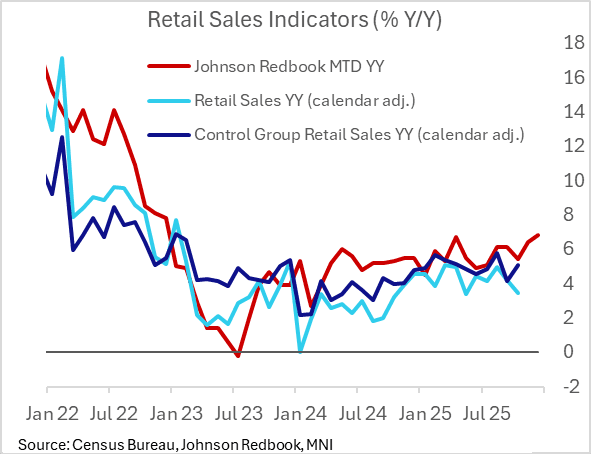

- MNI US DATA: Best Redbook Growth In 3 Years Points To Solid End-2025 Retail Sales

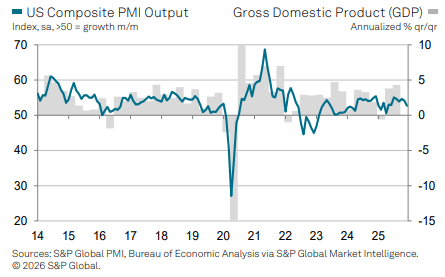

- MNI US DATA: Final Service PMI Trimmed In Dec, Input Cost Inflation Sting Softened

US

MNI FED: Richmond's Barkin: Economy Resilient, Policy Now Within Neutral Ranges

Richmond Fed President Barkin (not a 2026 FOMC voter but votes in 2027)'s speech on the economic outlook Tuesday is typically guarded on the expected path of policy rates. We would still expect Barkin is in line with the FOMC 2026 median implying 1 rate cut this year though he's not in any rush to ease. Barkin takes a measured approach in his speech, noting that after some "insurance" cuts, policy is close to neutral, with the dual mandate variables finely balanced.

NEWS

MNI TARIFFS: US Supreme Court Could Rule On Tariff Legality On Friday

It's possible that the Supreme Court announces a ruling on the legality of the White House's IEEPA tariffs on Friday Jan 9 (per the Court's updated calendar here they have set Friday as an "Opinion Day"; the justices sit at 10am), but it's not certain given that they do not announce in advance what opinions that they are providing.

- However it wouldn't be a big surprise if they did announce their ruling Friday. Most expectations have been that the ruling will be announced either January or February, and there is obviously some urgency in deciding the case given the subject matter. Arguments were heard on Nov 5.

MNI POLITICAL RISK: Congressional Briefings On Venezuela Op. Set For Weds. Morning

Briana Reilly at Punchbowl News posts on X: "Full House briefing on Venezuela operation scheduled for 11:30am [16:30 GMT] tomorrow, sources tell Ally Mutnick and me. Will follow a 10am [15:00 GMT] all-senators briefing."

MNI US: Trump Speaks To House GOP Retreat

President Donald Trump has just begun speaking to the House Republican retreat taking place today in Washington, D.C., Livestream here. These will be the first direct comments from the president to any members of Congress since the operation to capture Venezuelan President Nicolás Maduro over the weekend.

MNI US: Majority Whip Confirms Death Of GOP California Rep. LaMalfa

House Majority Whip Tom Emmer (R-MN) has confirmed via X the death at age 65 of Republican Representative Doug LaMalfa, who represented California's 1st congressional district since 2013. LaMalfa's death means the House is now split 218-213 in favour of the Republicans, with four vacancies. A special run-off election takes place on 31 January for Texas's 18th congressional district. The November special election resulted in two Democrats making the run-off in the heavily blue seat, meaning the Democratic total in the House will rise to 214 as soon as the new representative is sworn in.

Speaking to NBC News on 5 January, Trump said, "We need Greenland for national security, and that includes Europe...You know I'm very loyal to Europe. We need it for national security, right now…I think that Greenland is very important for the national security of the United States, Europe, and other parts of the free world." He said that there was “no timeline” for the US taking action, but that he is “very serious” about it.

US TSYS

MNI US TSYS: Treasuries Pare Early Losses, Eye on Employ Data, SCOTUS on Tariffs Fri

- Treasuries are running mildly weaker after the bell, well off morning lows after massive selling in Jan'26 Fed Funds (-450k, total DV01near $19M) in the first half - potentially tied to positioning ahead of SCOTUS opinion day Friday on Trump tariffs.

- In FX, this has translated to further USD strength, prompting a continued reversal of yesterday's weakness. We noted at the time the low levels of participation in the EURUSD, GBPUSD rallies and that's helping both pairs show back through 1.17 and 1.35 respectively. Others looks far more resilient, with AUDUSD remaining higher on the session.

- Currently, TYH6 trades 112-12 (-1.5) vs. 112-06 low / 112-14 high; Curves currently mixed: 2s10s at 70.386 -.256, 5s30s -.091 at 114.438.

- Treasuries are in consolidation mode and continue to trade above key support at 111-29, the Dec 10 low and bear trigger. The trend remains bearish and a break of 111-29 would confirm a resumption of the bear cycle. This would open 111-19 initially, a Fibonacci projection.

- Services PMI: 52.5 in Dec final (flash and cons 52.9) after 54.1 in Nov; Composite PMI: 52.7 in Dec final (flash 53.0) after 54.2 in Nov; the downward revision for services is in contract to the unrevised final manufacturing reading reported last week.

- It's possible that the Supreme Court announces a ruling on the legality of the White House's IEEPA tariffs on Friday Jan 9 (per the Court's updated calendar here they have set Friday as an "Opinion Day"; the justices sit at 10am), but it's not certain given that they do not announce in advance what opinions that they are providing.

- Looking ahead: ADP private employ & JOLTS data tomorrow, NFP Friday.

OVERNIGHT DATA

MNI US DATA: Final Service PMI Trimmed In Dec, Input Cost Inflation Sting Softened

The final S&P Global US services PMI was revised lower for December for a joint low with June and last lower in April after wide-ranging tariff announcements at the time. New orders saw their weakest increase in over eighteen months (chiming with the 20-month low in the flash release) whilst services cost inflation was revised a little softer but still clearly very strong (operating expenses increased by their most since last May vs the steepest in over three years in the flash). The composite activity index points to downward momentum in Q4 real GDP growth after the strong 4.3% annualized in Q3.

- Services PMI: 52.5 in Dec final (flash and cons 52.9) after 54.1 in Nov.

- Composite PMI: 52.7 in Dec final (flash 53.0) after 54.2 in Nov.

- The downward revision for services is in contract to the unrevised final manufacturing reading reported last week.

MNI US DATA: Best Redbook Growth In 3 Years Points To Solid End-2025 Retail Sales

Retail sales rose by 6.8% Y/Y in December per the Johnson Redbook index, following a 7.1% Y/Y increase in the week ending Jan 3 (which marks the end of the retail month). This was above the 6.5% targeted by retailers and the best month in Y/Y growth terms since December 2022 (all figures, like the Census Bureau's "official" retail series, are in nominal terms).

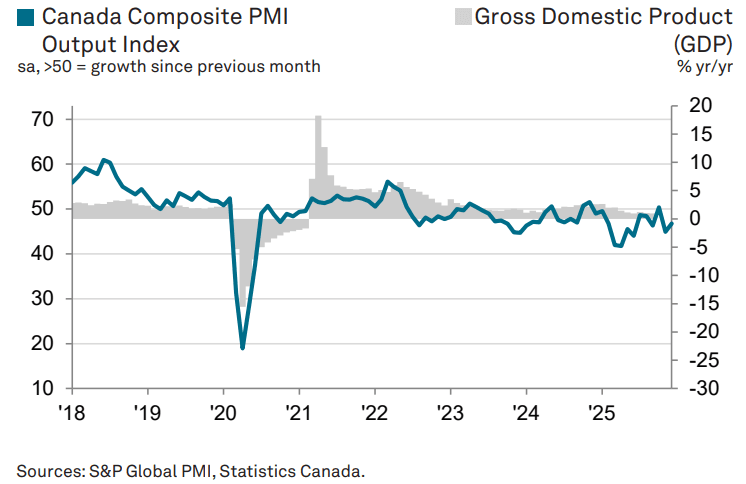

MNI CANADA DATA: Still-Weak Composite PMIs Point To Soft Q4 Growth

Canadian PMIs picked up in December, with Services up to 46.5 (44.3 prior) and the Composite up to 46.7 (44.9 prior). Despite the improvements, the PMIs were below the 50 level for a 12th month in the last 13 (the Manufacturing reading out earlier showed an 11th consecutive sub-50 month at 48.6, up 0.2 from prior), suggesting a continued deterioration in business activity. The brief jump above 50 in October looks like a false dawn, with Canadian economic activity remaining weak in as private sector actors grapple with the US-Canada trade conflict.

MARKETS SNAPSHOT

Key market levels of markets in late NY trade:

DJIA up 482.6 points (0.99%) at 49459.28

S&P E-Mini Future up 45.25 points (0.65%) at 6988.5

Nasdaq up 157.2 points (0.7%) at 23549.44

US 10-Yr yield is up 0.4 bps at 4.1652%

US Mar 10-Yr futures are steady at at 112-13.5 at 112-13.5

EURUSD down 0.0033 (-0.28%) at 1.1689

USDJPY up 0.22 (0.14%) at 156.6

WTI Crude Oil (front-month) down $1.32 (-2.26%) at $57.01

Gold is up $45.57 (1.02%) at $4494.69

European bourses closing levels:

EuroStoxx 50 up 8.1 points (0.14%) at 5931.79

FTSE 100 up 118.16 points (1.18%) at 10122.73

German DAX up 23.51 points (0.09%) at 24892.2

French CAC 40 up 25.93 points (0.32%) at 8237.43

US TREASURY FUTURES CLOSE

Curve update:

3M10Y +1.154, 56.906 (L: 54.279 / H: 58.886)

2Y10Y -0.238, 70.404 (L: 69.721 / H: 72.156)

2Y30Y -0.523, 139.166 (L: 138.439 / H: 141.63)

5Y30Y +0.131, 114.478 (L: 113.837 / H: 115.913)

Current futures levels:

Mar 2-Yr futures down 0.5/32 at 104-12.75 (L: 104-11.125 / H: 104-13.375)

Mar 5-Yr futures steady at at 109-9.5 (L: 109-05 / H: 109-10)

Mar 10-Yr futures down 0.5/32 at 112-13 (L: 112-06 / H: 112-14)

Mar 30-Yr futures down 1/32 at 115-9 (L: 114-26 / H: 115-12)

Mar Ultra futures steady at at 117-18 (L: 116-30 / H: 117-19)

MNI US 10YR FUTURE TECHS: (H6) Support Remains Exposed

- RES 4: 113-00+ 61.8% retracement of the Nov 25 - Dec 10 bear leg

- RES 3: 112-31 High Dec 18 and key short-term resistance

- RES 2: 112-25+ High Dec 30 / 31

- RES 1: 112-20 50 -day EMA

- PRICE: 112-09 @ 10:52 GMT Jan 6

- SUP 1: 112-01+/111-29 Low Dec 23 / 10 and the bear trigger

- SUP 2: 111-19 1.236 proj of the Oct 17 - Nov 5 - 25 price swing

- SUP 3: 111-11 1.382 proj of the Oct 17 - Nov 5 - 25 price swing

- SUP 4: 111-00 Round number support

Treasuries are in consolidation mode and continue to trade above key support at 111-29, the Dec 10 low and bear trigger. The trend remains bearish and a break of 111-29 would confirm a resumption of the bear cycle. This would open 111-19 initially, a Fibonacci projection. Key short-term resistance is at 112-31, the Dec 18 high, where a break would undermine a bear theme and signal scope for a stronger recovery instead.

SOFR FUTURES CLOSE

Current White pack (Mar 26-Dec 26):

Mar 26 -0.020 at 96.465

Jun 26 -0.030 at 96.670

Sep 26 -0.020 at 96.835

Dec 26 -0.010 at 96.895

Red Pack (Mar 27-Dec 27) -0.005 to +0.010

Green Pack (Mar 28-Dec 28) +0.010 to +0.015

Blue Pack (Mar 29-Dec 29) +0.010 to +0.015

Gold Pack (Mar 30-Dec 30) +0.010 to +0.015

REFERENCE RATES

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 3.70% (-0.05), volume: $3.441T

- Broad General Collateral Rate (BGCR): 3.66% (-0.04), volume: $1.348T

- Tri-Party General Collateral Rate (TCR): 3.66% (-0.04), volume: $1.313T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 3.64% (+0.00), volume: $92B

- Daily Overnight Bank Funding Rate: 3.64% (+0.00), volume: $178B

FED Reverse Repo Operation

RRP usage recedes to $2.582B with 10 counterparties this afternoon vs. $6.485B Monday. Compares to December 12 low of $0.838B (lowest level since mid-March 2021); this years highest excess liquidity measure: $460.731B on June 30.

MNI PIPELINE: Corporate Bond Update: $56.25B Total to Price, Third Largest on Record

$56.25B to Price Tuesday after $57.85B priced Monday, $114.1B total so far. Not unusual to see the backlog of borrowers after the holidays, as well as getting ahead of earnings blackout. The next earnings cycle kicks off in earnest next week with Bank of NY Mellon, JPM reporting on Tuesday January 13, Bank of America, Wells Fargo and Citigroup on Wednesday, Goldman Sachs, Blackrock and Morgan Stanley on Thursday.

- Date $MM Issuer (Priced *, Launch #)

- 01/06 $6B #Orange $750M 3Y +50, $1.25B 5Y +70, $1.5B 7Y +85, $2B 10Y +95, $500M 30Y +100

- 01/06 $6B #Israel $2.25B 5Y +90, $2B 10Y +100, $1.75B 30Y +125

- 01/06 $6B *EIB 5Y SOFR+32

- 01/06 $4.5B #Broadcom $750M 5Y +60, $1.25B 7Y +70, $1.25B 10Y +78, $1.25B 30Y +88

- 01/06 $3.5B *ADB 10Y SOFR+45

- 01/06 $3.5B #TotalEnergies Capital $1.5B 5Y +53, $1.25B 7Y +63, $750M 10Y +68

- 01/06 $3.5B #Kexim $1.25B 3Y +23, $500M 3Y SOFR+40, $1.25B 5Y +26, $500M 10Y +30

- 01/06 $3.3B #BPCE $1B 6NC5 +105, $1.5B 11NC10 +125, $800M 21NC20 +155

- 01/06 $2.5B #Standard Chartered $1B 4NC3 +77, $500M 4NC3 SOFR+92, $1B 11NC10 +107

- 01/06 $2.5B #TD Bank $1B 2Y +45, $600M 2Y SOFR+58, $900M 5Y +70 (drops 5Y SOFR leg)

- 01/06 $2.5B #Nat'l Bank of Australia $650M 3Y +35, $600M 3Y SOFR+53, $500M 5Y +45, $750M 5Y SOFR+68

- 01/06 $2B #American Honda $700M 3Y +62, $30M 3Y SOFR+78, $500M 5Y +77, $500M 10Y +95

- 01/06 $1.75B Charter Communications 7Y, 10Y guidance TBA

- 01/06 $1.75B #AERCAP $900M 3Y +70, $850M 7Y +92

- 01/06 $800M #Simon Property 5Y +65

- 01/06 $750M #HPS Corp $350M +3Y +170, $400M +5Y +200

- 01/06 $750M *F&G Global Funding 3Y +97

- 01/06 $700M *Principle Life 5Y +75

- 01/06 $700M #CIBC 60.5NC5.5 6.5%

- 01/06 $650M #Corebridge Global 5Y +85

- 01/06 $600M #Northwestern Mutual 5Y +58

- 01/06 $500M Mitsubishi HC Finance AM 5Y +85

- 01/06 $500M *DBJ 10Y SOFR+61

- 01/06 $500M #Penske Trucking 5Y +85

- 01/06 $500M #CNH Industrial +5Y +85

MNI BONDS: EGBs-GILTS CASH CLOSE: Yields Fall Again As Data Come In On Dovish Side

European yields fell for a second consecutive session Tuesday, with some moderation in Eurozone inflation at end-2025.

- Softer-than-expected German state-level/national inflation helped Bunds rally over the course of the session, with Gilts largely following suit with no major UK-specific macro/headline drivers on the day.

- The short-end/belly led gains on a higher probability of ECB cuts priced by end-2026.

- Other data were also accommodating to European rates. French HICP was broadly in line but CPI was slightly weaker than expected. Final December PMIs were on the weak side too, with the Eurozone composite revised down 0.4 points to 51.5, and the UK's down 0.7 to 51.4.

- Periphery / semi-core EGB spreads were little changed. OAT spreads notably rose vs falls elsewhere, with French Finance Minister Lescure saying the fiscal deficit could come in higher than 5.4% of GDP this year.

- Looking ahead to Wednesday, with 2/3 of country reports in, we estimate some downside risks to the 2.0% Y/Y consensus for the Eurozone HICP reading (we get Dutch and Austrian readings before the EZ print, with Italy coming simultaneously with the Eurozone number).

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 2.7bps at 2.1%, 5-Yr is down 2.9bps at 2.424%, 10-Yr is down 2.8bps at 2.842%, and 30-Yr is down 2.7bps at 3.48%.

- UK: The 2-Yr yield is down 2.3bps at 3.697%, 5-Yr is down 2.3bps at 3.915%, 10-Yr is down 2.6bps at 4.48%, and 30-Yr is down 1.9bps at 5.227%.

- Italian BTP spread down 0.6bps at 69.3bps / French OAT up 0.5bps at 70.9bps

MNI FOREX: EUR Pressured by Soft Inflation, AUD Extends Advance Ahead of CPI

- The USD index has drifted higher on Tuesday, as markets appear lacking in conviction ahead of the important US ISM services and NFP data releases later in the week. Elsewhere, Euro weakness has been evident through the session on the back of softer-than-expected French and German inflation data releases, while higher beta currencies continue to react favourably to the stronger equity/commodity backdrop.

- Following the initial Eurozone inflation releases earlier in the session, EURUSD has been grinding steadily lower from the 1.1743 highs, consolidating back below 1.17 ahead of the APAC crossover. For EURAUD, the cross has extended its break below support at 1.7462, continuing to trade at the lowest level since May, signalling scope for a more protracted selloff towards a key downside target at 1.7248, the May 2025 low.

- AUDUSD made fresh cycle highs at 0.6739 today, strengthening bullish conditions for the pair. Notable topside levels include 0.6795 and 0.6858 are the next chart points of note, projection levels of the Nov 21 - Dec 10 - 18 price swing. Notably, AUDNZD has risen to another cycle high during today’s session, as the cross now operates at the highest level since 2013. Australian CPI data is due on Wednesday.

- In EM, the South African Rand continues to standout, printing fresh cycle highs earlier in the session amid the ongoing constructive price action for metals. The trend condition in USDZAR remains firmly bearish, with sights on 16.2545 next, the 1.764 projection of the Sep 4 - Oct 9 - Nov 5 price swing.

- US ISM services will highlight Wednesday’s calendar, as markets also await Friday’s release of non-farm payrolls.

WEDNESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 07/01/2026 | 0700/0800 | ** | Retail Sales | |

| 07/01/2026 | 0745/0845 | ** | Consumer Sentiment | |

| 07/01/2026 | 0830/0930 | ** | S&P Global Final Eurozone Construction PMI | |

| 07/01/2026 | 0855/0955 | ** | Unemployment | |

| 07/01/2026 | 0900/1000 | *** | Bavaria CPI | |

| 07/01/2026 | 0900/1000 | *** | Baden Wuerttemberg CPI | |

| 07/01/2026 | 0930/0930 | ** | S&P Global/CIPS Construction PMI | |

| 07/01/2026 | 1000/1100 | *** | EZ HICP Flash | |

| 07/01/2026 | 1000/1100 | *** | EZ HICP Flash | |

| 07/01/2026 | 1000/1100 | *** | EZ HICP Flash | |

| 07/01/2026 | 1000/1000 | ** | Gilt Outright Auction Result | |

| 07/01/2026 | 1000/1100 | *** | EZ HICP Flash (2dp) | |

| 07/01/2026 | 1000/1100 | *** | Italy Flash Inflation | |

| 07/01/2026 | 1200/0700 | ** | MBA Weekly Applications Index | |

| 07/01/2026 | 1315/0815 | *** | ADP Employment Report | |

| 07/01/2026 | 1500/1000 | *** | ISM Non-Manufacturing Index | |

| 07/01/2026 | 1500/1000 | ** | Factory New Orders | |

| 07/01/2026 | 1500/1000 | ** | Factory New Orders | |

| 07/01/2026 | 1500/1000 | *** | JOLTS jobs opening level | |

| 07/01/2026 | 1500/1000 | *** | JOLTS quits Rate | |

| 07/01/2026 | 1500/1000 | * | Ivey PMI | |

| 07/01/2026 | 1500/1000 | ** | Durable Goods New Orders | |

| 07/01/2026 | 1500/1000 | ** | Durable Goods New Orders | |

| 07/01/2026 | 1530/1030 | ** | US DOE Petroleum Supply | |

| 07/01/2026 | 1530/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 07/01/2026 | 2110/1610 | Fed Vice Chair Michelle Bowman | ||

| 08/01/2026 | 2330/0830 | ** | average wages (p) | |

| 08/01/2026 | 0030/1130 | ** | Trade Balance |