PIPELINE: Corporate Bond Update: $56.25B Total to Price, Third Largest on Record

$56.25B to Price Tuesday after $57.85B priced Monday, $114.1B total so far. Not unusual to see the backlog of borrowers after the holidays, as well as getting ahead of earnings blackout. The next earnings cycle kicks off in earnest next week with Bank of NY Mellon, JPM reporting on Tuesday January 13, Bank of America, Wells Fargo and Citigroup on Wednesday, Goldman Sachs, Blackrock and Morgan Stanley on Thursday.

- Date $MM Issuer (Priced *, Launch #)

- 01/06 $6B #Orange $750M 3Y +50, $1.25B 5Y +70, $1.5B 7Y +85, $2B 10Y +95, $500M 30Y +100

- 01/06 $6B #Israel $2.25B 5Y +90, $2B 10Y +100, $1.75B 30Y +125

- 01/06 $6B *EIB 5Y SOFR+32

- 01/06 $4.5B #Broadcom $750M 5Y +60, $1.25B 7Y +70, $1.25B 10Y +78, $1.25B 30Y +88

- 01/06 $3.5B *ADB 10Y SOFR+45

- 01/06 $3.5B #TotalEnergies Capital $1.5B 5Y +53, $1.25B 7Y +63, $750M 10Y +68

- 01/06 $3.5B #Kexim $1.25B 3Y +23, $500M 3Y SOFR+40, $1.25B 5Y +26, $500M 10Y +30

- 01/06 $3.3B #BPCE $1B 6NC5 +105, $1.5B 11NC10 +125, $800M 21NC20 +155

- 01/06 $2.5B #Standard Chartered $1B 4NC3 +77, $500M 4NC3 SOFR+92, $1B 11NC10 +107

- 01/06 $2.5B #TD Bank $1B 2Y +45, $600M 2Y SOFR+58, $900M 5Y +70 (drops 5Y SOFR leg)

- 01/06 $2.5B #Nat'l Bank of Australia $650M 3Y +35, $600M 3Y SOFR+53, $500M 5Y +45, $750M 5Y SOFR+68

- 01/06 $2B #American Honda $700M 3Y +62, $30M 3Y SOFR+78, $500M 5Y +77, $500M 10Y +95

- 01/06 $1.75B Charter Communications 7Y, 10Y guidance TBA

- 01/06 $1.75B #AERCAP $900M 3Y +70, $850M 7Y +92

- 01/06 $800M #Simon Property 5Y +65

- 01/06 $750M #HPS Corp $350M +3Y +170, $400M +5Y +200

- 01/06 $750M *F&G Global Funding 3Y +97

- 01/06 $700M *Principle Life 5Y +75

- 01/06 $700M #CIBC 60.5NC5.5 6.5%

- 01/06 $650M #Corebridge Global 5Y +85

- 01/06 $600M #Northwestern Mutual 5Y +58

- 01/06 $500M Mitsubishi HC Finance AM 5Y +85

- 01/06 $500M *DBJ 10Y SOFR+61

- 01/06 $500M #Penske Trucking 5Y +85

- 01/06 $500M #CNH Industrial +5Y +85

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

USDCAD TECHS: Bull Channel Breakout

- RES 4: 1.4140 High Nov 5 and a key resistance

- RES 3: 1.4131 High Nov 21

- RES 2: 1.4051 High Nov 28

- RES 1: 1.3939/4016 Low Nov 28 / 20-day EMA

- PRICE: 1.3865 @ 16:35 GMT Dec 5

- SUP 1: 1.3853 Intraday low

- SUP 2: 1.3840 50.0% retracement of the Jun 16 - Nov 6 bull cycle

- SUP 3: 1.3812 Low Sep 23

- SUP 4: 1.3779 Low Sep 22

A bear theme in USDCAD remains intact and Friday’s strong sell-off reinforces a bear theme. The pair has breached an important support at 1.3942, the base of a bull channel drawn from the Jul 23 low. The break highlights a stronger bear cycle and signals scope for an extension towards 1.3840 next, a Fibonacci retracement point. Initial firm resistance to watch is 1.4016, 20-day EMA.

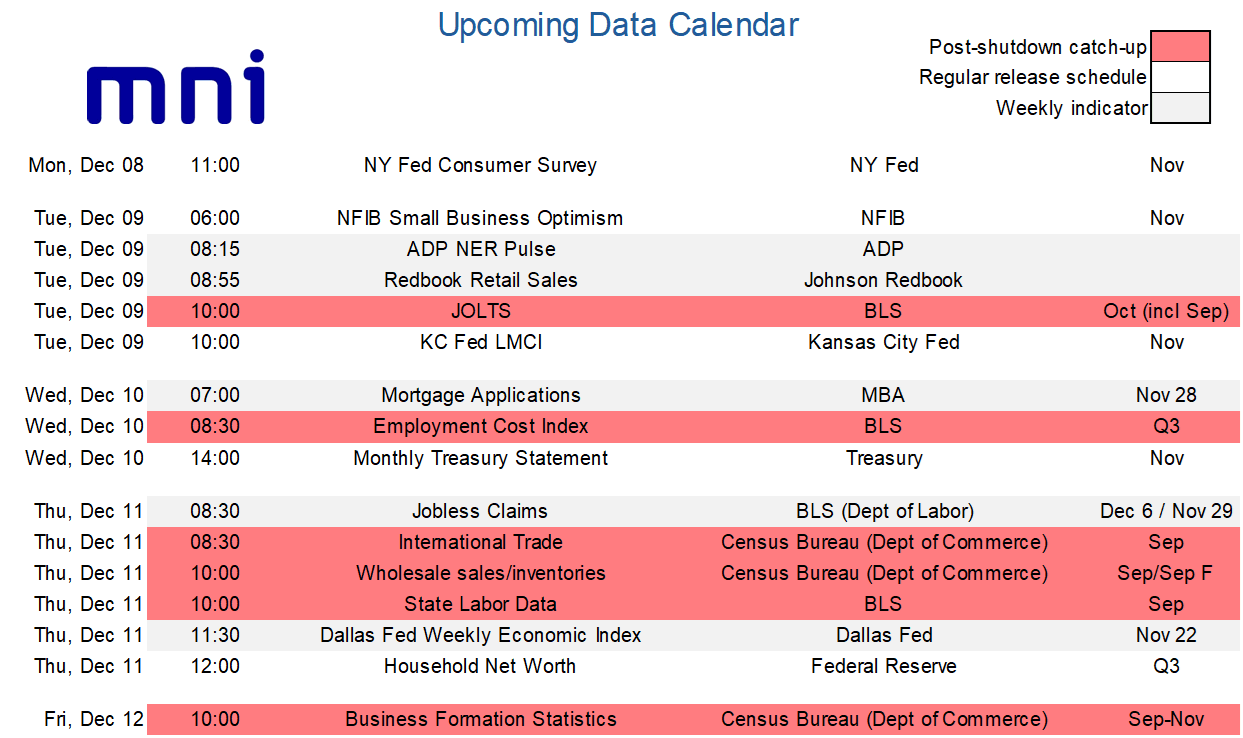

LOOK AHEAD: US Week Ahead: FOMC Decision Dominates, Post Shutdown Data Catch-Up

- Next week’s US calendar is dominated by the FOMC decision on Wednesday, with a third consecutive 25bp cut almost fully priced.

- Expect it to be a contentious meeting however, with many arguing for a pause not least whilst they’re still relatively in the dark on key official data releases following the government shutdown.

- Fed Chair Powell opted for a surprisingly hawkish tone at the late October press conference, highlighting a deeply divided committee on prospects for another cut in December.

- The “fog” had appeared to win out until NY Fed’s Williams, a senior permanent voter, gave unusually explicit guidance on still seeing room “for a further adjustment in the near term”. With no pushback from FOMC members or media briefings, it appears this message has approval from the core of the FOMC which should be enough to see a rate cut this month. The likely catalyst was the further increase in the unemployment rate to 4.44% back in September, although subsequent tracking suggests stabilization and jobless claims data don’t show any signs of deterioration.

- We’ll be looking for the number of hawkish dissents (we’d be surprised if anyone joins Miran dissenting for a 50bp cut) and expect a greater number to object to a cut in the 2025 dot plot, whilst the distribution of dots for 2026 should be in greater focus.

- As for the economic projections, we expect upward revisions to GDP growth but downward revisions to near-term core PCE inflation with tariff passthrough proving less severe than previously feared.

Aside from the Fed, we also receive two months worth of JOLTS data along with other delayed releases as the shutdown data backlog is slowly caught up.

AUDUSD TECHS: Bullish Impulsive Wave Extends

- RES 4: 0.6723 High Oct 21 ‘24

- RES 3: 0.6707 High Sep 17 and a key resistance

- RES 2: 0.6660 High Sep 18

- RES 1: 0.6649 Intraday high

- PRICE: 0.6630 @ 16:32 GMT Dec 5

- SUP 1: 0.6580/6533 High Nov 13 / 20-day EMA

- SUP 2: 0.6517 Low Nov 27

- SUP 3: 0.6466/21 Low Nov 26 / 21

- SUP 4: 0.6415 Low Aug 21 / 22 and a bear trigger

A strong impulsive bull wave in AUDUSD remains intact, having printed 10 consecutive sessions of higher highs. Recent gains have cleared a number of important short-term resistance points, strengthening a bull theme and highlighting scope for a continuation higher. Today’s rally has resulted in a breach of 0.6640, 76.4% of the Sep 17 - Nov 21 bear leg. This opens 0.6707, the Sep 17 high and key resistance. Key support to watch is at 0.6533, 20-day EMA.