MNI ASIA OPEN: Kevin Hassett Lead Contender for Fed Chair

EXECUTIVE SUMMARY

- MNI FED: Hassett A "Leading Contender" For Fed Chair: Washington Post

- MNI FED: Cleveland's Hammack: Close To Neutral Already, Important To "Wait And See"

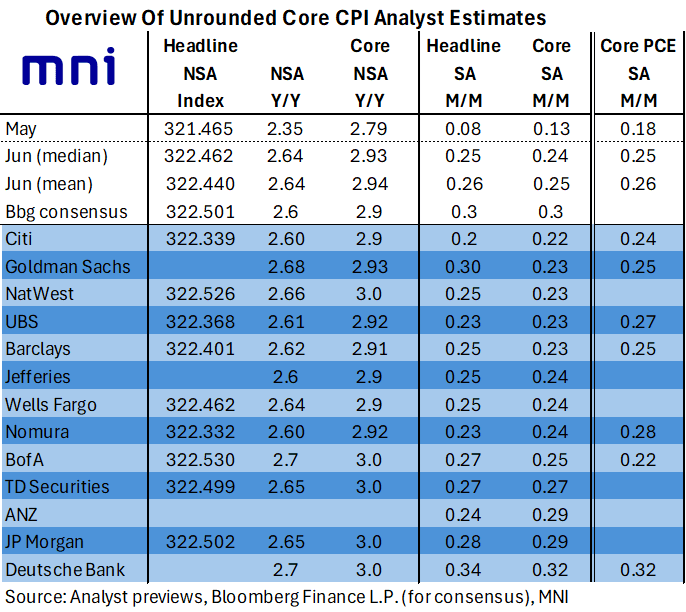

- MNI US INFLATION: MNI US CPI Preview: Passthrough Pressure Mounting

- MNI US OUTLOOK/OPINION: Analysts See Core CPI On Cusp Of 0.2% or 0.3% M/M In June

US

MNI FED: Hassett A "Leading Contender" For Fed Chair: Washington Post

The Washington Post reported Monday that National Economic Council director Kevin Hassett is "emerging as a leading contender to become the next chair of the Federal Reserve, according to people who have discussed the matter with White House officials". Appointing Hassett to succeed Chair Powell (whose term ends May 2026) would be considered a development that augurs support at the top of the Fed for lower rates: in recent weeks he's advocated for strong easing in the Fed funds rate.

MNI FED: Cleveland's Hammack: Close To Neutral Already, Important To "Wait And See"

Cleveland Fed President Hammack (non-2025 voter, hawk) reiterated her patient approach to any future policy easing in an interview with Fox Business Monday. Hammack had previously cited a wide range of estimates of neutral rates from 2% to 4.6%.

NEWS

MNI US OUTLOOK/OPINION: Analysts See Core CPI On Cusp Of 0.2% or 0.3% M/M In June

Ahead of tomorrow’s US CPI release, we note that the broad Bloomberg consensus looks for both core and headline CPI inflation at 0.3% M/M in June although unrounded estimates suggest a risk of rounding lower.

MNI US-RUSSIA: Trump Expected To Announce UKR Weapons Package, Endorse RU Sanctions

10:00 ET 15:00 BST: President Donald Trump will hold a (closed press) White House meeting with NATO SecGen Mark Rutte, where he is expected to finalise a new plan to arm Ukraine “that is expected to include offensive weapons,” per Axios. Later today, Trump is expected to make a 'major statement' on Russia. No timing has been released.

US TSYS

MNI US INFLATION: MNI US CPI Preview: Passthrough Pressure Mounting

We've just published our preview of the June CPI report - Download Full Report Here

- Consensus sees core CPI inflation at a seasonally adjusted 0.3% M/M in June on a rounded basis, but with sizeable risk of undershooting at 0.2% (MNI median unrounded estimate at 0.24% M/M /average 0.25%).

- This would mark an acceleration from 0.13% M/M in May, with core services ticking up and core goods more than reversing May’s unexpected M/M deflation. Headline CPI meanwhile is seen at 0.3% M/M or 0.25% M/M unrounded after 0.08% in May, amid a bounce in gasoline-driven energy prices.

MNI US TSYS: Tsys Hold Narrow Range Ahead June CPI Inflation Data

- Treasuries held a narrow range finishing near steady/mixed Monday, focus on Tuesday's June CPI inflation data and several Fed speakers ahead of Friday evening's policy blackout.

- Consensus sees core CPI inflation at a seasonally adjusted 0.3% M/M in June on a rounded basis, but with sizeable risk of undershooting at 0.2% (MNI median unrounded estimate at 0.24% M/M /average 0.25%).

- Unscheduled Fed speaker: Cleveland Fed President Hammack (non-2025 voter, hawk) reiterated her patient approach to any future policy easing in an interview with Fox Business Monday. Hammack had previously cited a wide range of estimates of neutral rates from 2% to 4.6%.

- Currently, the Sep'25 10Y contract trades +2 at 110-25 (110-20 low / 110-29.5 high), inside technicals: support at 110-17 (61.8% of the May 22 - Jul 1 bull leg); resistance above at 111-13+/111-28 (High Jul 10 / High Jul 3).

- The Washington Post reported Monday that National Economic Council director Kevin Hassett is "emerging as a leading contender to become the next chair of the Federal Reserve, according to people who have discussed the matter with White House officials".

- The latest earnings cycle with banks and financial stocks reporting tomorrow: Blackrock, JPMorgan Chase & Co, Wells Fargo & Co, Bank of New York Mellon, State Street Corp and Citigroup.

OVERNIGHT DATA

No US economic data or scheduled Fed speakers Monday, focus on CPI and PPI on Tuesday and Wednesday respectively.

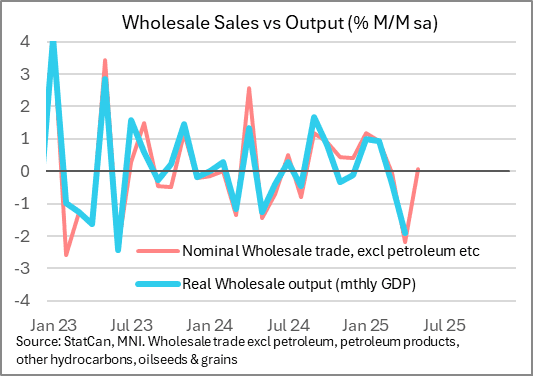

MNI CANADA DATA: Better-Than-Expected Wholesale Sales A Small Boost For May GDP

Wholesale sales rose 0.1% M/M in May (ex petroleum, products, other hydrocarbons, oilseed & grain), rising in 5 of 7 subsectors and marking a return to growth after two contractions. This was a better result than the -0.4% M/M seen in StatCan's advance estimate, and significantly better than the -2.2% in April (upward rev by 0.1pp).

MNI US 10YR FUTURE TECHS: (U5) Support Holds For Now

- RES 4: 112-23 High May 1 and key resistance

- RES 3: 112-15 61.8% retracement of the Apr 7 - 11 sell-off

- RES 2: 112-12+ High Jul 1 and a bull trigger

- RES 1: 111-13+/111-28 High Jul 10 / High Jul 3

- PRICE: 110-23 @ 1615 ET Jul 14

- SUP 1: 110-20+/17 Low Jul 14 / 61.8% of the May 22 - Jul 1 bull leg

- SUP 2: 110-10+ Low Jun 16

- SUP 3: 110-03 76.4% of the May 22 - Jul 1 bull leg

- SUP 4: 109-28 Low Jun 6 and 11

Treasury futures maintain a softer short-term tone and the contract is trading closer to its recent lows. Price has breached the 50-day EMA, at 110-31. This undermines a recent bull theme and exposes 110-17 next, a Fibonacci retracement point and a key support. Clearance of this price point would strengthen a bearish threat. Note that it also remains possible that the recent move down is a correction. Resistance to watch is at 111-13+, Jul 10 high.

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.31% (+0.00), volume: $2.754T

- Broad General Collateral Rate (BGCR): 4.30% (+0.00), volume: $1.121T

- Tri-Party General Collateral Rate (TCR): 4.30% (+0.00), volume: $1.094T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $103B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $265B

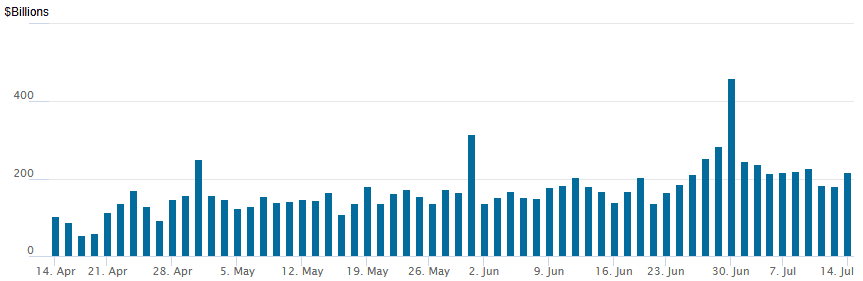

FED Reverse Repo Operation

RRP usage rises to $217.841B this afternoon from $181.637B Friday, total number of counterparties at 45. Usage had fallen to $54.772B on Wednesday, April 16 -- lowest level since April 2021 - compares to yesterday's (July 1) $460.731B highest usage since December 31.

MNI PIPELINE: Corporate Bond Update: Athene Global & Aircastle Launched

- Date $MM Issuer (Priced *, Launch #)

- 07/14 $850M #Athene Global 5Y +105

- 07/14 $650M #Aircastle 5Y +120

- Expected this week:

- 07/15 $500M Boots Group 7NC3 (includes GBP & EUR issuance) Investor calls

- 07/15 $1B Univision Communications 7NC3 9.5%a

- 07/15 $500M Macy's 8NC3

- 07/?? $1.5B Kioxia Holdings 5NC2, 8NC3

MNI BONDS: EGBs-GILTS CASH CLOSE: Curves Continue To Steepen, But Gilts Outperform

The previous week's rise in yields took a breather Monday, but curves continues to steepen.

- Yields fluctuated but resolved higher up in early trading, stemming from the weekend's threat of higher US tariffs on the EU and Mexico.

- Bund yields largely retained their early rise. However dovish comments from BoE Governor Bailey (noting potential for easier policy if the labour market deteriorates quicker than the Bank expects) and the soft REC labour market report helped Gilts outperform on the day.

- Core FI was bid into the European cash close, helped by a continued pullback in oil prices.

- 30Y German yields continued to march higher, to another fresh post-2011 high close, as fiscal concerns persisted.

- The UK curve bull steepened on the day, with Germany's twist steepening. Periphery / semi-core EGB spreads moved a little wider.

- On the calendar Tuesday: French PM Bayrou is set to unveil the main proposals of the 2026 state budget and we get the German ZEW survey. In the UK, the Mansion House event Tuesday and inflation and labour market data on Wednesday and Thursday are the key risk events of the week.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 2.4bps at 1.876%, 5-Yr is down 1bps at 2.278%, 10-Yr is up 0.4bps at 2.729%, and 30-Yr is up 1.8bps at 3.245%.

- UK: The 2-Yr yield is down 4.4bps at 3.812%, 5-Yr is down 2.8bps at 4.015%, 10-Yr is down 2.2bps at 4.6%, and 30-Yr is down 0.3bps at 5.43%.

- Italian BTP spread up 1.7bps at 86.3bps / Spanish up 0.8bps at 61.4bps

MNI FOREX: USD Index Recovering Further, GBP Underperforms

- The USD index is rising once again on Monday, extending the ongoing cautious recovery from cycle lows to ~1.8%. This follows the DXY closing above 20-day EMA resistance on Friday, which marked a bullish development for the greenback.

- Early weakness in G10 was led by the likes of AUD and NZD as the threats of further global tariffs had a negative impact on risk sentiment. Despite the subsequent stabilisation for risk/equities, the dollar remains firmer as we approach the APAC crossover and tomorrow’s US CPI data.

- GBP has also been a notable underperformer, steadying edging lower across US hours and tilting GBPUSD to fresh pullback lows below 1.3440. A UK jobs report from KPMG REC showed a particularly pessimistic/stagflationary set of figures, with permanent staff appointments falling, availability of candidates increasing and permanent staff salary increases rising at the fastest rate since last October. Consequently, EURGBP has broken and cleared above the early July high - putting the cross at the best levels since early April. Price action narrows the gap to the key bull trigger at 0.8738, the 2025 high and near-term upside target.

- Higher US yields continue to underpin USDJPY’s strong rally across July, as markets also remain cautious surrounding BOJ rate hikes and the upcoming upper house election on Sunday. Japan's ruling LDP party received its lowest score in an opinion poll since returning to power in 2012 in a survey by public broadcaster NHK on Monday, underlining the prospect that the governing bloc may struggle this weekend.

- As such, USDJPY reached as high as 147.76 today, just 30 pips shy of the June highs, located at 148.03. Above here, 148.65 remains a key technical point for USDJPY, the May 12 high and a reversal trigger.

- Tuesday’s data calendar is stacked with China activity figures kicking things off. The focus will then swiftly turn to US and Canadian inflation data, final inputs before both the Fed and BOC decisions on July 30. We will also have the beginning of quarterly earnings season with financials the usual early focus.

TUESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 15/07/2025 | 0700/0900 | *** | HICP (f) | |

| 15/07/2025 | 0900/1100 | ** | Industrial Production | |

| 15/07/2025 | 0900/1100 | *** | ZEW Current Expectations Index | |

| 15/07/2025 | 1230/0830 | *** | CPI | |

| 15/07/2025 | 1230/0830 | ** | Monthly Survey of Manufacturing | |

| 15/07/2025 | 1230/0830 | ** | Empire State Manufacturing Survey | |

| 15/07/2025 | 1230/0830 | *** | CPI | |

| 15/07/2025 | 1230/0830 | *** | CPI | |

| 15/07/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 15/07/2025 | 1300/0900 | * | CREA Existing Home Sales | |

| 15/07/2025 | 1315/0915 | Fed Vice Chair Michelle Bowman | ||

| 15/07/2025 | 1645/1245 | Fed Governor Michael Barr | ||

| 15/07/2025 | 1845/1445 | Boston Fed's Susan Collins | ||

| 15/07/2025 | 2000/2100 | Mansion House: Chancellor Reeves and BOE Bailey | ||

| 15/07/2025 | 2245/1845 | Dallas Fed's Lorie Logan |