US INFLATION: MNI US CPI Preview: Passthrough Pressure Mounting

Jul-14 18:26

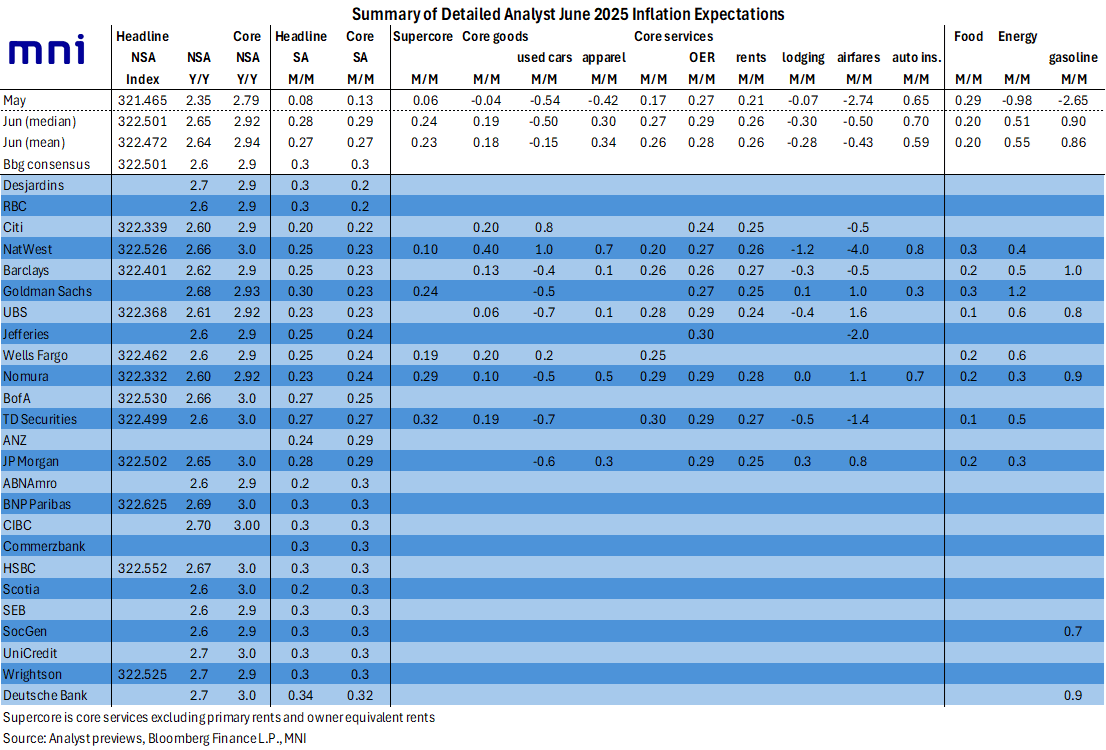

We've just published our preview of the June CPI report - Download Full Report Here

- Consensus sees core CPI inflation at a seasonally adjusted 0.3% M/M in June on a rounded basis, but with sizeable risk of undershooting at 0.2% (MNI median unrounded estimate at 0.24% M/M /average 0.25%).

- This would mark an acceleration from 0.13% M/M in May, with core services ticking up and core goods more than reversing May’s unexpected M/M deflation. Headline CPI meanwhile is seen at 0.3% M/M or 0.25% M/M unrounded after 0.08% in May, amid a bounce in gasoline-driven energy prices.

- It’s possible that June’s report will only be starting to show the delayed impact from the April reciprocal tariffs with the largest impact perhaps only to be seen in July. There appears a rough consensus of three months from tariff implementation to more notable consumer price increases.

- Goods will be in particular focus as tariffs are seen having an increasing influence on inflation as the summer unfolds. Categories to watch include apparel, communications/recreational goods, and furniture.

- In services, OER is seen steady with rent CPI picking up, while travel-related categories are seen remaining a drag. Supercore inflation was particularly subdued in May at 0.06% M/M and the estimates we’ve seen on average look for an acceleration to 0.23-0.24% M/M.

- It's unlikely that a downside inflation surprise would persuade the Federal Reserve to seriously consider cutting rates at its next decision on July 30, given the expected ongoing pickup in tariff-related prices.

- But a continued lack of evidence that tariffs are having an outsized effect on consumer prices would certainly help lay the groundwork for a resumption of easing in September.

- Headed into CPI (Tue) and PPI (Wed), the Fed’s preferred Core PCE gauge is seen at 0.25-0.26%.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US FISCAL: Available Extraordinary Measures Pick Up Ahead Of Tax Date

Jun-13 20:42

Treasury had $144B in "extraordinary measures" available to keep the government financed as of June 11 per a release Friday. That is up from $84B a week earlier and the highest since April 28.

- However, TGA cash continues to fall, to $309B latest (lowest since early April) Combined with a pullback in Treasury cash ($376B), keeping the total resources available to avert an "x-date" in the summer at around $450B .

- There will be another uptick in Treasury cash in the coming days, and it's likely Treasury allowed some of the extraordinary measures to be rebuilt (ie not exercised) in anticipation of more cash coming in.

- This is likely to be the last major uplift before the summer at which point x-date speculation will pick up if Congress hasn't passed a debt limit increase by then.

FED: Two Cuts Priced This Year Headed Into FOMC Week

Jun-13 20:28

As we head into the June Fed meeting week, market pricing is reflective of the FOMC’s messaging (that we describe in our preview):

- The next cut is only fully priced by the October FOMC meeting, with September seeing a roughly 80% implied probability of bringing the next 25bp reduction.

- Exactly 50bp of cuts are priced through end-2025, implying two Q4 cuts.

- That’s a shift from just after the May meeting, after which the next cut was fully priced by September, and there were closer to three cuts priced for the rest of the year.

- Overall cuts are seen backloaded this year (after 15bp in September, 29bp of cuts priced in Q4 - Oct/Dec combined), but falls off in Q1 (just 21bp cuts priced, 9bp of cuts priced for January and 12bp for March)

FED: Summary Of Economic Projections: Higher 2025 Inflation, Weaker Growth

Jun-13 20:21

The MNI Markets Team’s expectations for the updated Economic Projections are below.

- As of the May meeting, the Federal Reserve staff – whose outlook tends to be broadly shared by the median Committee member – revised their forecasts for growth weaker in 2025 and 2026, “as announced trade policies implied a larger drag on real activity relative to the policies that the staff had assumed in their previous forecast. Trade policies were also expected to lead to slower productivity growth and therefore to reduce potential GDP growth over the next few years. With the drag on demand expected to start earlier and to be larger than the supply response, the output gap was projected to widen significantly over the forecast period. The labor market was expected to weaken substantially, with the unemployment rate forecast moving above the staff's estimate of its natural rate by the end of this year and remaining above the natural rate through 2027."

- On inflation, "The staff's inflation projection was higher than the one prepared for the March meeting. Tariffs were expected to boost inflation markedly this year and to provide a smaller boost in 2026; after that, inflation was projected to decline to 2 percent by 2027."

- Our expectations for these changes fall somewhere in between those projections and the March SEP – a slightly higher unemployment rate, substantially higher inflation in 2025 but to a lesser extent in 2026, and weaker GDP growth this year. Longer-run variables should be unchanged.

MNI Markets Team Expectations For June 2025 Summary Of Economic Projections Medians