MNI ASIA OPEN: Hawkish Tweaks to ECB Lagarde’s Presser

EXECUTIVE SUMMARY

- MNI ECB: MNI ECB Review: Market Maintains Mildest Of Easing Biases

- MNI EXCLUSIVE: Senior Chinese Policy Advisor on Outlook for U.S.-China Relations

- MNI US: Senate Passes Joint Res. Rolling Back Biden-Era Alaska Oil Restrictions

- MNI TARIFFS: Senate Passes Symbolic Resolution Terminating Trump's Global Tariffs

- MNI US DATA: Dallas Fed Points To Slowing GDP Growth Based On Weekly Indicators

US

MNI EXCLUSIVE: Senior Chinese Policy Advisor on Outlook for U.S.-China Relations

- A senior Chinese policy advisor gives her outlook for U.S.-China relations following the Trump-Xi summit -- On MNI Policy MainWire now, for more details please contact sales@marketnews.com

NEWS

MNI ECB: MNI ECB Review: Market Maintains Mildest Of Easing Biases

The ECB left its three key rates unchanged again, including the deposit rate at 2.00%, as fully expected. The decision statement offered no surprises, noting general resilience with an expected caveat from the uncertain outlook whilst reiterating data-dependence and a meeting-by-meeting approach.

MNI TARIFFS: Senate Passes Symbolic Resolution Terminating Trump's Global Tariffs

The US Senate has passed a resolution terminating the national emergency declaration that US President Donald Trump used to impose reciprocal tariffs on trading partners. The resolution will go no further as House Speaker Mike Johnson (R-LA) established a new rule preventing such legislation from reaching the House floor. If the resolution were to pass the House, it would be subject to a presidential veto.

MNI US: Senate Passes Joint Res. Rolling Back Biden-Era Alaska Oil Restrictions

The Senate has voted 52-45 to repeal a Biden administration-era rule restricting oil and gas development in Alaska's National Petroleum Reserve, including Alaska's North Slope. Senator John Fetterman (D-PA) was the only Democrat to vote in favour of the resolution.

REUTERS - ECB: European Central Bank policymakers are preparing for something of a showdown at their next meeting in December, when new three-year projections will shed light on whether or not they risk undershooting their target, four sources told Reuters.

US TSYS

MNI US TSYS: Post-FOMC Retreat in Rates, ECB Held Steady

- Treasuries look to finish weaker, off morning lows, curves mildly steeper (2s10s +.522 at 48.089, 5s30s +1.245at 92.638), projected rate cut pricing hold near late Wednesday levels (* Post FOMC): Dec'25 at -18bp (-15.5bp), Jan'26 at -26.5bp (-26bp), Mar'26 at -35.1bp (-35.3bp), Apr'26 at -41bp (-42bp).

- Currently, the Dec'25 10Y contract trades -7 at 112-22 vs. 112-16 low, 10Y yield +.0193 at 4.0950% vs. 4.1144% high. The contract has traded through the 50-day EMA, at 112-27. This highlights potential for a deeper retracement near-term. An extension lower would open 112-06 Low Sep 25 and the next key support.

- The ECB left its three key rates unchanged again, including the deposit rate at 2.00%, as fully expected. The decision statement offered no surprises, noting general resilience with an expected caveat from the uncertain outlook whilst reiterating data-dependence and a meeting-by-meeting approach.

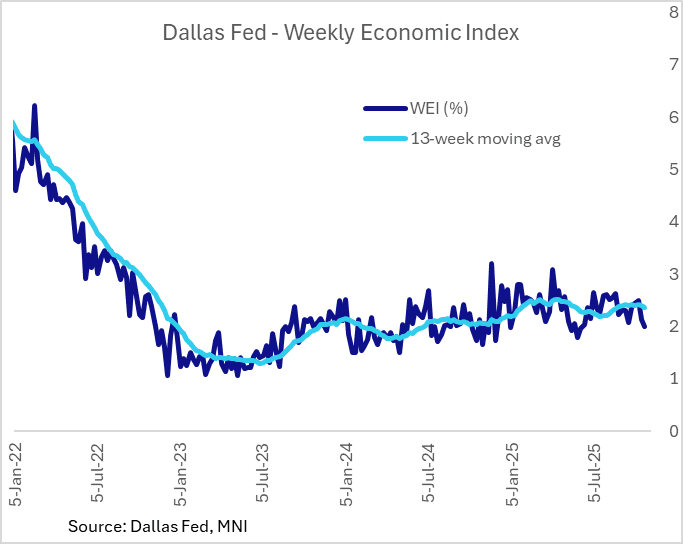

- Limited data on day 30 of the US Gov shutdown: The Dallas Fed's Weekly Economic Index slowed in the week of August to 2.00% in the week ending Oct 25 (scaled to 4-quarter growth), from 2.14% prior, marking a 20-week low.

- Look ahead to Friday: Data from BEA & BLS postponed due to the ongoing US Gov shutdown (day 30) - no Personal Income/Spending, PCE Prices or Employment Cost data tomorrow. Markets do get to see the latest Chicago PMI from MNI, and Fed speakers: Dallas Fed Logan bank funding conf (text, no Q&A) at 0930ET, Cleveland Fed Hammack & Atlanta Fed Bostic bank funding conf at 1200ET.

OVERNIGHT DATA

MNI US DATA: Dallas Fed Points To Slowing GDP Growth Based On Weekly Indicators

The Dallas Fed's Weekly Economic Index slowed in the week of August to 2.00% in the week ending Oct 25 (scaled to 4-quarter growth), from 2.14% prior, marking a 20-week low. This dragged down the 13-week moving average to 2.36% after 7 consecutive weeks above 2.40%, for the lowest since August 23.

MARKETS SNAPSHOT

Key market levels of markets in late NY trade:

DJIA down 139.62 points (-0.29%) at 47503.9

S&P E-Mini Future down 66.75 points (-0.96%) at 6856

Nasdaq down 360.4 points (-1.5%) at 23595.08

US 10-Yr yield is up 1.2 bps at 4.0873%

US Dec 10-Yr futures are down 5.5/32 at 112-23.5

EURUSD down 0.0035 (-0.3%) at 1.1566

USDJPY up 1.32 (0.86%) at 154.04

WTI Crude Oil (front-month) down $0.15 (-0.25%) at $60.33

Gold is up $94.73 (2.41%) at $4024.15

European bourses closing levels:

EuroStoxx 50 down 6.63 points (-0.12%) at 5699.18

FTSE 100 up 3.92 points (0.04%) at 9760.06

German DAX down 5.32 points (-0.02%) at 24118.89

French CAC 40 down 43.59 points (-0.53%) at 8157.29

US TREASURY FUTURES CLOSE

3M10Y +4.234, 23.566 (L: 17.269 / H: 24.988)

2Y10Y +0.329, 47.896 (L: 46.701 / H: 49.038)

2Y30Y +0.704, 103.224 (L: 100.979 / H: 104.861)

5Y30Y +1.034, 92.427 (L: 90.103 / H: 93.852)

Current futures levels:

Dec 2-Yr futures down 1.75/32 at 104-4 (L: 104-02.5 / H: 104-06)

Dec 5-Yr futures down 3/32 at 109-6.75 (L: 109-02.25 / H: 109-10.5)

Dec 10-Yr futures down 6.5/32 at 112-22.5 (L: 112-16 / H: 112-29.5)

Dec 30-Yr futures down 18/32 at 117-21 (L: 117-09 / H: 118-03)

Dec Ultra futures down 28/32 at 121-26 (L: 121-13 / H: 122-14)

MNI US 10YR FUTURE TECHS: (Z5) Pullback Extends

- RES 4: 114-02 High Oct 17 and the bull trigger

- RES 3: 113-29 High Oct 22

- RES 2: 113-18+ High Oct 28

- RES 1: 113-07+ 20-day EMA

- PRICE: 112-23+ @ 1257 ET Oct 30

- SUP 1: 112-16 Intraday low

- SUP 2: 112-14 Low Oct 9

- SUP 3: 112-06 Low Sep 25 and a reversal trigger

- SUP 4: 111-28+ Trendline support drawn from the May 22 low

A sharp sell-off in Treasuries yesterday and the follow through today, undermines a recent bullish theme. The contract has traded through the 50-day EMA, at 112-27. This highlights potential for a deeper retracement near-term. An extension lower would open 112-06 Low Sep 25 and the next key support. On the upside, the contract needs to trade above 113-18+, the Oct 28 high to signal a possible bullish reversal.

SOFR FUTURES CLOSE

Current White pack (Dec 25-Sep 26):

Dec 25 -0.025 at 96.245

Mar 26 -0.035 at 96.425

Jun 26 -0.030 at 96.650

Sep 26 -0.030 at 96.810

Red Pack (Dec 26-Sep 27) -0.035 to -0.025

Green Pack (Dec 27-Sep 28) -0.025 to -0.02

Blue Pack (Dec 28-Sep 29) -0.025 to -0.02

Gold Pack (Dec 29-Sep 30) -0.03 to -0.025

REFERENCE RATES

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.27% (-0.04), volume: $3.061T

- Broad General Collateral Rate (BGCR): 4.24% (-0.04), volume: $1.150T

- Tri-Party General Collateral Rate (TCR): 4.24% (-0.04), volume: $1.115T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.12% (+0.00), volume: $98B

- Daily Overnight Bank Funding Rate: 4.12% (+0.00), volume: $189B

FED Reverse Repo Operation

RRP usage slips to $19.166B with 18 counterparties this afternoon from $19.504B Wednesday. Compares to $2.435B on October 24 (lowest level since mid-March 2021) and the year's highest usage of $460.731B on June 30.

PIPELINE: Corporate Bond Update: October Going Out With Bang

$30B Meta 6pt jumbo leads - 5th largest on record (matching $30B AbbVie jumbo 10-part on 11/12/19, and $30B ATT/Discovery 11pt via Magallanes inc on 3/922).

- Date $MM Issuer (Priced *, Launch #)

- 10/30 $30B *Meta $4B 5Y +50, $4B 7Y +70, $6.5B 10Y +78, $4.5B 20Y +88, $6.5B 30Y +98, $4.5B 40Y +110

- 10/30 $5B #HSBC $2.25B 6Y +90, $500M 6Y SOFR+119, $2.25B 11Y +105

- 10/30 $2.8B #Santander $1.25B 5Y +83, $300M 5Y SOFR+112, $1.25B 10Y +103

- 10/30 $2.3B #NatWest $850M 3Y +57, $600M 3Y SOFR+80, $850M 5Y +70

- 10/30 $700M *PPG Industries +5Y +70

- 10/30 $500M #MSCI +10Y +110

MNI BONDS: EGBs-GILTS CASH CLOSE: Bunds Digest ECB Meeting Smoothly

Bunds outperformed Gilts amid broader weakness in global bonds Thursday.

- A more hawkish-than-expected Fed press conference late Wednesday saw a negative spill-over impact into Europe Thursday, stabilizing just ahead of the ECB decision.

- In data, Spanish and German flash inflation surprised to the upside. French flash Q3 GDP was stronger-than-expected, Germany was broadly in line, while Italy surprised to the downside.

- The ECB release brought virtually no surprises and saw rate pricing little changed, with global FI picking up from session lows despite some hawkish tweaks to Lagarde’s press conference. The now typical Reuters sources piece later in the day pointed to a more contentious December meeting.

- MNI's review of the ECB decision is here.

- Bonds would regain ground for most of the rest of the session. On the day, Bunds marginally outperformed Gilts, which were weighed down by uncertainty over the political future of UK Chancellor Reeves; periphery / semi-core EGB spreads tightened modestly.

- Friday brings the Eurozone-wide October flash inflation print (and those of Italy and France).

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 1.2bps at 1.986%, 5-Yr is up 2.1bps at 2.253%, 10-Yr is up 2.2bps at 2.643%, and 30-Yr is up 1.1bps at 3.199%.

- UK: The 2-Yr yield is up 3bps at 3.796%, 5-Yr is up 3.6bps at 3.908%, 10-Yr is up 3.2bps at 4.424%, and 30-Yr is up 1.7bps at 5.181%.

- Italian BTP spread down 0.4bps at 75.6bps / French OAT down 0.6bps at 78bps

MNI FOREX: USD Index Consolidating Lurch Higher, Pressure on JPY Remains

- Post-Fed optimism for the US dollar has extended on Thursday, with the USD index (+0.32%) notably rising to the highest level since August 01. Price action has been underpinned by the market questioning the Fed’s December easing prospects, following Chair Powell’s acknowledgement that there are no foregone conclusions on another rate reduction.

- The greenback rally has been most notable against the Japanese yen, following the Bank of Japan remaining on hold and failing to provide any explicit signals regarding a December hike. The broad JPY weakness has prompted USDJPY to rally to fresh 8-month highs, reaching an intra-day peak of 154.45, an impressive 229 pips off initial session lows. Sights are on 154.80 next, the Feb 12 high.

- Elsewhere, GBP continued its run of poor form, with cable breaking a significant technical support level through 1.3140. Given the multiple daily lows and the significance of the level, market participants will quickly turn their attention to potential targets of a more protracted move lower. Ongoing fiscal concerns have been exacerbated on Thursday by rising uncertainty over Chancellor Reeve’s future amid new information coming to light surrounding a breach of housing rules.

- Downside levels for cable include 1.3041, the Apr 14 low and 1.2971, the 1.382 projection of the Sep 17 - 25 - Oct 1 price swing. Below here, the April 07 low is located at 1.2709. EURGBP has had a steadier session around 0.88, with topside targets for the ongoing rally include 0.8835 and 0.8875, the April 2023 high.

- The broad greenback strength has tilted EURUSD back below 1.16, narrowing the gap to 1.1542, the Oct 9 low. Clearance of this level would confirm a resumption of the bear cycle that started Sep 17, opening 1.1516, a Fibonacci retracement.

- Further Eurozone inflation data highlights the Friday calendar. China manufacturing and non-manufacturing PMIs are also scheduled, before Canada August GDP.

FRIDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 31/10/2025 | 0700/0800 | ** | Import/Export Prices | |

| 31/10/2025 | 0700/0800 | ** | Retail Sales | |

| 31/10/2025 | 0730/0830 | ** | Retail Sales | |

| 31/10/2025 | 0745/0845 | *** | HICP (p) | |

| 31/10/2025 | 0745/0845 | ** | PPI | |

| 31/10/2025 | 0930/0930 | Blue Book / Pink Book | ||

| 31/10/2025 | 1000/1100 | *** | EZ HICP Flash | |

| 31/10/2025 | 1000/1100 | *** | EZ HICP Flash | |

| 31/10/2025 | 1000/1100 | *** | Italy Flash Inflation | |

| 31/10/2025 | 1000/1100 | *** | EZ HICP Flash | |

| 31/10/2025 | 1230/0830 | *** | Gross Domestic Product by Industry | |

| 31/10/2025 | 1230/0830 | *** | Personal Income and Consumption | |

| 31/10/2025 | 1230/0830 | *** | Employment Cost Index | |

| 31/10/2025 | 1230/0830 | *** | Gross Domestic Product by Industry | |

| 31/10/2025 | 1330/0930 | Dallas Fed's Lorie Logan | ||

| 31/10/2025 | 1342/0942 | *** | MNI Chicago PMI | |

| 31/10/2025 | 1500/1100 | Finance Dept monthly Fiscal Monitor (expected) | ||

| 31/10/2025 | 1600/1200 | Fed's Beth Hammack, Raphael Bostic | ||

| 31/10/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 31/10/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 31/10/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly |