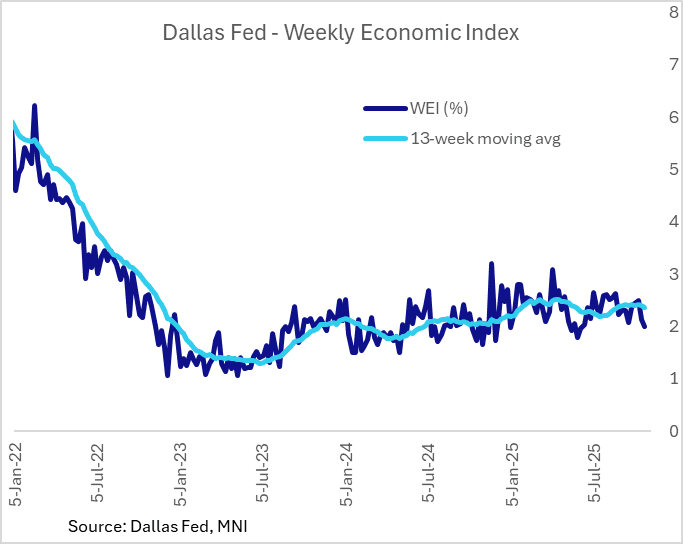

US DATA: Dallas Fed Points To Slowing GDP Growth Based On Weekly Indicators

The Dallas Fed's Weekly Economic Index slowed in the week of August to 2.00% in the week ending Oct 25 (scaled to 4-quarter growth), from 2.14% prior, marking a 20-week low.

- This dragged down the 13-week moving average to 2.36% after 7 consecutive weeks above 2.40%, for the lowest since August 23.

- While that should be caveated by the lack of official continuing/initial jobless claims data (which instead are imputed by the Dallas Fed for the purposes of its estimates), this indicator is suggestive that the upward momentum that appeared to have been building through the end of Q3 has tapered off somewhat as Q4 goes on.

- The track record of the WEI has been decent including in identifying solid growth through much of 2025, and has become a little more worthwhile to follow amid the dearth of federal government data.

- It's not entirely clear what drove the latest weekly slowdown since we don't have access to much of the private-sector data the authors use, but we did note a slight downtick (but still solid) Redbook retail sales growth in the latest week, as well as a slowdown in federal tax withholding and weaker railroad traffic (not to mention last week's estimated uptick in initial claims).

- The WEI's inputs: "To measure consumer behavior, we include the Redbook same-store retail sales index and the Rasmussen Consumer Index. To measure labor market conditions, we include initial and continuing unemployment insurance claims, the American Staffing Association Index of temporary and contract employment, and federal tax withholding data from Booth Financial Consulting. For production, we include U.S. steel production from the American Iron and Steel Institute, U.S. electricity output data from the Edison Electric Institute, a measure of fuel sales based on Energy Information Administration data, and total railroad traffic from the Association of American Railroads."

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EU: Leaders To Hold Informal Meeting 1 Oct On Defence & Ukraine

An informal meeting of heads of state and/or government takes place at Christiansborg Palace in the Danish capital, Copenhagen on Wednesday, 1 October. The main topics of discussion will be common European defence (in the context of numerous Russian incursions into EU member states’ airspace by drones and aircraft in recent weeks) and support for Ukraine.

- The common defence talks will focus on delivery of the EU's 'Readiness 2030' programme (formerly 'ReArm Europe'), which seeks to utilise up to EUR800bln to bolster the EU's defences and defence sector.

- The Ukraine talks are likely to include discussions on using frozen Russian assets held in the EU to fund Ukraine’s reconstruction via a ‘reparation loan’, as well as another round of sanctions.

- EU Observer reports, "Some or all of the frozen assets in Euroclear would be moved into a Special Purpose Vehicle (SPV) and transferred to Ukraine in 2026 and 2027, in exchange for zero-coupon (euro)bonds issued by the commission. The bonds would be backed by guarantees from a "coalition of the willing" EU member states and possibly other G7 countries prepared to support the plan. Von der Leyen on Tuesday insisted the plan is legally watertight, since it stops short of outright confiscation of Russia’s sovereign assets."

- Doorstep comments from leaders on arrival will start at ~11:30CET (05:30ET, 10:30BST). The closing press conference, national briefings and exit doorstep comments will get underway following the conclusion of the informal EUCO meeting at ~17:30CET (11:30ET, 16:30BST).

BOE: Breeden: Policy Is Restrictive, Seeking Confidence In Future Disinflation

In her first substantive commentary on monetary policy since early June, BOE's Breeden sounds supportive of easing policy further albeit without specifying a timeline, writing in a speech Tuesday that "Looking ahead, although the impact of past rises in Bank Rate looks to be around their peak, they will still be weighing on the level of demand and so continue to contribute to the disinflationary process. While the degree of restrictiveness has fallen over the past 18 months as the MPC has reduced Bank Rate, I still judge the current monetary policy stance to be restrictive and so continuing to squeeze persistence from the system." (Speech link here).

- Importantly, "I do not see evidence that the disinflation process is veering off-track. Instead it remains my central case that the “hump” will prove just a bump in the road."

- She says that there are "of course" risks to to her outlook, and that "In such a world it may be tempting to wait to see the “whites of disinflation’s eyes” before looking to reduce the restrictiveness of policy further." But "managing the upside risks to inflation in this way brings risk in the other direction: holding policy too tight for too long comes with costs to output and employment, which could then pull inflation below target...More broadly, there are downside risks to demand which could also pull inflation below target further out. "

- What she's looking for: "With this context, I will be focused on identifying those indicators that give me confidence that the future disinflationary process - in particular the “hand-off” from wages to services price inflation - is remaining on track. Indicators of pricing intentions, from surveys and intelligence from our Agents, will be important here, as will conversations like those I have had in Cardiff today underlining the important part you’re playing in the team trying to understand what’s going on in the economy. Indeed we might think of indicators such as these as signposts that help determine whether we are likely to veer off track. And they will therefore be key in determining when it might be appropriate to remove further restrictiveness."

- While Breeden's support for a cut in November would likely be key to such a decision by the MPC at that meeting, rate pricing through year-end is little changed: now a little closer to 2bp cuts for Nov than 1bp prior to speech release, and 6bp through year-end.

FED: US TSY 52W BILL AUCTION: HIGH 3.540%(ALLOT 70.11%)

- US TSY 52W BILL AUCTION: HIGH 3.540%(ALLOT 70.11%)

- US TSY 52W BILL AUCTION: DEALERS TAKE 40.55% OF COMPETITIVES

- US TSY 52W BILL AUCTION: DIRECTS TAKE 4.26% OF COMPETITIVES

- US TSY 52W BILL AUCTION: INDIRECTS TAKE 55.19% OF COMPETITIVES

- US TSY 52W AUCTION: BID/CVR 2.92