MNI ASIA OPEN: Fed Guidance Less Hawkish Than Anticipated

EXECUTIVE SUMMARY

- MNI: Fed Cuts Rates, Higher Bar For More; Resumes Asset Buys

- MNI BOC: Downplaying Recent Data Upside Suggests Lack Of Impetus To Move On Rates

- MNI INTERNATIONAL TRADE: USTR Greer Speaks On Washington's Trade Stance & Tariffs

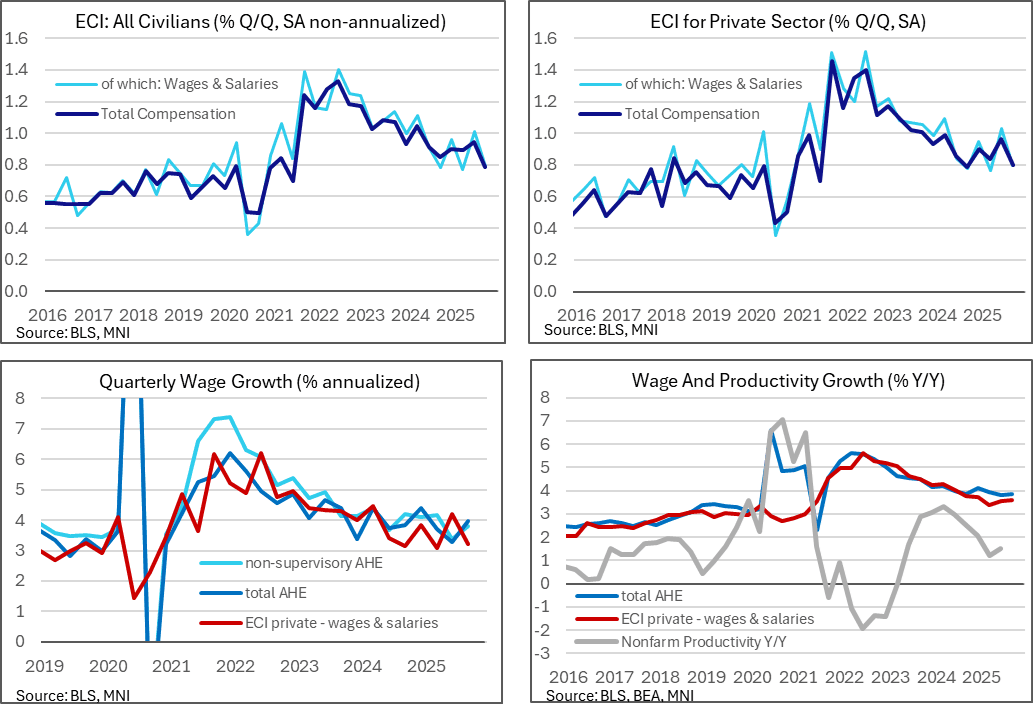

- MNI US DATA: ECI Cools With Softest Quarter Since 2021

US/CANADA

MNI: Fed Cuts Rates, Higher Bar For More; Resumes Asset Buys

A divided Federal Reserve lowered interest rates for a third time this year Wednesday, with officials indicating a higher bar for future cuts as borrowing costs reach the range of what policymakers see as neutral. Policymakers penciled in one more rate cut in 2026 and in 2027 on median, unchanged from the September Summary of Economic Projections.

- "In considering the extent and timing of additional adjustments to the target range for the federal funds rate, the Committee will carefully assess incoming data, the evolving outlook, and the balance of risks," the Fed said in its post-meeting statement.

- Three officials dissented against the decision, the most since 2019. Chicago Fed President Austan Goolsbee and Kansas City Fed President Jeffrey Schmid wanted to keep rates on hold while Governor Stephen Miran voted for the third time in favor of a larger 50 basis point reduction.

MNI BOC: Macklem Acknowledges Economy More Resilient Than Previously Expected

Through the Q&A, Gov Macklem continues to portray the Bank's economic outlook as largely unchanged since the October meeting, though there have been acknowledgements throughout today's communications that the economy is on more solid ground than they had expected.

- Macklem says that the upside surprise to GDP growth in Q3 and the upward revisions to prior years don't alter the Bank's outlook that there is still a negative output gap, however the gap may be smaller than was estimated in the October Monetary Policy Report (which saw the gap as being closed by end-2026):

MNI BOC: Downplaying Recent Data Upside Suggests Lack Of Impetus To Move On Rates

As largely expected the BOC produced a fairly neutral appraisal of the economy and rate outlook, alongside with the unanimously-expected overnight rate hold at 2.25%. The market reaction is slightly dovish (about 2-3bp of implied hiking taken out of the path over the next 7 meetings), reflecting the Statement's downplaying of recent upside surprises in macro data developments.

- There is no change to October's guidance that "Governing Council sees the current policy rate at about the right level to keep inflation close to 2% while helping the economy through this period of structural adjustment." However the statement inserts "Uncertainty remains elevated." before repeating "If the outlook changes, we are prepared to respond."

NEWS

MNI INTERNATIONAL TRADE: USTR Greer Speaks On Washington's Trade Stance & Tariffs

Speaking at an Atlantic Council event (livestream here), US Trade Representative Jamieson Greer talks on how the Trump administration has reshaped global trade. On trade negotiations in North America. Says it "makes sense to discuss trade issues separately with Mexico and Canada," adding that there "could be certain areas where trilateral discussion can make sense, including on the rule of law or external trade policies." Says that the USMCA trade deal "could be exited, revised, or renegotiated; all of those things are on the table."

BLOOMBERG: "US SEIZES OIL TANKER OFF THE COAST OF VENEZUELA"

US TSYS

MNI US TSYS: Rates Rally, Fed Guidance Less Hawkish Than Anticipated

- Treasuries look to finish near late session highs after the FOMC delivered an expected 25bp rate cut, while anticipation for hawkish guidance proved less so - fueling bull curve steepening as Chairman Powell answered journalist questions.

- Currently, the TYH6 contract trades +10.5 at 113-13.5 vs. 113-14.5, initial key resistance is seen at 112-25+, the 20-day EMA. A break of this average would signal a possible reversal.

- Policymakers penciled in one more rate cut in 2026 and in 2027 on median, unchanged from the September Summary of Economic Projections. "In considering the extent and timing of additional adjustments to the target range for the federal funds rate, the Committee will carefully assess incoming data, the evolving outlook, and the balance of risks," the Fed said in its post-meeting statement.

- As the FOMC press conference progressed, negative sentiment towards the dollar has re-emerged, with the USD index extending session lows and now down a little more than 0.5%. Gains across the G10 have been broad based and are certainly more balanced than earlier on Wednesday.

- Earlier data - the ECI increased 0.79% non-annualized in Q3 (sa, cons 0.9) after an unrevised 0.94% in Q2 and 0.89% in Q1. It’s the softest quarter since 2Q21. The wages & salaries component also moderated to 0.79% after 1.01% in Q2 although that’s back close to the 0.77% in Q1.

OVERNIGHT DATA

MNI US DATA: ECI Cools With Softest Quarter Since 2021

The delayed Employment Cost Index report for Q3 saw its softest nominal wage pressures since 2021 even if the wages & salaries component has recently seen equally soft quarters. At these rates, the labor market is unlikely to be putting material pressure in either direction on inflation.

- The ECI increased 0.79% non-annualized in Q3 (sa, cons 0.9) after an unrevised 0.94% in Q2 and 0.89% in Q1. It’s the softest quarter since 2Q21. The wages & salaries component also moderated to 0.79% after 1.01% in Q2 although that’s back close to the 0.77% in Q1. The private sector metrics broadly reflect these trends, at 0.80% for total compensation and 0.80% for wages & salaries.

MARKETS SNAPSHOT

Key market levels of markets in late NY trade:

DJIA up 497.46 points (1.05%) at 48057.75

S&P E-Mini Future up 44 points (0.64%) at 6892.5

Nasdaq up 77.7 points (0.3%) at 23654.15

US 10-Yr yield is down 4.1 bps at 4.1468%

US Mar 10-Yr futures are up 9/32 at 112-12

EURUSD up 0.0067 (0.58%) at 1.1694

USDJPY down 0.91 (-0.58%) at 155.97

WTI Crude Oil (front-month) up $0.71 (1.22%) at $58.96

Gold is up $23.38 (0.56%) at $4231.89

European bourses closing levels:

EuroStoxx 50 down 10.2 points (-0.18%) at 5708.12

FTSE 100 up 13.52 points (0.14%) at 9655.53

German DAX down 32.51 points (-0.13%) at 24130.14

French CAC 40 down 29.82 points (-0.37%) at 8022.69

US TREASURY FUTURES CLOSE

Curve update:

3M10Y -0.447, 46.846 (L: 41.683 / H: 49.462)

2Y10Y +4.177, 61.077 (L: 55.46 / H: 61.115)

2Y30Y +6.661, 125.576 (L: 117.92 / H: 125.682)

5Y30Y +4.672, 106.451 (L: 100.495 / H: 106.625)

Current futures levels:

Mar 2-Yr futures up 4.5/32 at 104-9.625 (L: 104-04 / H: 104-10)

Mar 5-Yr futures up 7.75/32 at 109-5.5 (L: 108-26.25 / H: 109-07)

Mar 10-Yr futures up 8.5/32 at 112-11.5 (L: 111-29 / H: 112-14.5)

Mar 30-Yr futures up 11/32 at 115-17 (L: 114-29 / H: 115-26)

Mar Ultra futures up 10/32 at 118-21 (L: 118-00 / H: 119-03)

MNI US 10YR FUTURE TECHS: (H6) Bear Cycle Extends

- RES 4: 113-29+ High Oct 17 and a key resistance

- RES 3: 113-23 High Oct 23

- RES 2: 113-07/22+ High Dec 3 / High Nov 25

- RES 1: 112-25+ 20-day EMA

- PRICE: 112-13.5 @ 1546 ET Dec 10

- SUP 1: 111-29+ Intraday low

- SUP 2: 111-19 1.236 proj of the Oct 17 - Nov 5 - 25 price swing

- SUP 3: 111-11 1.382 proj of the Oct 17 - Nov 5 - 25 price swing

- SUP 4: 111-00 Round number support

A bearish theme in Treasuries remains intact and this week’s move down reinforces current conditions. An important short-term support at 112-07, the Nov 5 low and a bear trigger, has been cleared. The breach strengthens a bear theme and signals scope for a move towards 111-19 next a Fibonacci projection. Initial key resistance is seen at 112-25+, the 20-day EMA. A break of this average would signal a possible reversal.

SOFR FUTURES CLOSE

Current White pack (Dec 25-Sep 26):

Dec 25 +0.015 at 96.280

Mar 26 +0.050 at 96.450

Jun 26 +0.075 at 96.665

Sep 26 +0.080 at 96.805

Red Pack (Dec 26-Sep 27) +0.050 to +0.075

Green Pack (Dec 27-Sep 28) +0.025 to +0.040

Blue Pack (Dec 28-Sep 29) +0.020 to +0.025

Gold Pack (Dec 29-Sep 30) +0.020 to +0.025

REFERENCE RATES

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 3.93% (-0.02), volume: $3.244T

- Broad General Collateral Rate (BGCR): 3.90% (-0.03), volume: $1.315T

- Tri-Party General Collateral Rate (TCR): 3.90% (-0.03), volume: $1.285T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 3.89% (+0.00), volume: $85B

- Daily Overnight Bank Funding Rate: 3.89% (+0.00), volume: $161B

FED Reverse Repo Operation

RRP usage rises to $5.045B with 17 counterparties this afternoon from $3.211B Tuesday. Compares to Tuesday November 18: $0.905B - lowest level since mid-March 2021; this years highest excess liquidity measure: $460.731B on June 30.

MNI PIPELINE: Corporate Bond Update: Asurion LLC Upsized to $3.3B, Launched

- Date $MM Issuer (Priced *, Launch #)

- 10/10 $3.3B #Asurion LLC 7NC3 8%, upsized from $1.25B after investor calls earlier in week

- $1.25B Priced Tuesday

- 12/09 $750M #Bank of Montreal 2NC1 +50

- 12/09 $500M #American National Global Funding 3Y +100

MNI BONDS: EGBs-GILTS CASH CLOSE: German Short-End Remains Under Light Pressure

European yields rose slightly Wednesday.

- The German curve saw light bear flattening with continued short-end underperformance as ECB hike pricing edging higher for 2026 despite some pushback against that notion by ECB's Villeroy and Simkus.

- That helped drag on the UK short-end/belly as well. Overall on the day though the German short-end underperformed its UK counterpart; vice-versa for the long-end.

- In a session limited on data and macro developments, softer-than-expected US employment cost data helped global core FI recover from early session lows. ECB's Kazaks told an MNI Connect event that monetary policy remains in a "good place" with no need to act in December.

- Periphery/semi-core EGB spreads were little changed on the day, with OAT spreads closing slightly wider despite the French National Assembly passing the 2026 Social Security budget after Tuesday's close.

- Attention after the cash close will be on the US Federal Reserve decision; Thursday's calendar includes the SNB decision.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 2.3bps at 2.177%, 5-Yr is up 1bps at 2.476%, 10-Yr is up 0.1bps at 2.851%, and 30-Yr is down 0.6bps at 3.453%.

- UK: The 2-Yr yield is up 0.5bps at 3.79%, 5-Yr is up 1.1bps at 3.983%, 10-Yr is up 0.1bps at 4.506%, and 30-Yr is up 1bps at 5.205%.

- Italian BTP spread up 0.1bps at 69.6bps / French OAT up 0.3bps at 71.6bps

MNI FOREX: USD Selling Resumes, DXY Extends Decline to 0.65%

- As the FOMC press conference progressed, negative sentiment towards the dollar has re-emerged, with the USD index extending session lows and now down a little more than 0.5%. Gains across the G10 have been broad based and are certainly more balanced than earlier on Wednesday.

- This dynamic has propelled the likes of EUR, AUD and NZD to fresh recovery highs, while the Japanese Yen has been eroding the week’s advance with USDJPY now trading back below the 156.00 handle. GBPUSD is also pressing towards 1.34, while the Swiss Franc and Swedish krona remain the day’s best performers.

- For EURUSD, spot is testing the 1.17 handle for the first time since October 17, keeping the technical bull cycle intact. The recent breach of key short-term resistance at 1.1656, the Nov 13 high and a bull trigger, and today’s extension higher strengthens the underlying bullish sentiment. 1.1728 and 1.1779 represent the next levels on the topside.

- AUDUSD has notably risen above the September 18 high of 0.6660, extending the impressive surge from the November lows to 4.12% amid the more hawkish RBA and firmer risk sentiment. A strong impulsive bull wave in AUDUSD remains intact, signalling scope for a continuation near-term. 0.6707 remains a key resistance point, the September 17 high.

- In similar vein, NZDUSD has extended above pivot resistance at 0.5800, registering a 0.5825 high on Wednesday, while USDSEK (-1.12%) has significantly narrowed the gap to recent cycle lows at 9.1936. A break below here would place the pair at the lowest level since February 2022.

THURSDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 11/12/2025 | 0700/0800 | *** | Final Inflation Report | |

| 11/12/2025 | 0700/0800 | *** | Final Inflation Report | |

| 11/12/2025 | 0830/0930 | *** | SNB Interest Rate Decision | |

| 11/12/2025 | 0950/0950 | BOE Bailey Pre-recorded Chat on Financial Stability | ||

| 11/12/2025 | 1000/1000 | BOE Bailey Gives Evidence At Covid-19 Inquiry | ||

| 11/12/2025 | 1100/0600 | *** | Turkey Benchmark Rate | |

| 11/12/2025 | - | *** | Money Supply | |

| 11/12/2025 | - | *** | Social Financing | |

| 11/12/2025 | - | *** | New Loans | |

| 11/12/2025 | - | ECB Lagarde and Cipollone at Eurogroup Meeting | ||

| 11/12/2025 | 1330/0830 | *** | Jobless Claims | |

| 11/12/2025 | 1330/0830 | ** | WASDE Weekly Import/Export | |

| 11/12/2025 | 1330/0830 | * | Household debt-to-income | |

| 11/12/2025 | 1330/0830 | ** | International Merchandise Trade (Trade Balance) | |

| 11/12/2025 | 1330/0830 | ** | Trade Balance | |

| 11/12/2025 | 1330/0830 | ** | Trade Balance | |

| 11/12/2025 | 1500/1000 | * | Services Revenues | |

| 11/12/2025 | 1500/1000 | ** | Wholesale Trade | |

| 11/12/2025 | 1500/1000 | ** | Wholesale Trade | |

| 11/12/2025 | 1530/1030 | ** | Natural Gas Stocks | |

| 11/12/2025 | 1630/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 11/12/2025 | 1630/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 11/12/2025 | 1800/1300 | *** | US Treasury Auction Result for 30 Year Bond | |

| 12/12/2025 | 0430/1330 | ** | Industrial Production |