US TSYS: Rates Rally, Fed Guidance Less Hawkish Than Anticipated

- Treasuries look to finish near late session highs after the FOMC delivered an expected 25bp rate cut, while anticipation for hawkish guidance proved less so - fueling bull curve steepening as Chairman Powell answered journalist questions.

- Currently, the TYH6 contract trades +10.5 at 113-13.5 vs. 113-14.5, initial key resistance is seen at 112-25+, the 20-day EMA. A break of this average would signal a possible reversal.

- Policymakers penciled in one more rate cut in 2026 and in 2027 on median, unchanged from the September Summary of Economic Projections. "In considering the extent and timing of additional adjustments to the target range for the federal funds rate, the Committee will carefully assess incoming data, the evolving outlook, and the balance of risks," the Fed said in its post-meeting statement.

- As the FOMC press conference progressed, negative sentiment towards the dollar has re-emerged, with the USD index extending session lows and now down a little more than 0.5%. Gains across the G10 have been broad based and are certainly more balanced than earlier on Wednesday.

- Earlier data - the ECI increased 0.79% non-annualized in Q3 (sa, cons 0.9) after an unrevised 0.94% in Q2 and 0.89% in Q1. It’s the softest quarter since 2Q21. The wages & salaries component also moderated to 0.79% after 1.01% in Q2 although that’s back close to the 0.77% in Q1.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Nearer The End of US Govt Shutdown

- Treasuries look to finish weaker, near the middle of Monday's range - optimism buoyed as the US Govt shutdown appears to be nearer an end after eight Democrats broke formation with colleagues to reopen the Govt.

- Stocks rallied, led by chip makers while Health Care sector shares continued to decline in the second half - if the US Govt shutdown ends without an extension of Affordable Care Act (ACA) subsidies.

- Reactions across G10 do not surprise, with the boost to risk assets filtering through to the underperforming JPY, while supporting the likes of AUD, NZD and NOK.

- Treasury futures pare losses slightly (TUZ5 104-04.88, -1.88) after $58B 3Y note auction (91282CPK1) stops through: drawing 3.579% high yield vs. 3.589% WI; 2.85x bid-to-cover vs. 2.66x prior.

- No economic data Monday, Tuesday limited to NFIB Small Business Optimism at 0600ET. Markets open for Veterans Day "holiday" - may weigh on volumes Tuesday.

AUDUSD TECHS: Bear Threat Remains Present Despite S/T Gains

- RES 4: 0.6707 High Sep 17 and a bull trigger

- RES 3: 0.6663 2.0% 10-dma Envelope

- RES 2: 0.6644 76.4% retracement of the Sep-Oct bear leg

- RES 1: 0.6537/0.6618 50-day EMA / High Oct 29

- PRICE: 0.6520 @ 16:31 GMT Nov 10

- SUP 1: 0.6459 Low Nov 5

- SUP 2: 0.6440 Low Oct 14 and key support

- SUP 3: 0.6415 Low Aug 21 / 22 and a bear trigger

- SUP 4: 0.6373 Low Jun 23

Despite Monday’s early gains, a bearish short-term tone in AUDUSD remains intact. The recent breach of the 50-day EMA undermines a recent bullish theme. This has exposed the next key support at 0.6440, the Oct 14 low. Key resistance and a short-term bull trigger is at 0.6618, the Oct 29 high. Initial resistance to monitor is at 0.6537, the 50-day EMA. A clear break of the average would strengthen a bullish case.

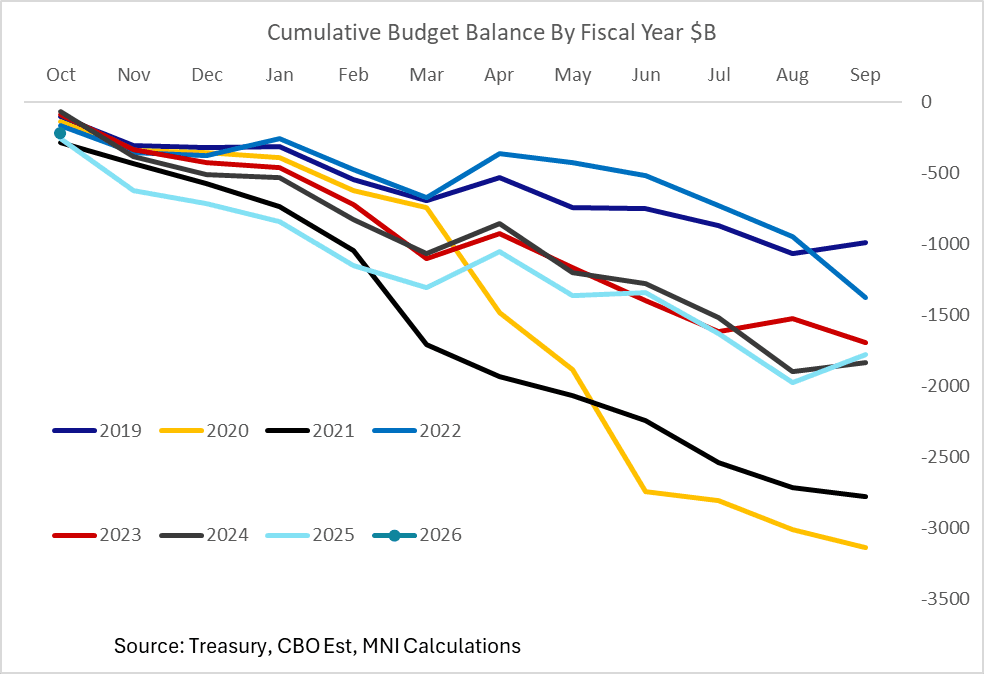

US FISCAL: CBO: October Deficit Shrinks, Shutdown/Timing Issues Muddy Comparison

The Congressional Budget Office estimates that the federal government posted a $219B deficit in October, vs just over $258B a year earlier. This would still be one of the bigger October deficit in recent years but regarding that $39B Y/Y decrease: revenues were up $75B vs a year earlier, "driven by larger collections of individual income and payroll taxes and by increased customs duties", and while outlays were up $37B that was due to a timing shift without which outlays would have decreased (not increased) by $70B vs Oct 2024.

- Overall accounting for timing changes in this first month of the fiscal year, "the decrease in the deficit for October also would have been larger— $145 billion rather than $39 billion. CBO estimates that outlays were smaller than a year ago in part because of the lapse in discretionary appropriations that began on October 1, 2025."

- As such the imminent reopening of the government will probably mean that outlays ramp up shortly to make up for lost ground.

- We should also note that CBO - whose estimates are usually quite accurate - undershot the actual September surplus by $34B, which it attributes to the lack of full data in shutdown: "Because data were not available from many agencies during the lapse in funding, CBO’s estimate of September spending did not account for certain transactions with the Treasury, a number of which were recorded as offsetting receipts."

- Treasury is due to publish its October estimates on Thursday but it's unclear whether it will produce a report even if the shutdown is resolved by then.