MNI ASIA OPEN: Fed Gov Miran Espousing Third Mandate

EXECUTIVE SUMMARY

- MNI US TSYS/SUPPLY: Aggressive Bill Size Increases Continue

- MNI FED: Daly Doesn’t See Potential AI Bubble Threatening Financial Stability -Axios

- MNI US: Jeffries Rules Out 1-Year Obamacare Extension Ahead Of 7th Govt Funding Vote

- MNI US DATA: Redbook Points To Robust Q3 Retail Sales Momentum, Official Data Or Not

- MNI US DATA: Consumer Borrowing Slows, Not Major Tailwind For Consumption

- MNI US DATA: Consumer Inflation Expectations Firm Mildly In September - NY Fed

US

MNI BRIEF: Third Mandate Flows From Dual Mandate Success-Miran

Federal Reserve Governor Stephen Miran said Tuesday the central bank needs to lower interest rates and that stable long term interest rates flow from success in achieving the central bank's dual mandate goals. "Most people think that achieving moderate, long term interest rates will naturally come out of achieving maximum employment and stable prices," he said in Q&A at an event hosted by the Managed Funds Association. "I agree with that. I could imagine there being sort of tail scenarios of the world in which that's not the case. But I don't think that any of those tail scenarios are remotely describing a reality that I see now, or that I would expect to see."

MNI FED: Daly Doesn’t See Potential AI Bubble Threatening Financial Stability -Axios

SF Fed’s Daly gave an AI-focused interview to Axios (full report here), her first public comments since she said on Sep 25 that the policy rate remains modestly restrictive with more cuts needed over time to balance risks. Axios has published an interview with SF Fed’s Daly (non-voter) which it summarizes as saying that “Daly doesn't think a potential AI bubble in the stock market would threaten broader financial stability.”

NEWS

MNI US: Jeffries Rules Out 1-Year Obamacare Extension Ahead Of 7th Govt Funding Vote

Laura Weiss at Punchbowl News reporting that House Minority Leader Hakeem Jeffries (D-NY) has called a potential one-year extension for enhanced Obamacare subsidies a “non-starter”. Comes after Punchbowl reported that Senator Mike Rounds (R-SD) “has talked about doing a one-year clean extension and then a second year with reforms/phase-outs. But this is by no means a majority view among Senate Republicans, and certainly not House Republicans.”

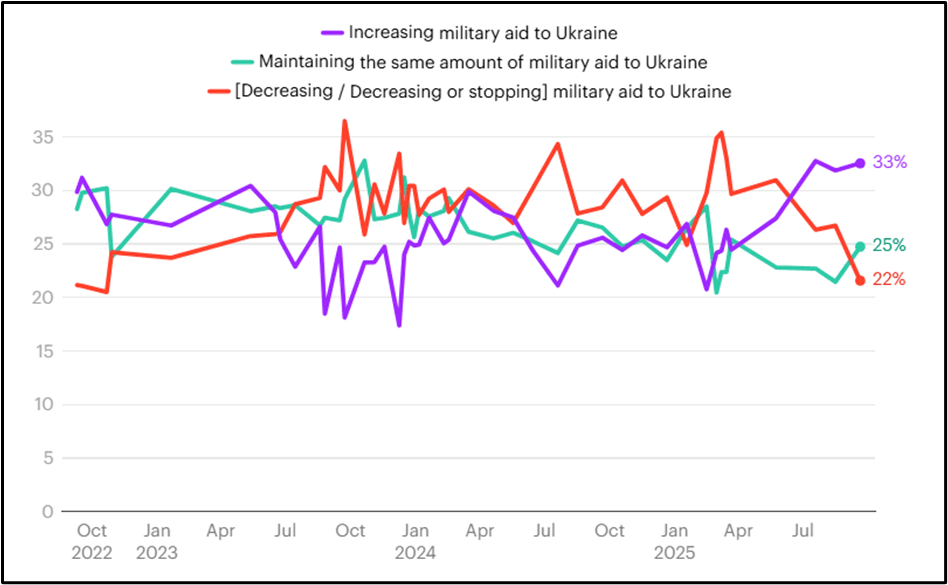

MNI SECURITY: US Opinion Shifts In Favour Of Ukraine Ahead Of Trump-Stubb Meeting

US President Donald Trump will welcome Finnish President Alexander Stubb to the White House on Thursday for a working meeting. Stubb has one of the closest personal relationships with Trump of any European backer of Ukraine.

- A new YouGov survey has found that US adults increasingly support more US military aid to Ukraine. 33% of US adults now believe the US should increase military aid, a reversal from earlier this year when a plurality of US adults believed the US should decrease the level of military aid provided. The survey shows a trend reversal among Republicans, with only 35% of Republican adults supporting decreasing/cutting aid to Ukraine, down from 60% in March. Figure 1: Do you favour the US ...? (% of US adult citizens)

Source: YouGov

MNI RUSSIA: Kremlin-Waiting On US Re: Tomahawks For Kyiv, Would Be Serious Escalation

Reuters reporting comments from Kremlin spox Dmitry Peskov. Regarding the prospect of the US selling long-range Tomahawk missiles to Ukraine, Peskov says, "We need to wait for clearer statements from the US." Adds "It's important to understand that we are talking about missiles that could theoretically be nuclear-capable," (n.b. Ukraine does not possess any nuclear weapons). Peskov says the supply of Tomahawk missiles to Ukraine "would be a serious escalation." Echoes comments from President Vladimir Putin on 5 September, who said the sale of Tomahawks to Ukraine would mark a "completely new, qualitatively new stage of escalation."

US TSYS

MNI US TSYS: Tsys Rise as Risk Sentiment Cools, Focus On Wednesday's FOMC Minutes

- Treasuries unwound early weakness - look to finish higher across the board Tuesday as risk sentiment cooled early in the first half with stocks rejecting new record highs.

- Stocks are holding weaker levels on narrow ranges after SPX and the Nasdaq indexes retreated from new record highs on Tuesday's open. No obvious block or headline driver as rates climbed to new session highs.

- Treasuries briefly extended highs after the Tsy $58B 3Y note auction (91282CPC9) stops through again: drawing 3.576% high yield vs. 3.584% WI; 2.66x bid-to-cover vs. 2.73x prior.

- Tsy Dec'25 10Y contract currently at 112-20 (+7.5) vs. 112-24 high, initial firm resistance to watch is 113-00, the Sep 24 high. A break would be bullish. Curves mixed: 2s10s -.684 at 55.678, 5s30s +.662 at 101.848.

- U.S. government shutdown extended into a 7th day, and a lack of breakthrough by the end of this week will begin to prompt furloughed workers to miss pay checks, adding pressure to lawmakers to come to a resolution.

- Look ahead: September FOMC Minutes, Fed Speak, 10Y R/O.

OVERNIGHT DATA

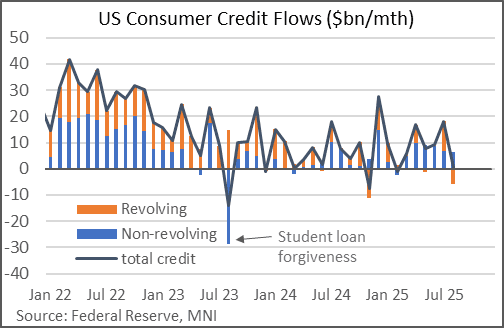

MNI US DATA: Consumer Borrowing Slows, Not Major Tailwind For Consumption

The Fed's latest consumer credit report shows a sharp slowdown in the growth of total credit, to a 6-month low of $363M M/M (or 0.1% M/M). It was well below the $14.0B expected and follows July's $18.0B rise (4.3% M/M) gain, which was upwardly revised from $16.0B.

- The pullback was driven by a $6.0B drop in revolving credit outstanding, the biggest decline in 9 months, partially reversing a $11.2B rise in July. Non-revolving credit continued to rise steadily, by $2.3B (slowest in 4 months but around the prior 6-month average of $1.9B). Recall that revolving makes up 25% of overall consumer credit, largely made up of credit cards; nonrevolving credit is basically made up of student and auto loans.

MNI US DATA: Consumer Inflation Expectations Firm Mildly In September - NY Fed

The NY Fed consumer survey (link) saw inflation expectations on balance increase in September. 1Y and 3Y expectations remain comfortably rangebound whilst the 5Y approach is at the high end of its short historical range.

- 1Y inflation expectations increased 20bps from 3.2% to 3.4% for its highest since April.

- 3Y inflation expectations edged up 5bps on an unrounded basis to 3.05% although remains broadly unchanged having averaged 3.02% since December. 5Y inflation expectations edged up 5bps to 2.97% for its highest since February.

- The report showed that more households report being better off than a year ago but the outlook for the labor market deteriorated.

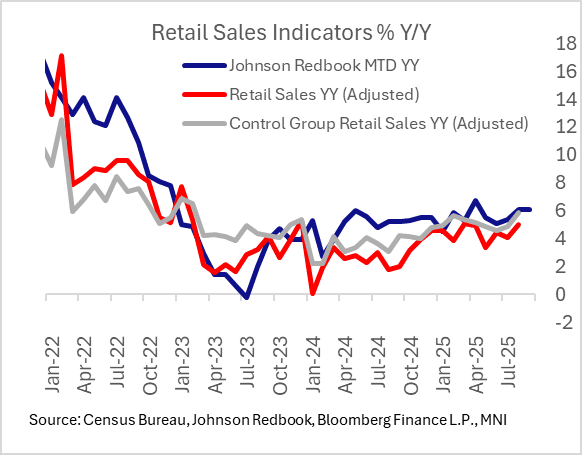

MNI US DATA: Redbook Points To Robust Q3 Retail Sales Momentum, Official Data Or Not

Johnson Redbook Retail Sales rose by 5.8% Y/Y in the week ending Oct 4, bringing growth in the full month of September to 6.1% Y/Y (under their methodology, the month has 5 retail weeks). That's slightly softer than the 6.3% targeted by retailers but would still represent robust sales through the end of Q3.

- Additionally, their preliminary target for October growth (based on retailers' plans) is 5.7% Y/Y.

- It's still uncertain of course, but with every day of the federal shutdown that goes by, it's less and less likely we get the September Census Bureau retail sales report as scheduled on Oct 16.

MNI US DATA: Manheim Car Prices A Little Softer, Downside For CPI

- Manheim used vehicle prices were softer than thought earlier in September, now seen to have dipped -0.2% M/M in the full month release vs a 0.05% M/M increase in the mid-month version. It follows a flat August, in what are relatively small moves after -0.5% in July, 1.6% in June, -1.4% in May and 2.8% in April.

MNI US TSYS/SUPPLY: Aggressive Bill Size Increases Continue

Treasury continued to raise bill auction sizes in Tuesday's announcements, with the 4-, 8-, and 17-week (4-month) bills each seeing offering sizes being boosted to all-time records. On Wednesday Treasury will sell $69B in 17-week bills (up $2B), while Thursday it will sell $110B in 4-week bill (up $5B) and $95B in 8-week bill (up $5B). This will raise $29B in net cash upon settlement next Tuesday, the highest for a bill settlement day since Sept 2.

- While October up-sizings were well-expected and are typical for the month, the increases announced over the last week appear to be coming earlier and bigger than expected. Wrightson ICAP for example this morning wrote "We think the across-the-board increases in the weekly bill offerings announced last week will cover the Treasury’s cash needs over the next few weeks. Accordingly, we look for unchanged offering sizes in this morning’s announcement."

- It's not entirely clear why Treasury has boosted sizes so aggressively - this is likely more about managing cash flows (TGA was still a sizeable $798B yesterday) rather than any insight into fiscal dynamics, but we note that this week's 3-/6-month bill sales were a little soft following respective re-sizings.

MARKETS SNAPSHOT

Key market levels of markets in late NY trade:

DJIA down 91.99 points (-0.2%) at 46602.98

S&P E-Mini Future down 22 points (-0.32%) at 6766.25

Nasdaq down 153.3 points (-0.7%) at 22788.36

US 10-Yr yield is down 2.3 bps at 4.1288%

US Dec 10-Yr futures are up 8/32 at 112-20.5

EURUSD down 0.0059 (-0.5%) at 1.1652

USDJPY up 1.62 (1.08%) at 151.98

WTI Crude Oil (front-month) up $0.39 (0.63%) at $62.08

Gold is up $20.07 (0.51%) at $3980.88

European bourses closing levels:

EuroStoxx 50 down 15.1 points (-0.27%) at 5613.62

FTSE 100 up 4.44 points (0.05%) at 9483.58

German DAX up 7.49 points (0.03%) at 24385.78

French CAC 40 up 3.07 points (0.04%) at 7974.85

US TREASURY FUTURES CLOSE

3M10Y +0.626, 20.72 (L: 17.64 / H: 25.5)

2Y10Y -0.877, 55.485 (L: 54.272 / H: 57.162)

2Y30Y -0.613, 115.117 (L: 114.117 / H: 117.119)

5Y30Y +0.346, 101.532 (L: 100.191 / H: 102.151)

Current futures levels:

Dec 2-Yr futures up 1.375/32 at 104-7.875 (L: 104-05.87 / H: 104-08.625)

Dec 5-Yr futures up 5/32 at 109-9.25 (L: 109-02.5 / H: 109-11.25)

Dec 10-Yr futures up 8/32 at 112-20.5 (L: 112-09 / H: 112-24)

Dec 30-Yr futures up 16/32 at 116-24 (L: 116-01 / H: 117-00)

Dec Ultra futures up 20/32 at 120-7 (L: 119-09 / H: 120-16)

MNI US 10YR FUTURE TECHS: (Z5) Testing Support At The 50-Day EMA

- RES 4: 114-10 High Apr 7 (cont.)

- RES 3: 114-00 Round number resistance

- RES 2: 113-12/29 High Sep 18 / High Sep 11 and the bull trigger

- RES 1: 113-00 High Sep 24

- PRICE: 112-23.5 @ 1325 ET Oct 7

- SUP 1: 112-12+/01 50-day EMA / 50.0% of Jul 15 - Sep 11 upleg

- SUP 2: 111-26 Low Aug 26

- SUP 3: 111-13+ Low Aug 18 and a key support

- SUP 4: 111-01+ 76.4% retracement of the Jul 15 - Sep 11 bull phase

Treasuries continue to trade below last week’s high print of 112-31+ (Oct 3). Attention is on support at the 50-day EMA, at 112-12+. It has recently been pierced but for now remains intact. A clear break of it would undermine a bull theme and signal scope for a deeper retracement towards 111-13+, the Aug 18 low and the next key support. On the upside, initial firm resistance to watch is 113-00, the Sep 24 high. A break would be bullish.

SOFR FUTURES CLOSE

Current White pack (Dec 25-Sep 26):

Dec 25 +0.005 at 96.325

Mar 26 steady00 at 96.520

Jun 26 +0.005 at 96.735

Sep 26 +0.015 at 96.880

Red Pack (Dec 26-Sep 27) +0.020 to +0.025

Green Pack (Dec 27-Sep 28) +0.020 to +0.030

Blue Pack (Dec 28-Sep 29) +0.025 to +0.025

Gold Pack (Dec 29-Sep 30) +0.025 to +0.030

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.15% (-0.03), volume: $2.981T

- Broad General Collateral Rate (BGCR): 4.13% (-0.03), volume: $1.181T

- Tri-Party General Collateral Rate (TCR): 4.13% (-0.03), volume: $1.147T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.09% (+0.00), volume: $84B

- Daily Overnight Bank Funding Rate: 4.09% (+0.00), volume: $164B

FED Reverse Repo Operation

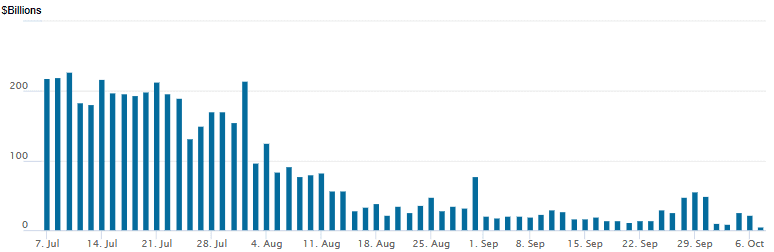

RRP usage retreats to new multi-year low of $4.622B (lowest level since early April 2021) with 14 counterparties this afternoon from $21.776B on Monday. Compares to this year's high usage of $460.731B on June 30.

MNI PIPELINE: Corporate Bond Update: $1.15B TD Synnex 2Pt Launched

$7.85B total to price Tuesday:

- Date $MM Issuer (Priced *, Launch #)

- 10/07 $2.5B *Bank of England 5Y +8a

- 10/07 $1.75B *CPPIB 3Y SOFR+39

- 10/07 $1.75B #Angola $1B +5Y 9.25%, $750M 10Y 10.125%

- 10/07 $1.15B #TD Synnex $550M +3Y +75, $600M 10Y +118

- 10/07 $700M *Türkiye Garanti Bankası 10.5NC5.5 7.625%

MNI BONDS: EGBs-GILTS CASH CLOSE: Curves Reverse Some Of Prior Steepening

Core European yields pulled back slightly Tuesday, with bull flattening across most curves partially reversing Monday's steepening.

- Yields started off on the ascent in morning trade, following on from Monday's weakness (triggered by apprehension over Japanese fiscal expansion following the LDP leadership elections).

- But tthey fell steadily over the course of the European afternoon however, with a sharp pullback in global equities boosting core instruments into the cash close.

- In data, German August factory orders were very weak, driven by softer foreign demand.

- On the day, the German curve leaned bull flatter, with Gilts more clearly bull flattening and outperforming German counterparts.

- Periphery/semi-core EGB spreads widened again, though this time OATs weren't the underperformers, with French spreads steadying after being sent higher after Monday's surprise resignation by PM Lecornu. Instead, Spain and Portugal 10Y/Bund widened 1+bp each.

- Wednesday's calendar includes an appearance by BOE's Pill and ECB's Muller, Elderson and Escriva, and German industrial production data (following on from factory orders).

- However most attention will be on France where ex-PM Lecornu will attempt to break a political deadlock ahead of telling President Macron whether a sustainable coalition government is workable or other alternatives (eg snap elections) should be pursued.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 0.3bps at 2.004%, 5-Yr is down 0.7bps at 2.298%, 10-Yr is down 1bps at 2.709%, and 30-Yr is down 0.3bps at 3.293%.

- UK: The 2-Yr yield is down 0.9bps at 3.983%, 5-Yr is down 0.5bps at 4.148%, 10-Yr is down 1.7bps at 4.719%, and 30-Yr is down 2.1bps at 5.534%.

- Italian BTP spread up 0.6bps at 82.7bps / Spanish up 1.1bps at 54.8bps

MNI FOREX: NZD Slides Into RBNZ Decision, BoJ Hike Patterns in Focus

- Through the London close JPY printing fresh pullback lows, helping trigger a new alltime high for EURJPY for a second session at 176.36. The JPY leg remains dominant for now, and Takaichi's ability to quell concern among junior coalition partners should prove key to any near-term JPY bounce and challenge to the JPY weakening bias.

- BoJ rate hike timing should also prove key here: the fading odds for an October hike have worked against JPY near-term, but more assertive messaging for a December hike may mean JPY weakness is limited here on out. We flagged earlier today the rising risk of a correction lower in JPY

crosses, which now screen overbought in many crosses on the 14-day RSI for the first time since mid-September. - The medium-term run higher in gold has continued, helping spot to new record highs of 3985.7 (although in futures space, COMEX gold has now shown above $4,000 for the first time), but the strength in gold looks pretty isolated: silver, oil prices and base metals are all seen lower, which may be limiting the bounce off lows for AUD/USD, which is yet to bounce back above 0.6600. NZD remains the underperformer into the RBNZ rate decision, and with 36bps of easing priced for Wednesday's meeting and a cumulative 63bps by November, markets may be erring in favour of a more sizeable rate cut this week.

- A return lower for NZD would re-open upside in AUD/NZD through to 1.1355-67 resistance, clearance above which returns focus to the bull trigger and cycle high at 1.1418.

- Despite a strong start to Tuesday trade, equity futures slipped sharply following the opening bell, opening a decent gap with the alltime highs posted across a number of markets in recent weeks. Small cap names underperformed, evident in the Russell 2000 slipping faster than the S&P 500. The government shutdown extended into a 7th day, and a lack of breakthrough by the end of this week will begin to prompt furloughed workers to miss paycheques, adding pressure to lawmakers to come to a resolution. House Dem Leader Jeffries painted a bleak picture of the hopes of near-term talks, suggesting there remains a very large gap between lawmakers on resolving the government shutdown - he noted a proposal to extend ACA credits for one year as "laughable" and unacceptable.

- German industrial production data is the data highlight Wednesday, while the FOMC minutes are set to follow, providing the FOMC's latest views on policy ahead of the government shutdown from one week ago. Several central bank speakers are due, including ECB's Escriva, Muller & Elderson, BoE's Pill and Fed's Musalem, Barr & Kashkari.

WEDNESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 08/10/2025 | 0500/1400 | Economy Watcher's Survey | ||

| 08/10/2025 | 0600/0800 | ** | Industrial Production | |

| 08/10/2025 | 0600/0800 | *** | Flash Inflation Report | |

| 08/10/2025 | 0600/0800 | *** | Flash Inflation Report | |

| 08/10/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 08/10/2025 | 1030/1230 | ECB Elderson In Panel at Finance Conference | ||

| 08/10/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 08/10/2025 | 1320/0920 | St. Louis Fed's Alberto Musalem | ||

| 08/10/2025 | 1330/0930 | Fed Governor Michael Barr | ||

| 08/10/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 08/10/2025 | 1430/1030 | ** | US DOE Petroleum Supply | |

| 08/10/2025 | 1500/1600 | BOE Pill Speech at University of Birmingham | ||

| 08/10/2025 | 1600/1800 | ECB Lagarde Video Message at Werner Report Event | ||

| 08/10/2025 | 1700/1300 | ** | US Note 10 Year Treasury Auction Result | |

| 08/10/2025 | 1800/1400 | FOMC Minutes | ||

| 08/10/2025 | 1915/1515 | Minneapolis Fed's Neel Kashkari | ||

| 08/10/2025 | 2145/1745 | Fed Governor Michael Barr |