MNI ASIA MARKETS ANALYSIS:Pres Trump Touts Buying Stocks Again

HIGHLIGHTS

- Treasuries retreated throughout Thursday's session, higher than expected Unit Labor Cost Rise and rising stocks weighing while 30Y bond auction tail contributed to bear curve flattening.

- The Bank of England Monetary Policy Committee delivered its expected 25 basis point cut at its May meeting, lowering the policy rate to 4.25%, but the committee splintered with a three-way vote on the decision.

- Pres Trump w/ UK PM Starmer announced a "breakthrough" trade deal earlier, details to be worked out over coming months.

- Commerce Sec Lutnick said UK would purchase $10B worth of Boeing planes at Pres Trump's UK trade annc, this will apparently be International Consolidated Airlines Group (IAG).

US TSYS

MNI US TSYS: Near Late Session Lows, Unit Labor Costs Rises, US/UK Trade Deal

- Treasuries look to finish near late Thursday session lows (TYM5 110-26, -23.5 vs. 110-22.5 low), initially triggered by higher than expected rise in Unit Labor Costs and a $25B 30Y bond auction that tailed.

- While Pres Trump's annc of a "breakthrough" US/UK trade deal did little to forestall the steady decline in rates, Pres Trump's suggestion: "better go out and buy stocks now" did help to buoy equity markets through midday.

- Commerce Sec Lutnick said UK would purchase $10B worth of Boeing planes at Pres Trump's UK trade annc, this will apparently be International Consolidated Airlines Group (IAG).

- The BoE lowered the policy rate to 4.25%, but the committee splintered with a three-way vote on the decision.

- Cross asset roundup: Bbg US$ index finished near May 2 highs (BBDXY +8.23 at 1230.92), Gold weaker at 3292.25 (-72.21), Crude firmer (WTI +1.87 at 59.94), while stocks have scaled off second half highs, SPX eminis currently +73.00 at 5725.0.

- Friday look ahead: Data supplanted by return of Fed speakers from media blackout: Barr, Kugler, Williams, Barkin, Waller, Hammack and Cook expected.

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.30% (-0.02), volume: $2.535T

- Broad General Collateral Rate (BGCR): 4.29% (-0.02), volume: $1.060T

- Tri-Party General Collateral Rate (TCR): 4.29% (-0.02), volume: $1.023T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $111B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $298B

FED Reverse Repo Operation

RRP usage recedes to $139.768B this afternoon from $154.859B yesterday, total number of counterparties at 32. Usage had fallen to $54.772B last Wednesday, April 16 -- lowest level since April 2021. Conversely, usage had surged to the highest level since December 31, 2024 on Monday, March 31: $399.167B.

US SOFR/TREASURY OPTION SUMMARY

SOFR & Treasury put option flow continued to revolve around low delta downside puts as underlying rates continued to extend lows through the second half. Curves bear flattened with bonds underperforming after today's $25B 30Y auction tailed. Projected rate cut pricing cools vs. morning levels (*) as follows: Jun'25 at steady at -4.2bp, Jul'25 at -16.7bp (-18.7bp), Sep'25 -34.2bp (-38.4bp), Oct'25 -49.2bp (-55.7bp)

SOFR Options:

-10,000 SFRU5 96.43/96.93 call spds, 5.25

Update, over +55,000 SFRZ5 95.68 puts, 3.5 pit/screen

Block, 5,000 SFRZ5 95.50/95.87 put spds, 5.5 ref 96.40

+20,000 SFRZ5 95.68 puts, 3.5

+5,000 0QM5 97.56 calls, 1.5

1,750 SFRK5 95.75/95.81 put spds ref 95.755

2,000 SFRH6/2QH6 96.00 put spds on 3x2 ratio

3,000 SFRM5 95.81/95.93 put spds ref 95.76

+2,500 SFRM5 95.68/95.81/95.93 put flys, 2.75

+3,000 SFRN5/SFRU5 96.18/96.37 call spd strip 2.0 over -6,000 0QM5 97.00/97.18 call spd

+3,500 SFRN5 95.75/95.87/96.00 put flys, 2.75

+5,750 SFRU5 95.81/SFRZ5 95.68 put spds, 1.5 net/Sep over

-2,000 3QN5 97.00/98.25 call spds, 4.0 ref 96.49

over 4,000 SFRN5 95.87 puts ref 96.11

3,000 SFRM5 95.75 puts, ref 95.755

+3,500 SFRM5 95.75/95.87/96.00 put flys, 2.75

-1,500 SFRK5 95.50/95.62/95.75 put flys, 1.5 ref 95.755

+3,000 SFRM5 95.68/95.75/95.81 put flys, 1.75

-2,000 SFRN5 96.75/97.00 call spds, 1.0 ref 96.125

Treasury Options:

Update, +10,000 TYM/TYQ 112.5 call spds 44

2,000 TYN5 111.5 calls vs. 110.5/111.5 2x1 put spds ref 111-13

4,000 wk5 US 118/120 call spds ref 114-28

over 8,000 wk5 5Y 109.25/109.75 call spds ref 108-19.25

2,100 TYN5 108.5/114.5 strangles ref 111-12.5

Block/screen, -30,000 TYN5 109.5/110.5 put spds 16 ref 111-21

1,500 USQ5 108 puts ref 114-25

+4,700 wk3 TY 110 puts, 4

+2,000 TUN5 104.12/104.87 call spds, 12

-2,500 FVM5 108.25 puts, 15-14.5

+2,500 FVM5 108.75 puts, 30.5-31.5

MNI EGBS: /GILTS CASH CLOSE: Session Lows On Trade Optimism And A Hawkish BoE Cut

- EGBs and Gilts have extended session lows along with equity futures firming through US President Trump’s press conference on the US-UK trade deal.

- Gilts led the sell-off, with moves extending a sharp reaction to a more hawkish than expected BoE earlier today. The latter is clear to see in today’s bear flattening:

- 2Y yields: 12.5bp Gilts, +5.9bp Bunds, +5.3bp OATs, +4.2bp BTPs and +5.4bp for Spain.

- 10Y yields: 8.7bp Gilts, +5.9bp Bunds, +4.3bp OATs, +3.4bp BTPs and +4.5bp for Spain.

- The firmer risk back-drop has supported the periphery, with GGBs 3.5bp tighter and BTPs 2.5bp tighter to Bunds. IRISH leads however at 4.2bp tighter, aided by strong demand at today’s 2034 sale (2x sold vs prior offering) and the trade backdrop considering Ireland’s particular sensitivity.

- BTP-Bund spreads are one standout more broadly, at 104.6bps being right at the low end of recent ranges and last lower in late 2021.

- RXM5 has recently touched session lows of 130-91 (-0.60) to reverse most of yesterday’s gains which saw a high of 131.72. The trend needle has been pointing north, with resistance at a bull trigger of 132.03 (Apr 7 high) but should today’s decline become more entrenched it could see support at 130.58 (50-day EMA).

- EU-focused trade headlines following the US-UK deal: "*TRUMP: WE INTEND TO MAKE A DEAL WITH THE EU […] HOPE TO MEET EUROPE'S VON DER LEYEN” - bbg

- When asked more broadly rather than just EU: *TRUMP: 10% BASE RATE FOR UK NOT A TEMPLATE, WILL BE HIGHER”.

- Earlier today, Bloomberg reported the EU is planning to hit €95 billion of US exports with additional tariffs if ongoing trade talks with Trump’s team fail to yield a satisfactory result.

MNI FOREX: USD Index Rises to Fresh Recovery Highs Amid Sentiment Boost/Patient Fed

- Major equity indices have rallied significantly on Thursday as progress on trade talks/deals provides a more constructive tone for risk sentiment. Outperformance for the US benchmarks is providing a firm underlying bid for the US dollar, with the patient FOMC providing an additional greenback tailwind.

- As a result, the ICE dollar index has risen to fresh recovery highs above 100.50, with the index looking likely to close above its 20-day EMA, the first daily close above this average since February 28 and undoubtedly a bullish development.

- The renewed dollar optimism has been most pronounced against the Japanese yen, particularly benefiting from the 10bp move higher for front-end US yields and the boosted risk backdrop. The 1.3% USDJPY rally has seen the pair narrow the gap substantially to the post-BOJ highs at 145.92, and the key 50-day EMA resistance, intersecting at 146.23. A breach of this average would signal scope for a stronger recovery towards 148.27 (Apr 9 high) and 149.28 (Apr 3 high).

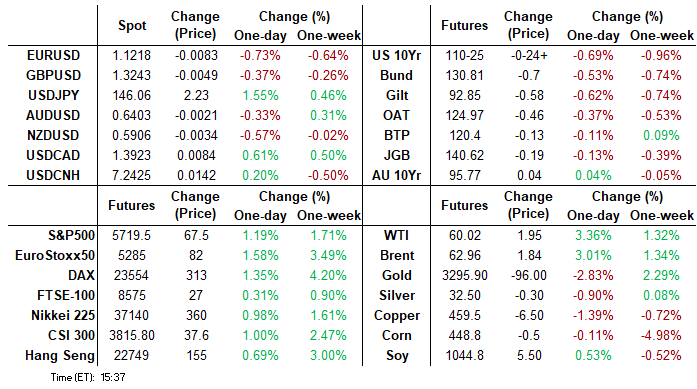

- EURUSD (-0.65%) has printed fresh pullback lows at 1.1221 on Thursday, as downside momentum extended below the May 01 low of 1.1266. The 20-day EMA has also remained key on the EURUSD chart, having supported the pair extremely well since the break higher in early March. A close below 1.1279 would signal scope for a deeper pullback, initially looking for 1.1144, the April 03 high.

- GBP relatively outperforms following a hawkish lean to the May BOE decision. Two votes for an unchanged decision were a surprise, and the seemingly close call for the majority who voted for a 25bp cut garnered support for GBP. The stronger dollar helped cable reverse back to pre-BOE levels, however the half a percent decline for EURGBP remains noteworthy.

- China trade data, Canadian employment and comments from FOMC members will be highlights on the Friday economic calendar.

MNI FX OPTIONS: Expiries for May09 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1200(E992mln), $1.1260(E890mln), $1.1275(E992mln), $1.1300(E1.5bln), $1.1350(E818mln), $1.1375-85(E954mln), $1.1400-10(E1.1bln)

- USD/JPY: Y141.00($1.3bln), Y145.00($2.2bln), Y145.50($688mln), Y146.00($744mln)

- GBP/USD: $1.3125(Gbp615mln), $1.3375(Gbp845mln)

- AUD/USD: $0.6400(A$1.0bln)

- USD/CAD: C$1.3700($1.2bln), C$1.3750($1.3bln), C$1.3990-00($680mln), C$1.4170($1.0bln)

- USD/CNY: Cny7.4000($697mln)

MNI US STOCKS: Late Equities Roundup: Still Well Bid After Pres Trump Endorsement

- Stocks remain well bid after Pres Trump's suggestion: "better go out and buy stocks now" at his UK trade deal annc earlier. Indexes have scaled off second half highs in late trade with the DJIA trading up 501.34 points (1.22%) at 41616.35, S&P E-Minis up 67 points (1.19%) at 5719.25, Nasdaq up 294.8 points (1.7%) at 18033.79.

- Energy and Industrial sectors continued to outperform in late trade, oil and gas shares buoyed the former as crude prices gained (WTI +1.86 at 59.93): Occidental Petroleum +5.84%, Devon Energy +5.74%, Halliburton +4.96%, Diamondback Energy +4.49% and Valero Energy +4.21%.

- Leading gainers in the Industrials sector include: Axon Enterprise surged 14.66% after posting upbeat earnings, Paycom Software +8.96%, Delta Air Lines +6.58%, United Airlines Holdings +6.04% and Dayforce +4.94%.

- Meanwhile, Health Care and Consumer Staples sectors continued to underperform in the second half, pharmaceutical makers weighing on the former: Cencora -4.89%, Cardinal Health -3.06%, McKesson -2.86%, Regeneron Pharmaceuticals -2.45% and Eli Lilly -2.14%. Broadline retailers weighed on the Consumer Staples sector: Dollar General -0.83%, Altria Group -0.67%, Walmart -0.40% and Costco Wholesale -0.15%

- Earnings expected after today's close include: LPL Financial Holdings, Paramount Global, DraftKings, Illumina Inc, Coinbase Global, Microchip Technology, HubSpot, Grindr, Wolfspeed, MARA Holdings, SoundHound AI, Insulet Corp, Rocket Lab USA, McKesson Corp, Expedia, Cloudflare, Sweetgreen, Pinterest and Lyft.

MNI US STOCKS: Boeing Shares Elevated But Off Highs

Boeing shares remain elevated at 192.95 (+7.39, +3.97%) but off earlier high of 194.75 after Commerce Sec Lutnick said UK would purchase $10B worth of Boeing planes at Pres Trump's UK trade annc earlier. Some details via Bbg: "IAG POISED TO ORDER ABOUT 30 787 JETS FROM BOEING", IAG: International Consolidated Airlines Group.

MNI EQUITY TECHS: E-MINI S&P: (M5) Northbound

- RES 4: 5863.74 200-dma

- RES 3: 5837.25 High Mar 25 and a bull trigger

- RES 2: 5773.25 High Apr 2

- RES 1: 5724.75 High May 2

- PRICE: 5685.50 @ 14:27 BST May 8

- SUP 1: 5547.58 20-day EMA

- SUP 2: 5355.25/5127.25 Low Apr 24 / 21 and a key support

- SUP 3: 4996.43 76.4% retracement of the Apr 7 - 10 bounce

- SUP 4: 4832.00 Low Apr 7 and the bear trigger

Trend conditions in S&P E-Minis are unchanged, they remain bullish. The contract has breached the 50-day EMA, at 5624.12. A continuation higher would expose 5837.25 next, the Mar 25 high and a bull trigger. It is still possible that the entire rally since Apr 7 is a correction. A reversal lower would signal the end of this corrective phase and expose initially, support at 5127.25, the Apr 21 low. First support to watch is 5547.58, the 20-day EMA.

MNI COMMODITIES: Crude Rises, Gold Declines As Trade Tensions Ease

- Crude has extended gains today on signs of easing trade tensions, with the US announcing a trade deal with the UK. Looming US-China trade talks on Saturday are also supportive.

- WTI Jun 25 is up by 3.2% at $59.9/bbl.

- OPEC oil output edged lower in April despite a scheduled output hike taking effect, according to a Reuters survey.

- From a technical perspective, a downtrend in WTI futures remains intact and short-term gains are considered corrective. Attention is on $54.67, the Apr 9 low and a bear trigger. Key resistance to watch is $63.73, the 50-day EMA.

- Meanwhile, spot gold has declined by another 1.7% to $3,307/oz, taking total losses over the last two sessions to 3.6% as trade tensions have eased.

- The yellow metal remains 2% higher week-to-date, however, as it has recovered from its recent lows. This recovery suggests that the correction between Apr 22 - May 1, is over.

- A continuation higher would refocus attention on key resistance and the bull trigger at $3,500.1, the Apr 22 high.

- Key short-term support has been defined at $3,202.0, the May 1 low. A break of this level is required to signal scope for a deeper retracement.

- Elsewhere, copper has also fallen by another 1.2% to $460/lb, taking the decline over the last two sessions to 3.6%.

- A continuation of weakness would expose $436.00, the Apr 10 low.

FRIDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 09/05/2025 | 0600/0800 | *** | CPI Norway | |

| 09/05/2025 | 0800/1000 | * | Industrial Production | |

| 09/05/2025 | 0840/0940 | BOE Bailey Keynote Address at Reykjavik Economic Conference | ||

| 09/05/2025 | 0955/0555 | Fed Governor Michael Barr | ||

| 09/05/2025 | 1045/0645 | Fed Governor Adriana Kugler | ||

| 09/05/2025 | 1115/1215 | BOE's Pill At National MPC Agency Briefing | ||

| 09/05/2025 | - | *** | Trade | |

| 09/05/2025 | 1230/0830 | *** | Labour Force Survey | |

| 09/05/2025 | 1230/0830 | New York Fed's John Williams | ||

| 09/05/2025 | 1230/0830 | *** | Labour Force Survey | |

| 09/05/2025 | 1230/0830 | Richmond Fed's Tom Barkin | ||

| 09/05/2025 | 1235/0835 | New York Fed's Roberto Perli | ||

| 09/05/2025 | 1530/1130 | Fed Governor Christopher Waller | ||

| 09/05/2025 | 1530/1130 | New York Fed's John Williams | ||

| 09/05/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 09/05/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 09/05/2025 | 2345/1945 | St. Louis Fed's Alberto Musalem | ||

| 09/05/2025 | 2345/1945 | Fed Governor Michelle Bowman | ||

| 10/05/2025 | 2345/0145 | ECB's Schnabel on Monetary Policy Panel | ||

| 09/05/2025 | 2345/1945 | Cleveland Fed's Beth Hammack | ||

| 09/05/2025 | 2345/1945 | Fed Governor Lisa Cook | ||

| 10/05/2025 | 0130/0930 | *** | CPI | |

| 10/05/2025 | 0130/0930 | *** | Producer Price Index |