MNI ASIA MARKETS ANALYSIS: Ylds Retreat, Heavy Data, Month End

HIGHLIGHTS

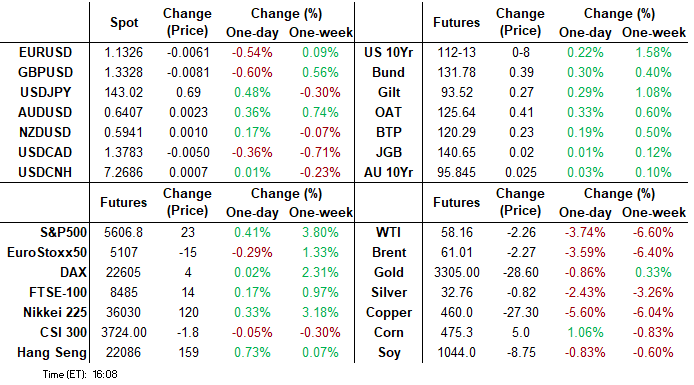

- Treasuries recovered from an early Wednesday sell-off: stronger-than-expected (or at least, less-weak-than-expected) US GDP and PCE inflation data saw 10Y yield rise 4.2254% high.

- Rates and equities rebounded midmorning after solid PCE income growth reflected in the PCE data partially offset by tariff impacts.

- Quiet session for once for the greenback, Bbg US$ index gaining slightly (BBDXY +.97 at 1223.16), crude prices under pressure (WTI -2.33 at 58.09) after Reuters cited Saudi sources that the Kingdom is unwilling to prop up the oil market with further supply cuts.

MNI US TSYS: Tsys & Stocks Break Resistance, Month End Partially Cited

- Treasuries broke through narrow session range late Wednesday, look to finish mostly higher, curves moderately steeper with bonds underperforming all day.

- Early data driven volatility, Tsys tested major resistance after softer than expected April ADP at 62k (sa, cons 115k) after a downward revised 147k (initial 155k) in March.

- Rates and equities reverse course - extended lows after higher than expected GDP Price index, Personal Consumption and Core PCE data. Stocks rebounded after solid PCE income growth reflected in the PCE data partially offset by tariff impacts.

- Jun'25 10Y currently +7.5 at 112-12.5 vs. -16 high (10Y yld currently 4.1562%), resistance at 112-16 (1.0% 10-dma envelope) followed by 113-04 (76.4% retracement of the Apr 7 - 11 bear leg).

- Trade negotiation related headlines continued to deliver real vol to markets, but it appeared late bounce in rates and stocks was at least partially month end related.

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.36% (+0.00), volume: $2.623T

- Broad General Collateral Rate (BGCR): 4.35% (+0.00), volume: $1.059T

- Tri-Party General Collateral Rate (TCR): 4.35% (+0.00), volume: $1.018T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $104B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $273B

FED Reverse Repo Operation

RRP usage jumps to $250.601B this afternoon from $157.537B yesterday. Usage had fallen to $54.772B last Wednesday, April 16 -- lowest level since April 2021. Conversely, usage had surged to the highest level since December 31, 2024 on Monday, March 31: $399.167B. The number of counterparties climbs to 54 from 37 yesterday.

US SOFR/TREASURY OPTION SUMMARY

Option desks reported decent SOFR & Treasury option volumes Wednesday, mixed flow segued to downside puts in the second half. Underlying futures firmer, testing highs late (TYM5 +8 at 112-13 vs. -13.5 high). Curves twisted steeper in late trade (2s10s +3.616 at 55.382). Projected rate cut pricing looks steady to lower vs. early morning levels (*) as follows: May'25 at -1.6bp (-2.6bp), Jun'25 at -17.1bp (-16.7bp), Jul'25 at -41.1bp (-38.1bp), Sep'25 -64.8bp (-59.2bp).

SOFR Options:

Block, 10,000 SFRM5 95.75/95.93 put spds, 10.5 ref 95.91

-10,000 2QU5 97.25/97.31 call spds 1.5 ref 96.845 (unwind of buys from Apr 4)

+3,000 SFRU5 96.50/97.00 call spds 1.75 over 3QU5 96.87/97.25 call spd

-2,500 SFRZ5 96.68 straddles, 73.0 ref 96.69

5,200 SFRM5 95.81/95.87 2x1 put spds

6,000 SFRU5 95.68/95.87/96.00 put flys ref 96.30

Block, 2,500 SFRZ5/0QZ5 96.25 put spds, 4.5

3,000 0QZ5 99.00/100.0 call spds ref 97.00

2,500 SFRH6 97.25/98.25 call spd vs. 2QH6 97.00/98.00 call spd

Block/screen: 7,500 0QM5 97.00/97.25/97.50 call flys

3,000 SFRM5 96.18/96.31 call spds ref 95.90

Treasury Options:

Update, over 33,000 TYN5 108.5/109.5/110.5 put trees ref 112-09.5 to -12.5

12,000 TYM5 110.25/111.5 put spds, 21 ref 112-06.5

1,500 TYM5 109/110 put spds vs. 110.25/111.25 call spds

1,500 TYM5 114/116/118 call flys ref 112-05

-19,500 TYM5 114 calls, 18

3,600 TYM5 112.5 straddles, 157 ref 112-09

Block, 21,000 FVU5 111/114 call spds 29.5 vs. 109-07.75/0.20%

6,250 FVM5 109.25 straddles ref 109-06.25

9,000 wk3 TY 112.25 puts ref 112-09.5

8,000 wk3 FV 109 puts, 31.5 ref 109-02.75 (exp 5/16)

over 8,200 USM5 120 calls & 9,200 USM 124 calls, partially spd

4,000 Wed wkly TY 112.75/113 call spds (exp today)

3,600 TYM5 109/110/111 put flys ref 112-06.5

over 12,000 TYM5 114 calls, 17-18

1,250 FVM5 107.5/107.75/108.25 broken put flys ref 109-02.5

MNI BONDS: EGBs-GILTS CASH CLOSE: Bellies Outperform

European yields fell on a data-heavy Wednesday.

- After some initial overnight weakness, Bunds and Gilts largely looked through higher-than-expected Q1 Eurozone GDP and French and German state-level flash inflation.

- Core instruments would strengthen through the European morning session on weaker equities and oil prices which helped support global FI generally.

- Stronger-than-expected (or at least, less-weak-than-expected) US GDP and PCE inflation data saw core FI pull back sharply, but Bunds and Gilts would rally anew as equities tumbled on US growth fears.

- The German and UK curves leaned bull steeper on the day, with outperformance in the bellies. Periphery EGB spreads widened modestly, with GGBs underperforming.

- Following today's inflation releases, April Eurozone core HICP (Friday) is seen as having upside risks vs the 2.5% Y/Y estimate coming into the week.

- Thursday is a holiday (Labor Day) throughout much of Europe, though in the UK we get consumer credit / money supply / mortgage data, as well as final April Manufacturing PMI.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 5bps at 1.686%, 5-Yr is down 5.9bps at 1.985%, 10-Yr is down 5.3bps at 2.444%, and 30-Yr is down 4.5bps at 2.882%.

- UK: The 2-Yr yield is down 4bps at 3.803%, 5-Yr is down 4.1bps at 3.917%, 10-Yr is down 3.9bps at 4.441%, and 30-Yr is down 3.7bps at 5.207%.

- Italian BTP spread up 1bps at 112bps / Greek up 1.3bps at 85.5bps

MNI FOREX: Dollar Index Holds Narrow Range Following US Data

- The USD index is moderately firmer Wednesday following the plethora of data releases from the US. Slightly softer Q1 US GDP and Chicago PMI prints were countered by higher PCE, which continue to stoke stagflationary concerns for the US economy. However, the data providing a stale picture, month-end flow dynamics and the close proximity to the employment report on Friday have kept overall FX ranges contained.

- Weaker sentiment was greater reflected by the slippage for major equity benchmarks, which has translated into a 0.2% uptick for the DXY to 99.45. The index continues to consolidate below the 100 mark as the underlying bearish USD trend remains intact at this juncture.

- GBP stands out as the weakest performer across G10. The Friday/Monday daily candles for GBP/USD form a tweezer top - the first real bearish candle pattern on the daily chart since January. A further slide in the pair sees first support into 1.3280, ahead of the 20-day EMA at 1.3202.

- Elsewhere, broad EUR weakness played out in the aftermath of month-end, prompting EURUSD to press fresh weekly lows below 1.1330. While the recent pullback in EURUSD is considered corrective and the bullish trend structure is unchanged for now, the pair’s ability to gain traction above 1.14 this week appears a relatively bearish development at the margin.

- A break of the April 23 low at 1.1308 would focus the market on key support at the 20-day EMA (1.1251), of which a break would signal scope for a deeper corrective pullback towards 1.1144 initially.

- Weaker equity sentiment countered higher-than-expected CPI figures in Australia. Notably, AUDUSD has traded either side of the 0.6400 handle for eight consecutive trading sessions, with bullish trend conditions still in play, but the pair unable to build any lasting momentum above the February highs around 0.6410.

- Thursday focus turns to the Bank of Japan decision before US ISM Manufacturing PMI. Liquidity may be negatively impacted as a number of nations will be off for the Labour Day holiday.

MNI FX OPTIONS: Expiries for Apr30 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1375-95(E2.7bln), $1.1425(E500mln)

- USD/JPY: Y140.50($1.9bln), Y142.00($1.8bln), Y144.40-50($959mln), Y145.00($1.5bln), Y148.50($716mln)

- AUD/USD: $0.6115(A$1.1bln), $0.6250(A$702mln)

- NZD/USD: $0.5950(N$521mln)

MNI US STOCKS: Late Equities Roundup: Remain Broadly Weaker But Off Lows

- Stocks remain broadly weaker late Wednesday, off morning lows to near the middle of a wide session range. Currently, the DJIA trades down down 235.06 points (-0.58%) at 40291.68, S&P E-Minis down 44.25 points (-0.79%) at 5539.5, Nasdaq down 187.4 points (-1.1%) at 17273.72.

- Stocks had pared nearly half of the early session losses after solid PCE income growth reflected in the PCE data partially offset by tariff impacts, while pessimistic earnings kept a lid on further dip buying, Caterpillar declined .8% after lowering sales sales targets. Note, Microsoft and Meta trade lower ahead of earnings after the close (*).

- Laggers included Super Micro Computer down over 14.47% after missing earnings expectations late Tuesday, First Solar -9.73%, Garmin -9.50%, CoStar Group -8.72%, Norwegian Cruise Line -8.26%, International Paper -5.28% and Starbucks -6.47% after second quarter sales disappointed.

- Energy stocks retreated as crude prices continued to fall (WTI -2.19 at 58.23): ONEOK -7.20%, Targa Resources -4.95%, APA -4.68%, Kinder Morgan -4.19% and Diamondback Energy -3.73%.

- Some tech, industrial and health care stocks rejected the selloff: Seagate Technology +9.11%, Trane Technologies +7.94%, Western Digital +7.09%, Vulcan Materials +6.41%, PPG Industries +4.48%. Elsewhere, Regeneron Pharmaceuticals gained 4.39% while GE HealthCare Technologies +3.66%.

- *Earnings expected to release after today's close include: Wingstop, Allstate, Host Hotels & Resorts, QUALCOMM, eBay, Teladoc Health, Microsoft Corp, American Water Works, Crown Castle, Align Technology, Meta Platforms, Robinhood Markets, Equinix, Ventas, Albemarle Corp, MetLife, KLA and MGM Resorts.

MNI COMMODITIES: WTI Falls As Saudi Arabia Appears Willing To Sustain Lower Prices

- WTI extended declines today after Reuters cited Saudi sources that the Kingdom is unwilling to prop up the oil market with further supply cuts and can handle a prolonged period of lower prices.

- WTI Jun 25 is down by 3.7% at $58.2/bbl.

- The possible shift in Saudi policy suggests a move towards higher production, targeting market share.

- A medium-term bearish theme in WTI futures remains intact and the latest move down reinforces this theme. Below here, next support is seen at $54.67 the April 9 low and the bear trigger, followed by $53.72, a Fibonacci projection.

- Meanwhile, spot gold has edged down by 0.5% to $3,302/oz.

- This latest move down in gold appears corrective and the trend needle continues to point north. The next objective is $3,547.9, a Fibonacci projection. Initial firm support to watch lies at $3,245.4, the 20-day EMA.

- Elsewhere, copper has fallen by 5.6% to $460/lb amid reports that traders in China were squaring off their positions ahead of the 5-day Labour Day holiday there.

- The move in copper undermines the recent bullish theme and suggests that the rally between Apr 7 - 23 has been a correction. Further weakness would expose $436.00, the Apr 10 low, ahead of $407.40, the Apr 7 low and key support.

THURSDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 01/05/2025 | 0630/0830 | ** | Retail Sales | |

| 01/05/2025 | 0830/0930 | ** | BOE Lending to Individuals | |

| 01/05/2025 | 0830/0930 | ** | BOE M4 | |

| 01/05/2025 | 0830/0930 | ** | S&P Global Manufacturing PMI (Final) | |

| 01/05/2025 | - | *** | Domestic-Made Vehicle Sales | |

| 01/05/2025 | 1230/0830 | *** | Jobless Claims | |

| 01/05/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 01/05/2025 | 1345/0945 | *** | S&P Global Manufacturing Index (final) | |

| 01/05/2025 | 1400/1000 | *** | ISM Manufacturing Index | |

| 01/05/2025 | 1400/1000 | * | Construction Spending | |

| 01/05/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 01/05/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 01/05/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 02/05/2025 | 0130/1130 | * | Producer price index q/q | |

| 02/05/2025 | 0130/1130 | *** | Retail trade quarterly | |

| 02/05/2025 | 0130/1130 | ** | Retail Trade |