MNI ASIA MARKETS ANALYSIS: USD Pulls Back Ahead Of Fed Cut

MNI (NEW YORK) -

HIGHLIGHTS:

- The US dollar came under pressure on the eve of the Fed decision, falling to its weakest level vs the Euro since 2021

- Yields declined across the Treasury curve despite stronger-than-expected US retail sales data, with equities fading recent gains

- Markets are fully discounting 25bp cuts by both the Fed and Bank of Canada Wednesday - MNI previews below

US TSYS: Solid Session On Eve Of Fed Meeting

The short end continued to gain ground Tuesday on the eve of the Fed decision, but notably 10Y, 20Y, and 30Y Treasury yields were on course for their lowest close since April 4.

- Morning data saw Treasuries sell off, with August retail sales coming in on the hot side (as did import prices, offset by lower revisions), with the implied strong consumer dynamics later spurring an upgrade in the Atlanta Fed's GDPNow for Q3 growth to 3.41% from 3.09%.

- However, that would mark the low point of the session, with Treasuries finding a foothold as equities faded.

- The 20Y auction saw a small trade through (0.2bp) along with more encouraging internals, including he lowest dealer takeup since mid-2024. While there was little reaction in broader Treasuries, which had already moved to the session's best levels ahead of the auction, the auction cemented a positive tone for the space heading into Wednesday's Fed decision.

- The short-end/belly outperformed in a bull steepening move overall. Fed rate cut expectations extended very mildly on the day (about 1bp through the next 5 FOMC meetings), with a 25bp cut Wednesday a little over 100% priced, and 68bp total through end-year.

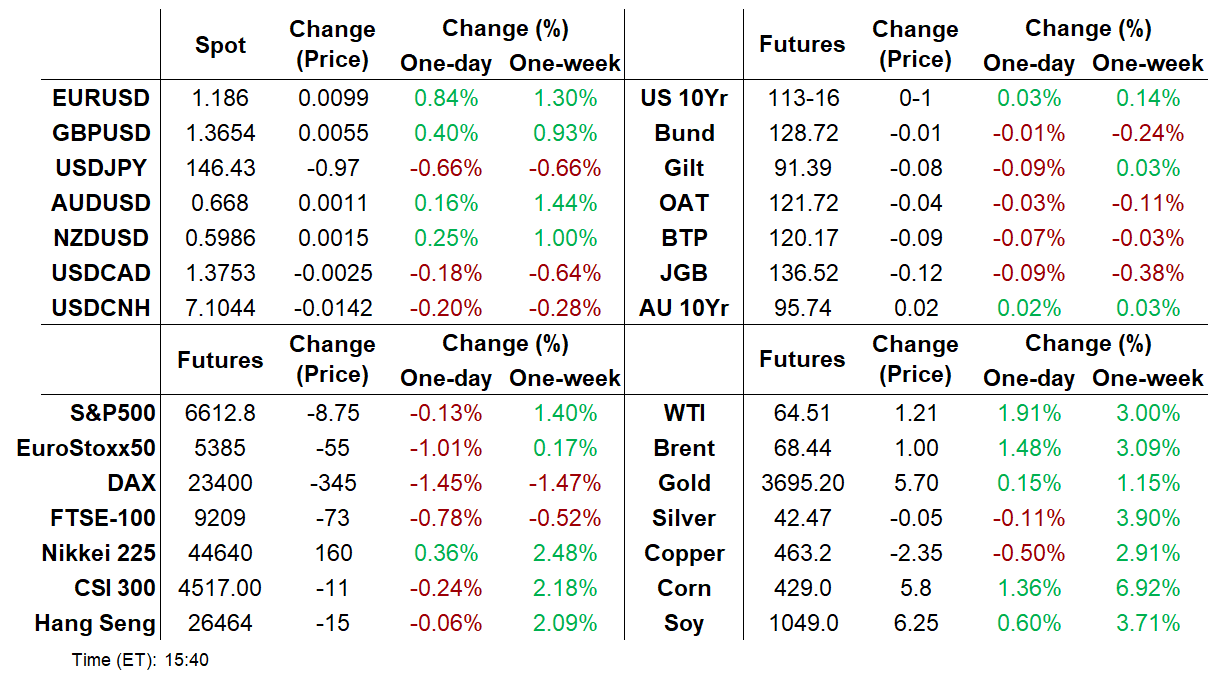

- Latest levels: The 2-Yr yield is down 2.5bps at 3.5116%, 5-Yr is down 1.6bp at 3.5900%, 10-Yr is down 0.6bps at 4.0317%, and 30-Yr is down 1bps at 4.6506%. Dec 10-Yr futures (TY) up 1.5/32 at 113-16.5 (L: 113-8.5 / H: 113-18.5)

- Data is on the light side Wednesday (MBA mortgage apps and housing starts/permits), leaving the stage clear for the FOMC decision and projections and Chair Powell's press conference. Besides the expected cut (and outside chance of 50bp), there will be with attention on any shift lower in the 2025 rate "Dots" as well as potential dissents. Much more in our preview here.

MNI Fed Preview-September 2025: A Reluctant Return To Easing

- The Federal Reserve is set to resume its easing cycle at the September 16-17 meeting with a 25bp cut to the funds rate range to 4.00-4.25%.

- The decision to cut after a 5-meeting pause was well-telegraphed by Chair Powell, whose Jackson Hole speech described a “shifting balance of risks” toward a weaker labor market that “may warrant adjusting our policy stance”.

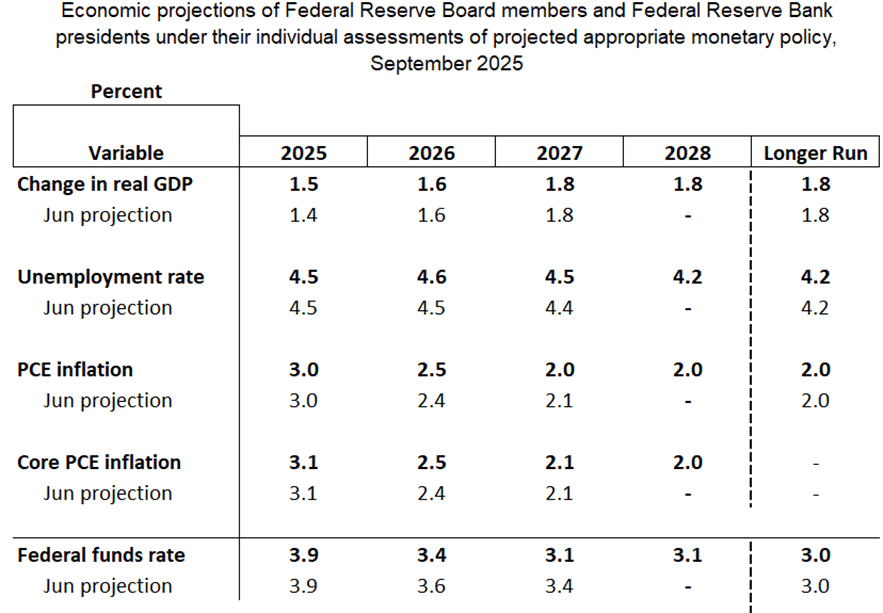

- The updated quarterly projections aren’t likely to bring many changes to the macroeconomic variables, but as usual the signal sent from the Fed rate “Dot Plot” will garner attention. A Committee split between expecting one or two further cuts this year is likely, keeping each of the remaining meetings of 2025 “live”.

- The Statement will downgrade the description of the labor market to reflect a rise in the unemployment rate and poor payrolls growth, and is likely to include at least one dissent to the rate decision.

- But with a Committee that is fairly divided on the way forward, Powell will be noncommittal on future action, reiterating that policy is not on a preset course, and upcoming decisions will be data-dependent.

- A key undercurrent is an increasingly activist approach to Fed personnel management from the White House, which leaves the composition of the FOMC uncertain not just over the medium-term but also at this meeting.

- All but 2 analysts expect a 25bp cut at the September FOMC, based on 32 sell-side previews MNI saw.

- Standard Chartered and Societe Generale expect the FOMC to cut by 50bp.

MNI BoC Preview-Sept 2025: Cuts To Resume On Softening Data

- The Bank of Canada is expected to cut its benchmark overnight rate by 25bp to 2.50% on Wednesday September 17. This comes after three consecutive holds, amid a period in which activity and labour market data proved more resilient than expected in the face of the US-Canada trade conflict.

- Data since the July meeting have been almost unambiguous in tilting the balance toward a further easing, culminating with softer core CPI trends in August’s inflation report released on the eve of the decision.

- Almost all Canadian analysts expect a 25bp cut to be announced Wednesday.

- A 25bp reduction would bring rates toward the lower end of the BOC’s estimated neutral range.

- With no Monetary Policy Report released at this meeting and thus no new economic projections, there will be initial attention on the decision statement which is expected to remain non-committal on future cuts but retain the overall easing bias. That’s a tone likely to be echoed at the press conference.

- While Governing Council’s message will probably reiterate they are proceeding “carefully” with a meeting-by-meeting approach, the overall meeting communications will leave the door open to another rate cut in October if data continue to develop in a similar direction over the interim period.

- Views on the BOC terminal rate are split between those analysts who see one further cut beyond this week (2.25% terminal), and those who see two more (2.00%, so slightly below what would largely be considered neutral). That matches markets pricing between 1 and 2 cuts by end-2026 in addition to this week’s.

MNI BCB Preview – Sep 25: Copom To Maintain Hawkish Messaging

- Analysts are unanimous that the Copom will leave the Selic rate unchanged at 15.00% for a second consecutive meeting on Wednesday, as it maintains its high for longer stance.

- Although inflation has continued to edge lower, it remains well above target, while unanchored inflation expectations are still a concern for the Board, despite a further gradual improvement.

- As such, there are unlikely to be any surprises in the post-meeting statement, given the firm guidance of maintaining the Selic rate at current levels for “a very prolonged period” to ensure the convergence of inflation to target.

- Many analysts only see the easing cycle beginning in the first quarter of next year, although some still see risks of an earlier move.

SOFR FIXES AND PRIOR SESSION REFERENCE RATES

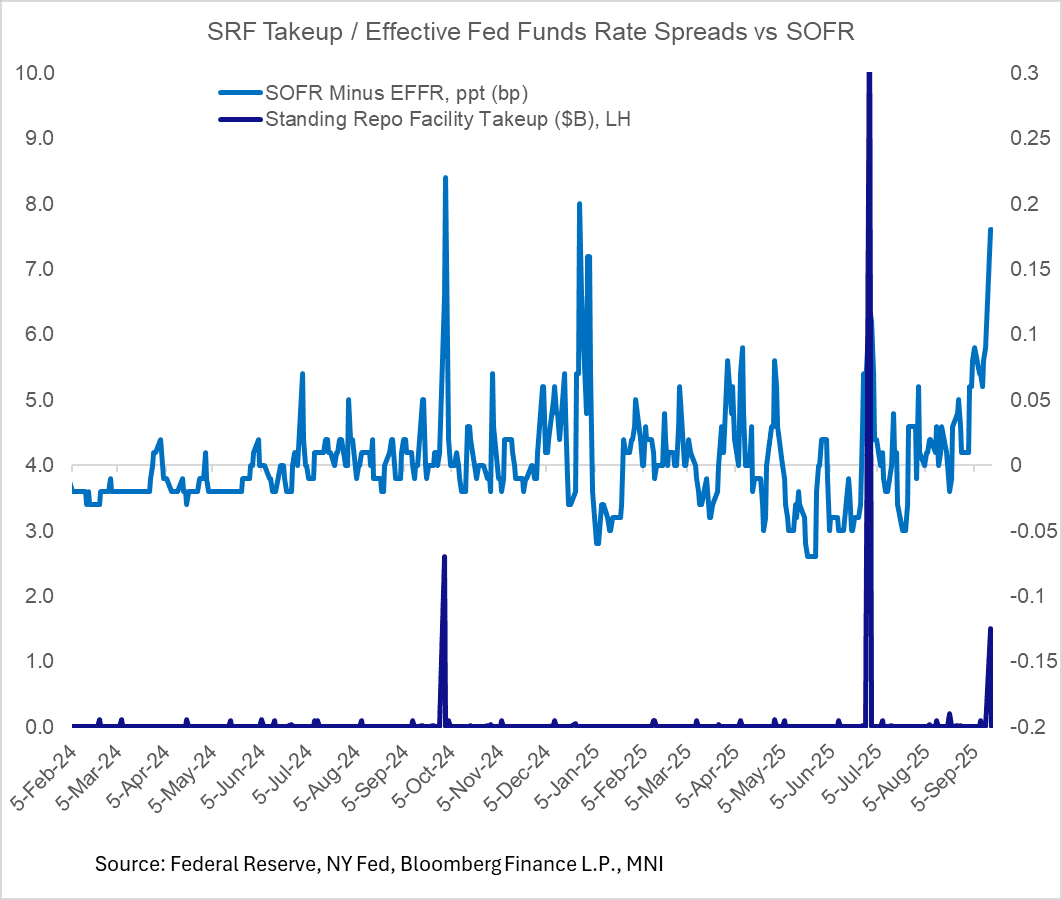

US TSYS/OVERNIGHT REPO: Repo Market Pressure Ahead Of Possible FOMC QT Talks

Secured rates rose sharply Monday, with SOFR rising 9bp to 4.51%. That was the highest rate outright and biggest spread to EFFR of 2025 so far (last exceeded in December 2024).

- It's also notable that we saw the biggest takeup of the Fed's standing repo facility ($1.5B) Monday since end-June (which was a month- and quarter-end). That's reversed today with barely any SRF takeup.

- Monday's pressures were partly a result of an important tax date. It was probably also exaggerated by a net $78B Treasury coupon settlement, which should reverse to some extent Tuesday with just under $50B of net TBill paydowns due.

- Amid the funding market pressures as reserves wind down, however, attention turns to Wednesday's FOMC press conference, with some expectations that Powell could acknowledge that the Committee discussed ending QT in its 2 day meeting starting today (Goldman Sachs sees QT ending at the October meeting).

REPO REFERENCE RATES (rate, change from prev. day, volume):

* Secured Overnight Financing Rate (SOFR): 4.51%, 0.09%, $2877B

* Broad General Collateral Rate (BGCR): 4.50%, 0.1%, $1136B

* Tri-Party General Collateral Rate (TGCR): 4.50%, 0.1%, $1097B

New York Fed EFFR for prior session (rate, chg from prev day):

* Daily Effective Fed Funds Rate: 4.33%, no change, volume: $91B

* Daily Overnight Bank Funding Rate: 4.33%, no change, volume: $181B

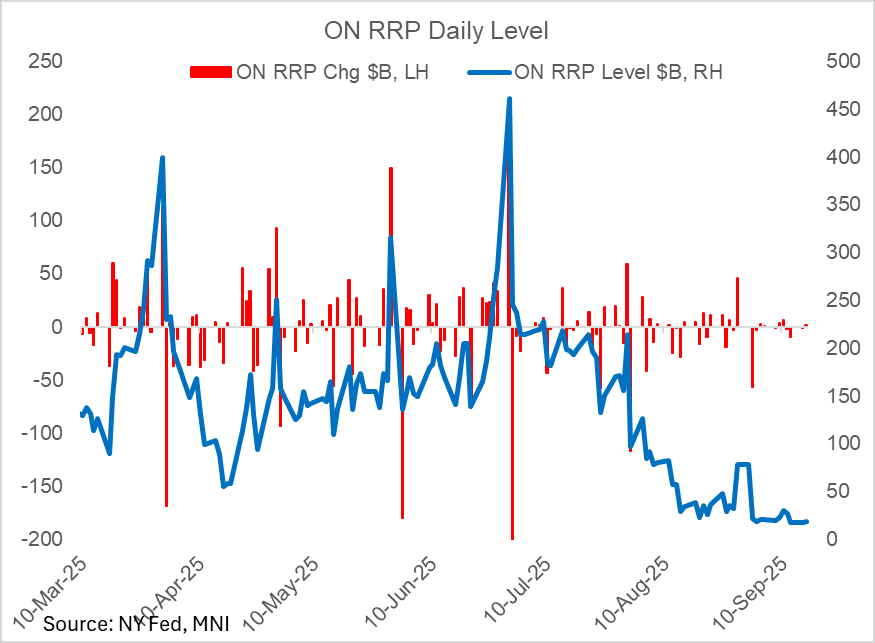

US TSYS/OVERNIGHT REPO: ON RRP Takeup Ticks Up From Multi-Year Low

Overnight reverse repo facility takeup ticked up for the first session in the last four, but remained near post-2021 lows.

- A $1.9B rise Tuesday from Monday's post-April 2021 low brought takeup to $18.8B.

- That left takeup still flatlining vs the habitual $100B+ levels seen prior to August, and is likely to remain around low levels until month-end when the usual month-/quarter-end pressures tend to increase takeup.

US Options Roundup: Sep 16 2025

Tuesday's US rates/bond options flow included:

- SFRV5 95.75/95.87/96.00c fly, traded flat in 5k (on block)

- SFRV5 95.87c, traded for 47.5 in 2k

- SFRX5 96.62/96.75cs, bought for 1 in 10k total

- SFRZ5 96.00 puts 23K given at 1.0 over several clips

- SFRZ5 96.37/96.50/96.56/96.68c condor, traded 2.25 in 2.5k

- SFRZ5 96.50/96.37/96.25p ladder, traded 2.25 in 2.5k

- 0QH6 97.00/96.75ps vs 3QH6 96.75/96.50ps, traded flat in 1.5k

- 0QH6 96.87/96.75/96.37/96.25p condor, bought for 3.5 in 1.5k

- 0QZ5 97.00/98.00 call spread sold at 21 in 7.25k

BONDS: EGBs-GILTS CASH CLOSE: UK Curve Belly Underperforms Pre-CPI

EGBs and Gilts traded mixed Tuesday amid key UK data releases and ahead of the Fed and BoE decisions.

- Yields picked up in morning European trade, with Gilts weighed down in particular by firmer-than-anticipated aspects of the latest UK labour market report.

- Yields would peak in early afternoon after US retail sales data printed much stronger than expected, but would subsequently subside over the rest of the European cash session, as a pullback in equities renewed a bid for core FI.

- DMO announced a reduction in the size of 30Y Gilt auctions, helping the UK curve flatten toward the end of the session.

- Elsewhere in data, Euro area industrial production increased in July in line with expectations, while the September German ZEW survey's expectations component was much stronger-than-expected.

- The German curve twist steepened, with the UK's twist flattening with underperformance in the belly. Periphery/semi-core EGB spreads were little changed on the day.

- Wednesday's European calendar highlight is the UK CPI release (MNI preview here) though there will be global interest in the Federal Reserve meeting after the close as well as multiple ECB speakers (including Lagarde), with the BoE decision looming Thursday.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 1.6bps at 2.002%, 5-Yr is down 1.1bps at 2.285%, 10-Yr is up 0.2bps at 2.693%, and 30-Yr is up 1.5bps at 3.275%.

- UK: The 2-Yr yield is up 1.1bps at 3.964%, 5-Yr is up 1.8bps at 4.079%, 10-Yr is up 0.6bps at 4.639%, and 30-Yr is down 0.9bps at 5.453%.

- Italian BTP spread up 0.1bps at 78.5bps / French OAT spread up 0.5bps at 79.6bps

OPTIONS: Busy Session For Euribor And Sonia Leans Toward Upside Tuesday

Tuesday's Europe US rates/bond options flow included:

- RXV5 127.50p, bought for 10 in 3k

- ERH6 98.125/98.25/98.4375/98.625c condor, bought for 2.5 in 5k

- ERM6 98.3125c, bought for 4 in 10k total

- ERX5 98.00/98.0625/98.125/98.1875c condor, bought for 0.75 in 3.5k

- ERZ5 98.00/97.875/97.75p ladder, sold at 3.75 in 5k

- 2RX5 97.6875/97.8125cs vs 3RX5 97.5625/97.6875cs, bought the 2yr for 1.75 and 2 in 18k total

- SFIZ5 96.15/20/25/30 call condor bought for 0.5 in 3k

- SFIZ6 97.25/97.75cs x5 vs 96.25p x1, bought the cs for 3 in 1.75k (8.75k x 1.75k)

- SFIZ6 97.25/97.75cs, bought for 4.25 in 3.75k

FOREX: Dollar Weakness Extends, EURUSD at Four-Year Highs

- USD weakness picking up momentum in recent minutes as EURUSD (+0.65%) extends to fresh four-year highs above 1.1829. As noted, the stealthy appreciation leading into the Fed will be providing confidence for those looking for the next leg higher for the pair, with several sell-side analysts continuing to hold strong with year-end forecasts of 1.20 and above.

- Clearance of this hurdle confirms a resumption of the primary uptrend and it’s worth noting the Sep 10 2021 high comes in just above current spot at 1.1851.

- For USDJPY (-0.54%), we are also currently plumbing new session lows at typing, around 146.60. This narrows the gap to key short-term support at 146.21, the Aug 14 low and a bear trigger. A break of this level would highlight a stronger bearish threat and highlight a range breakout.

DATA/EVENTS CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 17/09/2025 | 0600/0800 | ** | Unemployment | |

| 17/09/2025 | 0600/0700 | *** | Consumer inflation report | |

| 17/09/2025 | 0730/0930 | ECB Lagarde at ECB Annual Research Conference | ||

| 17/09/2025 | 0800/1000 | ECB Cipollone At Associazione Bancaria Italiana EC Meeting | ||

| 17/09/2025 | 0900/1100 | *** | EZ HICP Final | |

| 17/09/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 17/09/2025 | 1115/1315 | ECB Cipollone Speaks at Netherlands Central Bank Resilience Conference | ||

| 17/09/2025 | 1230/0830 | * | International Canadian Transaction in Securities | |

| 17/09/2025 | 1230/0830 | *** | Housing Starts | |

| 17/09/2025 | 1230/0830 | *** | Housing Starts | |

| 17/09/2025 | 1345/0945 | *** | Bank of Canada Policy Decision | |

| 17/09/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 17/09/2025 | 1430/1030 | BOC press conference | ||

| 17/09/2025 | 1430/1030 | ** | US DOE Petroleum Supply | |

| 17/09/2025 | 1800/1400 | *** | FOMC Statement | |

| 18/09/2025 | 2245/1045 | *** | GDP | |

| 18/09/2025 | - | NorgesBank Meeting | ||

| 18/09/2025 | - | Bank of Japan Meeting | ||

| 18/09/2025 | 2350/0850 | * | Machinery orders | |

| 18/09/2025 | 0130/1130 | *** | Labor Force Survey |