MNI BoC Preview-Sept 2025: Cuts To Resume On Softening Data

Sep-16 2025 15:15By: Tim Cooper

CanadaBank of Canada

Hidden PDF

EXECUTIVE SUMMARY:

- The Bank of Canada is expected to cut its benchmark overnight rate by 25bp to 2.50% on Wednesday September 17. This comes after three consecutive holds, amid a period in which activity and labour market data proved more resilient than expected in the face of the US-Canada trade conflict.

- Data since the July meeting have been almost unambiguous in tilting the balance toward a further easing, culminating with softer core CPI trends in August’s inflation report released on the eve of the decision.

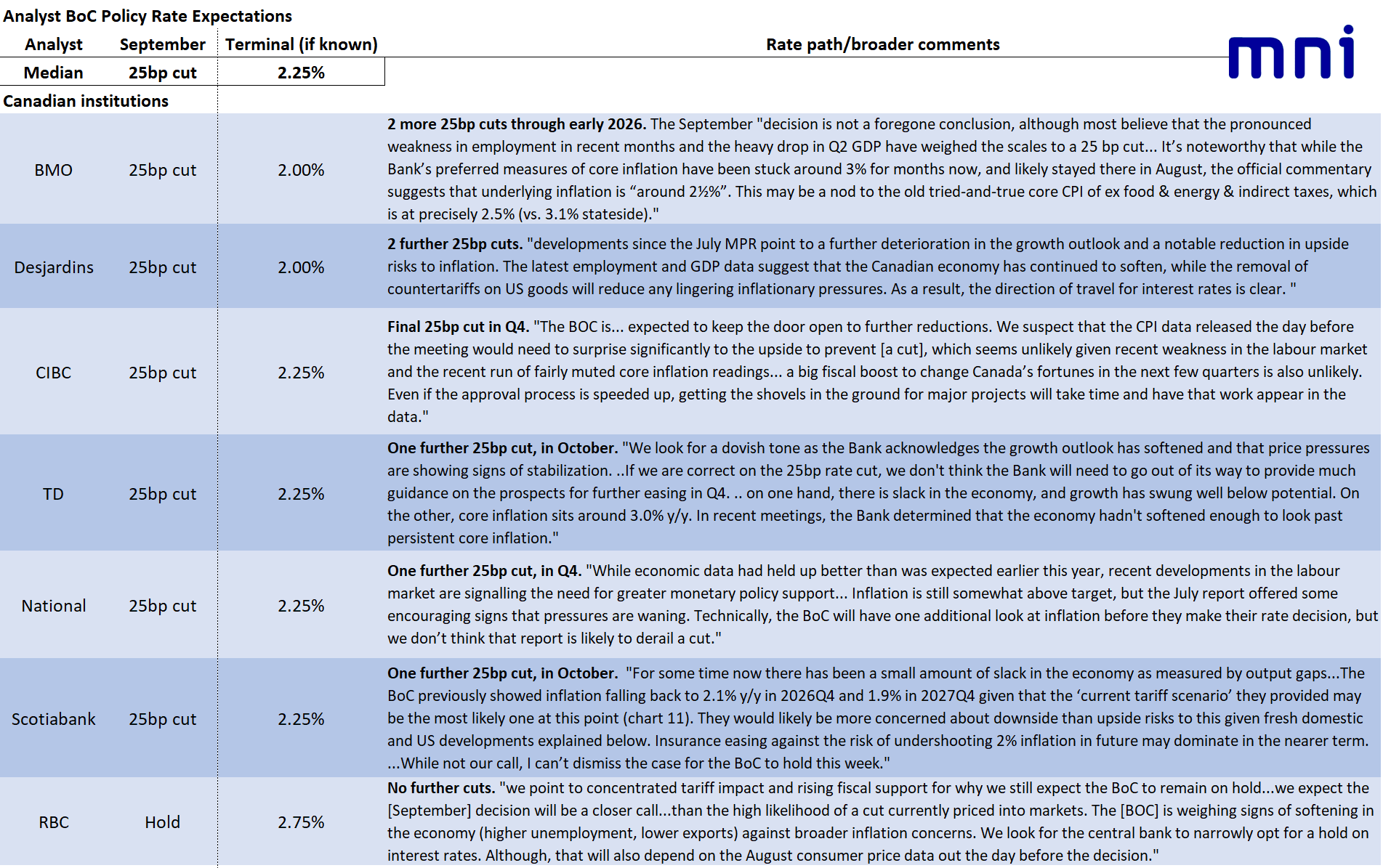

- Almost all Canadian analysts expect a 25bp cut to be announced Wednesday.

- A 25bp reduction would bring rates toward the lower end of the BOC’s estimated neutral range.

- With no Monetary Policy Report released at this meeting and thus no new economic projections, there will be initial attention on the decision statement which is expected to remain non-committal on future cuts but retain the overall easing bias. That’s a tone likely to be echoed at the press conference.

- While Governing Council’s message will probably reiterate they are proceeding “carefully” with a meeting-by-meeting approach, the overall meeting communications will leave the door open to another rate cut in October if data continue to develop in a similar direction over the interim period.

- Views on the BOC terminal rate are split between those analysts who see one further cut beyond this week (2.25% terminal), and those who see two more (2.00%, so slightly below what would largely be considered neutral). That matches markets pricing between 1 and 2 cuts by end-2026 in addition to this week’s.