MNI Fed Preview-September 2025: Analyst Outlook

Sep-15 16:52By: Tim Cooper

USFederal Reserve

Download Full Report Here

This update of our September 12 Fed preview includes analyst expectations - starting page 36.

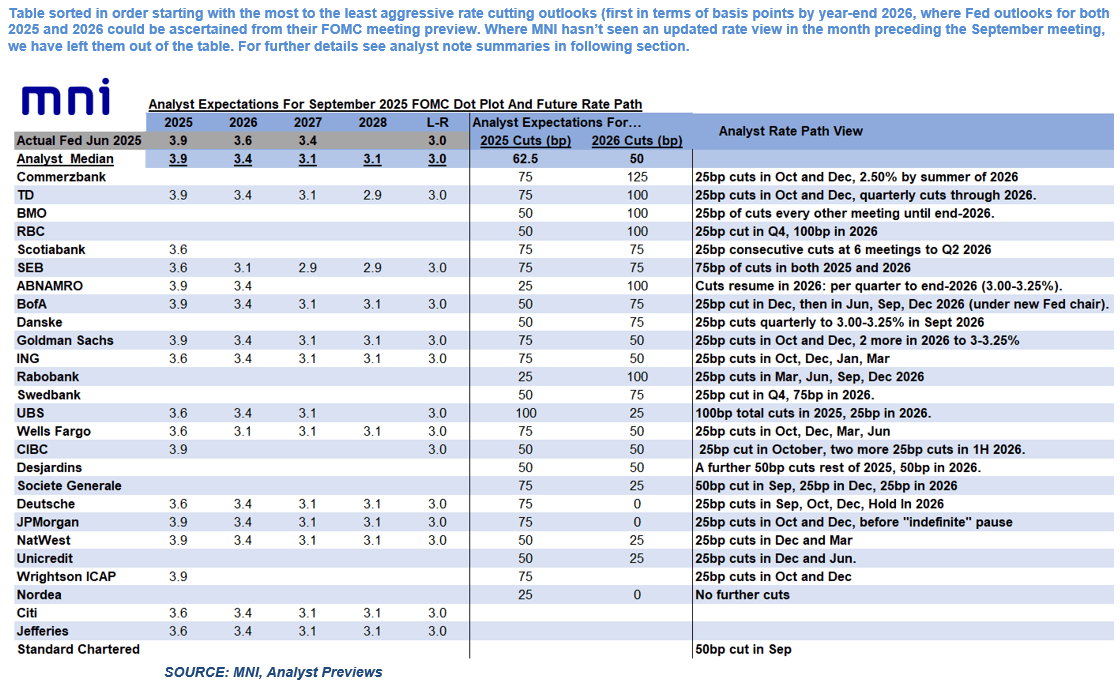

September 2025 FOMC Analyst Views: 2 Or 3 Cuts This Year

All but 2 analysts expect a 25bp cut at the September FOMC, based on 32 sell-side previews MNI saw.

- Standard Chartered and Societe Generale expect the FOMC to cut by 50bp.

- Most analysts who expressed an opinion believe that Gov Miran (if confirmed in time for the decision) will dissent in favor of a 50bp or greater cut, with potential for 2 or 3 total dovish dissents (Waller/Bowman).

- Risks of a dissent toward a hold are seen as limited (candidates: Schmid, Goolsbee, Musalem).

- SEP/Dot Plot: Analysts see a slightly lower “dot” profile in the Fed funds medians vs the last edition in June. For 2025 the median is narrowly in favor of a 3.9% (unchanged) end-year median, though many see 3.6%. For 2026 most see 3.4% (down from 3.6% in June), moving to 3.1% by end 2027 (down from 3.4% in June). No analyst sees the longer-run rate changing (3.0%).

- Analysts see the macroeconomic projections remaining relatively unchanged.

- Statement: The statement is widely expected to revise the language around the characterization of the labor market, to reflect the rise in unemployment and slowdown in payrolls growth.

- There are no expectations that the Fed will change the language re the description of inflation, or the 2nd paragraph’s balance of risks. However we saw one expectation that the Fed could alter the forward guidance sentence (Citi: To remove “and timing”).

- Future action: Expectations for total easing in 2025 (including September’s rate cut) ranges from 25bp (ABN Amro, Rabobank, Nordea) to 100bp (UBS). However, the median is 62.5bp, implying a split between 50 and 75bp of easing in 2025 – mirroring expectations of the Dot Plot.

- The median for total cuts by end-2026 is 125bp, ranging from 25bp to 200bp.