MNI ASIA MARKETS ANALYSIS: Twisting Steeper, Stable Inflation

HIGHLIGHTS

- Treasuries look to finish mixed Friday, curves twisting steeper after intermediates to bonds reversed this morning's post-data highs (personal income & spending higher than exp, Core PCE steady).

- Renewed optimism for the dollar remained the theme of the week - despite Friday's retreat, market participants will be wary of next week’s busy calendar, culminating in the September US jobs report.

- Major US equity indexes are drifting higher again late Friday, nearing early session highs after this morning's relatively stable PCE inflation data buoyed risk appetites.

US TSYS

MNI US TSYS: TSY Roundup: Curves Twist Steeper as Rate Cut Pricing Gains Slightly

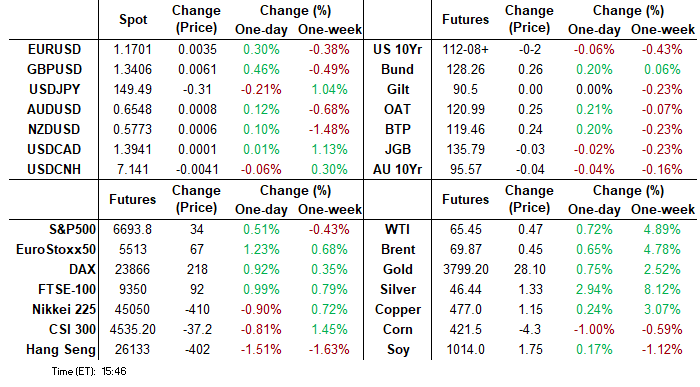

- Treasuries look to finish mostly lower - off this morning's post data highs, curves twisting steeper (2s10s +2.558 at 53.803) with short end rates outperforming. As such - projected rate cut pricing gained momentum vs. early morning levels (*): Oct'25 at -22.4bp (-21.5bp), Dec'25 at -40.5bp (-39.0bp), Jan'26 at -49.9bp (-47.7bp), Mar'26 at -59.9bp (-57.5bp).

- Treasury futures whipsawed lower but quickly reversed to session highs after personal income/spending came out slightly higher than expected, PCE/Core PCE in-line with expected rises. August's core PCE reading of 0.227% M/M was basically exactly in line with expectations (0.22% MNI median), and came with a downward revision to July's figure (now 0.235%, was (0.273%). That marks the slowest monthly M/M print in 4 months.

- Tsys followed Bund's lower at midmorning only to rebound after UofM sentiment and inflation expectations come out slightly lower than expected. The headline sentiment index came in at 55.1 (55.4 prelim, 58.2 August), with economic conditions at 60.4 (61.2 prelim, 61.7 prior) and expectations 51.7 (51.8 prelim 55.9 prior). The inflation expectations were revised down: 1Y to 4.7% from 4.8%, and 5-10Y to 3.7% from 3.9%.

- Currently, the Dec'25 10Y trades -2.5 at 112-08 (yld 4.18172 +.0174) - initial support at 112-01 (50.0% retracement of the Jul 15 - Sep 11 bull phase); resistance above at 113-00 (High Sep 24).

- Overall, renewed optimism for the dollar has been the theme of the week, although market participants will be wary of next week’s busy calendar, culminating in the September US jobs report.

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.18% (+0.05), volume: $2.965T

- Broad General Collateral Rate (BGCR): 4.17% (+0.05), volume: $1.141T

- Tri-Party General Collateral Rate (TCR): 4.17% (+0.05), volume: $1.112T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.09% (+0.00), volume: $92B

- Daily Overnight Bank Funding Rate: 4.09% (+0.00), volume: $194B

FED Reverse Repo Operation

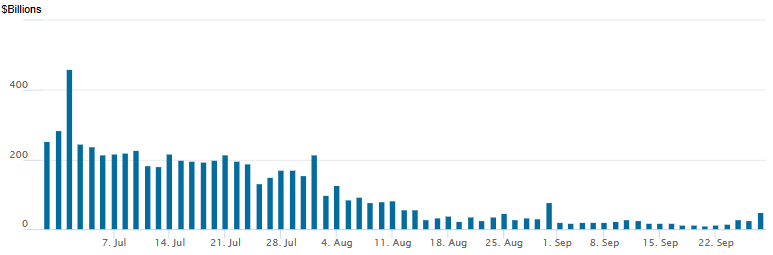

RRP usage surges to $48.073B ahead month end with 23 counterparties this afternoon from $25.369B Thursday. Compares to $11.363B on Friday, September 16 - lowest level since early April 2021. The year's high usage stands at $460.731B on June 30.

US SOFR/TREASURY OPTION SUMMARY

SOFR/Treasury option volumes remained strong, generally better calls on net with some large low delta puts trading in the second half. Underlying futures are mixed after the bell - well off knee-jerk/post-data highs. Curves twisted steeper, however, with short end rates outperforming. As such - projected rate cut pricing gained momentum vs. early morning levels (*): Oct'25 at -22.4bp (-21.5bp), Dec'25 at -40.5bp (-39.0bp), Jan'26 at -49.9bp (-47.7bp), Mar'26 at -59.9bp (-57.5bp).

SOFR Options:

Block, 5,000 SFRV5 96.06 puts, cab

over 21,000 SFRZ5 95.87 puts, cab

+4,000 3QV5 96.50 puts, 4.0 vs. 96.57 to -.575/0.30%

+8,000 0QZ5 97.00/97.06/97.18/97.25 call condors, 1.0 vs. 96.895 to -.88/0.05%

+2,500 0QZ5 97.00 puts, 23.5 vs. 96.875/0.62%

+5,000 SFRZ5 96.50/96.75 2x1 call spds (wrong way), 3.75 ref 96.27

+2,000 SFRH6 96.43 straddles, 31.75-32.0

-12,000 SFRZ5/SFRH6 96.43 call spds, 12.75 (Mar over)

Block/screen, +20,000 0QZ5 97.75 calls, 1.0

+2,000 SFRZ5 96.37/96.50/96.62 call flys, 2.0 ref 96.27

over 7,500 SFRZ5 96.62/96.68 call spds ref 96.265 to -.27

3,000 SFRZ5 96.00/96.37 1x3 call spds ref 96.275

-5,000 SFRZ5 95.75/96.00/96.25 put trees, 7.0

4,000 SFRZ5 96.18/96.31/96.50/96.62 call condors ref 96.27

4,000 SFRZ5 97.00 calls, 1.0-0.75

3,600 SFRV5 96.06/96.12 put spds ref 96.26 to -.265

Block/screen, +7,500 0QZ5 97.00 calls vs. 3QZ5 96.75 calls, 0.0-0.5

Block, +4,000 SFRZ5 96.50/96.62 call spds, 0.75

-6,000 SFRV5 96.31 calls, 2.0 vs. 96.25/0.10%

+2,000 SFRZ5 96.06/96.18/96.25/96.31 broken put condors 0.5

-4,500 0QX5 96.87/97.12 strangles, 17.5 ref 96.86

2,000 SFRV5 96.12 puts, 0.5 ref 96.27

Treasury Options:

Block, +18,000 FVX5 108.5/109.5 call over risk reversals, 0.5 vs. 108-31.75/0.60%

4,800 TYZ5 110/114 strangles, 35 ref 112-08.5

7,000 TUZ5 105 calls, 2.5ref 104-04

+52,000 wk2 Tuesday US 109 puts, 1 ref 116-03 (exp 10/7)

over +58,000 USX5 104 puts, 1-2 ref 116-06 to -04

3,600 TYX5 109/109.5/110 put trees

2,500 USV5 112/116 2x1 put spds ref 116-14 to -12

over 7,500 TYV5 112.5 puts, 9 last ref 112-12

4,900 FVV5 109 puts, 1

2,700 USX5 113/116 put spds vs. 119 calls ref 116-12 to -13

3,900 TYV5 113 straddles, ref 112-13 to-13.5

appr 4,000 TYV5 112 straddles, 16 ref 112-13.5

2,500 FVZ5 108/110 strangles, ref 109-03.5

over 10,800 TYZ5 113/113.5/114/114.5 call condors ref 112-12.5

4,000 w2 TY 112 puts ref 112-11 (exp 10/10)

-2,000 TYX5 112 puts, 33 vs. 112-07/0.43%

-10,000 FVX5 110.75 calls, 2.5 vs. 109-01/0.08%

+4,000 TYX5 112.5/113/113.5/114.5 broken call condors on 4x4x4x3 ratio, 1 db

over +9,000 FVV5 108.75 puts, 0.5 ref 109-01.25

+3,000 TYX5 111.5 puts, 20 ref 112-08.5

MNI BONDS: EGBs-GILTS CASH CLOSE: Light EGB Gains Ahead Of Euro Inflation Round

European yields fell modestly to close the week.

- Yields largely reversed Thursday's rise, with a pullback seen through most of the session after an indifferent start (particularly for Gilts which looked to continue their yield rise in early trade).

- Bunds and Gilts largely shrugged off further solid US macro data in the form of personal consumption, as well as a notable uptick in crude oil prices.

- A sizeable core FI rally in late afternoon - with no discernable trigger - saw yields hit the low of the days, but they since ticked back up to close nearly flat for the session.

- European data wasn't a market mover: ECB 3Y consumer inflation expectations were steady at 2.5% (but 0.1pp above expected), while Spanish GDP was revised up going back to 2023.

- On the day, both the German and UK curves leaned bull flatter. For the week, the German curve twist flattened (2Y +0.7bp, 10Y -0.2bp), with the UK's bear flattening (2Y +3.3bp, 10Y +3.1bp).

- Periphery/semi-core EGB spreads closed mixed. OATs outperformed, with French PM Lecornu saying he would restart the contentious 2026 budget from scratch.

- The highlight early next week is the release of Eurozone flash September inflation data, while BOE speakers (including Ramsden Monday) bear watching.

Closing Yields / 10-Yr EGB Spreads To Germany:

- Germany: The 2-Yr yield is down 0.9bps at 2.03%, 5-Yr is down 2.5bps at 2.335%, 10-Yr is down 2.7bps at 2.746%, and 30-Yr is down 1.4bps at 3.328%.

- UK: The 2-Yr yield is down 0.4bps at 4.015%, 5-Yr is down 0.2bps at 4.175%, 10-Yr is down 1.1bps at 4.746%, and 30-Yr is down 0.5bps at 5.561%.

- Italian BTP spread up 0.1bps at 83.5bps / French OAT down 0.7bps at 82.2bps

MNI EGB OPTIONS: Larger Euribor Call Spread Buying Seen Friday

Friday's Europe rates/bond options flow included:

- RXX5 123p, bought for 1.5 in 4k

- ERF6 98.12/98.25cs, bought for 2 in 12k total

- ERH6 98.00/97.9375ps, sold at 3.25 in 5k

- ERM6 98.3125/98.4375 call spread vs ERH6 97.9375/97.8125 put spread, paper pays 0.25-0.50 for the call spread in 6k

- SFIZ5 96.25/96.35/96.45c fly, bought for 1.25 in 4k

- SFIF6 96.25/96.15ps 1x2, bought for 1.25 in 2k

- SFIU6 96.50/96.70cs, bought for 6 in 2.5k.

- 0NH6 96.50/96.80cs 1x2, bought for 3 in 2.5k

MNI FOREX: USD Index Off Recovery Highs into Close, GBP Recovers Well

- Following two days of strong gains for the greenback, the USD index has eased off recovery highs on Friday, declining around 0.32% to finish the week. Overall, renewed optimism for the dollar has been the theme of the week, although market participants will be wary of next week’s busy calendar, culminating in the September US jobs report.

- Intra-day gains have been led by GBP in G10, with cable rising back to above the 1.34 handle. It is worth putting this into perspective following the steep declines on Thursday, and the technical breaks below two significant trendlines, bolstering the short-term bearish theme for the pair. For now, spot has bounced well from the early September lows, however, given the lingering fiscal and political uncertainty in the UK, a deeper selloff towards 1.3140 should not be ruled out.

- In similar vein, NZDUSD is a touch firmer today but looks likely to close the week below the pivotal 0.5800 mark. This week’s price action has made headway towards the next technical targets of 0.5728 and 0.5636. The well documented impressive rally for AUDNZD extended overnight to reach 1.1351, before momentum has stalled. Market participants continue to eye a move towards 1.1491, the September 2022 high.

- USDJPY rose to within 4 pips of the 150 mark overnight, and it’s notable that the recovery has outpaced that of the DXY, rallying 3.07% to its peak. A bullish candle pattern on Sep 17 - a hammer - provided an early reversal signal which remains valid. Sights are on 150.92, the Aug 1 high and key resistance.

- There was little to impact momentum in either direction for EURUSD, with large option expiries between 1.1685-1.1710 on Friday capping the US session range. The trend theme in EURUSD is unchanged, it remains bullish and the recent pullback appears corrective. However, support at 1.1680. the 50-day EMA, has been pierced and will be monitored in coming sessions.

- Spanish CPI, US pending home sales and Fed Speak highlights Monday’s calendar.

MNI US STOCKS: Late Equities Roundup: DJIA Leading Leading Second Half Bid

- Major US equity indexes are drifting higher again late Friday, nearing early session highs after this morning's relatively stable PCE inflation data buoyed risk appetites. Still off record highs from earlier in the week, the DJIA currently trades up 365.7 points (0.8%) at 46314.7, S&P E-Minis up 37 points (0.56%) at 6697.5, Nasdaq up 87.9 points (0.4%) at 22473.63.

- A mix of auto, food and travel related stocks supported the Consumer Discretionary sector in the second half: Domino's Pizza +4.20%, Tesla +3.51%, Ford Motor +3.44%, MGM Resorts Int +3.31% and Expedia Group +2.60%.

- Support for Energy sector shares eased as crude prices moved off highs (WTI +.70 at 65.68 vs. 66.40 high). Support for oil and gas stocks as geopolitical tensions rose after Russian military jets entered neighboring countries airspace: Devon Energy +2.82%, Schlumberger +2.63%, Halliburton +2.07% and Diamondback Energy +2.02%.

- Information Technology and Consumer Staples sector shares continued to underperform in late trade, semiconductor and hardware makers leading the decline in Tech after strong early week gains: Oracle Corp -2.26%, Seagate Technology -1.52%, Super Micro Computer -1.49% and Advanced Micro Devices -1.35%.

- There were some notable gainers in IT, however: Intel Corp +5.96%, CDW Corp +4.73% and AppLovin Corp +4.17%.

- Meanwhile, broadline retailers weighed on the Consumer Staples sector: Costco Wholesale -2.64%, Archer-Daniels-Midland -1.64%, Dollar General -0.99% and Keurig Dr Pepper -0.93%.

MNI EQUITY TECHS: E-MINI S&P: (Z5) Corrective Cycle

- RES 4: 6812.29 2.382 proj of the Aug 20 - 28 - Sep 2 price swing

- RES 3: 6800.00 Round number resistance

- RES 2: 6787.63 1.382 proj of the Aug 1 - 15 - 20 price swing

- RES 1: 6756.75 High Sep 22

- PRICE: 6695.00 @ 1509 ET Sep 25

- SUP 1: 6632.07 20-day EMA

- SUP 2: 6577.25 Low Sep 10

- SUP 3: 6513.37 50-day EMA

- SUP 4: 6417.25 Low Aug 12

A bull cycle in S&P E-Minis remains intact and the latest pullback is considered corrective. The contract is approaching initial support at the 20-day EMA, at 6632.07. A clear breach of this average would signal scope for a deeper retracement potentially towards the 50-day EMA, at 6513.37. Key short-term resistance has been defined at 6756.75, the Sep 22 high where a break would resume the primary uptrend.

COMMODITIES

MNI AMERICAS OIL: Americas End of Day Oil Summary: Crude Rises

WTI crude markets are on track for a strong weekly gain for the first time since early August. A weaker dollar has supported crude’s gains today, alongside continued focus on Russian supply risks. Yesterday’s upward revision to US GDP for the second quarter was also supportive of sentiment. Initial resistance to watch is $65.43, the Sep 2 high. A clear break of it would suggest potential for a stronger recovery, towards key short-term resistance at $68.43, the Jul 30 high. On the downside, key support and the bear trigger has been defined at $60.85, Aug 13 low.

- EU leaders have been clear in their message to Russia that a NATO alliance would be ready to respond to repeated violations of European airspace by Russia, predominantly with drones. US Defense Secretary Pete Hegseth ordered an urgent meeting of top military commanders for an unusual meeting early next week.

- Indian official told Trump a significant reduction in oil imports from Russia would require purchases from sanctioned supplies Iran and Venezuela instead, Bloomberg said.

- WTI Nov futures were up 1.1% at $65.72

- WTI Dec futures were up 1.1% at $65.14

MONDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 29/09/2025 | 0650/0850 | ECB Cipollone Keynote At Baltic Digital Euro Conference | ||

| 29/09/2025 | 0700/0900 | *** | HICP (p) | |

| 29/09/2025 | 0830/0930 | ** | BOE Lending to Individuals | |

| 29/09/2025 | 0830/0930 | ** | BOE M4 | |

| 29/09/2025 | 0900/1100 | * | Consumer Confidence, Industrial Sentiment | |

| 29/09/2025 | 0900/1100 | ECB Schnabel On Current Aspects of Monetary Policy | ||

| 29/09/2025 | 1200/1400 | ECB Lane In Policy Panel At Inflation Conference | ||

| 29/09/2025 | 1200/0800 | Cleveland Fed's Beth Hammack | ||

| 29/09/2025 | 1330/0930 | NY Fed's Roberto Perli | ||

| 29/09/2025 | 1400/1000 | ** | NAR Pending Home Sales | |

| 29/09/2025 | 1430/1030 | ** | Dallas Fed manufacturing survey | |

| 29/09/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 29/09/2025 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 29/09/2025 | 1730/1330 | St. Louis Fed's Alberto Musalem | ||

| 29/09/2025 | 1730/1330 | Ex-St. Louis Fed's James Bullard | ||

| 29/09/2025 | 1730/1330 | New York Fed's John Williams | ||

| 29/09/2025 | 2200/1800 | Atlanta Fed's Raphael Bostic | ||

| 30/09/2025 | 2301/0001 | * | BRC Monthly Shop Price Index | |

| 30/09/2025 | 2350/0850 | ** | Industrial Production | |

| 30/09/2025 | 2350/0850 | * | Retail Sales (p) | |

| 30/09/2025 | 0130/0930 | *** | CFLP Manufacturing PMI | |

| 30/09/2025 | 0130/0930 | ** | CFLP Non-Manufacturing PMI | |

| 30/09/2025 | 0130/1130 | * | Building Approvals | |

| 30/09/2025 | 0145/0945 | ** | S&P Global Final China Manufacturing PMI | |

| 30/09/2025 | 0430/1430 | *** | RBA Rate Decision |