MNI ASIA MARKETS ANALYSIS: Tsys Off 4W Low Ahead Fed Blackout

HIGHLIGHTS

- Treasuries look to finish higher Friday - off Tuesday lows to near where the week started, longer curves near the steepest levels since October 2021 (5s30s at 104.684 Friday).

- Federal Reserve interest media Blackout regarding policy late Friday through July 31, day after the next FOMC announcement.

- Despite trading with a softer tone for much of Friday’s session, some late greenback strength has seen the USD index pare losses to remain just moderately lower on the session.

US TSYS

MNI US TSYS: Tsys Near Steady on Week Heading Into Fed Backout

- Treasuries look to finish firmer - near steady for the week as rates bounce off the week's 4W lows Friday, light volumes (TYU5 under 920k) ahead of the weekend and the start of the Fed's media Blackout on policy (through July 31).

- Early data driven volatility: Treasuries pared support slightly after higher than expected Housing Starts & Build Permit data: starts came in at 1,321k (1,300k expected, 1,263k prior upwardly rev by 7k), with permits up 3k to 1,397k. Building permits remained below the 1,400k mark for a 2nd consecutive month.

- Treasuries extended highs briefly then pared move to pre-UofM release levels as UofM sentiment came out slightly higher while inflation expectations look lower. Inflation expectations surprise lower in the preliminary July survey, with the 1Y at 4.4% (cons 5.0 after 5.0 in June) and 5-10Y at 3.6% (cons 3.9 after 4.0 in June). The 1Y is the lowest since January and the 5-10Y is the lowest since February.

- Pres Trump signed landmark crypto bill into law Friday: GENUIS Act, a bill to create a regulatory framework for stablecoins.

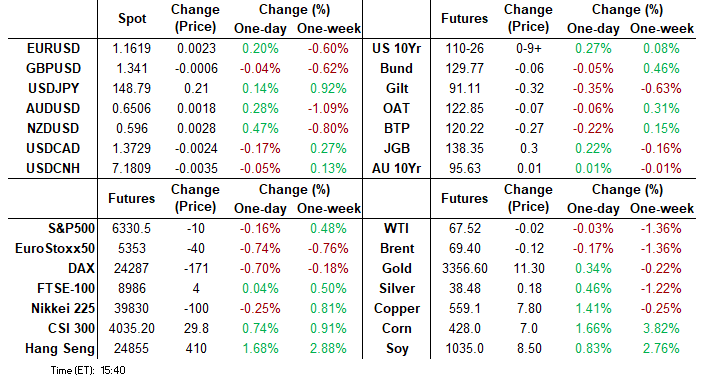

- Sep'25 10Y contract trades +10 at 110-26.5 vs. -29 high. Initial resistance is at 110-30+, the 20-day EMA, followed by 111-13.5/111-28 (High Jul 10 / High Jul 3). Curves mildly steeper: 2s10s +0.761 at 55.030, 5s30s +2.221 at 103.902.

- Cross asset: Bbg US$ index well off lows: BBDXY -1.19 at 1206.39 (1202.46 Low); stocks mildly lower (SPX eminis -10 at 6330.75); gold up 9.7 at 3348.67.

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.34% (+0.00), volume: $2.743T

- Broad General Collateral Rate (BGCR): 4.33% (+0.00), volume: $1.140T

- Tri-Party General Collateral Rate (TCR): 4.33% (+0.00), volume: $1.110T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $113B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $273B

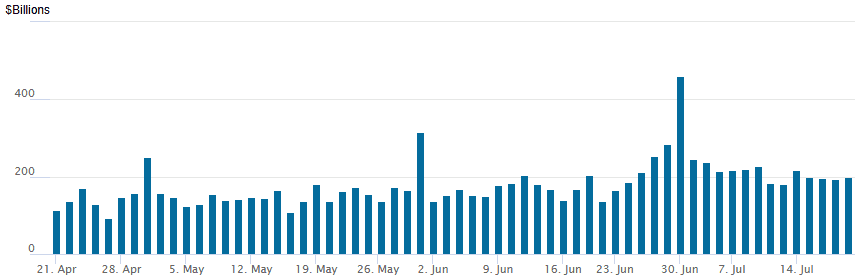

FED Reverse Repo Operation

RRP usage inches up to $199.298B this afternoon from $193.660B yesterday, total number of counterparties at 36. Usage had fallen to $54.772B on Wednesday, April 16 -- lowest level since April 2021 - compares to July 1: $460.731B highest usage since December 31.

US SOFR/TREASURY OPTION SUMMARY

SOFR & Treasury options trade remained mixed on modest volumes Friday. Underlying futures firmer/near the week highs, curves steeper (2s10s +0.972 at 55.241, 5s30s +2.124 at 103.805). Projected rate cut pricing gains slightly vs. early morning (*) levels: Jul'25 steady at -1.2bp, Sep'25 at -16.6bp (-15.2bp), Oct'25 at -29.2bp (-28.2bp), Dec'25 at -46.5bp (-44.9bp).

SOFR Options:

5,000 0QZ5 96.50/96.75 2x1 put spds ref 96.825

+5,000 0QZ5 97.00/97.50/98.00 call flys 5.0 over 0QU5 96.87/97.37/97.87 call fly

+1,000 SFRV5/SFRX5/SFRZ5 95.75/96.00 2x1 put spd strips, 20.0

Update, +12,500 SFRZ5 96.25/96.37/96.50 call flys, 0.87-1.0 adds to +10k Block at 0.75

1,000 SFRQ5 195.68/95.75/95.81 put flys

over +11,200 SFRU5 96.12/96.18 call spds, 0.5 ref 95.835/0.05%

3,000 SFRU5 95.68/95.75 put spds

5,300 SFRQ5 96.00 calls, 1.5 ref 95.825/0.20%

2,000 0QQ5 96.50 puts, 2.5 ref 96.775/0.05%

over 10,000 SFRZ5 96.25/96.37/96.50 call flys, 0.75 ref 96.09

+10,000 0QQ5 96.81 calls, 0.5-1.0

Treasury Options:

3,000 TYU5 108 puts, 5 ref 110-28

5,000 TYU5/TYV5 109 put spds, 19

6,700 TYQ5 111 straddles, 34

5,000 TYX5 107/108.5/110 put flys ref 110-23.5

1,500 TYQ5 112.25/113.75 1x2 call spds ref 110-24

+3,000 TYQ5 112.25 calls, 1

2,500 TYQ5 111/112 call spds, ref 110-25.5

+15,000 TYQ5 114.25 calls, 1 vs. 110-25.5/0.02%

-1,600 TYQ5 112.25/113.75 1x2 call spds, 0.0 ref 110-25

4,000 TYQ5 110 puts, 5 last, 1k tied to 109.5 put

2,200 TYQ5 111 calls, 9 last

2,400 TYQ5 111.5 calls, 4 last

1,000 FVU5 107.25/109.25 strangles ref 108-05.75

2,500 TUU5 103.25/103.5/103.62/103.75 broken put condors ref 103-20 to -19.87

MNI BONDS: EGBs-GILTS CASH CLOSE: Gilts Maintain Underperformance For The Week

European yields rose modestly Friday, with curve steepening seen in both EGBs and Gilts.

- There were few evident macro/headline catalysts, with yields weighed down early (with a pickup in energy prices and equities) and no subsequent recovery.

- For the third consecutive session, Gilt yields gapped higher at the cash open, and didn't deviate much through the session. 10Y yields saw the highest intraday yields since June 2 and highest close since May 28, with the curve twist steepening.

- Bund yields also picked up modestly in early trade but remained within Thursday's ranges for the rest of the session. The German curve bear steepened.

- Periphery EGBs erased a bit of early weakness to close very slightly tighter to Bunds.

- For the week, Gilts badly underperformed Bunds, partly on the back of more solid-than-expected labour market and CPI data.

- The UK curve bear steepened mildly on the week, with Bunds easily outperforming as German yields moved lower in parallel across the curve: UK 2Y yields +4.6bp / 10Y + 5.2bp; German 2Y yields -3.0bp / 10Y -3.0bp.

- Next week's main event is the ECB decision Thursday - with a rate hold expected, focus will be President Lagarde’s characterisation of risks at the press conference, which will likely shape the market reaction. Flash July PMIs and the ECB's Q2 Bank Lending Survey will also garner attention.

MNI OPTIONS: Busy Week For Sonia Concludes With Mixed Trade

Friday's Europe rates/bond options flow included:

- RXU5 121.50 puts paper paid 1 on 4K.

- SFIZ5 96.30/96.55/96.80 call fly vs. 96.35/96.15 put spread paper paid -3.5 for the call fly on 8.5K

- SFIH6 96.70/96.85 call spread 5K given at 2.75

MNI FOREX: USDJPY Consolidates Weekly Advance Ahead of Japan UH Election

- Despite trading with a softer tone for much of Friday’s session, some late greenback strength has seen the USD index pare losses to remain just moderately lower on the session. Some late weakness for equities appears to have been behind the dollar reversal, but overall, currency markets have lacked conviction across the session.

- Scandinavian currencies remain at the top of the G10 leaderboard, while the likes of AUD (+0.40%) and NZD have remained resilient (+0.59%). In contrast, the Japanese yen is lower on Friday, as markets remain concerned regarding this week’s upper house election in Japan, and the potential fiscal ramifications ahead. GBP is unchanged having briefly flirted back above the significant trendline break this week. A short-term bear cycle in GBPUSD remains in place.

- Despite the softer USD index today, it has broadly consolidated a solid weekly advance of around 0.5% and fresh recovery highs this week underpin the more constructive short-term outlook. Both the Australian dollar and the Japanese yen have been particular laggards across the week, as domestic developments weigh.

- In Australia, a much weaker-than-expected jobs report has bolstered RBA easing bets, while the increased volatility surrounding the Trump-Powell spat has likely provided an additional headwind to higher beta currencies. AUDUSD support at the 50-day EMA, at 0.6490, was temporarily breached. A clear break of this EMA would highlight a stronger reversal and signal scope for an extension lower.

- In Japan, the ruling party is still projected to lose its majority in the upper house, and this has allowed USDJPY to reach fresh 3-month highs this week above 149.00. Above here, attention will be on 149.38, the 50.0% retracement of the Jan 10 - Apr 22 bear leg, and 150.49, the Apr 2 high. On the downside, initial support is seen at 146.92 (Jul 16 low), however key short-term support is located at 145.66, the 50-day EMA.

- On Monday, New Zealand Q2 CPI highlights the economic calendar.

EQUITIES

MNI US STOCKS: Late Equities Roundup: Off New Highs Ahead Heavy Earning Next Week

- Stocks hold near steady to moderately weaker late Friday - after the SPX emini and Nasdaq indexes managed to extend all time highs around the open. Currently, the DJIA trades down 205.52 points (-0.46%) at 44281.67, S&P E-Minis down 9.5 points (-0.15%) at 6332, Nasdaq down 0.2 points (0%) at 20889.61.

- While generally upbeat upbeat earnings at the start of the latest cycle helped push indexes to new highs this week, investors took profits ahead next week's full docket of earnings releases across multiple sectors: Consumer Staples, Tech and Media, Industrial, Health Care, Energy and Financials.

- Some big names reporting next week include: Domino's Pizza, Coca-Cola, Alphabet, AT&T Inc, T-Mobile, Verizon Communications, IBM, Intel, Philip Morris, PulteGroup, Hasbro Inc, Amphenol, O'Reilly Automotive, Tesla and CSX Corp.

- Meanwhile, Friday's leading gainers included: Invesco +14.18%, Regions Financial +6.65%, Vistra +6.16%, Dell Technologies +5.72%, Constellation Energy +4.75%, Tesla +3.35%, Targa Resources +3.07%, NRG Energy +2.99% and Enphase Energy +2.61%

- Conversely, Health Care sector stocks, particularly pharmaceuticals underperformed: Molina Healthcare -7.55%, Elevance Health -6.62%, West Pharmaceutical Services -6.02%, Viatris -3.72% and Centene -3.47%. Other laggers included Netflix -4.81%, 3M Co -4.45%, Builders FirstSource -3.87%, Schlumberger -3.62% and Exxon Mobil -3.45%.

MNI EQUITY TECHS: E-MINI S&P: (U5) Fresh Cycle High

- RES 4: 6439.884 1.500 proj of the May 23 - Jun 11 - 23 price swing

- RES 3: 6402.44 1.382 proj of the May 23 - Jun 11 - 23 price swing

- RES 2: 6381.50 1.764 proj of the Apr 7 - 10 - 21 price swing

- RES 1: 6357.00 Intraday high

- PRICE: 6331.75 @ 1405 ET Jul 18

- SUP 1: 6288.25 Low Jul 17

- SUP 2: 6237.47/6092.32 20- and 50-day EMA values

- SUP 3: 5811.50 Low May 23

- SUP 4: 5645.75 Low May 7

S&P E-Minis are trading higher today and this has resulted in a fresh cycle high. The climb confirms a resumption of the uptrend and maintains the price sequence of higher highs and higher lows. Note that moving average studies are in a bull-mode position highlighting a clear dominant uptrend. Sights are on 6381.50, a Fibonacci projection. Key support is at the 50-day EMA, at 6092.32. Support at the 20-day EMA is at 6237.47.

MNI AMERICAS OIL: WTI crude came under pressure

July 18 - Americas End-of-Day Oil Summary: WTI crude came under pressure after EU revealed its import ban on Russian refined products obtained in third countries will have a transitional period of six months. This also bolstered ULSD futures, which had also been higher after the EIA reported higher implied demand year-on-year.

- Japan’s PM Ishiba said Treasury Secretary Bessent had told him that he was sure a good deal between the US and Japan was possible.

- US President Trump was reportedly eyeing tariff rates of 10% -15% on more than 150 countries.

- The EU has adopted its latest Russia sanctions package, including a dynamic oil price cap, and sanctions on India’s Vadinar refinery, alongside sanctions on tankers involved in Russia’s energy trade.

- The EU’s latest restrictions on Russian crude are unlikely to alter the global supply picture, Bloomberg said.

- In the first two weeks of July, global oil demand has averaged 105.2 million barrels per day (bpd), up by 600,000 bpd from a year earlier and largely in line with forecast, JPMorgan analysts said.

- South Korean refiners, the second-biggest buyers of US crude this year, have so far purchased ~12m-14m bbls of US oil for arrival in October, according to Bloomberg sources.

- WTI Aug futures were down 0.3% at $67.34

- WTI Sep futures were down 0.3% at $66.04

MONDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 21/07/2025 | 0900/1100 | EZ Quarterly GDP Third Estimate | ||

| 21/07/2025 | 0900/1100 | Eurozone Q1 Deficit/Debt Data | ||

| 21/07/2025 | 1230/0830 | * | Industrial Product and Raw Material Price Index | |

| 21/07/2025 | 1430/1030 | ** | BOC Business Outlook Survey | |

| 21/07/2025 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 21/07/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill |