MNI ASIA MARKETS ANALYSIS: Tsy Ylds Rise With Mid-East Tension

HIGHLIGHTS

- Middle East tensions flared after Israel bombed appr 200 targets in Iran overnight, including a couple nuclear facilities that also resulted in several high level military commander deaths.

- Markets remained wary of further escalation - Iran reportedly launching dozens of missiles in retaliation. Israel officials said the operation will last several days.

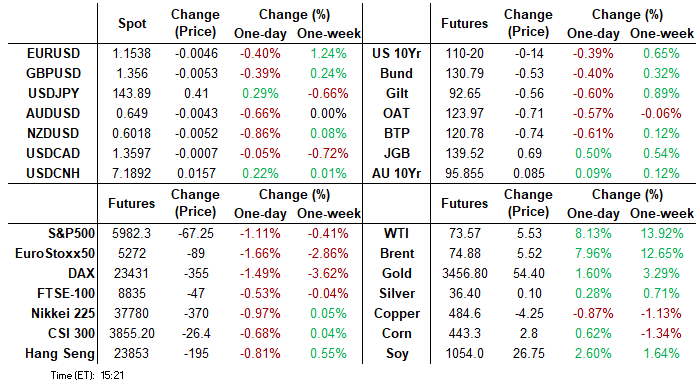

- Crude prices surged (WTI tapped 77.16 overnight, trades 73.24 in late NY hours), stocks retreated: SPX eminis -61.0 at 5988.0, while the Bbg US$ index bounced off the lowest levels since April '22 overnight (1197.45) to 1202.82 (+2.80).

- Aside from geopolitical risks, markets await the next FOMC policy announcement next week Wednesday

US TSYS

MNI US TSYS: Risk-Off Gains Traction as Iran Retaliates Against Israeli Strikes

- Treasuries look to finish broadly lower Friday, off late session lows amid some position squaring amid reports Iran has retaliated against Israel's heavy bombing the night before with dozens of their own missile Friday.

- Israel struck over 200 targets in Iran including nuclear facilities overnight, killing several military commanders. Iran has 7 known nuclear facilities: Arak, Bushehr, Darkhovin, Fordow, Karun, Natanz and Isfahan -- of which the last 2 were hit. Israeli officials said the operation would last several days.

- Treasuries came under pressure after latest UofM sentiment came out higher than expected, 1Y inflation much lower than expected (5-10Y in-line). Details implied a notably heavier response from republican-leaning respondents, who have much lower inflation expectations under the Trump administration.

- According to data pulled in by Bloomberg, whilst the median 1Y expectations slipped from 6.6% to 5.1%, democrats increased from 9.4% to 10.1%, independents from 7.2% to 7.5% and republicans from 1.0% to 1.5%.

- After the bell, Tsy Sep'25 10Y futures currently trade -14 at 110-20 vs. 110-14 low, technical support below at 109-28 (Low Jun 6 / 11). Curves steeper: 2s10s +1.512 at 46.245, 5s30s +1.914 at 89.213.

- Cross asset: Stocks remain weaker (SPX eminis -68.75 at 5980.75), Gold higher at 3437.00, Bbg US$ index +2.95 at 1202.97.

- Aside from geopolitical risks, markets await the next FOMC policy announcement next week Wednesday.

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.28% (+0.00), volume: $2.663T

- Broad General Collateral Rate (BGCR): 4.27% (+0.00), volume: $1.098T

- Tri-Party General Collateral Rate (TCR): 4.27% (+0.00), volume: $1.062T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $114B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $290B

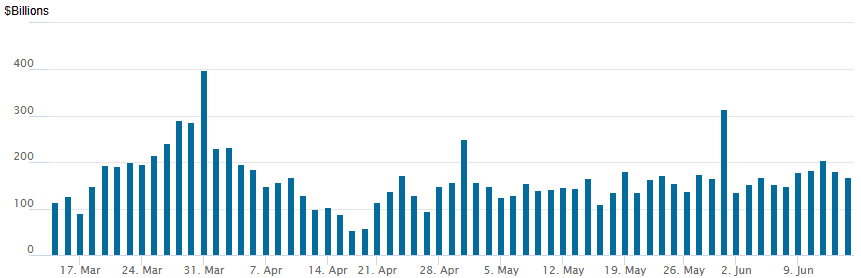

FED Reverse Repo Operation

RRP usage retreats to $168.645B this afternoon from $181.417B yesterday, total number of counterparties at 27. Usage had fallen to $54.772B on Wednesday, April 16 -- lowest level since April 2021. Conversely, usage had surged to the highest level since December 31, 2024 on Monday, March 31: $399.167B.

US SOFR/TREASURY OPTION SUMMARY

Option desks reported mixed SOFR & Tsy option flow overnight, rather muted volumes in contrast to heavier underlying futures volumes following last night's by Israel on Iran. Underlying futures weaker but rising off late overnight lows, projected rate cut pricing steady to slighly cooler vs. late Thursday levels (*) as follows: Jun'25 at -0.8bp, Jul'25 at -5.9bp (-5.9bp), Sep'25 at -22.4bp (-23.2bp), Oct'25 at -34.9bp (-35.9bp), Dec'25 at -50.5bp (-52.3bp).

SOFR Options:

+27,500 0QN5 96.75 calls, 8.5 vs. 96.62/0.34%

Update, +14,000 SFRU5 95.56/95.75/95.87 put trees, 6.25-6.50

Block/screen, +5,000 SFRV5 96.12/96.25/96.37/96.50 call condors, 2.0 net

+4,000 2QH6 97.00/98.00 call spds 14.5-15.0

+5,000 0QU5 96.75/97.00/97.25 call flys, 3.0

4,000 SFRQ5 95.81/SFRV5 95.87 put spds

-4,000 SFRM5/SFRU 95.62/95.75 put spd spd, 3.0/Jun over

4,000 0QM5 96.62/3QM5 96.50 call spd, 0.5 net Blues over

4,000 SFRN5 95.93/96.06 call spds, 4.0

Treasury Options:

7,500 TYN5 108.5/109/109.25 put trees, ref 110-15.5

5,000 TYN5 108.5/109 2x1 put spds ref 110-17

Block, 10,000 TYN5 108.5/112.5 strangles, 2 vs. 110-18/0.14%

Block, 20,000 wk2 TY 111 puts, 19 ref 110-20

3,000 FVN5 107/107.5 put spds, 2.5 ref 107-30.75

over 11,000 wk1 FV 109/110 call spds, 6.5-7.0 (exp 7/3)

over +17,500 FVN5 108.5/109 call spds 11.5 ref 108-02.5 to -02.25

-2,500 TYN5 110.25 puts, 9

+2,000 TYQ5 108/112 call over risk reversals, 27-28 vs. 111-01/0.44%

3,000 TYQ5 109/113 strangles ref 110-28

2,500 TYN5 112/112.5/112.75 call flys, ref 111-01

+4,200 TYU5 107/108 put spds, 7 ref 111-02

over 16,100 TYN5 112 calls, 5-12 ref 111-10

MNI BONDS: EGBs-GILTS CASH CLOSE: Weaker On Geopolitics

European yields rose Friday, but still closed lower for the week.

- Geopolitical risk was the dominant theme, with Israel's strikes on Iran overnight seeing Bunds and Gilts rally strongly on Friday's open.

- But from there, yields would head higher: with Iran not immediately retaliating, oil prices retraced and equities found their footing.

- In a lighter session for data, the UK BoE/Ipsos survey showed inflation expectations didn't pick up further in May, but medium-term readings remain elevated. Final May HICP prints from Germany, France and Spain were unsurprising, and while April Eurozone industrial production was below-consensus, this comes after Q1 distortions.

- The German curve bear steepened, while the UK's leaned bear flatter. On the week, Bunds and Gilts closed stronger, with some modest bull flattening in both the German (2Y -2.4bp, 10Y -4.1bp) and UK (2Y -7.3bp, 10Y -9.4bp) curves.

- Periphery EGB spreads closed slightly wider, with BTPs underperforming.

- Next week's schedule is highlighted by the BOE decision Thursday, preceded by UK CPI Wednesday.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 4bps at 1.856%, 5-Yr is up 5.7bps at 2.136%, 10-Yr is up 5.7bps at 2.535%, and 30-Yr is up 5.5bps at 2.987%.

- UK: The 2-Yr yield is up 7.4bps at 3.94%, 5-Yr is up 7.9bps at 4.064%, 10-Yr is up 7.3bps at 4.55%, and 30-Yr is up 6.7bps at 5.26%.

- Italian BTP spread up 2.2bps at 94.9bps / French OAT up 1.3bps at 72.2bps

MNI EGB OPTIONS: Busy Week In Euro Rates Concludes With Quieter Session

Friday's Europe rates/bond options flow included:

- ERQ5 98.4375/98.5625cs, bought for half in 5k

MNI FOREX: Israeli Strikes Can Only Provide So Much for Support For Dollar

- The USD Index rallied sharply on the back of the initial reports that Israel was pursuing broad military strikes against Iranian nuclear facilities, partially reversing a decent part of the week's trade-led weakness. EUR was among the hardest hit, prompting EUR/USD to post a near 150 pip fade off the cycle high at the Friday low.

- This price action soon reversed, however, as markets parsed the contained fallout for oil prices, production and supply from the Israeli strikes. As a result, the USD Index faded well, ensuring the definitive downtrendline resistance drawn off the early February high was never really under threat - a key theme that stays in focus headed into next week's Fed meeting.

- Looking ahead, any material escalation in geopolitical tensions could reignite risk-off. Iran's leadership have pledged a firm response to the Israeli strikes, and any action made toward US interests in the area could see increased ire from Trump - who has continued to press for a nuclear deal with Tehran. This continues to support front-end vols - with AUD, NZD seen among the most sensitive across early Friday trade.

- Sizeable options influence could play a part in spot vol in the coming few sessions - next week sees a major strike rolling off on Monday in USD/JPY at Y145.00: $4.9bln, as well as E4.6bln in EUR/USD at $1.1700.

- Central banks are of more interest next week, with both the BoJ, BoE and Fed rate decisions all due. No change is expected at any of the three meetings, however their views on policy further down the line - particularly into year-end, will be carefully watched.

MNI OPTIONS: Expiries for Jun16 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1400(E1.3bln), $1.1450-65(E2.0bln), $1.1500(E1.9bln), $1.1565-80(E1.6bln), $1.1600(E1.5bln), $1.1700(E4.6bln)

- USD/JPY: Y145.00($4.9bln)

- AUD/USD: $0.6503-05(A$500mln), $0.6560-63(A$1.0bln)

MNI US STOCKS: Late Equities Roundup: Mid-East Tension Buoys Oil&Gas, Defense Stocks

- Stocks remain in negative territory early Friday, off overnight lows as markets remain wary of further unrest in the Middle East after Israel launched attacks against Iran overnight. Israel struck over 200 targets in Iran including nuclear facilities overnight, killing several military commanders.

- Iran has 7 known nuclear facilities: Arak, Bushehr, Darkhovin, Fordow, Karun, Natanz and Isfahan -- of which the last 2 were hit. Israeli officials said the operation would last several days. Iranian officials vowed sever retaliations for the attacks.

- Currently, the DJIA trades down 847.18 points (-1.97%) at 42120.19, S&P E-Minis down 74.5 points (-1.23%) at 5974.25, Nasdaq down 265.3 points (-1.3%) at 19396.94.

- Not surprisingly Energy and Industrial sectors continued to outperform in the second half due to the attacks, oil and gas shares led gainers as crude prices soared (WTI tapped overnight high of 77.16, trades 72.90 at the moment +4.86): Halliburton +4.37%, APA +3.51%, EOG Resources +3.42%, Targa Resources +3.13%, Occidental Petroleum +3.04%.

- Defense stocks buoyed the Industrials sector: Northrop Grumman +3.85%, Lockheed Martin +3.33%, RTX +3.21%, L3Harris Technologies +2.69%, Huntington Ingalls Industries +1.31% and General Dynamics +1.10%.

- On the flipside, Financial and Information Technology sectors continued to underperform, services weighed on the former: Visa -5.72%, Corpay -5.04%, Mastercard -5.03%, PayPal Holdings -4.76% and American Express -3.32%.

- Meanwhile, semiconductor and hardware makers weighed on the IT sector: Monolithic Power Systems -6.06%, Super Micro Computer -5.12%, Adobe -4.80%, Arista Networks -3.03% and Synopsys -2.91%.

MNI EQUITY TECHS: E-MINI S&P: (M5) Monitoring Support

- RES 4: 6172.38 1.500 proj of the Apr 7 - 10 - 21 price swing

- RES 3: 6124.00 High Feb 24

- RES 2: 6080.75 High Feb 26

- RES 1: 6074.75 High Jun 11

- PRICE: 5992.25 @ 14:28 BST Jun 13

- SUP 1: 5927.50/5825.83 Intraday low / 50-day EMA

- SUP 2: 5756.50 Low May 23

- SUP 3: 5596.00 Low May 7

- SUP 4: 5455.50 Low Apr 30

The trend condition in S&P E-Minis remains bullish and the contract traded to a fresh cycle high on Wednesday, reinforcing current bullish conditions. For now, today’s pullback is considered corrective. The contract has pierced support at 5933.69, the 20-day EMA. A clear breach of this average would expose the 50-day EMA, at 5825.83. Key short-term resistance has been defined at 6074.75, the Jun 11 high.

COMMODITIES

MNI AMERICAS OIL: WTI crude has surged higher

WTI crude has surged higher today amid a major escalation in Middle East tensions after Israeli strikes on Iranian nuclear facilities/military targets. Signs that Iranian officials are in contact with Trump has seen some of the gains reversed, highlighting market sensitivity to any potential signs of de-escalation. Given uncertainty around the duration of the offensive, gains largely held firm into the close.

- Israel comments suggest that military operations will continue until its objectives are met, while focus is also on Iran's response. The country stated it will respond harshly against the US and Israel in response to the attacks.

- Upside pressure being added to by Trump’s comments that “it will only get worse,” and that “the next already planned attacks” will be “even more brutal,” as the market focuses on the potential for an extended bombing campaign by Israel.

- Reports suggest Israel has struck Iran again throughout the day including in Shiraz, Tabriz and Natanz, while Iran sent a wave of ~100 drones to attack Israel.

- Iran reported that there was no damage to its oil refineries or storage tanks, according to Bloomberg.

- WTI July futures were up 7.5% at $72.98

- WTI Aug futures were up 7.3% at $71.53

- RBOB Jul futures were up 4.0% at $2.23

- ULSD Jul futures were up 7.9% at $2.36

- US gasoline crack down 1.8$/bbl at 26.09$/bbl

- US ULSD crack up 1.8$/bbl at 26.07$/bbl

MONDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 16/06/2025 | 0800/1000 | *** | HICP (f) | |

| 16/06/2025 | 1030/1230 | ECB Cipollone At Osservatorio Banca Impresa 2030 Meeting | ||

| 16/06/2025 | 1215/0815 | ** | CMHC Housing Starts | |

| 16/06/2025 | 1230/0830 | ** | Empire State Manufacturing Survey | |

| 16/06/2025 | 1300/0900 | * | CREA Existing Home Sales | |

| 16/06/2025 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 16/06/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 16/06/2025 | 1700/1300 | ** | US Treasury Auction Result for 20 Year Bond | |

| 16/06/2025 | - | FOMC Meetings with S.E.P. | ||

| 17/06/2025 | 0200/1100 | *** | BOJ Policy Rate Announcement |