MNI ASIA MARKETS ANALYSIS: Trump Nominates Miran for Fed Gov

HIGHLIGHTS

- Treasuries reversed early gains - see-sawed lower late Thursday, a poorly received 30Y bond sale (4.813% high yield vs. 4.791% WI) contributed to the second half reversal.

- Bank of England MPC voted 5-4 to cut Bank Rate to 4.00% after a second ballot, while a "gradual and careful" approach .. still warranted, MPC emphasized that "restrictiveness of monetary policy has fallen"

- Trump nominated Council of Economic Advisers Chair Miran to serve as a Federal Reserve governor while Fed Gov Waller is emerging as a top candidate to serve as the central bank’s chair, Bbg reported.

- Trump/Putin summit expected "in the coming days", with both sides working out the details.

US TSYS

MNI US TSYS: Tsys Weaker After 30Y Tail, Miran Nominated for Fed Gov, BoE Cut

- Treasuries look to finish mildly lower across the board Thursday, bonds reversing midday support after Tsy $28B 30Y auction (912810UM8) tailed 2.2bp: 4.813% high yield vs. 4.791% WI; 2.27x bid-to-cover vs. 2.38x in the prior month.

- Treasury futures pared early losses after slightly higher than expected weekly & continuing jobless claims (prior down-revised for continuing claims): Initial jobless claims 226k (sa, cons 222k) in the week to Aug 2 after a marginally upward revised 219k (initial 218k). Continuing claims 1974k (sa, cons 1950k) in the week to Jul 26 after a downward revised 1936k (initial 1946k).

- Unit Labor Costs higher with an up-revision to prior: +1.6% Q/Q SAAR (1.5% expected, prior rev up to 6.9% from 6.6%).

- Tsy Sep'25 10Y futures currently trades -3.5 at 112-04 (112-01 low, 112-09 high). Curves mixed: 2s10s +1.271 at 52.264, 5s30s -0.111 at 104.033.

- Trump nominated Council of Economic Advisers Chair Miran to serve as a Federal Reserve governor while Fed Gov Waller is emerging as a top candidate to serve as the central bank’s chair, Bbg reported.

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.34% (+0.00), volume: $2.866T

- Broad General Collateral Rate (BGCR): 4.32% (-0.01), volume: $1.176T

- Tri-Party General Collateral Rate (TCR): 4.32% (-0.01), volume: $1.147T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $112B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $264B

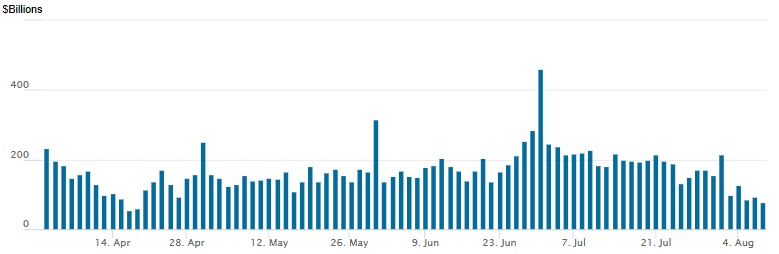

FED Reverse Repo Operation

RRP usage falls to $77.961B this afternoon (lowest levels since mid-April when levels fell to the mid-50s) from $91.966B yesterday, total number of counterparties at 26. Lowest usage of the year at $54.772B on Wednesday, April 16 -- in turn the lowest level since April 2021 - compares to July 1: $460.731B highest usage since December 31.

--On Friday, someone paid 1.0 for 50k 0QZ 9787.5/9800cs and 0.5 for 50k or more 9837.5/9850cs Yesterday, he bought 50k 0QZ 9800/9837.5/9850c fly 1x1x1 for 3 (and sold the 9837.5/9850cs at 0.25).

US SOFR/TREASURY OPTION SUMMARY

Upside calls/call spds continued to drive Treasury & SOFR option volumes Thursday, two-way Treasury option vol flow late. Underlying futures mildly weaker - at/near lows with bonds reversing course after 30Y auction tailed. Projected rate cut pricing eases slightly vs. morning (*) levels: Sep'25 at -22.8bp (-23.4bp), Oct'25 at -38.9bp (-39.4bp), Dec'25 at -59.4bp (-59.7bp), Jan'26 at -70.9bp (-71.4bp).

SOFR Options:

+30,000 SFRU5 96.12/96.25 call spds, 1.5 ref 95.93

+3,000 SFRU5 96.18/96.25 call spds, 0.62

-10,000 SFRZ5 96.18/96.37 call spds 8.0 vs. 96.285/0.20%

Block: 20,000 SFRM6 96.50/97.00/97.50 call flys 2.0 over SFRM6 96.12 put

1,500 SFRZ5 96.31/96.37 call spds ref 96.275

Block, 2,500 SFRZ5 96.43/96.56/96.68 call flys, 1.0 ref 96.27

+5,000 SFRZ5 96.31/96.37/96.56/96.62 call condors, 1.75

7,150 SFRV5 96.00/96.18 3x2 put spds

Blocks, +15,000 SFRZ5 96.25/96.37/96.50/96.62 call condors 3.0

+10,000 SFRZ5 99.00 calls, cab

3,100 SFRV5 95.81/95.93 put spds ref 96.27

1,500 SFRU5 95.81/95.87/96.00/96.06 call condors

3,000 SFRU5/SFRZ5 95.75 put spd

+5,000 SFRZ5 96.87/97.25 call spds, 1.5 vs. 96.26/0.07%

2,500 SFRZ5 96.37/SFRH6 96.50 1x2 call spd 38

+2,000 SFRX5 96.56/96.75 call spds 2.75

Block, 3,500 SFRQ5/SFRU5 96.00/96.12 call spd spd, 1.0-1.25 (crossed late Wed)

Treasury Options:

+3,200 TYU5 112 straddles, 57

-10,000 TYV5 110.5/114 strangles 39-38 (appr imp vol 5.58%)

-12,000 FVU5 109.75/110 call strip, 8

Block: -4,750 WNU5 117.5/120 call over risk reversals, 22 vs. 119-11/0.70%

5,000 wk2 US 117 calls, 1 ref 115-27

+2,800 TYU5 112 straddles, 60

3,000 TUV5 104/104.5 call spds ref 104-05.88

6,000 wk2 TY 112/wk3 TY 112.5 1x2 call spds ref 112-06

1,500 FVU5 110/110.75 1x2 call spds ref 109-01.25

4,000 FVU5 108.25 puts ref 108-30.25

1,000 TYU5 110/111 put spds ref 112-04

-2,000 wk2 TY 112.25 puts, 11

-5,000 FVU5 108.75 puts, 12.5

-5,000 USU5 116.5 calls, 32

MNI BONDS: EGBs-GILTS CASH CLOSE: Gilts Underperform After Hawkish BOE

Gilts underperformed Thursday after a more hawkish-than-expected Bank of England decision.

- While the BOE eased 25bp as fully expected, there was an unprecedented deadlock in a first vote, with the second ballot delivering what Gov Bailey called a "finely balanced" 5-4 decision in favour of a quarter-point cut.

- When combined with hawkishly-interpreted short-term inflation projections and language shifts, the UK short-end bore the brunt in a bear flattening move on the curve (2s10s have now erased the steepening seen since July 1).

- In data, German industrial production came in weak with lower revisions but this had limited market impact.

- For the day, the UK and German curves twist flattened, with periphery/semi-core EGB spreads closing mostly tighter to Bunds.

- Friday's regional calendar is light, with BOE's Pill scheduled to speak, and some second-tier Eurozone data (including French ILO unemployment).

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 0.1bps at 1.919%, 5-Yr is down 0.9bps at 2.226%, 10-Yr is down 2bps at 2.63%, and 30-Yr is down 3.5bps at 3.138%.

- UK: The 2-Yr yield is up 5.6bps at 3.877%, 5-Yr is up 4.5bps at 4.004%, 10-Yr is up 2.1bps at 4.547%, and 30-Yr is down 0.9bps at 5.351%.

- Italian BTP spread down 0.5bps at 79.3bps / Spanish bond spread down 0.8bps at 57.2bps

MNI EGB OPTIONS: Flurry Of Sonia Call Structure Buying After Hawkish BOE

Thursday's Europe rates/bond options flow included:

- SFIZ5 96.10/96.25/96.40/96.55 12K call condors blocked at 6.75 (paper to paper, per source)

- SFIZ5 96.50/96.75cs vs 96.00/95.75ps, bought the cs for half in 6k

- SFIH6 96.70/97.00/97.20 broken c fly, bought for 2.5 in 2k

MNI FOREX: USD Index Still Driven by Speculation Over Make-Up of FOMC

- Price action in the USD Index remained dominated by speculation over Fed leadership. Reportedly, Trump advisers are pushing for current FOMC member Waller to lead the Fed after Powell's departure. The headline helped trigger some USD positive moves given Waller's relative credibility and insider knowledge of the Fed relative to Kevin Hassett - who argued for a Greenspan-like approach to rate-setting earlier this week.

- Later in the session, CEA Chair Stephen Miran was touted to take Kugler's place on the Fed Board of Governors. Miran, an Oval Office insider who has backed the President on trade deals, US economic dominance and the benign inflation backdrop - prompted a minor spell of USD weakness, aiding EUR/USD to head into the close either side of 1.1650.

- GBP shot higher against all others in G10 into the Thursday close on the back of the BOE rate decision. While the bank voted to cut rates by 25bps - as expected - there was more opposition among the committee for easing than expected and, for the first time, the vote on policy went to a second round after an initial failure to reach consensus. The unexpected opposition to cutting rates today proved a surprise for markets, and prompted UK rates to price out the odds of further easing through year-end.

- November BoE rate cut odds dropped below 50%, and another 25bps easing through year-end is now less than fully priced. As a result, GBP surged through 1.34 against the USD, narrowing the gap on the 50-dma in the process. This leaves prices still well below the late July highs of 1.3589, let alone 1.3789, the YTD high. With the September BoE unlikely to deliver any policy change, this leaves the Autumn budget as the next major UK macro event - particularly as estimates this week showed the UK Treasury with considerably less wiggle room on debt than previously expected.

- Focus Friday turns to unemployment rate data from France and the Canadian jobs report for July. Central bank speakers include Fed's Musalem and BoE's Pill.

MNI OPTIONS: Expiries for Aug08 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1500(E1.5bln), $1.1550(E614mln), $1.1600(1.1bln), $1.1650(E741mln), $1.1700(E1.3bln)

- USD/JPY: Y146.00($672mln), Y147.45-50($765mln)

- EUR/GBP: Gbp0.8675(E1.3bln), Gbp0.8700(E1.3bln)

- AUD/USD: $0.6500(A$4.4bln)

- USD/CAD: C$1.3750($851mln)

MNI US STOCKS: Late Equities Roundup: Continued Retreat

- Stocks continued to retreat from early morning highs, SPX eminis and Nasdaq indexes weathering the selling better than the DJIA late Thursday. Currently, the DJIA trades down 307.67 points (-0.7%) at 43885.41, S&P E-Minis down 25.25 points (-0.4%) at 6345.5, Nasdaq down 22.6 points (-0.1%) at 21147.16.

- Stocks had pared early session gains after Bloomberg reported that Fed Gov Waller "is emerging as a top candidate to serve as the central bank’s chair among President Donald Trump’s advisers as they look for a replacement for Jerome Powell, according to people familiar with the matter."

- While Waller (with Bowman) dissented against the last rate decision and opted to cut rates, his credibility as an insider candidate relative to Hassett is showing in this market reaction. As the piece notes: "Trump advisers are impressed with Waller’s willingness to move on policy based on forecasting, rather than current data, and his deep knowledge of the Fed system as a whole".

- Health Care, Financials, Communication Services and Industrials sectors continued to lead decliners: Fortinet -25.24% despite beating estimates (just not by enough apparently), Eli Lilly & Co -14.36% as it’s weight loss drug underperforms in trials. Elsewhere: Airbnb -9.10%, Ralph Lauren -6.88%, Warner Bros Discovery-6.68%, CF Industries Holdings -6.55%, Crowdstrike Holdings -6.27%, McKesson -5.52%, Gartner -5.31% and Autodesk -5.02%.

- On the positive side, IT, Utility, Consumer Staples and Energy sectors remained supportive in late trade: Becton Dickinson +7.99%, Zimmer Biomet Holdings +7.91%, APA Corp +7.59%, Insulet +6.72%, Enphase Energy +6.11%, Viatris +5.77%, Albemarle +5.26%, Advanced Micro Devices +5.08%, Atmos Energy +4.53% and Occidental Petroleum +4.08%.

- Companies expected to announce earnings after the close include: Sempra, TripAdvisor Inc, Take-Two Interactive Software, GoDaddy, Expedia Group, Akamai Technology, Live Nation Entertainment, Motorola Solutions, Pinterest, Twilio, Microchip Technology Inc, Rocket Lab, Wynn Resorts, Goodyear, Gilead Sciences, Monster Beverage and Block Inc.

MNI EQUITY TECHS: E-MINI S&P: (U5) Corrective Pullback Extends

- RES 4: 6523.63 1.764 proj of the May 23 - Jun 11 - 23 price swing

- RES 3: 6500.00 Round number resistance

- RES 2: 6477.31 1.618 proj of the May 23 - Jun 11 - 23 price swing

- RES 1: 6468.50 High Jul 31 and the bull trigger

- PRICE: 6351.00 @ 1325 ET Aug 7

- SUP 1: 6244.36 2.0% 10-dma Envelope

- SUP 2: 6239.50 Low Aug 1

- SUP 3: 6213.75 50% retracement of Jun - Aug Upleg

- SUP 4: 6203.65 50-day EMA

Equities sold off sharply Friday on the back of the soft NFP print - pushing prices through mid-July lows in the process. Since that spell of weakness, price has traded either side of support at the 20-day EMA, at 6325.25, signaling scope for a deeper retracement toward the 50-day EMA at 6203.65. Clearance of this average is required to signal a stronger reversal. The primary trend remains up, leaving key short-term resistance and the bull trigger at 6468.50, the Jul 31 high.

COMMODITIES

MNI AMERICAS OIL: WTI crude prices ended lower

August 7 - Americas End-of-Day Oil Summary: WTI crude prices ended lower amid signs of progress towards peace in Ukraine given a planned Trump-Putin meeting next week and owing to continued economic concerns following Trump’s punitive 25% additional tariff on India announced yesterday.

- President Trump said that special envoy Witkoff made “great progress” in Russia and that he should meet with President Putin next week. He sounded very uncertain though on the chance of a truce despite his August 8 deadline.

- RBC: “Despite the strong pushback from the Modi government, we do believe that the White House has the tools to force a significant reduction in India imports of Russian oil.”

- India is unlikely to step down from its stance on its Russian oil purchases yet, Platts reports, though refiners are adopting a cautious approach to Russian crude.

- WTI Sep futures were down 0.8% at $63.88

- WTI Oct futures were down 0.6% at $63.02

FRIDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 08/08/2025 | 0500/1400 | Economy Watchers Survey | ||

| 08/08/2025 | 0600/0800 | ** | Private Sector Production m/m | |

| 08/08/2025 | 1115/1215 | BOE Pill At National MPC Agency Briefing | ||

| 08/08/2025 | 1230/0830 | *** | Labour Force Survey | |

| 08/08/2025 | 1230/0830 | *** | Labour Force Survey | |

| 08/08/2025 | 1420/1020 | St. Louis Fed's Alberto Musalem | ||

| 08/08/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 08/08/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 09/08/2025 | 0130/0930 | *** | CPI | |

| 09/08/2025 | 0130/0930 | *** | Producer Price Index |