MNI ASIA MARKETS ANALYSIS: Trade Talks and Negotiation Slogs

HIGHLIGHTS

- Treasuries look to finish mixed Tuesday, curves unwinding a large portion of Monday's steepening with bonds outperforming the short end.

- Markets re-assessing tariff-tied risks to global trader and the Trump Admin's efforts to meddle with the Federal Reserve's independent policy making.

- Brief midday risk-on move followed headlines that Tsy Sec Bessent (speaking at a JP Morgan event in DC - closed to public and media) sees the China tariff standoff as unsustainable and expects a de-escalation to occur.

- Sentiment cooled yet again after Tsy Sec Bessent China headlines clarified: trade negotiations will be a slog.

MNI US TSYS: Reality Check Slowly Emerging For Tariff Negotiations

- Treasuries look to finish mixed Tuesday, curves unwinding a large portion of Monday's steepening with bonds outperforming weaker short end rates (2s10s -6.174 at 58.027) as markets re-assess tariff-tied risks to global trader and the Trump Admin's efforts to meddle with the Federal Reserve's independent policy making.

- Europe returned from extended Easter holiday improved market depth more than trade volumes evidently (TYM5 at 1.2M near steady to Monday's levels) while the week openers risk-off tone was gradually unwound.

- Brief midday risk-on move extended after headlines that Tsy Sec Bessent (speaking at a JP Morgan event in DC - closed to public and media) sees the China tariff standoff as unsustainable and expects a de-escalation to occur. Bloom quickly came off the rose as sources clarified the gist of negotiations would be a "slog".

- Limited react to data: The Philly Fed non-mfg activity index fell further in April to -42.7 from -32.5 in Mar, -13.1 in Feb and -9.1 in Jan; Johnson Redbook Same-Store Retail month-to-date Y/Y sales up 7.0% (the week ending April 19 was +7.4% Y/Y). Same with Fed speakers, taking a back seat to headline risk.

- Cross asset: Gold retreats to 5372.0 currently after topping 5500.0 briefly overnight; Greenback rebounding BBG US$ index +5.01 at 1221.15; SPX eminis +110 at 5294.75.

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.32% (+0.00), volume: $2.469T

- Broad General Collateral Rate (BGCR): 4.32% (+0.01), volume: $1.027T

- Tri-Party General Collateral Rate (TCR): 4.32% (+0.01), volume: $987B

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $96B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $273B

FED Reverse Repo Operation

RRP usage climbs to $137.951B this afternoon from $114.114B yesterday. Usage had fallen to $54.772B last Wednesday, April 16 -- lowest level since April 2021. Conversely, usage had surged to the highest level since December 31, 2024 on Monday, March 31: $399.167B. The number of counterparties at 42.

US SOFR/TREASURY OPTION SUMMARY

SOFR & Treasury option flow remained mixed on net Tuesday, early SOFR calls segued to low delta put structures as underlying futures traded weaker in the short end, curves scaling back from Monday's broad based steepening (2s10s -6.385 at 57.816). As such, projected rate hike pricing consolidated vs. morning levels (*) as follows: May'25 -2.7bp (-3.4bp), Jun'25 at -17.7bp (-18.3bp), Jul'25 at -38.6bp (-41.6bp), Sep'25 -57.6bp (-59.5bp).

SOFR Options:

Block/screen, 15,000 SFRU5/SFRV5 95.62 put spds, 0.25-0.50 steepener

+2,500 SFRU5/SFRV5 95.62 put spds cab

-2,500 SFRZ6 96.25/97.25 call over risk reversals, 8.0 vs. 96.86/0.75%

+3,000 SFRU5 95.25/95.75 put spds, 3.0

+5,000 SFRK5 96.93/97.12/97.31 call flys 2.5 vs. 96.87/0.05%

+2,500 SFRM6 98.75/99.00/99.75 call trees, 0.5 ref 96.85

+4,000 SFRM6 99.00/100.00 call spds 4.25 vs. 96.855/0.10%

+2,500 0QN5 96.75/97.00 call spd vs. 0QU5 97.25/97.75 call spds 0.25 net

+5,000 0QK5 96.93/97.12/97.31 call flys, 2.5

-2,500 0QU5 96.87 straddles 70.5

+1,500 0QM5 96.87 straddles 47.5

11,000 SFRM5 95.87/96.00/96.18 broken call flys ref 95.92

21,000 SFRZ5 96.75/97.00/97.12 broken call flys ref 96.57

4,000 3QZ5 94.00/95.00 put spds ref 96.31

2,000 0QN5 96.50/96.81 put spds

2,000 SFRN5 95.93/96.25 put spds vs. 0QN5 96.81 puts

3,000 SFRM5 SFRZ5 96.75/97.00/97.12 broken call flys ref 96.565

1,500 SFRM5 96.06/96.18 call spd vs 2QM5 96.75/96.87 call spd spd

1,000 2QK5 96.75/97.00 call spds vs. 96.00/96.25 put spds ref 96.70

1,000 SFRK5 95.62/95.75/95.81/95.87 put condors ref 95.925

1,500 SFRZ5 95.68 puts ref 96.575

Treasury Options:

2,000 TYK5/Wed weekly 111 call spds

1,500 TYM5 109.5/112 put spds ref 110-27.5

1,800 TYK5 110/112.25/110.75 2x1x1 put trees

1,800 TYK5 110.75/111.25/111.5 1x1x2 call trees

2,500 USK5 110/111.5 2x1 put spds 6 ref 113-13

5,400 TYK5 112/112.75 1x3 call spds ref 110-23

5,000 TYK5 110/111 3x2 combo

2,000 FVK5 108/109/110 call flys

over 7,000 TYK5 111.25 calls 9-10 ref 110-21.5 to -24.5

2,000 TYM5 112/113/114.5/116 call condors ref 110-17.5

1,000 TYK5 109.25/109.75/110.25 put flys ref 110-19

over 12,000 TYK5/TYM5 112 call spds ref 110-20.5 to -21

2,300 TYM5 114/116 call spds, 7 ref 110-21

MNI BONDS: EGBs-GILTS CASH CLOSE: OATs Underperform, UK Curve Bull Steepens

European FI had a constructive session in the return from a 4-day holiday Tuesday.

- Shrugging off Monday's US Treasury weakness, curves bull steepened early, continuing from Thursday's pre-holiday, post-ECB price action.

- OATs underperformed, with Bloomberg reporting that President Macron is considering calling a snap legislative election in France as soon as the autumn.

- In other developments, BOE's Greene sounded less hawkish on the rate outlook compared with her previous appearances, helping UK rate cut pricing deepen, while Eurozone flash April consumer confidence printed the weakest since November 2023.

- Yields saw a modest spike in the minutes ahead of the cash close on a Bloomberg report that US Treasury Secretary Bessent expects a de-escalation in US-China trade tensions.

- The UK curve bull steepened sharply, with Germany's bull flattening. Periphery EGB spreads were flat/slightly tighter to Bund.

- Tuesday's calendar highlight is flash April PMIs, while we also get UK public sector net borrowing data and an appearance by BOE's Pill, Bailey and Breeden.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 2.5bps at 1.661%, 5-Yr is down 3.7bps at 1.982%, 10-Yr is down 2.9bps at 2.443%, and 30-Yr is down 3.7bps at 2.859%.

- UK: The 2-Yr yield is down 9bps at 3.83%, 5-Yr is down 6.4bps at 3.98%, 10-Yr is down 2.1bps at 4.545%, and 30-Yr is up 2.9bps at 5.368%.

- Italian BTP spread down 0.7bps at 116.6bps / French OAT up 1bps at 77.5bps

MNI OPTIONS: Large Euro Rate Upside Notable In Return From Holiday

Tuesday's Europe rates/bond options flow included:

- RXK5 129/130.50cs, sold at 146 in 12.5k

- ERM5 97.8125/97.9375cs, sold at 9.75 in 20k

- ERM5 98.12/98.25 call spread paper paid 1.25 on 5K

- ERU5 98.375/98.50/98.625c fly, bought for 2.5 in 10k

- ERZ5 98.3125/98.0625 put spread, paper sells for 8 in 15k

- ERZ5 98.3125p, sold at 14.5 down to 14 in 8k.

- ERZ5 98.1875/98.4375/98.6875/98.9375c condor, bought for 10 and 10.5 in 25k total

- ERZ5 98.50/62 call spread vs. 98.31/18 put spread paper paid 0.5 for the put spread on 13K

- ERZ5 98.75/99.00/99.25c fly, bought for 2.25 in 8k

- ERH6 98.4375/98.125 1x2 put spread, paper pays 2.25 in 9.5k

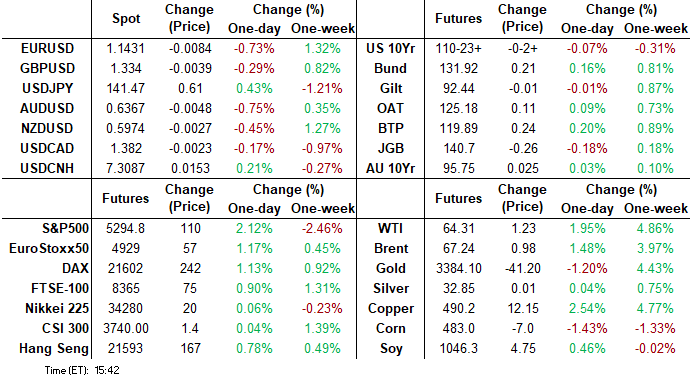

MNI FOREX: Significant Risk Recovery Places US Dollar on Firmer Footing

- Monday’s sharp extension of greenback weakness prompted the USD index to print fresh 3-year lows below the 98.00 mark. Despite an initial selloff on Tuesday, these lows remained untested and the subsequent powerful rebound for risk sentiment has provided a solid boost to the dollar, rising against all G10 peers on the session as we approach the APAC crossover.

- Despite the meagre 0.3% advance on the session, a lot of the commentary has been centred around USDJPY, which briefly printed below the psychological 140.00 mark. The pair’s selloff did fall short of the September lows, located at 139.58 – as this area appears to have assisted the short-term recovery, with spot consolidating around the 140.70 mark for much of the session, before catching an additional bid on the latest Bessent headlines on a China deal being possible - to reach session highs above 141.30. Resistance remains much further out at 143.28 initially, the April 16 high.

- Low liquidity moves on Monday may have exacerbated the price action for the dollar, and the powerful turnaround for US equities on Tuesday might suggest that a lot of bad news was priced into the market, leaving the greenback susceptible to a short-term correction. USDCHF has risen 1.1% to 0.8180 in sympathy, while EURUSD has extended its pullback to 1.1435.

- The close linkage between US-tied assets means the higher beta currencies in G10 have relatively underperformed, with the likes of AUD, NZD and GBP remaining moderately lower on the Tuesday. It is worth noting that a negative close for GBPUSD today would halt a consecutive winning streak of ten days for the pair. Support will be found at the prior breakout at 1.3207.

- Wednesday’s calendar will be highlighted by flash European PMIs as markets also eagerly await any Fed speak following Trump’s vociferous attacks on the central bank.

MNI FX OPTIONS: Expiries for Apr23 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1400(E1.9bln), $1.1500-10(E1.3bln)

- USD/JPY: Y138.50($560mln), Y141.00-20($808mln)

- AUD/USD: $0.6290-00(A$2.7bln), $0.6350-55(A$1.2bln)

- NZD/USD: $0.5855(N$704mln)

- USD/CAD: C$1.3975($562mln)

- USD/CNY: Cny7.3000($679mln)

MNI US STOCKS: Late Equities Roundup: Stock Bounce Tested By Headline Risk

- Stocks look to finish higher Tuesday, off highs as headline risk continue to hamper sentiment. Stocks surged back to late Friday levels briefly after headlines that Tsy Sec Bessent (speaking at a JP Morgan event in DC - closed to public and media) sees the China tariff standoff as unsustainable and expects a de-escalation to occur.

- Sentiment cooled yet again after Tsy Sec Bessent China headlines clarified: trade negotiations will be a slog, that negotiations haven’t started but that a deal is possible, according to people who attended his session.

- Currently, the DJIA trades up 978.46 points (2.56%) at 39149.95 (vs. Monday's low of 37830.66), S&P E-Minis up 127 points (2.45%) at 5312 (Monday low of 5127.25), Nasdaq up 421.2 points (2.7%) at 16292.42 (Monday low of 15685.33).

- Consumer Discretionary and Financial sector shares led gainers in late trade, PulteGroup +8.14%, Caesars Entertainment +6.00%, Royal Caribbean Cruises +5.13%, Tesla +4.72% and CarMax +4.38% led gainers in the Discretionary sector.

- Financials were buoyed by Invesco +8.75%, Global Payments +5.14%, KKR & Co I+4.79%, W R Berkley +4.72% and Discover Financial Services +4.38%.

- On the flipside, defense stocks trade broadly weaker with Northrop Grumman-14.55%, RTX -9.85% while Huntington Ingalls Industries dipped -0.85%.

- Earnings after the close: Capital One Financial, Baker Hughes, Tesla, Manhattan Associates, EQT Corp, Steel Dynamics Inc, Intuitive Surgical Inc, Enphase Energy Inc and Range Resources Co.

MNI EQUITY TECHS: E-MINI S&P: (M5) Bear Threat Remains Present

- RES 4: 5773.25 High Apr 2

- RES 3: 5652.57 50-day EMA

- RES 2: 5528.75 High Apr 10 and the bull trigger

- RES 1: 5437.24 20-day EMA

- PRICE: 5242.75 @ 14:23 BST Apr 25

- SUP 1: 5098.16 61.8% retracement of the Apr 7 - 10 bounce

- SUP 2: 4996.43 76.4% retracement of the Apr 7 - 10 bounce

- SUP 3: 4832.00 Low Apr 7 and the bear trigger

- SUP 4: 4760.88 1.618 proj of the Feb 19 - Mar 13 - 25 price swing

A reversal higher in S&P E-Minis on Apr 9 highlighted the start of a correction. The trend condition has been oversold following recent weakness and gains have allowed this to unwind. The contract remains below important resistance points and the trend condition is bearish. The latest move down signals the end of the corrective cycle. Sights are on 4832.00, the Apr 7 low and bear trigger. Initial resistance to watch is 5437.24, the 20-day EMA.

MNI COMMODITIES: Crude Gains, Gold Pulls Back From Record High

- Oil prices are higher today after the US imposed sanctions on Iran’s LPG trade, reversing most of yesterday’s losses amid demand concerns due to tariffs and US monetary policy.

- Comments by Trump about his call with Netanyahu and Bessent’s comments on China were late drivers of the rally.

- WTI Jun 25 is up by 1.9% at $64.3/bbl.

- A bearish theme in WTI futures remains intact and the recovery since Apr 9 is - for now - considered corrective. The move higher is allowing an oversold trend condition to unwind.

- Initial firm resistance is seen at $64.49, the Mar 5 low and a recent breakout level.

- Meanwhile, gold has pulled back from a fresh record high reached earlier in the session, with the yellow metal currently 1.4% lower today at $3,377/oz.

- Gold remains 8% higher MTD, amid ongoing haven demand, and it traded briefly at the $3,500 level earlier today, before traders took profit.

- The trend needle in gold continues to point north, with initial resistance at today’s intra-day high, followed by $3,547.9, a Fibonacci projection.

- Elsewhere, copper has rallied by 2.2% today to $489/lb, amid optimism of a de-escalation in US-China trade tensions. However, gains were pared after US Treasury Secretary Bessent said that negotiations with China will be a slog.

- For copper futures, the latest recovery, although strong, appears corrective - for now. However, price pierced $490.27, a Fibonacci retracement today, and a clear break would open $521.30, the Mar 28 high.

WEDNESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 23/04/2025 | 0600/0700 | *** | Public Sector Finances | |

| 23/04/2025 | 0630/0730 | DMO remit revision following FY24/25 CGNCR | ||

| 23/04/2025 | 0715/0915 | ** | S&P Global Services PMI (p) | |

| 23/04/2025 | 0715/0915 | ** | S&P Global Manufacturing PMI (p) | |

| 23/04/2025 | 0730/0930 | ** | S&P Global Services PMI (p) | |

| 23/04/2025 | 0730/0930 | ** | S&P Global Manufacturing PMI (p) | |

| 23/04/2025 | 0800/1000 | ** | S&P Global Services PMI (p) | |

| 23/04/2025 | 0800/1000 | ** | S&P Global Manufacturing PMI (p) | |

| 23/04/2025 | 0800/1000 | ** | S&P Global Composite PMI (p) | |

| 23/04/2025 | 0800/1000 | ECB Wage Tracker | ||

| 23/04/2025 | 0830/0930 | *** | S&P Global Manufacturing PMI flash | |

| 23/04/2025 | 0830/0930 | *** | S&P Global Services PMI flash | |

| 23/04/2025 | 0830/0930 | *** | S&P Global Composite PMI flash | |

| 23/04/2025 | 0900/1100 | ** | Construction Production | |

| 23/04/2025 | 0900/1100 | * | Trade Balance | |

| 23/04/2025 | 1030/1130 | BOE's Pill speech at University of Leeds | ||

| 23/04/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 23/04/2025 | 1300/0900 | Chicago Fed's Austan Goolsbee | ||

| 23/04/2025 | 1330/0930 | St. Louis Fed's Alberto Musalem | ||

| 23/04/2025 | 1330/0930 | Fed Governor Christopher Waller | ||

| 23/04/2025 | 1345/0945 | *** | S&P Global Manufacturing Index (Flash) | |

| 23/04/2025 | 1345/0945 | *** | S&P Global Services Index (flash) | |

| 23/04/2025 | 1400/1000 | *** | New Home Sales | |

| 23/04/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 23/04/2025 | 1530/1130 | ** | US Treasury Auction Result for 2 Year Floating Rate Note | |

| 23/04/2025 | 1700/1300 | * | US Treasury Auction Result for 5 Year Note | |

| 23/04/2025 | 1715/1815 | BOE's Bailey at Institute of International Finance | ||

| 23/04/2025 | 1800/1400 | Fed Beige Book | ||

| 23/04/2025 | 1800/1900 | BOE's Breeden on Monetary Policy and Financial Stability | ||

| 23/04/2025 | 1915/2115 | ECB's Lane in panel on Central Bankers' Dilemmas Amid Changing Liquidity | ||

| 23/04/2025 | 1945/2145 | ECB's Cipollone in panel on Tokenization and the Financial System | ||

| 23/04/2025 | 2230/1830 | Cleveland Fed's Beth Hammack |