MNI ASIA MARKETS ANALYSIS: Stocks Mark New All-Time Highs

HIGHLIGHTS

- Treasuries sold off sharply after higher than expected jobs gains for June, some desks positioned for rally after Wednesday's ADP job LOSS.

- Strong Labor Market data weighed heavily on projected rate cuts into year end, from nearly -75bp prior to near -50bp at midday.

- Stocks liked to strong jobs data, SPX eminis and Nasdaq climbed to new all-time highs (DJIA still off early December 2024 highs).

- The selloff in US$ from June 23 highs has halted.

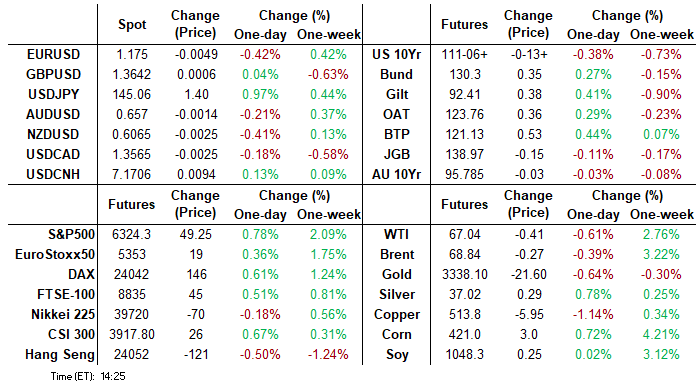

US TSYS

MNI US TSYS: Yields Rebound on Strong June Jobs Gain, Dip in Unemployment

- Treasuries are broadly weaker into the early pre-holiday close, off this morning's post employment data lows - rates hold a rather narrow range after the initial knee-jerk sell-off.

- Brief two-way after the final data for the session, ISM Services Prices Paid & Employment slightly lower, New Orders higher while Factory/Durables Orders are in-line. slightly lower than expected S&P Global Services PMI, Composite near in-line.

- Currently, Sep'25 10Y trades -13 at 111-07 (110-31L / 111-28H). Through first key support at 111.08.5 (the 20-day EMA), next 110-30+ 50-day EMA, followed by 110-16 (Low Jun 20). Curves bear flatten: 2s10s -3.682 at 45.321; 5s30s -4.441 at 89.048. 10Y yield tapped 4.3576% high finished at 4.3457%.

- A 46k beat for NFPs in June (147k vs cons 106k) vs a 26k miss for private payrolls (74k vs cons 100k). The difference being government payrolls surging by 73k for the largest increase since Mar 2024. It comprised of -7k for federal (still weak after DOGE cuts earlier this year) but state +47k and local +33k.

- The major downside surprise in the unemployment rate (4.117% unrounded is the lowest since January, down from 4.244% prior and well below the rounded 4.3% consensus) came with a drop of 222k in the number of unemployed (the largest drop of the year) after 4 consecutive rises.

- Projected rate cut pricing significantly cooler vs. this morning's pre-data (*) levels: Jul'25 at -1.2bp (-6.3bp), Sep'25 at -19.1bp (-30.1bp), Oct'25 at -34.2bp (-47.3bp), Dec'25 at -51.8bp (-67bp).

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.40% (-0.04), volume: $2.882T

- Broad General Collateral Rate (BGCR): 4.37% (-0.02), volume: $1.144T

- Tri-Party General Collateral Rate (TCR): 4.37% (-0.02), volume: $1.104T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $129B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $268B

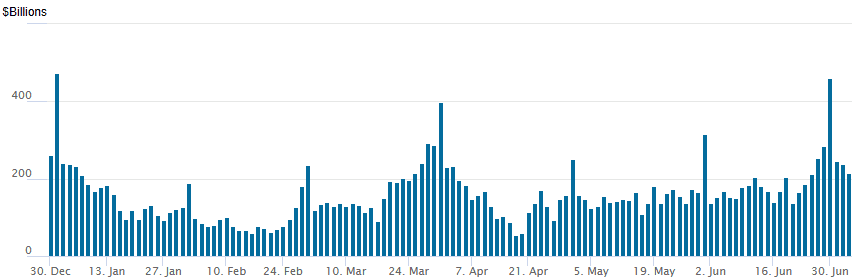

FED Reverse Repo Operation:

RRP usage slips to $214.665B this afternoon from $237.307B yesterday, total number of counterparties at 45. Usage had fallen to $54.772B on Wednesday, April 16 -- lowest level since April 2021 - compares to yesterday's (July 1) $460.731B highest usage since December 31.

US SOFR/TREASURY OPTION SUMMARY

Late SOFR options mildly bullish w/ call spd buying put sales and some bear curve flattener trade: Underlying futures remain broadly weaker but off initial post-employment data lows. Projected rate cut pricing significantly cooler vs. this morning's pre-data (*) levels: Jul'25 at -1.2bp (-6.3bp), Sep'25 at -19.1bp (-30.1bp), Oct'25 at -34.2bp (-47.3bp), Dec'25 at -51.8bp (-67bp).

SOFR Options:

+4,000 SFRZ5 96.50/96.25 call spds, 6.0 ref 96.17

-9,000 SFRU5 95.62/95.75 put spds, 3.0 ref

2,000 SFRZ5 95.87 put/SFRM6 96.00 put spd, 5 net/flattener

Update +32,000 SFRZ5 95.75/95.87/96.25/96.37 put condors, 6.0-6.25 ref 96.17

-5,000 0QN5 96.62/96.81 put spds, 7.0 vs. 96.77/0.40%

-10,000 SFRU5 96.00/96.37 call spds, 3.75 ref 95.90

-4,000 SFRQ5 95.62/95.75 put spds, 1.75 ref 95.90

-5,000 SFRU5 96.00 calls, 6.0 ref 95.895

6,100 0QN5 97.00 calls vs. 0QU5 96.37 puts ref 96.875

4,000 SFRH6 97.25/97.50 call spds vs. 3QH6 97.12/97.37

2,000 0QN5 96.50/96.75 put spds, ref 96.885

1,500 0QQ5 96.93/97.18/97.56 broken call flys ref 96.885

over 17,000 SFRN5 96.12 calls

+2,000 SFRZ5 96.50/96.75 vs. 2QZ5 97.00/97.18 call spd spd, 0.5 net steepener

+5,000 SFRN5 96.06/96.18/96.31 call flys, 1.5

+5,000 SFRU5 96.25/96.37 call spds, 1.25 vs. 95.98/0.06%

2,000 SFRH6 96.00/96.50 put spds, 20.0 vs 96.545/0.25%

-2,000 SFRZ5 96.25/96.50 call spds vs 95.75/96.00 put spds, 3.5 net call spd over

+1,500 SFRU5 95.68/95.81 2x1 put spd, 2.5

Treasury Options

5,000 TYU5 106/108 put spds, ref 111-07.5

5,000 TYU5 110.5/111.5/112.5 call flys

2,500 TYU5 109/110/111 put trees,

-30,000 TYU5 112 calls, 57 total volume over 38k

2,000 USU5 104/107 2x1 put spds

+1,000 Mon wkly TY 110.75/111.25 put spds, 4 vs. 111/29/0.10%

+1,500 wk2 TY 111 puts, 8

+2,000 TYU5 107 puts, 7

-1,750 FVQ5 108/109.5 call spds, 47 vs. 111-25.5/0.52%

2,000 TYQ5 112.5/113.5/114.5 call trees ref 111-26

over 5,200 TYQ5 112 calls, 34-35 ref 111-25 to -25.5

MNI BONDS: EGBs-GILTS CASH CLOSE: Yields Pull Back Despite Strong Data

European yields fell in a bull flattening move Thursday, shrugging off a stronger-than-expected US employment report.

- Bunds and Gilts were stronger in early trade, recovering some of the ground lost after Wednesday's UK fiscal panic-related selloff and despite notable French/Spanish bond supply and an upward revision to Eurozone and UK final PMIs.

- US nonfarm payrolls came in above consensus with the unemployment rate unexpectedly falling, pushing yields sharply higher, but the move reversed over the rest of the afternoon into the cash close.

- The German and UK curves both bull flattened, with Gilts outperforming after Wednesday's sizeable underperformance.

- Periphery/semi-core EGB spreads were mixed, with BTPs outperforming and OAT spreads widening slightly.

- Friday's calendar includes German factory orders and French/Spanish industrial production data, along with appearances by ECB's Elderson and Villeroy, as well as BOE's Taylor.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 2.9bps at 1.834%, 5-Yr is down 4.1bps at 2.142%, 10-Yr is down 4.9bps at 2.615%, and 30-Yr is down 4bps at 3.077%.

- UK: The 2-Yr yield is down 4bps at 3.841%, 5-Yr is down 6.2bps at 3.98%, 10-Yr is down 7bps at 4.542%, and 30-Yr is down 8.2bps at 5.338%.

- Italian BTP spread down 1.6bps at 83.4bps / French OAT up 0.3bps at 66.1bps

MNI OPTIONS: Mixed Trade Preceding US Payrolls

Thursday's Europe rates/bond options flow included:

- RXQ5 130/129/128p fly, bought for 17 in 1.25k

- ERV5 98.125/98.0625/98.00p ladder, bought for 0.75 in 8k

- SFIZ5 96.40/96.65/96.90c fly vs 96.05p, bought the cs for 2 in 14k

- SFIZ5 96.25p, bought for 7.75 in 4k

MNI FOREX: USD Remains Stronger on NFP, but Gains Fading Fast

- The USD is holding the bulk of the post-payrolls gains, with JPY, NZD and CHF among the hardest hit - as identified by the run-up in vols headed into today's print. Infitting with straddle pricing, USD/JPY trades ~120 pips above pre-data levels, but has faded off the high of 145.23.

- While EUR/USD initially fell to a weekly low at 1.1718, the losses are being pared swiftly, rallying ~40 pips off lows - likely as markets assess the continued decline in the size of the labor force and participation suggesting diminishing labor supply (more on that above).

- For the USD Index, this has put price back above the well-trodden downtrendline support drawn off the March 2024 low and - theoretically - back inside the falling wedge pattern that's dictated the USD's decline this year.

- We wrote earlier this week that the oversold position does raise the possibility that either; a correction unfolds soon, or that the pace of the trend slows down, resulting in more volatile price action going forward.

MNI FX OPTIONS: Expiries for Jul04 NY cut 1000ET (Source DTCC)

- USD/JPY: Y142.00($720mln), Y143.45-60($1.1bln), Y144.00-20($776mln)

- GBP/USD: $1.3820-35(Gbp592mln)

- AUD/USD: $0.6500(A$1.4bln), $0.6600(A$2.6bln)

- USD/CAD: C$1.3925($650mln)

MNI US STOCKS: At/Near All-Time Highs into Early Equities Close

- Stocks remain strong ahead the early Thursday close, at (SPX emini & Nasdaq) or near (DJIA) all-time highs after headline employment data showed higher than expected job gains for June with government payrolls surging by 73k for the largest increase since Mar 2024.

- Currently, the DJIA trades up 358.86 points (0.81%) at 44842.17 (all-time high of 45073.63 on December 4), S&P E-Minis up 49.75 points (0.79%) at 6324.5 vs. 6328.25 all-time high today, Nasdaq up 196.7 points (0.9%) at 20579.45 vs. 20598.44 all-time high today.

- Information Technology and Energy sectors continued to outperform, leading gainers included: First Solar +8.60%, Enphase Energy +4.28%, Cadence Design Systems +5.15%, Synopsys +5.39%, AES Corp +3.41% and Vistra +2.36%.

- Conversely, home builder shares traded weaker as the nod towards a stronger labor market chilled projected rate cuts into year end, laggers included: Lennar Corp -3.94%, DR Horton -2.39%, NVR Inc and PulteGroup both -1.75%. Other laggers included Dollar General Corp -1.68%, Dollar Tree -1.23%, Bunge Global -3.37% and Archer Daniels Midland -1.41%.

- Reminder, stocks are closing early ahead of Friday's 4th of July Holiday, both the New York Stock Exchange and Nasdaq will close at 1300ET.

MNI EQUITY TECHS: E-MINI S&P: (U5) Continues To Appreciate

- RES 4: 6402.44 1.382 proj of the May 23 - Jun 11 - 23 price swing

- RES 3: 6381.00 1.764 proj of the Apr 7 - 10 - 21 price swing

- RES 2: 6356.12 1.236 proj of the May 23 - Jun 11 - 23 price swing

- RES 1: 6333.25 Intraday high

- PRICE: 6326.00 @ 1420ET Jul 3

- SUP 1: 6223.25 Low Jun 30

- SUP 2: 6118.90/5987.37 20- and 50-day EMA values

- SUP 3: 5811.50 Low May 23

- SUP 4: 5645.75 Low May 7

The trend condition in S&P E-Minis is unchanged, it remains bullish and the contract continues to appreciate. Resistance at 6128.75, the Jun 11 high, has recently been breached. The break confirms a resumption of the uptrend that started Apr 7. Note too that a key resistance and a bull trigger at 6277.50, the Feb 21 high, has also been cleared. Sights are on 6356.12, a Fibonacci projection. Key support is at the 50-day EMA - at 5987.

FRIDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 04/07/2025 | 0600/0800 | ** | Manufacturing Orders | |

| 04/07/2025 | 0645/0845 | * | Industrial Production | |

| 04/07/2025 | 0700/0900 | ** | Industrial Production | |

| 04/07/2025 | 0700/0900 | ** | Unemployment | |

| 04/07/2025 | 0730/0930 | ** | S&P Global Final Eurozone Construction PMI | |

| 04/07/2025 | 0800/1000 | * | Retail Sales | |

| 04/07/2025 | 0800/1000 | ECB Elderson Speech At IMF OEDNE/World Bank Meeting | ||

| 04/07/2025 | 0830/0930 | ** | S&P Global/CIPS Construction PMI | |

| 04/07/2025 | 0900/1100 | ** | PPI | |

| 04/07/2025 | 1500/1600 | BOE Taylor Speech On Natural Interest Rate |