MNI ASIA MARKETS ANALYSIS: Soft PPI Underpins Rate Cut Pricing

HIGHLIGHTS

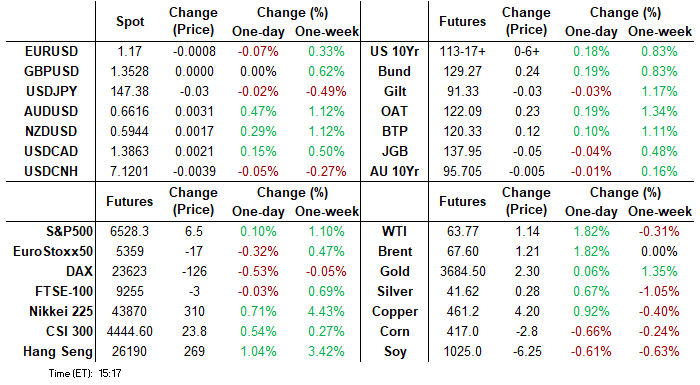

- Weak Data and a strong 10Y Treasury auction re-open (4.033% vs. 4.047% WI) helped push Treasuries to session highs Wednesday, Dec'25 10Y futures near last Friday's high of 113-21.5.

- USD index reaction muted, with just a 0.05% move lower on the session. Major pairs such as EURUSD and USDJPY have held relatively contained ranges as we await the August CPI report to follow on Thursday.

- Projected rate cuts rebound from early morning (*) levels: Sep'25 at -28bp (-27.2bp), Oct'25 at -47.7bp (-45.9bp), Dec'25 at -70bp (-67.5bp), Jan'26 at -82.7bp (-79.9bp).

- Focus turns to Thursday's ECB rate decision/press conference and the key US CPI release.

US TSYS

MNI US TSYS: Near Post-Auction Highs, Focus on Thu's CPI after Today's Dovish PPI

- Treasuries look to finish near late Thursday session highs after soft PPI data and a strong 10Y Treasury auction re-open, futures back near last Friday highs ahead of tomorrow's headline CPI inflation data.

- After the bell, Dec'25 10Y futures trades +8 at 113-19 vs. 113-20.5 high, initial technical resistance at 113-21+ High Sep 5, followed by 113-26.5 (2.764 proj of the Jul 15 - 22 - 28 price swing).

- The main headline PPI final demand unexpectedly fell by 0.1% M/M (+0.3% expected, with a prior rev to 0.7% from 0.9% prior). The ex-food/energy metric posted identical figures, including the downward revision. This was the lowest for each since April.

- Treasuries climbed higher after the strong $39B 10Y note auction re-open (91282CNT4) stopped through: drawing 4.033% high yield vs. 4.047% WI; 2.65x bid-to-cover vs. 2.35x prior. Dec'25 10Y futures extended highs: 113-20.5, 4.0321% yld, before drawing some fast$ selling.

- Despite the dovish adjustment for US yields in the aftermath of the US PPI report, the impact on the USD index has been more muted, with just a 0.05% move lower on the session.

- Focus turns to Thursday's ECB rate decision/press conference and the key US CPI release: Consensus (Bloomberg median) is for core CPI to come in at 0.3% M/M rounded in August, same as July (0.32% unrounded). Unrounded core CPI expectations suggest a slight skew toward risks of a rounded-up 0.4%, with an unrounded MNI median of 0.32% and range of estimated of 0.29% to 0.36%.

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.40% (+0.00), volume: $2.863T

- Broad General Collateral Rate (BGCR): 4.38% (-0.01), volume: $1.143T

- Tri-Party General Collateral Rate (TCR): 4.38% (-0.01), volume: $1.114T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $112B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $208B

FED Reverse Repo Operation

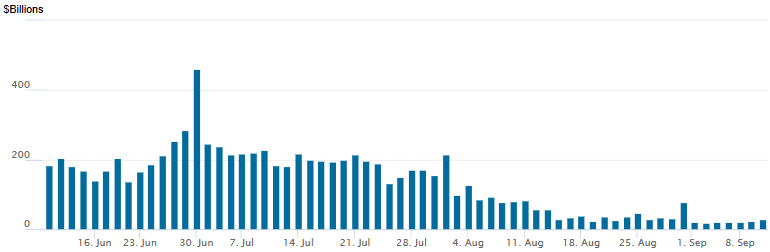

RRP usage climbs to $29.400B with 18 counterparties this afternoon from $22.915B Tuesday. Compares to $17.923B on Wednesday, Sep 3 - the lowest levels since early April 2021. This year's high usage of $460.731B occurred on June 30.

US SOFR/TREASURY OPTION SUMMARY

SOFR & Treasury options leaned towards upside calls Wednesday, focus on tomorrow's CPI inflation data after this morning's softer than expected PPI underpinned underlying futures. Rate futures drifting around post-data highs while projected rate cuts rebound from early morning (*) levels: Sep'25 at -28bp (-27.2bp), Oct'25 at -47.7bp (-45.9bp), Dec'25 at -70bp (-67.5bp), Jan'26 at -82.7bp (-79.9bp).

SOFR Options:

-8,000 SFRZ5 96.50 calls, 6.5 vs. 96.355/0.33%

-2,500 SFRH6 97.00 calls, 9.0 vs. 96.595/0.26%

-5,000 SFRZ5 96.00/96.12/96.25/96.37 call condors, 4.0 ref 96.355

-7,000 SFRU5 96.00 calls, 1.0 ref 95.9825

+4,000 SFRZ5 96.68/96.87/96.93 call flys, 1.25

10,000 0QZ5 96.87 put vs. 3QZ5 96.62 put spds 0.0 net/Blue Dec over

Block/screen over 35,000 SFRZ5 96.43 calls, 8.0 ref 96.33 to -33.5

Block, 2,870 SFRH6 96.87 calls 54.5 vs. 97.095/0.58%

Block, 5,000 SFRH6 96.50/96.87/97.00 broken put trees, 4.75/splits vs. 97.11

-9,000 SFRH6 96.00/96.31/96.43 broken put trees, 3.0

9,000 SFRH6 96.00 puts, 1.75 last

3,500 SFRV5 96.37/96.62/97.00 broken call flys ref 96.335

+3,274 SFRZ5 96.50/96.62/96.68/96.81 call condors, 1.0

5,000 SFRX5 96.43/96.68 call spds

5,000 SFRV5 96.31 puts ref 96.335

2,000 SFRZ5 96.50/96.62 call spds ref 96.33

+5,000 SFRU5 95.93/96.00/96.06 call flys, 2.5

over 7,000 SFRU5 96.00/96.12/96.25 call flys, 0.5-0.75 ref 95.9725

Treasury Options:

-8,170 TYV5 112.5/113.5/114.5 call flys, 20 vs. 113-15/0.05%

6,800 TYV5 114.5/115 call spds ref 113-16.5

4,100 FVV5 110.5/111 call spds

over 4,500 FVX5 110 calls, 31 ref 109-29 to -28.75

10,000 TYX5 111/112 put spds, 8 ref 113-15

Block, 10,000 TYX5 113/114 call spds vs. 111.5/113 put spds 0.0 net

10,000 TYV5 113.5/TYX5 112.5 put spds, 2 net/Nov over

2,000 USV5 112/113/115 1x1x2 broken put trees

2,000 TYV5 113.5 straddles,

+2,000 FVZ5 110/111 call spds vs. 108.75 put, 2.0 net ref 109-25

2,000 USX5 133 calls vs. 3,000 USX5 104 puts ref 116-27

-1,000 TYZ5 113 straddles, 209 ref 113-10

+5,000 TUV5 104/104.75 call over risk reversals, 2

-4,000 TYZ5 130.5 calls w/ -2,000 TYZ5 104.5 puts ref 113-10.5

1,140 TYV5 112/112.5 3x2 put spds ref 113-09.5

2,200 TYV5 112.25 puts ref 113-08.5

MNI BONDS: EGBs-GILTS CASH CLOSE: Short-End Underperformance Ahead Of ECB

EGBs and Gilts traded in mixed fashion Wednesday, with underperformance at the short end of respective curves.

- While Gilt yields remained within this week's ranges throughout the day, 10Y Bund yields touched an intraday post-Aug 7 low in early trade as markets digested overnight news of Poland downing Russian drones in its territory.

- Lower-than-expected inflationary pressures in the US producer price report saw a brief rally across global core instruments, but EGBs and Gilts were content to drift into the cash close ahead of event risk Thursday.

- The German curve twist flattened on the day, with the UK's bear flattening.

- OAT spreads were little changed albeit underperformed periphery/semi-core EGBs more widely, following overnight news that French President Macron had named centrist/ex-defence minister Lecornu as the new Prime Minister.

- While US CPI will garner significant attention, Thursday's European highlight is the ECB decision (MNI preview here in PDF).

- Along with the expected rate-hold along with communications reiterating a data dependent approach, Lagarde's characterisation of economic resilience and/or the extent to which uncertainty has been alleviated by the US-EU trade deal should help shape market reaction.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 1.1bps at 1.952%, 5-Yr is unchanged at 2.225%, 10-Yr is down 0.7bps at 2.652%, and 30-Yr is down 0.7bps at 3.273%.

- UK: The 2-Yr yield is up 2.6bps at 3.94%, 5-Yr is up 1.8bps at 4.055%, 10-Yr is up 1bps at 4.633%, and 30-Yr is up 0.5bps at 5.482%.

- Italian BTP spread down 0.6bps at 81.5bps / French OAT spread down 0.3bps at 80.9bps

MNI EGB OPTIONS: Plethora Of Call Spread Structures Trade In Euribor Wednesday

Wednesday's Europe rates/bond options flow included:

- ERH6 98.31/98.43 call spread vs. 97.93/97.81 put spread (vs. 98.085), paper paid 0.75 for the package on 4K, buying the call spread

- ERU5 98.00/98.06 call spread paper paid 0.25 on 6.5K

- ERU6 98.25/98.4375 call spread vs. 97.9375/97.75 put spread paper paid 0.75 for the call spread on 6K

MNI FOREX: AUDUSD Trades to Fresh 10-Month Highs Following Soft US PPI

- Despite the dovish adjustment for US yields in the aftermath of the US PPI report, the impact on the USD index has been more muted, with just a 0.05% move lower on the session. Major pairs such as EURUSD and USDJPY have held relatively contained ranges as we await the August CPI report to follow on Thursday.

- With that said, firmer equity sentiment and higher oil prices have notably buoyed riskier currencies, with AUD, NZD and NOK clearly outperforming in G10.

- AUDUSD has breached a key resistance point, trading up to a fresh 10-month high of 0.6636 in the process and strengthening the underlying bullish trend. The next targets for the move are 0.6688 (Nov 07 high) and 0.6700, the 76.4% retracement of the Oct-Apr selloff.

- In contrast, lingering French political risks and geopolitical developments between Russia/Poland have relatively weighed on the Euro, allowing EURAUD to extend its recent depreciation. Despite being a slow burner, EURAUD has respected the breach of trendline support (drawn from the year’s lows) and the cross briefly slipped through the July 31 lows and bear trigger at 1.7674. Targets on the downside include 1.7462 (Jun 10 low) and 1.7248 (May 14 low).

- Oil strength compounded the performance for NOK on the back of the higher-than-expected underlying Norwegian CPI print (3.1% Y/Y vs. Exp. 2.9%). As a result, EURNOK has traded steadily lower, clearing the September lows. The cross has also shown through 61.8% retracement for the upleg posted off the June low, opening next support into 11.5416.

- During Thursday’s APAC session, RBNZ Governor Hawkesby will speak, before Australia consumer inflation expectations. The focus will then turn to the ECB rate decision/press conference and the key US CPI release.

MNI FX OPTIONS: Expiries for Sep11 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1635-50(E3.4bln), $1.1700(E1.1bln), $1.1735-50(E2.2bln), $1.1775(E645mln), $1.1800(E1.3bln), $1.1825(E2.2bln), $1.1850-65(E1.3bln)

- USD/JPY: Y145.75($1.1bln), Y146.50($690mln), Y146.80($650mln), Y147.10-20($1.2bln), Y149.00-15($801mln), Y150.00($1.1bln)

- GBP/USD: $1.3600(Gbp609mln)

MNI US STOCKS: Late Equities Roundup: S&Ps, Nasdaq Paring Early Session Gains

- Stocks remain mixed late Wednesday, the weaker DJIA (after rising to new record high of 45,711.34 Tuesday) dragging the S&P eminis and Nasdaq indexes off early session highs. Currently, the DJIA trades down 237.69 points (-0.52%) at 45474.62, S&P E-Minis up 10 points (0.15%) at 6532, Nasdaq down 10.8 points (0%) at 21866.97.

- Information Technology and Utility/Energy sector shares continued to outperform in the second half, the tech sector led by software maker Oracle - rallying a whopping 38% after announcing it had secured "several billion-dollar contracts in it's latest quarter" the WSJ reported.

- Chip makers continued to underpin the tech sector: Broadcom +8.36%, Arista Networks +6.46%, NVIDIA +3.95% and Micron Technology +3.87%.

- Utility/Energy sector shares held gains as oil prices rebound (WTI +1.13 at 63.76): Vistra Corp +8.07%, Constellation Energy +7.80%, NRG Energy +5.22%, PG&E Corp +3.14%, APA Corp +5.42%, Baker Hughes +3.29% and Halliburton +3.22%.

- Conversely, Consumer Discretionary and Health Care sectors revered prior session gains, the former weighed by Amazon.com -3.02%, CarMax -2.70%, McDonald's -2.49%, Chipotle Mexican Grill -2.17%.

- Meanwhile, equipment and services shares weighed on the Health Care sector: Bio-Techne -4.82%, HCA Healthcare -4.38%, Insulet -4.22% and ResMed -3.52%.

MNI EQUITY TECHS: E-MINI S&P: (U5) Fresh Cycle High

- RES 4: 6673.37 2.236 proj of the May 23 - Jun 11 - 23 price swing

- RES 3: 6617.73 2.0% 10-dma envelope

- RES 2: 6600.00 Round number resistance

- RES 1: 6565.25 Intraday high

- PRICE: 6557.50 @ 07:23 BST Sep 10

- SUP 1: 6462.58/6371.75 20-day EMA / Low Sep 2

- SUP 2: 6365.35 50-day EMA

- SUP 3: 6313.25 Low Aug 6

- SUP 4: 6239.50 Low Aug 1 and a key support

A bull cycle in S&P E-Minis remains intact and the latest pullback has once again proved to be a shallow correction. The contract has traded to a fresh cycle today, breaching the Sep 5 high of 6541.75. This confirmed a resumption of the uptrend and maintains the price sequence of higher highs and higher lows. Sights are on the 6600.00 handle next, a Fibonacci projection. Initial support to watch is 6462.58, the 20-day EMA.

MNI COMMODITIES: Crude Extends Gains, Gold Rises As Geopolitical Tensions Escalate

- Crude prices have extended gains amid the escalation in geopolitical tensions following the shooting down of Russian drones over Poland.

- WTI spiked to an intraday high $64.08/b, before paring some of the move, after Trump sent a cryptic Truth Social post in response to the Russian drone incursion. Initial strength during the day was driven by earlier geopolitical tensions and risks of further sanctions/secondary tariffs on Russia, despite a large US crude inventory build.

- WTI OCT 25 is currently up by 1.7% at $63.7/bbl.

- Despite recent gains, the trend condition in WTI futures remains bearish. Initial resistance to watch is $66.03, the Sep 2 high. A stronger resumption of weakness would pave the way for a move towards $57.71, the May 30 low.

- Elsewhere, spot gold has risen by 0.6% to $3,648/oz, keeping the yellow metal close to yesterday’s all-time high at $3,674.3.

- Bullion has rallied ~10% since Aug 22 amid widespread expectations that the Fed will cut rates next week.

- Analysts at ANZ bank have raised their year-end gold forecast to $3,800 as they say rising risks to the labour market will likely prompt the Fed to maintain its easing stance through to March 2026.

- Gold remains in a clear bull cycle and last week’s gains plus this week’s bullish start reinforce current conditions. The next objective is $3,674.8, a Fibonacci projection, followed by $3,700 round number resistance.

THURSDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 11/09/2025 | 0600/0800 | *** | Final Inflation Report | |

| 11/09/2025 | 0600/0800 | *** | Final Inflation Report | |

| 11/09/2025 | 1100/0700 | *** | Turkey Benchmark Rate | |

| 11/09/2025 | - | *** | Money Supply | |

| 11/09/2025 | - | *** | New Loans | |

| 11/09/2025 | - | *** | Social Financing | |

| 11/09/2025 | 1215/1415 | *** | ECB Deposit Rate | |

| 11/09/2025 | 1215/1415 | *** | ECB Main Refi Rate | |

| 11/09/2025 | 1215/1415 | *** | ECB Marginal Lending Rate | |

| 11/09/2025 | 1230/0830 | *** | Jobless Claims | |

| 11/09/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 11/09/2025 | 1230/0830 | * | Household debt-to-income | |

| 11/09/2025 | 1230/0830 | *** | CPI | |

| 11/09/2025 | 1230/0830 | *** | CPI | |

| 11/09/2025 | 1230/0830 | *** | CPI | |

| 11/09/2025 | 1245/1445 | ECB Press Conference | ||

| 11/09/2025 | 1415/1615 | ECB Lagarde Presents Rate Decision on ECB Podcast | ||

| 11/09/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 11/09/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 11/09/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 11/09/2025 | 1700/1300 | *** | US Treasury Auction Result for 30 Year Bond | |

| 11/09/2025 | 1800/1400 | ** | Treasury Budget | |

| 12/09/2025 | 0430/1330 | ** | Industrial Production |