US TSYS: Near Post-Auction Highs, Focus on Thu's CPI after Today's Dovish PPI

Sep-10 19:10

- Treasuries look to finish near late Thursday session highs after soft PPI data and a strong 10Y Treasury auction re-open, futures back near last Friday highs ahead of tomorrow's headline CPI inflation data.

- After the bell, Dec'25 10Y futures trades +8 at 113-19 vs. 113-20.5 high, initial technical resistance at 113-21+ High Sep 5, followed by 113-26.5 (2.764 proj of the Jul 15 - 22 - 28 price swing).

- The main headline PPI final demand unexpectedly fell by 0.1% M/M (+0.3% expected, with a prior rev to 0.7% from 0.9% prior). The ex-food/energy metric posted identical figures, including the downward revision. This was the lowest for each since April.

- Treasuries climbed higher after the strong $39B 10Y note auction re-open (91282CNT4) stopped through: drawing 4.033% high yield vs. 4.047% WI; 2.65x bid-to-cover vs. 2.35x prior. Dec'25 10Y futures extended highs: 113-20.5, 4.0321% yld, before drawing some fast$ selling.

- Despite the dovish adjustment for US yields in the aftermath of the US PPI report, the impact on the USD index has been more muted, with just a 0.05% move lower on the session.

- Focus turns to Thursday's ECB rate decision/press conference and the key US CPI release: Consensus (Bloomberg median) is for core CPI to come in at 0.3% M/M rounded in August, same as July (0.32% unrounded). Unrounded core CPI expectations suggest a slight skew toward risks of a rounded-up 0.4%, with an unrounded MNI median of 0.32% and range of estimated of 0.29% to 0.36%.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

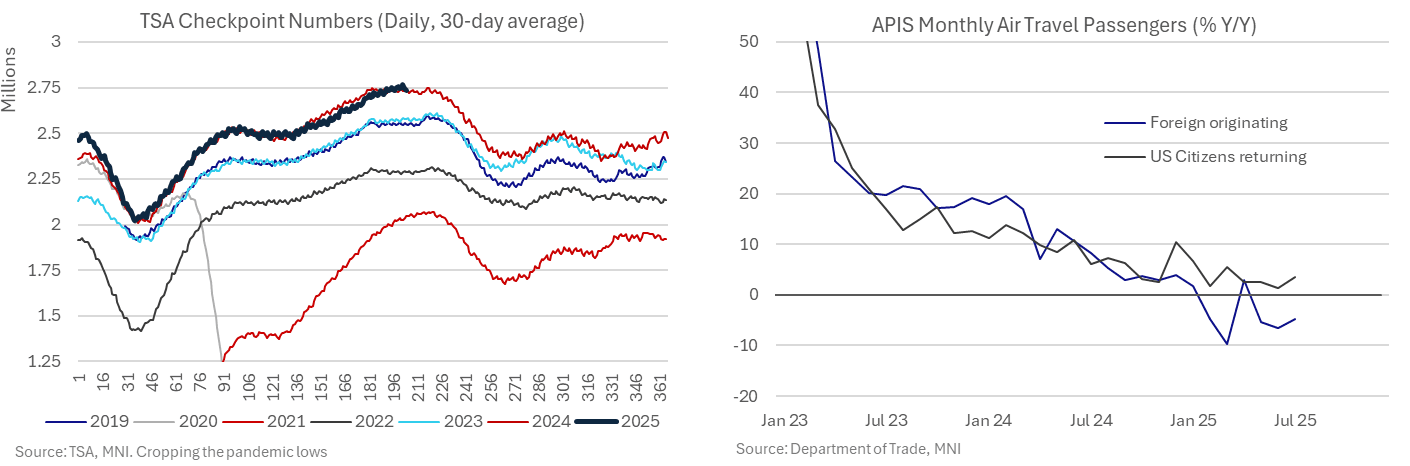

US OUTLOOK/OPINION: Travel CPI Categories Perhaps Less Sequentially Soft In July

Aug-11 19:01

[The below is a small section on latest travel demand in the US from the MNI US CPI Preview ahead of Tuesday's CPI report for July]

- Travel-related prices have been a source of generally larger than expected disinflationary pressure in recent months, although some travel data crudely suggest we might have seen the peak for this sequentially.

- TSA checkpoint numbers have returned closer to last year’s seasonal pattern after some weakness in prior months.

- APIS data meanwhile have stabilized at low Y/Y rates with US citizens returning rising 3.6% Y/Y in July (after 1.4% Y/Y in June or 3% Y/Y averaged since February) and foreign originating flights -4.9% Y/Y (after -6.6% Y/Y in June or -5% Y/Y since February).

EURJPY TECHS: Trend Structure Remains Bullish

Aug-11 19:00

- RES 4: 177.08 2.000 proj of the Feb 28 - Mar 18 - Apr 7 price swing

- RES 3: 175.43 High Jul 11 ‘24 and a key medium-term resistance

- RES 2: 174.86 1.764 proj of the Feb 28 - Mar 18 - Apr 7 price swing

- RES 1: 173.97 High Jul 28 and the bull trigger

- PRICE: 171.70 @ 15:31 BST Aug 11

- SUP 1: 169.73/45 Low Jul 31 / 23.6% of the Feb 28 - Jul 28 bull leg

- SUP 2: 169.62 50-day EMA

- SUP 3: 168.46 Low Jul 1

- SUP 4: 167.46 Low Jun 23

A bullish trend condition in EURJPY remains intact and for now the recent move down is considered corrective. Key support to watch lies at the 50-day EMA at 169.62. A clear break of the EMA is required to highlight a stronger short-term bearish threat. Moving average studies remain in a bull-mode position highlighting an uptrend. A break of the Jul 28 high of 173.97, would resume the bull cycle.

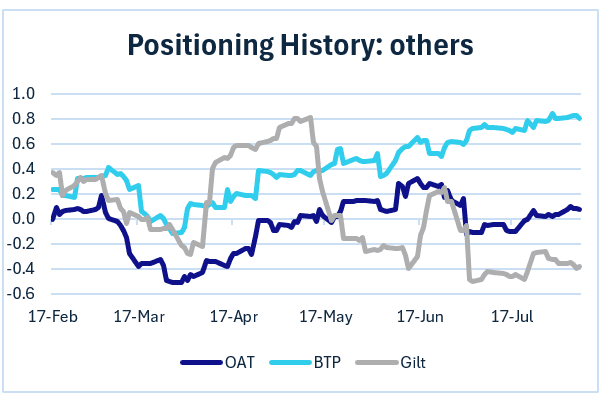

BONDS: Europe Pi: BTPs Stay Long, Gilts Short, OATs Flat (2/2)

Aug-11 18:50

Elsewhere in Europe Pi:

- OAT remains in flat territory, where it has been almost the entire year. Last week's trade was indicative of reduced longs.

- Gilt structural positioning remains in short territory. There were some longs set last week, however.

- BTP continues to edge further into "very long" territory. Indeed, trade indicative of further long-setting was seen in the most recent week.