MNI ASIA MARKETS ANALYSIS: Soft Data Weighs on Tsy Yields

HIGHLIGHTS

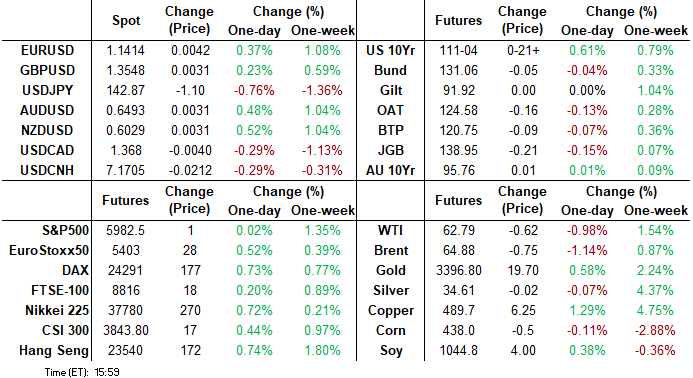

- Treasuries look to finish near midday highs Wednesday, projected rate cuts through year end back above 50bp again after this morning's soft ADP private payroll and ISM Services data.

- Off session lows, the Greenback nevertheless reversed the prior session gains after data set a negative tone for the US dollar on Wednesday.

- A moderately hawkish lean to the BOC decision is providing an additional tailwind for the Canadian dollar, with communications keeping the door open to a cut but not emphatically.

- The June 4 Beige Book reported that "economic activity has declined slightly since the previous report" while suggesting rising tariff-related inflationary pressures.

US TSYS

MNI US TSYS: Holding Near Highs After Soft ADP, ISM Services Data

- Treasuries look to finish near midday highs Wednesday, projected rate cuts through year end back above 50bp again after this morning's soft ADP private payroll and ISM Services data.

- The Sep'25 10Y contract trades +22 at 111-04.5 vs. 111-07 high, testing resistance at 111-05.5 (High May 9)

- The ISM services report for May showed a painful combination of another increase in prices paid (highest since late 2022) and new orders slumping (lowest since late 2022); the overall index hit its lowest (and first sub-50 reading) since Jun 2024.

- ADP employment increased just 37k (sa, cons 114k) in May after a marginally downward revised 60k (initial 62k) in April. Consensus currently stands at 120k for Friday's private payrolls release.

- Later in the session, the June 4 Beige Book reported that "economic activity has declined slightly since the previous report" while suggesting rising tariff-related inflationary pressures.

- Off session lows, the Greenback nevertheless reversed the prior session gains after data set a negative tone for the US dollar on Wednesday. USDJPY sits 0.85% lower on the session, having had a punchy 165 pip turnaround from the overnight highs.

- Focus turns to Thursday's weekly jobless claims, trade balance and unit labor costs.

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.32% (-0.03), volume: $2.711T

- Broad General Collateral Rate (BGCR): 4.30% (-0.02), volume: $1.082T

- Tri-Party General Collateral Rate (TCR): 4.30% (-0.02), volume: $1.045T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $120B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $297B

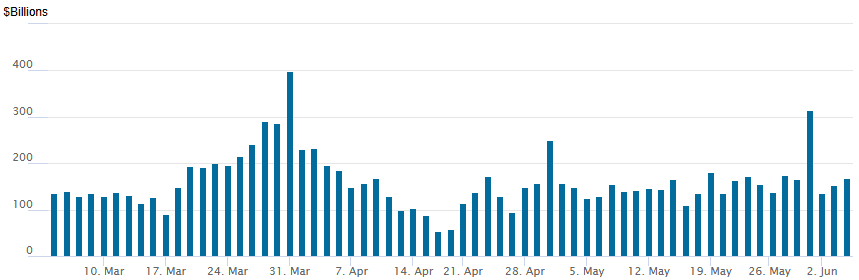

FED Reverse Repo Operation

RRP usage rises to $168.882B this afternoon from $153.177B yesterday, total number of counterparties at 45. Usage had fallen to $54.772B on Wednesday, April 16 -- lowest level since April 2021. Conversely, usage had surged to the highest level since December 31, 2024 on Monday, March 31: $399.167B.

US SOFR/TREASURY OPTION SUMMARY

Option desks reported decent SOFR & Treasury option volumes Wednesday, flow bias shifted from buying puts in the first half to selling puts/unwinding positions as underlying futures remained strong. Projected rate cut pricing continues to gain vs. morning levels (*) as follows: Jun'25 at -1.1bp (-0.7bp), Jul'25 at -7.8bp (-7.4bp), Sep'25 at -24.2bp (-22.7bp), Oct'25 at -39.3bp (-35.9bp), Dec'25 at -56.3bp (-52.4bp).

SOFR Options:

-30,000 SFRZ5 95.56/96.12 put spds, 18.75 vs. 96.19/0.40%

+4,000 SFRZ5 95.62/95.68/95.81 put trees, 1.0

+4,000 0QM5 96.62/96.87 call spds .75 over 3QM5 96.50/96.75 call spds

+15,000 0QZ5 95.00 puts, 1.5 ref 96.77

+3,000 SFRH8 97.50/98.50 call spds w/ 98.00/99.00 call spd strip, 33.5

+5,000 SFRZ5 95.56/95.68/95.81 put fly w/ 96.00/96.12/96.25 call fly strip 3.5

-4,000 SFRU5 95.75/95.81/96.00 put flys 2.5 over 95.68/95.81 put spds

Block, 2,000 0QN5 96.1/96.37 5x4 put spds, 8.0 net

+5,000 SFRM5 95.75/95.81 call spds, 0.37

-20,000 SFRZ5 96.00/96.25/96.50 put trees, 2.0 vs. 96.175/0.22% (-20k Tue)

+5,000 SFRN5 95.75/95.81 2x1 put spds, 0.75

+2,000 SFRZ5 97.12 calls, 6.5

+3,500 SFRQ5 95.62/95.75 put spds, 2.5 ref 95.92

+3,000 SFRZ5 96.25/96.75 1x2 call spds 1.25

4,200 SFRH6 95.37 puts ref 96.345 to -.40

3,000 0QZ5 96.00/96.25/96.50 put trees

4,000 0QM5 96.18/96.31/96.43 put trees ref 96.51

-3,500 SFRZ5 95.62/96.12 put spds, 20.0 vs. 96.155/0.40%

+1,000 SFRZ5 95.62/95.75 2x1 put spds, 0.0

4,000 SFRM5 95.81 calls, 0.5

1,000 0QU5 95.75/96.00/96.12/96.37 put condors

Block, +5,000 SFRU5 96.00/96.12/96.18 broken call flys, 1.87/splits

-1,000 0QV5 96.12/96.37 2x1 put spds, 0.5 ref 96.695

2,000 SFRZ5 95.62/95.75 put spds ref 96.16

Treasury Options:

2,000 FVU5 107/108.25 put spds 25.5 ref 108-13.25

9,000 TYN5 111/112 call spds 27 ref 111-05

over 13,400 FVN5 108.25 puts 24.5 ref 108-10.75

3,000 TYN5 107.5/109/110 1x3x1 broken put flys ref 111-01

1,200 USN5/USQ5 120 call spds 18 ref 113-08

+30,000 TYN5 108 puts, 2

+10,000 FVN5 109.5 calls, 4.5

over 4,000 TYQ5 107.5/109 put spds, 14 ref 111-01

2,200 FVU5 107 puts, 23 ref 108-09.5

Block, 10,000 FVN5 109.5 calls, 4.5 ref 108-05

2,000 FVN5 106.75 puts ref 107-30.75

over 12,700 TYN5 111 calls, 30-35

+2,000 Wed wk 10Y 110/110.25/110.5 put trees, 5 vs 110-18.5/0.08%

+2,900 USN5 107/109/111 put flys, 20 ref 112-04 to -05

+2,000 FVQ5 105.75 puts, 6

+3,000 Wed wk 10Y 110 puts, 1 vs 110-14 to -14.5/0.08%

MNI BONDS: EGBs-GILTS CASH CLOSE: German Curve Twist Flattens Pre-ECB

European curves flattened Wednesday, with Gilts outperforming Bunds.

- Bunds softened early, with Eurozone services PMI revised up, the German cabinet approving corporate tax cuts, and equities gaining ground. EGB weakness spilled over into Gilts.

- Afternoon moves in Gilts in particular tracked US Treasuries, which were buoyed by soft ADP private payroll and ISM Services data.

- For the session, the German curve twist flattened, with the UK's bull flattening.

- Periphery/semi-core EGB spreads were little changed; BTPs modestly outperformed.

- The ECB meeting, with an expected 25bp cut, is Thursday's focus - MNI's preview is here.

- We also get BoE DMP survey, and appearances by Greene and Breeden.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 1.2bps at 1.798%, 5-Yr is up 1.6bps at 2.098%, 10-Yr is up 0.3bps at 2.528%, and 30-Yr is down 1.8bps at 2.999%.

- UK: The 2-Yr yield is down 2.3bps at 4.005%, 5-Yr is down 2.8bps at 4.115%, 10-Yr is down 3.2bps at 4.606%, and 30-Yr is down 4.5bps at 5.322%.

- Italian BTP spread down 0.6bps at 96.4bps / French OAT up 0.3bps at 67.3bps

MNI OPTIONS: Pre-ECB Unwinds, Ratio Spreads Wednesday

Wednesday's Europe rates/bond options flow included:

- ERM5 98.00c, sold at 2.5 in 4k.

- ERU5 98.12/98.00ps 1x2, sold the 1 at 2.75 in 5k (downside unwind).

- ERU5 98.375/98.50 1x2 call spread paper pays 0.375 synthetic on 10K.

- 0RM5 98.25p, bought for 3.7 in 5k.

MNI FOREX: Greenback Sold on Weak US Data, Safe Havens Outperform

- Weaker-than-expected ADP employment data in the US set a negative tone for the US dollar on Wednesday, sentiment that was exacerbated by a soft ISM services print. With an associated move lower for US yields, notorious safe havens such as JPY and CHF are outperforming on Tuesday.

- USDJPY sits 0.85% lower on the session, having had a punchy 165 pip turnaround from the overnight highs. A bear cycle for the pair remains in play and sights remain on the next important support at 142.12, the May 27 low. Clearance of this level would confirm a resumption of the bear leg and open 139.89, the Apr 22 low. In similar vein, USDCHF (-0.76%) has gravitated back below the 0.82 handle, although spot remains just shy of the week’s lows at 0.8157.

- A moderately hawkish lean to the BOC decision is providing an additional tailwind for the Canadian dollar, with communications keeping the door open to a cut but not emphatically (Macklem's opening statement: "We also discussed the path ahead for the policy interest rate. Here, there was more diversity of views.”)

- USDCAD reaches fresh cycle lows below 1.3675, keeping bearish technical conditions firmly intact for the pair. Sights are on 1.3643 next, the Oct 9 low/Sep high. Below here, attention will be on 1.3579, the 1.5 Fibonacci projection of the Feb 3 - 14 - Mar 4 price swing, before the September lows at 1.3420 will garner attention.

- EURUSD regained the 1.14 handle amid the broad dollar weakness, but remains below the week’s best levels ahead of the ECB meeting on Thursday, where a 25bp rate cut is widely expected and forecast revisions will be of particular interest. Attention will then swiftly turn to Friday’s release of US employment data.

MNI FX OPTIONS: Expiries for Jun05 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1050(E5.9bln), $1.1300(E2.3bln), $1.1325-30(E1.0bln), $1.1375-85(E1.7bln), $1.1400(E2.4bln), $1.1415-25(E1.7bln), $1.1500(E1.5bln)

- USD/JPY: Y142.00($1.2bln), Y143.00-05($1.1bln), Y145.00-20($1.6bln)

- EUR/JPY: Y162.00(E571mln), Y167.00(E540mln)

- EUR/GBP: Gbp0.8345-60(E612mln)

- AUD/USD: $0.6490-95(A$1.8bln)

- NZD/USD: $0.5990-15(N$755mln)

- USD/CAD: C$1.3600($560mln)

MNI US STOCKS: Late Equities Roundup: Dow Slips Lower in Late Trade, Chip Stocks Up

- Stocks are holding mostly in late Wednesday trade, the Dow scaling back support while the Nasdaq extends modest session high on the back of strong gains in semiconductor makers.

- Currently, the DJIA trades down 10.24 points (-0.02%) at 42511.14, S&P E-Minis up 8.25 points (0.14%) at 5990.5, Nasdaq up 82.4 points (0.4%) at 19482.1.

- Tech stocks continued to outperform in the second half with ON Semiconductor +7.23%, NXP Semiconductors +5.74%, Lennar +3.21% and Seagate Technology +2.99%.

- Communication Services shares held earlier gains with Meta Platforms +2.92%, Live Nation Entertainment +2.66%, Netflix +1.85% and Match Group +1.56%.

- Conversely, Energy and Utility sectors continued to underperform as crude prices turned lower (WTI -0.43 to 62.98) after earlier headlines announced that "Saudi Arabia wants OPEC+ to continue with accelerated oil supply hikes," Bbg reported.

- Energy sector laggers included VValero Energy -3.08%, Phillips 66 -2.66%, Marathon Petroleum -2.62% and Schlumberger -2.48%. Meanwhile, Constellation Energy -3.30%, NRG Energy -1.76% and Vistra -1.51%.

MNI EQUITY TECHS: E-MINI S&P: (M5) Bulls Remain In The Driver's Seat

- RES 4: 6124.00 High Feb 24

- RES 3: 6080.75 High Feb 26

- RES 2: 6057.00 High Mar 3

- RES 1: 6008.00 High May 29

- PRICE: 5985.75 @ 14:19 BST Jun 4

- SUP 1: 5850.75/5765.62 20- and 50-day EMA values

- SUP 2: 5596.00 Low May 7

- SUP 3: 5455.50 Low Apr 30

- SUP 4: 5355.25 Low Apr 24

The trend condition in S&P E-Minis is unchanged, it remains bullish and the contract is trading just ahead of its recent high. A print above 5993.50 last week, the May 20 high and a bull trigger, highlights a resumption of the uptrend and maintains a price sequence of higher highs and higher lows. An extension would open 6057.00 next, the Mar 3 high. Key support lies at 5765.62, the 50-day EMA.

MNI COMMODITIES: Crude Falls On Possible Supply Hikes, Gold Rises

- Oil has come under fresh pressure as Bloomberg sources reported that Saudi Arabia is pushing for higher oil output in the months ahead to regain market share.

- Under OPEC+, Saudi Arabia is looking to add ‘at least’ 411kbd in August and potentially September, the report says. OPEC+ has already agreed to boost production by 411kbd in May, June and July.

- WTI Jul 25 is down by 0.9% at $62.9/bbl.

- For WTI futures, a bear threat remains present and the recovery since Apr 9 still appears corrective. However, key resistance at $62.52, the 50-day EMA, has been pierced and a clear break would highlight a stronger reversal and open $65.82, the Apr 4 high.

- Meanwhile, spot gold has risen by 0.8% today to $3,380/oz, buoyed by a weaker dollar following soft US ADP employment and ISM services data.

- ADP’s chief economist said that "after a strong start to the year, hiring is losing momentum." Focus ahead now shifts to Friday’s key NFP data.

- A bullish theme in gold remains intact, with sights on $3,435.6, the May 7 high.

- Elsewhere, copper has also risen by 1.6% to $491/lb amid supply issues at major mines in Chile and the DRC and declining inventories on the LME.

- Despite recent gains in copper, a bearish threat remains present. Key near-term resistance to watch is $498.25, the Apr 23 high, a break of which is required to reinstate a bullish theme.

THURSDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 05/06/2025 | 0545/0745 | ** | Unemployment | |

| 05/06/2025 | 0600/0800 | ** | Manufacturing Orders | |

| 05/06/2025 | 0600/0800 | *** | Flash Inflation Report | |

| 05/06/2025 | 0730/0930 | ** | S&P Global Final Eurozone Construction PMI | |

| 05/06/2025 | 0745/0845 | BOE's Greene Opening Remarks at Econdat Conference 2025 | ||

| 05/06/2025 | 0800/1000 | * | Retail Sales | |

| 05/06/2025 | 0830/0930 | Decision Maker Panel data | ||

| 05/06/2025 | 0830/0930 | ** | S&P Global/CIPS Construction PMI | |

| 05/06/2025 | 0900/1100 | ** | PPI | |

| 05/06/2025 | 1215/1415 | *** | ECB Deposit Rate | |

| 05/06/2025 | 1215/1415 | *** | ECB Main Refi Rate | |

| 05/06/2025 | 1215/1415 | *** | ECB Marginal Lending Rate | |

| 05/06/2025 | 1230/0830 | *** | Jobless Claims | |

| 05/06/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 05/06/2025 | 1230/0830 | ** | International Merchandise Trade (Trade Balance) | |

| 05/06/2025 | 1230/0830 | ** | Trade Balance | |

| 05/06/2025 | 1230/0830 | ** | Non-Farm Productivity (f) | |

| 05/06/2025 | 1230/0830 | ** | Trade Balance | |

| 05/06/2025 | 1245/1445 | ECB Press Conference | ||

| 05/06/2025 | 1400/1000 | * | Ivey PMI | |

| 05/06/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 05/06/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 05/06/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 05/06/2025 | 1600/1200 | Fed Governor Adriana Kugler | ||

| 05/06/2025 | 1620/1220 | BOC Deputy Kozicki speech | ||

| 06/06/2025 | 2330/0830 | ** | Household spending |