MNI ASIA MARKETS ANALYSIS: Shutdown - Beginning of the End?

HIGHLIGHTS

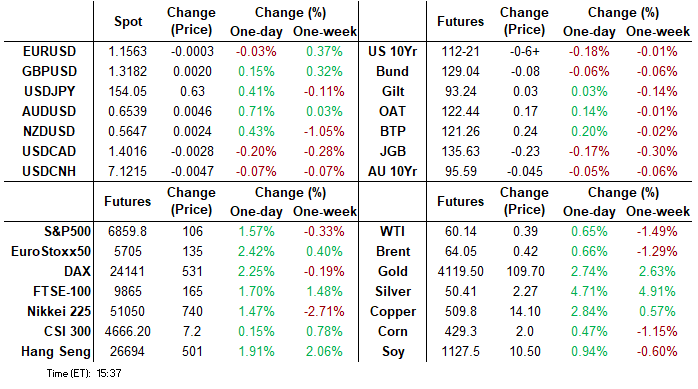

- Treasuries look to finish weaker Monday amid general optimism over re-opening the US Govt after 41 days of closure.

- Reactions across G10 do not surprise, with the boost to risk assets filtering through to the underperforming JPY, while supporting the likes of AUD, NZD and NOK.

- US Govt shutdown ending without an extension of Affordable Care Act (ACA) subsidies - weighed heavily on health care sector shares.

US TSYS

MNI US TSYS: Nearer The End of US Govt Shutdown

- Treasuries look to finish weaker, near the middle of Monday's range - optimism buoyed as the US Govt shutdown appears to be nearer an end after eight Democrats broke formation with colleagues to reopen the Govt.

- Stocks rallied, led by chip makers while Health Care sector shares continued to decline in the second half - if the US Govt shutdown ends without an extension of Affordable Care Act (ACA) subsidies.

- Reactions across G10 do not surprise, with the boost to risk assets filtering through to the underperforming JPY, while supporting the likes of AUD, NZD and NOK.

- Treasury futures pare losses slightly (TUZ5 104-04.88, -1.88) after $58B 3Y note auction (91282CPK1) stops through: drawing 3.579% high yield vs. 3.589% WI; 2.85x bid-to-cover vs. 2.66x prior.

- No economic data Monday, Tuesday limited to NFIB Small Business Optimism at 0600ET. Markets open for Veterans Day "holiday" - may weigh on volumes Tuesday.

REFERENCE RATES

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 3.93% (+0.01), volume: $3.069T

- Broad General Collateral Rate (BGCR): 3.89% (+0.00), volume: $1.216T

- Tri-Party General Collateral Rate (TCR): 3.89% (+0.00), volume: $1.192T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 3.87% (+0.00), volume: $83B

- Daily Overnight Bank Funding Rate: 3.87% (+0.00), volume: $162B

FED Reverse Repo Operation

RRP usage rises to $7.152B with 11 counterparties this afternoon from $4.903B Friday. Compares to $2.435B on October 24 (lowest level since mid-March 2021) and the year's highest usage of $460.731B on June 30.

US SOFR/TREASURY OPTION SUMMARY

Treasury options leaning toward low delta calls - large Jan'26 buyer resumes, SOFR option volumes remained rather modest. Underlying futures weaker, near middle session range - bit of risk as hopes of ending US Gov shutdown rise after eight Democrats voted with Rep's on CR to fund gov through end of January. Projected rate cut pricing retreats vs morning levels (*): Dec'25 at -15.5bp (-16.3bp), Jan'26 at -25.1bp (-26.1bp), Mar'26 at -35.2bp (-35.8bp), Apr'26 at -41.3bp (-41.6bp).

SOFR Options:

+10,000 0QZ5 96.50/96.62 put spds, 1.5 vs. 96.865 to -.87/0.10%

3,000 0QX5 96.87 puts, 4.5 vs. 96.87/0.52%

4,000 SFRZ5 96.37 calls, cab

over 4,000 SFRZ5 96.18 puts, 0.5 last

1,000 SFRZ5 96.06/96.12/96.18 put flys ref 96.24

Treasury Options:

-8,000 TYZ5 111.5/114 strangles, 44

2,200 USZ5 115/119 strangles, 18 ref 116-31

1,500 USF6 115/116/117 put flys

+25,000 TYF6 111.5 puts, 22

over 52,000 TYF6 113 calls, 42-45, ref 112-23 to -22.5

1,300 TUZ5 104.5/104.87 put spds ref 104-05.38

1,100 FVZ5 110.75/FVF6 110.5 call spds

+10,000 TYF5 113.5 calls, 31 (adds to +50k at 27 earlier)

over 25,500 TY/wk2 TY 112.5 put spds, 11 (TYZ over)

5,000 TYZ5 111/111.5/112.5 2x3x1 broken call flys ref 112-21

+50,000 TYF6 113.5 calls, 27 (last Thursday: +100,000 TYF6 113.5 calls, 30-32 vs. 112-18/0.32%)

over +/-15,400 TYZ5 113 calls, 16-17 ref 112-19

over 10,400 TYZ5 112.25 puts

3,000 TYZ5 113.5/114 call spds ref 112-19 to -18

1,200 TYZ5 110.75/111.75 put spds ref 112-18.5

2,300 TYF6 111/112 put spds ref 112-15.5

-1,500 TYG6 113.5 calls, 39 vs. 112-15/0.35%

+3,000 wk4 TY 113.5 calls, 11

+1,000 TYH6 112.5 straddles, 226

-4,000 wk2 TY 113.25 calls, 3

+2,000 USF6 130 calls, 1

1,000 FVZ5 108.25/108.5/108.75 put flys ref 109-07

+1,000 FVZ5 109.25 straddles, 34.5

+3,000 Thu wkly FV 109 puts, 1.5

3,400 TYZ5 114.5 calls, 3 ref 112-19.5

MNI BONDS: EGBs-GILTS CASH CLOSE: Core Curves Twist Flatten Ahead Of UK Labour Data

European curves flattened Monday.

- An apparent breakthrough in the US federal government shutdown over the weekend saw core instruments on the back foot early.

- But the rise in yields at the open would mark the highs for the day in Bunds and Gilts, with a fairly steady descent throughout the rest of the session.

- This was mainly following the trajectory of Treasuries paring losses as opposed to European macro/headline cues, though Bunds and Gilts would outperform their US counterparts on the day.

- UK Chancellor Reeves made the clearest indications yet that the government would break manifesto pledges not to raise income/NIC/VAT taxes.

- Periphery/semi-core EGBs outperformed alongside a risk-on rally in equities, with BTPs and OATs spreads tightening most.

- The German and UK curves both twist flattened, with Bunds slightly underperforming Gilts.

- The highlight of the week's calendar is UK labour market data out Tuesday - MNI's preview is here. The main focus is on private regular earnings, and we see risks to consensus expectations as tilted slightly to the upside.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 1.5bps at 2.005%, 5-Yr is up 1.2bps at 2.268%, 10-Yr is up 0.2bps at 2.668%, and 30-Yr is down 0.6bps at 3.26%.

- UK: The 2-Yr yield is up 0.9bps at 3.807%, 5-Yr is up 0.7bps at 3.935%, 10-Yr is down 0.5bps at 4.461%, and 30-Yr is down 1.1bps at 5.239%.

- Italian BTP spread down 2.3bps at 74.4bps / French OAT down 2.2bps at 77.5bps

MNI OPTIONS: Sonia Upside-Leaning Makes For Active Start To Week

Monday's Europe rates/bond options flow included:

- ERM6 98.75/98.875 call spread paper paid 0.25 on +5K

- SFIZ5 96.20/96.10 put spread vs. 0NZ5 96.50/96.40 put spread, paper paid 0.25 on 4.5K (+SFIZ5, -0NZ5)

- SFIH6 96.60/96.65/96.70 call fly paper paid 0.5 on 3K

- SFIH6 96.25/35/65/75 call condor paper paid 5.75 on 5K

- SFIH6 96.45/96.75 call spread vs. 96.30 puts paper paid 1.5 on 3.3

- SFIJ6 96.70/80 call spread vs. 96.25/15 put spread paper paid 1.5 on 7.5K for the call spread

- 0NZ5 96.70/96.90 call spread (vs 62+) 22K given at 3.75

MNI FOREX: Equity Sentiment Key to AUD Outperformance, JPY Under Pressure

- Renewed optimism surrounding the US government reopening have significantly boosted risk sentiment, prompting the US Dollar to consolidate last week's losses. Reactions across G10 do not surprise, with the boost to risk assets filtering through to the underperforming JPY, while supporting the likes of AUD, NZD and NOK.

- USDJPY rose sharply from the open and extended gains to a 154.25 high on Monday. The pair has once again met some resistance above the 154.00 handle, registering a seventh daily high between 154.14-154.48, bolstering the short-term significance of this resistance cluster. First important support to watch lies at 152.68, the 20-day EMA.

- AUD received further tailwinds from RBA Hauser comments being on the hawkish side. For AUDUSD (+0.70%), a break above key resistance at 0.6618 (Oct 29 high) would be required to reinstate a bullish theme.

- NOK meanwhile also benefits from an upside surprise to domestic October CPI. A December cut was already unlikely following last week's Norges Bank meeting and the prospects of that are likely to fall back even further. EURNOK has extended the pullback from 11.80, potentially forming a double top pattern multi-week.

- ZAR (+1%) outperforms in the emerging market space, very much a product of the precious metals rally (gold +2.5%, silver +4%), which adds further support to the positive risk backdrop, boosting higher beta currencies. Latin American currencies have followed suit, with all regional currencies rising Monday.

- Key to watch in the days ahead will be further developments on the shutdown, with a handful of legislative hurdles still to be met. UK labour market data takes focus Tuesday, while NZ inflation expectations and German ZEW also cross.

MNI OPTIONS: Expiries for Nov11 NY cut 1000ET (Source DTCC)

- AUD/USD: $0.6450(A$644mln)

Larger FX Option Pipeline - EUR/USD: Nov12 $1.1500-05(E1.1bln), $1.1688-90(E1.3bln); Nov13 $1.1590(E1.5bln)

- USD/JPY: Nov13 Y147.00($1.6bln), Y152.96-00($1.1bln), Y155.00($1.1bln)

- GBP/USD: Nov12 $1.3100(Gbp1.9bln), $1.3225-30(Gbp1.3bln)

- AUD/USD: Nov12 $0.6500(A$1.2bln), $0.6530-50(A$1.2bln); Nov14 $0.6750(A$2.2bln)

- USD/CAD: Nov14 C$1.4025-35($1.2bln)

MNI US STOCKS: Late Equities Roundup: Chip Stocks Leading Rally

- After a brief retreat this morning - stocks are extending session highs late Monday as semiconductor makers rebounded from better selling last week. Currently, the DJIA trades up 340.21 points (0.72%) at 47327.16, S&P E-Minis up 97.5 points (1.44%) at 6851.25, Nasdaq up 513.6 points (2.2%) at 23518.31.

- Last week's IT valuations in the rear view as focus turned to optimism over the US Gov shutdown ending soon. Leading tech sector shares include: Palantir Technologies +9.00%, Western Digital +6.50%, Micron Technology +6.02%, NVIDIA +5.02%, Advanced Micro Devices +4.97% and Akamai Technologies +4.45%.

- Communication Services and Consumer Discretionary sector shares followed:

- Alphabet +4.12%, Meta Platforms +1.86%, Match Group +1.43%, Walt Disney +1.43% and Netflix +1.23%.

- Tesla Inc +3.82%, Wynn Resorts +3.67%, Expedia Group +3.59%, Ralph Lauren +3.54% and Lululemon Athletica +2.76%.

- Conversely, Health Care sector shares continued to lead declines in the second half - if the US Govt shutdown ends without an extension of Affordable Care Act (ACA) subsidies: Centene -8.20%, Molina Healthcare -7.23%, Humana -4.58%, HCA Healthcare -4.57% and Elevance Health -4.30%.

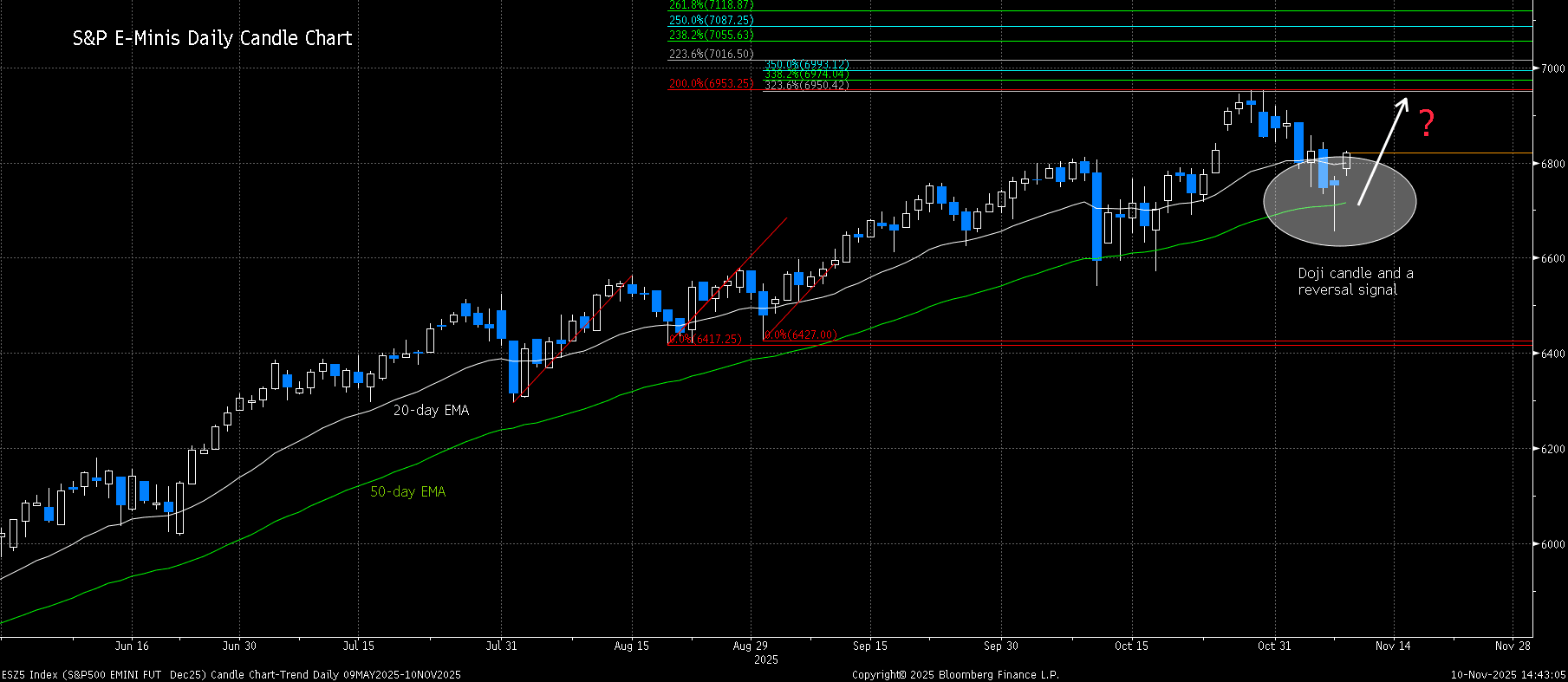

MNI EQUITY TECHS: E-MINI S&P: (Z5) Doji Reversal Candle

- RES 4: 7000.00 Psychological round number

- RES 3: 6993.12 3.500 proj of the Aug 20 - 28 - Sep 2 price swing

- RES 2: 6974.04 3.382 proj of the Aug 20 - 28 - Sep 2 price swing

- RES 1: 6857.75/6953.75 High Nov 5 / High Oct 30 and the bull trigger

- PRICE: 6822.25 @ 14:33 GMT Nov 10

- SUP 1: 6655.70 Low Nov 7 and key short-term support

- SUP 2: 6571.25 Low Oct 17

- SUP 3: 6540.25 Low Oct 10 and a key support

- SUP 4: 6476.62 23.6% retracement of the Apr 7 - Oct 30 bull cycle

The trend condition in S&P E-Minis remains bullish and the pullback since the Oct 30 high appears corrective. The contract has managed to find support below the 50-day EMA, currently at 6710.28 and a key support. Friday’s activity also highlights a potential reversal signal - a bullish doji candle. This defines key support at 6655.50, the Oct 7 low. A continuation higher would signal the end of a correction and open 6953.75, Oct 30 high and bull trigger.

COMMODITIES

MNI AMERICAS OIL: US OIL: November 10 - Americas End of Day Oil Summary: Crude Higher

WTI crude is slightly higher overall in a choppy, sideways session as markets weigh signs of an end to the US government shutdown against ongoing oversupply concerns. Both houses of Congress still need to agree to the continuing resolution. Price has recently traded through the 50-day EMA, at $60.87, signaling scope for a stronger recovery.

- Enough Democrats in the Senate look set to vote to pass a bill to end the government shutdown which is in its sixth week. The impasse was seen to be costly to the economy and would as a result weigh on energy demand.

- The market will monitor monthly reports closely this week for any deterioration in the excess supply situation. The IEA increased its 2026 surplus forecast in its October monthly report. It publishes updates on Nov. 13, while its annual outlook, EIA short-term energy outlook & OPEC report are out Nov. 12.

- US President Trump has given Hungary a one-year exemption from the US sanctions on Russia’s Rosneft and Lukoil, as “it’s very difficult for him [Hungarian PM Orban] to get the oil and gas from other areas”. According to Bloomberg, Hungary imports 90% of its oil from Russia.

- WTI Dec futures were up 0.6% at $60.13

- WTI Jan futures were up 0.6% at $60.03

TUESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 11/11/2025 | 0700/0700 | *** | Labour Market - AWE & Unemployment | |

| 11/11/2025 | 0700/0700 | *** | Labour Market - AWE & Unemployment | |

| 11/11/2025 | 0700/0700 | *** | Labour Market - Payrolls & Claimants | |

| 11/11/2025 | 0700/0700 | *** | Labour Market - Payrolls & Claimants | |

| 11/11/2025 | 0820/0920 | ECB Lagarde Video Message at Bank of Albania | ||

| 11/11/2025 | 0830/0930 | Riksbank Minutes | ||

| 11/11/2025 | 0830/0830 | BOE Greene in Panel at UBS European Conference | ||

| 11/11/2025 | 1000/1100 | *** | ZEW Current Expectations Index | |

| 11/11/2025 | 1100/0600 | ** | NFIB Small Business Optimism Index | |

| 11/11/2025 | 1200/0700 | ** | Brazil Final CPI | |

| 11/11/2025 | 1200/1200 | BOE APF Quarterly Report | ||

| 11/11/2025 | - | *** | Money Supply | |

| 11/11/2025 | - | *** | New Loans | |

| 11/11/2025 | - | *** | Social Financing | |

| 11/11/2025 | 1355/0855 | ** | Redbook Retail Sales Index | |

| 11/11/2025 | 0325/2225 | Fed Governor Michael Barr |