AMERICAS OIL: US OIL: November 10 - Americas End of Day Oil Summary: CrudeHigher

US OIL: November 10 - Americas End of Day Oil Summary: Crude Higher

WTI crude is slightly higher overall in a choppy, sideways session as markets weigh signs of an end to the US government shutdown against ongoing oversupply concerns. Both houses of Congress still need to agree to the continuing resolution. Price has recently traded through the 50-day EMA, at $60.87, signaling scope for a stronger recovery.

- Enough Democrats in the Senate look set to vote to pass a bill to end the government shutdown which is in its sixth week. The impasse was seen to be costly to the economy and would as a result weigh on energy demand.

- The market will monitor monthly reports closely this week for any deterioration in the excess supply situation. The IEA increased its 2026 surplus forecast in its October monthly report. It publishes updates on Nov. 13, while its annual outlook, EIA short-term energy outlook & OPEC report are out Nov. 12.

- US President Trump has given Hungary a one-year exemption from the US sanctions on Russia’s Rosneft and Lukoil, as “it’s very difficult for him [Hungarian PM Orban] to get the oil and gas from other areas”. According to Bloomberg, Hungary imports 90% of its oil from Russia.

- The US and China have suspended port fees on each other and paused investigations into the shipbuilding industry as trade tensions ease, Bloomberg said.

- Iraq cuts the December OSPs to Asia with Basrah Medium crude -$1.2/bbl on the month to a discount of $0.35/bbl.

- Lukoil has declared for majeure at Iraq’s West Qurna-2 oilfield, four sources told Reuters, after Western sanctions on Lukoil hampered its operations.

- The amount of crude held around the world on tankers that have been stationary for at least 7 days rose 11% w/w to 95.18m bbl as of Nov. 7, according to Vortexa data cited by Bloomberg.

- Global liquids demand is estimated to peak in the early 2030s at around 107mb/d, Rystad Energy said.

- Cracks ended firmer as the market watches for any further signs of refinery disruption. EIA inventory data will be delayed until Thursday due to Veterans Day.

- WTI Dec futures were up 0.6% at $60.13

- WTI Jan futures were up 0.6% at $60.03

- RBOB Dec futures were up 1.4% at $1.97

- ULSD Dec futures were up 1% at $2.51

- US gasoline crack up 0.7$/bbl at 22.52$/bbl

- US ULSD crack up 0.7$/bbl at 45.17/bbl

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US: Trump Oval Office Announcement Underway Shortly

US President Donald Trump is shortly due to deliver an announcement in the White House Oval Office. LIVESTREAM The announcement is expected to relate to drug pricing and could follow a similar template to a recent pledge from Pfizer.

- The announcement will be Trump's first press remarks since a market-moving Truth Social statement earlier today in which Trump suggested calling off a meeting with Chinese President Xi Jinping and raising tariffs on China in response to new export controls from Beijing on rare earths. See earlier bullets here and here.

RATINGS: Moody's Completes Periodic Review Of Belgium, No Rating Action

No ratings actions for Belgium from Moody's, which is quoted in a press release on Bloomberg: "Moody's Ratings (Moody's) has completed a periodic review of the ratings of Belgium and other ratings that are associated with this issuer. The review was conducted through a rating committee held on 2 October 2025 in which we reassessed the appropriateness of the ratings in the context of the relevant principal methodology(ies), and recent developments. This publication does not announce a credit rating action and is not an indication of whether or not a credit rating action is likely in the near future."

- There had been some speculation there could be a ratings action - MNI wrote Thursday: "* Moody's on Belgium (Current rating Aa3, Outlook Negative): We expect Moody's to maintain their current stance in the absence of 2026 budget details."

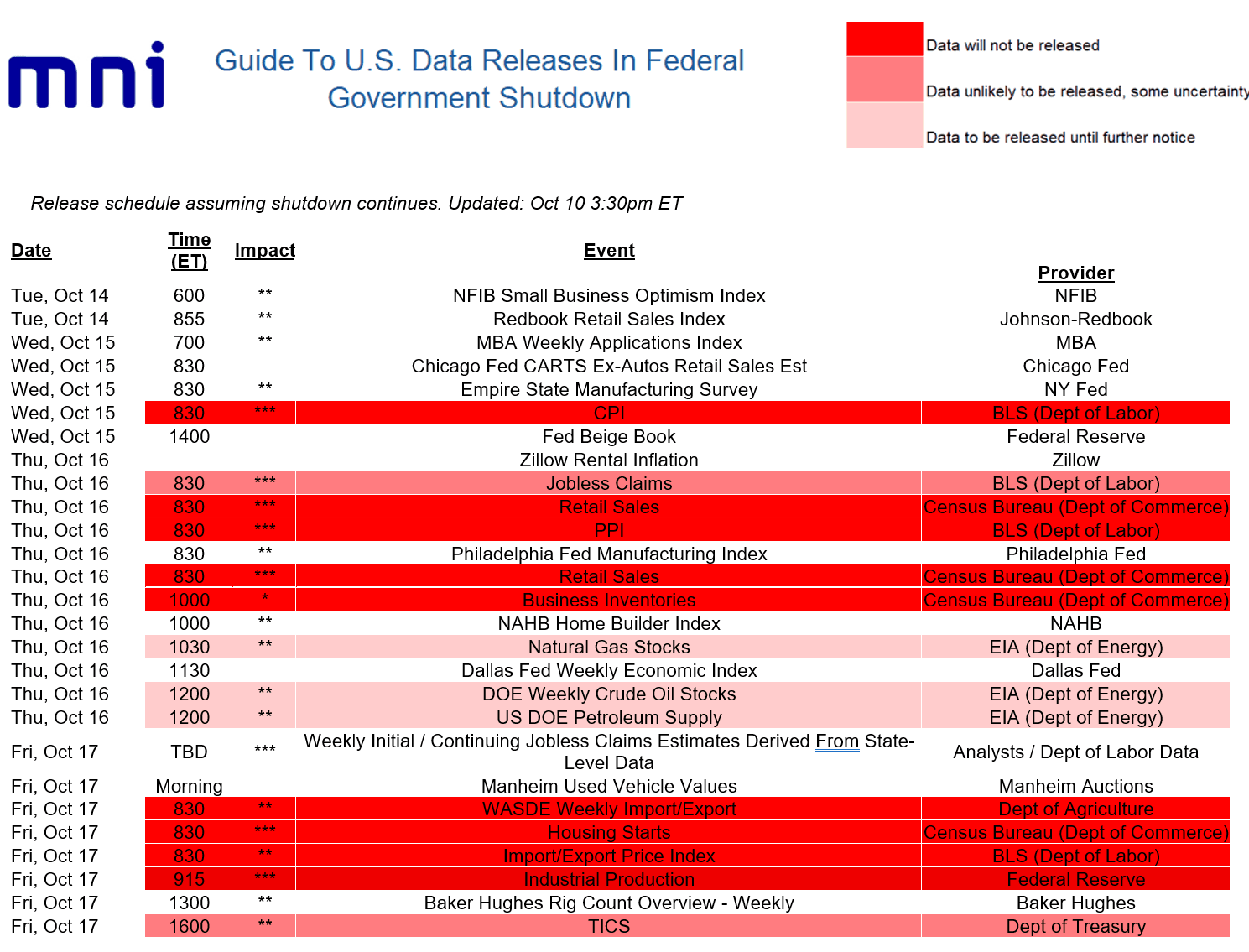

MACRO ANALYSIS: US Macro Week Ahead: No CPI, But Plenty Of Pre-Blackout FedSpeak

Below is the week’s data schedule, with MNI’s annotation of whether or not data will be postponed.

- As we went to press, the Fed announced that next week's Industrial Production data will be postponed (was due to be published next Friday Oct 17) as the data “incorporate a range of data from other government agencies, the publication of which has been delayed as a result of the federal government shutdown.”

- We won’t be getting September CPI as scheduled on Oct 15, but at least the BLS announced it will publish the data on Oct 24.

- As such next week we’ll be looking at some under-covered data points, including the Redbook weekly and Chicago Fed’s CARTS retail sales data (in lieu of the Census Bureau retail sales report), with a little more focus than usual on regional Fed manufacturing indices (NY, Philadelphia).

- Once again, the dearth of tier-one data leaves Fed commentary in focus ahead of the pre-FOMC blackout period: highlights for us are Philadelphia Fed President Paulson making her first comments on monetary policy on Monday since being appointed in the summer, while as always Chair Powell bears watching on Tuesday (we also hear from Bowman, Waller, Collins, Miran, Schmid, and Musalem).

- Additionally we get the latest Beige Book which was already key given the FOMC was already increasingly focused on anecdotal information as it attempts to navigate murky economic waters.