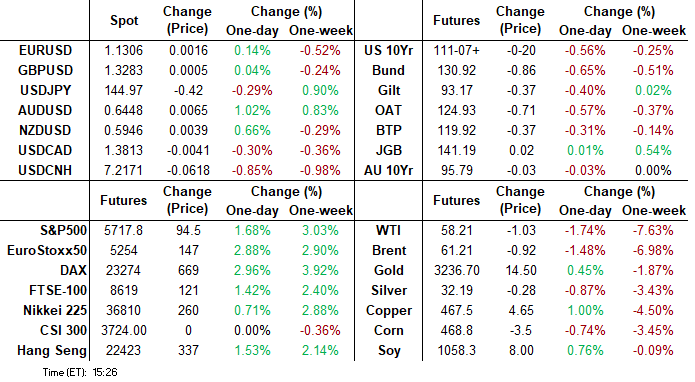

MNI ASIA MARKETS ANALYSIS: Sentiment Up on Trade Deal Hopes

HIGHLIGHTS

- Treasuries reversed early gains following this morning's higher than expected jobs gain of 177k (sa, cons 138k) of which private contributed 167k (sa, cons 125k).

- Stocks are extending late Friday session highs, trying to get ahead of further price gains in the event of any positive trade negotiation headlines.

- Projected rate cut pricing continues to recede even vs this morning's lows (*) as follows: May'25 at -0.8bp (-1.8bp), Jun'25 at -8.4bp (-15.5bp), Jul'25 at -25.7bp (-36.3bp), Sep'25 -45.6bp (-57.4bp).

- The US ISM services PMI will also garner attention Monday, where UK and Japan are both out for national holidays.

US TSYS

MNI US TSYS: Rates Retreat, Sentiment Improved Though Trade Risk Remains

- Treasuries look to finish near late Friday session lows after trading firmer on the open, higher than expected Nonfarm payrolls at 177k (sa, cons 138k) of which private contributed 167k (sa, cons 125k) triggered the early reversal.

- However, two-month revisions of -58k offset the 39k beat for nonfarm payrolls, with a similar story for private (a 42k surprise vs -48k two-month revision).

- Stocks are back near four week highs - pre-"Liberation Day" levels as hopes of some trade deal being made improved sentiment.

- The Wall Street Journal reports that "Beijing is considering ways to address the Trump administration’s gripes over China’s role in the fentanyl trade... potentially offering an off-ramp from hostilities to allow for trade talks to start." The Journal notes that "discussions remain fluid" and China "would like to see some softening of stance from President Trump".

- Currently, the Jun'25 10Y contract trades -20 at 111-07.5 vs 111-02 low -- initial technical support (50-dma) followed by 110-16.5/109-08 (Low Apr 22 / 11 and the bear trigger). Curves bear flattened, 2s10s -3.480 at 48.002, 5s30s -4.911 at 86.807.

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.39% (-0.02), volume: $2.789T

- Broad General Collateral Rate (BGCR): 4.35% (-0.02), volume: $1.084T

- Tri-Party General Collateral Rate (TCR): 4.35% (-0.02), volume: $1.044T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $107B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $247B

FED Reverse Repo Operation

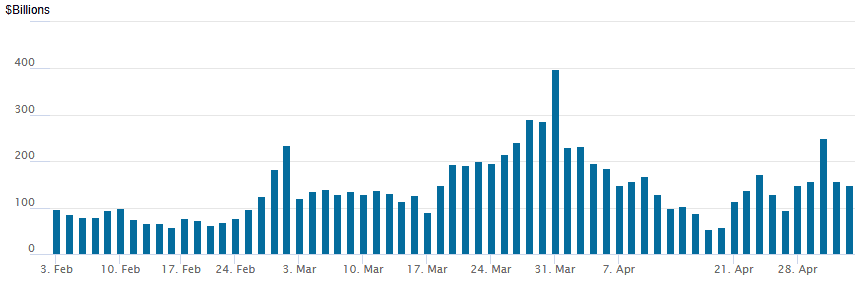

RRP usage slips to $147.882B this afternoon from $157.353B yesterday. Usage had fallen to $54.772B last Wednesday, April 16 -- lowest level since April 2021. Conversely, usage had surged to the highest level since December 31, 2024 on Monday, March 31: $399.167B. The number of counterparties at 35.

US SOFR/TREASURY OPTION SUMMARY

Option desks reported better SOFR call flow carried over from overnight, volumes robust through the Friday session, Treasury option volumes muted in comparison, also rotated around upside calls. Underlying futures broadly weaker, curves bear flattening with the short end underperforming (2s10s -3.538 at 47.944, 5s30s -5.497 at 86.221). Projected rate cut pricing continues to recede even vs this morning's lows (*) as follows: May'25 at -0.8bp (-1.8bp), Jun'25 at -8.4bp (-15.5bp), Jul'25 at -25.7bp (-36.3bp), Sep'25 -45.6bp (-57.4bp).

SOFR Options:

+100,000 0QU5/0QZ5 97.00/97.25 call spd spd, 1.0 net flattener (likely Sep unwind/roll to Dec, *see below)

-15,000 SFRN5/SFRU5 96.50 call spds 4.5

-25,000 SFRK5 95.50/95.75/95.87/96.00 put condors, 10.25

+20,000 SFRU5 98.00 calls, 2.0 ref 96.205

-25,000 SFRM5 96.00 calls, 4.5-4.0

+10,000 SFRM5 95.62/95.68 2x1 put spds, .25 ref 95.835

+35,000 SFRZ5 99.00 calls, 1.5 vs. 96.585/0.05%

+10,000 SFRZ5 96.75/97.25 call spds 11.75-12.25 ref 96.53

+10,000 SFRM5 96.25/96.37 call spds .62

Block, 6,000 SFRN5 96.50/0QN5 97.25 call spds, 2.5, midcurve over

3,000 SFRM5 95.62 puts ref 95.88

4,000 SFRU5 95.62/95.75/95.87 put flys

2,000 0QK5 97.00/97.25/97.50 call flys ref 96.915

3,000 SFRK5 96.12 calls ref 95.885

+1,000 SFRK5 95.81/95.93/96.06 call flys, 2.75

2,000 0QK5 96.93 straddles 28.5

+2,500 SFRU5 95.75 puts, 3.0 vs 96.285/0.10%

+1,000 SFRZ5 96.00/96.25/96.50 call flys, 3.5

2,500 SFRH6 97.50/97.75/98.00/98.25 call condors ref 96.765

+3,500 0QM5 97.25/97.75 call spds, 6.0 vs. 96.88/0.20%

2,125 0QN5 97.12/97.35 call spds ref 96.925

Treasury Options:

2,000 TYM5 112.5/113 1x2 call spds, 7 net/2-legs over

2,000 TYN5 110/TYM5 111 put spds 1 net

2,500 FVM5 108.75 calls, 27

1,250 TYM5 110.5/112.5 strangles, 41 ref 111-13.5

over 5,200 FVM5 109.75 calls, 14.5 ref 108-18

3,500 wk2 TY 112.75/113.5 1x2 call spds, 7 ref 111-11.5

1,500 TUM5 104.12 calls, 9.5 ref 103-27.25

9,600 Mon wkly FV 109.75 calls, 2 ref 108-27.5

5,000 wk2 TY 111 puts, 12

over 5,400 TYM5 113 calls, 28 last

+2,500 wk2 TY 110.25/110.5/111 broken put flys, 5.0 vs. 111-26/0.08%

4,000 wk2 FV 108 puts, 4.5

+2,000 TUM5 102.87 puts, 1

*Some context for the recently posted buy of 100,000 0QU5/0QZ5 97.00/97.25 call spd spd, 1.0 net debit for the bull curve flattener. The 400,000 option package is actually just rolling a long Sep'25 midcurve SOFR call spread to the Dec'25 midcurve spread -- as paper had bought the following 100,000+ spread on April 24: 0QM5 96.81/97.00 call spds vs. 0QU5 97.00/97.25 call spds, 1.0-1.25 net flattener (Sep over). The short Jun'25 midcurve call spread leg on April 24 was and unwind of some 95,000 0QM5 96.81/97.00 call spreads bought from 5.0 to 6.0 between April 2 and April 10.

MNI BONDS: EGBs-GILTS CASH CLOSE: Week Ends With Risk-On Yield Rise

Bund and Gilt yields rose to finish the week, with periphery/semi-core EGB spreads tightening in a largely risk-on session.

- EGBs opened weaker, catching up in the return to cash trade from Thursday's holiday. Gilts were on the front foot early however, with no particular catalyst (there was some political intrigue with the Reform UK party's strong local and byelection performance but this wasn't seen as a market-mover).

- Bunds saw relatively muted reaction to stronger-than-expected Eurozone flash April core HICP print and upward revisions to April manufacturing PMIs.

- The main driver in the session was the US April Employment Report which was more solid than had been anticipated, driving Treasury yields higher and dragging Bunds and Gilts in the same direction. With a risk-on tone pervading as equities gained, core yields closed on the highs.

- The German curve bear steepened, with the UK's leaning bear flatter through the 10Y segment. For the week, both curves steepened: Germany's bear steeper (2s +4.3bp, 10s +6.4bp), with the UK's twist steepening (2Y -0.2bp, 10Y +6.4bp).

- Periphery/semi-core EGB spreads fell, reflecting the risk-on backdrop.

- Recal that Monday is a UK market holiday. Next week sees the BOE decision (a 25bp cut is fully priced)

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 7.6bps at 1.762%, 5-Yr is up 9.5bps at 2.08%, 10-Yr is up 8.9bps at 2.533%, and 30-Yr is up 8.9bps at 2.971%.

- UK: The 2-Yr yield is up 3.5bps at 3.856%, 5-Yr is up 3.4bps at 3.977%, 10-Yr is up 2.7bps at 4.508%, and 30-Yr is up 4.3bps at 5.303%.

- Italian BTP spread down 1.7bps at 110.3bps / French OAT down 1.5bps at 71.4bps

MNI FOREX: AUDUSD Rises Above 0.6450 Amid Surging Equities/Softer Greenback

- Prior to the US employment report, the greenback traded weaker against all others, with the USD Index reversing off yesterday's recovery high at 100.375. Trade negotiations remain a focus for markets - with deals between the US and Japan/India seen as particularly advanced. Furthermore, a greater sense of optimism regarding China/US discussions is reflected by the 0.8% for the Chinese Yuan.

- A higher-than-expected NFP print was offset by lower revisions which sparked some short-term volatility. USDJPY snapped higher to 145.00 before then steadily reversing south to print fresh session lows below the 144.00 mark. Equities like the print however, as the lack of major deterioration in the US labour market boosts global sentiment prompting USDJPY to rally the best part of 100 pips into the close to ~144.70.

- This sentiment has bolstered the likes of AUD, NZD and the Scandies which are the best performers in G10. For AUDUSD specifically, fresh yearly highs above 0.6450 have been printed as the pair currently stands 1% high on the session. The underlying trend remains bullish, and spot has recently breached a key resistance at 0.6409, the Dec 9 ‘24 high. The initial target of 0.6471 (Dec 9 high) has been met, which places the focus on 0.6528 (Nov 29 high) next.

- There has been less enthusiasm for the Euro, and despite a post data surge to 1.1380, we are back closer to the 1.1300 mark ahead of the close, down around half a percent on the week. An additional mention to USDCHF, which continues to respect the prior breakdown point of 0.8333 as pivot resistance ahead of Swiss CPI on Monday.

- The US ISM services PMI will also garner attention Monday, where UK and Japan are both out for national holidays.

MNI OPTIONS: Expiries for May05 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1073(E2.4bln), $1.1100($1.5bln), $1.1120-25(E1.1bln), $1.1190-00(E2.0bln), $1.1285-00(E3.0bln), $1.1400(E636mln)

- GBP/USD: $1.3100-20(Gbp529mln)

- EUR/GBP: Gbp0.8525(E740mln)

- AUD/USD: $0.6500(A$509mln), $0.6550-60(A$1.0bln), $0.6635-45(A$1.1bln)

- USD/CAD: C$1.3865-70($2.6bln)

MNI US STOCKS: Late Equities Roundup: Drifting Near Four Week Highs on Trade Hopes

- Stocks are extending late Friday session highs, trying to get ahead of further price gains in the event of any positive trade negotiation headlines. For instance, the Wall Street Journal reports that "Beijing is considering ways to address the Trump administration’s gripes over China’s role in the fentanyl trade... potentially offering an off-ramp from hostilities to allow for trade talks to start."

- Stocks are back near pre-Liberation Day levels with the DJIA trades up 547.59 points (1.34%) at 41303.44, S&P E-Minis up 90 points (1.6%) at 5713.75, Nasdaq up 287.8 points (1.6%) at 17998.87.

- Interactive media and entertainment shares continued to buoy the Communication Services sector in late trade: Meta Platforms +5.57%, Electronic Arts +4.47%, Walt Disney +2.53% and Live Nation Entertainment +2.28%.

- While banks and services shares continued to support the Financial sector: Franklin Resources +7.34%, Discover Financial Services +5.00%, Capital One Financial +4.92%, Arthur J Gallagher +4.00% and Synchrony Financial +3.98%.

- Missing the broad based rally, the following shares weighed on the Consumer Discretionary sector: Hershey Co -3.19%, Conagra Brands -1.53%, Kroger -0.54% and General Mills -0.41%.

- Meanwhile, a small handful of oil & gas stocks weighed on the Energy sector as crude prices trade weaker (WTI -1.07 at 58.17): EOG Resources -1.15%, Targa Resources -0.11% while Occidental Petroleum rose a scant 0.15%.

- Earnings resume in earnest Monday, ahead th e open: Berkshire Hathaway, ON Semiconductor, Ares Management, Cummins, Tyson Food. After Monday’s close: Neurocrine Biosciences, Mattel, Ford Motor, Clorox, Diamondback Energy, Williams Cos, Realty Income, Celanese, Coterra Energy, Vertex Pharmaceuticals, Air Lease and Palantir Technologies Inc.

MNI EQUITY TECHS: E-MINI S&P: (M5) Tops 50-Day EMA

- RES 4: 5837.25 High Mar 25 and a bull trigger

- RES 3: 5865.15 200-dma

- RES 2: 5773.25 High Apr 2

- RES 1: 5662.25 High Apr 28

- PRICE: 5656.00 @ 08:35 BST May 2

- SUP 1: 5355.25/5127.25 Low Apr 24 / 21 and a key support

- SUP 2: 4996.43 76.4% retracement of the Apr 7 - 10 bounce

- SUP 3: 4832.00 Low Apr 7 and the bear trigger

- SUP 4: 4760.88 1.618 proj of the Feb 19 - Mar 13 - 25 price swing

The recovery in the e-mini S&P continues, with a tenth consecutive session of higher highs - the longest winning streak of the year so far, underpinning the short-term positive momentum for stocks. The bull cycle that started on Apr 7, remains in play and has breached a number of important short-term resistances. The index has topped 5618.25, the 50-day EMA, opening layered resistance at 5773.25-5774.43.

COMMODITIES

MNI AMERICAS OIL: WTI crude has declined today with OPEC+ moving its meeting

May 2 - Americas End-of-Day Oil Summary: WTI crude has declined today with OPEC+ moving its meeting to Saturday from May 5 raising uncertainty, adding to pressure from wider demand concerns. Threats of further sanctions on Iran and signs of a possible easing of trade tensions between the US and China have been supportive.

- OPEC+ has brought forward its video conference to discuss June production levels to Saturday, according to Bloomberg. It is scheduled for noon Vienna time and market expectations are generally for a large output hike.

- OPEC+ production fell by 200kb/d in April due to the winding down of operations in Venezuela by US producers.

- China’s Commerce Ministry said in a statement on Friday that it was evaluating recent messages by the US “hoping to start talks with China.”

- Trump stated that the US will sanction any nation or person who buys oil or petrochemicals from Iran in breach of sanctions. The US-Iran meeting provisionally planned for Saturday May 3rd has been rescheduled according to Qatari officials.

- WTI June futures were down 1.5% at $58.29

- WTI July futures were down 1.4% at $57.89

- RBOB Jun futures were down 1.4% at $2.02

- ULSD Jun futures were down 0.9% at $1.99

- US gasoline crack down 0.5$/bbl at 26.51$/bbl

- US ULSD crack up 0$/bbl at 25.40$/bbl

MONDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 05/05/2025 | 0630/0830 | *** | CPI | |

| 05/05/2025 | 0700/0300 | * | Turkey CPI | |

| 05/05/2025 | 1345/0945 | *** | S&P Global Services Index (final) | |

| 05/05/2025 | 1345/0945 | *** | S&P Global US Final Composite PMI | |

| 05/05/2025 | 1400/1000 | *** | ISM Non-Manufacturing Index | |

| 05/05/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 05/05/2025 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 05/05/2025 | 1700/1300 | *** | US Note 03 Year Treasury Auction Result | |

| 06/05/2025 | 0130/1130 | * | Building Approvals | |

| 06/05/2025 | 0145/0945 | ** | S&P Global Final China Services PMI | |

| 06/05/2025 | 0145/0945 | ** | S&P Global Final China Composite PMI |