MNI ASIA MARKETS ANALYSIS: Sentiment Ebbs Ahead Sep Minutes

HIGHLIGHTS

- Treasuries appeared to take on a risk-off tone - coinciding with equities quickly reversing course from new record highs in SPX and Nasdaq indexes, no obvious headline or flow driver.

- Federal Reserve Governor Stephen Miran said Tuesday the central bank needs to lower interest rates and that stable long term interest rates flow from success in achieving the central bank's dual mandate goals.

- SF Fed’s Daly gave an AI-focused interview to Axios, her first public comments since she said on Sep 25 that the policy rate remains modestly restrictive with more cuts needed over time to balance risks.

- Atlanta Fed’s Bostic (non-voter) in a moderated discussion, touting the bank’s surveys including its CFO survey and unstructured regional economic information network.

- The government shutdown extended into a 7th day, and a lack of breakthrough by the end of this week will begin to prompt furloughed workers to miss pay checks, adding pressure to lawmakers to come to a resolution.

US TSYS

MNI US TSYS: Tsys Rise as Risk Sentiment Cools, Focus On Wednesday's FOMC Minutes

- Treasuries unwound early weakness - look to finish higher across the board Tuesday as risk sentiment cooled early in the first half with stocks rejecting new record highs.

- Stocks are holding weaker levels on narrow ranges after SPX and the Nasdaq indexes retreated from new record highs on Tuesday's open. No obvious block or headline driver as rates climbed to new session highs.

- Treasuries briefly extended highs after the Tsy $58B 3Y note auction (91282CPC9) stops through again: drawing 3.576% high yield vs. 3.584% WI; 2.66x bid-to-cover vs. 2.73x prior.

- Tsy Dec'25 10Y contract currently at 112-20 (+7.5) vs. 112-24 high, initial firm resistance to watch is 113-00, the Sep 24 high. A break would be bullish. Curves mixed: 2s10s -.684 at 55.678, 5s30s +.662 at 101.848.

- U.S. government shutdown extended into a 7th day, and a lack of breakthrough by the end of this week will begin to prompt furloughed workers to miss pay checks, adding pressure to lawmakers to come to a resolution.

- Look ahead: September FOMC Minutes, Fed Speak, 10Y R/O.

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.15% (-0.03), volume: $2.981T

- Broad General Collateral Rate (BGCR): 4.13% (-0.03), volume: $1.181T

- Tri-Party General Collateral Rate (TCR): 4.13% (-0.03), volume: $1.147T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.09% (+0.00), volume: $84B

- Daily Overnight Bank Funding Rate: 4.09% (+0.00), volume: $164B

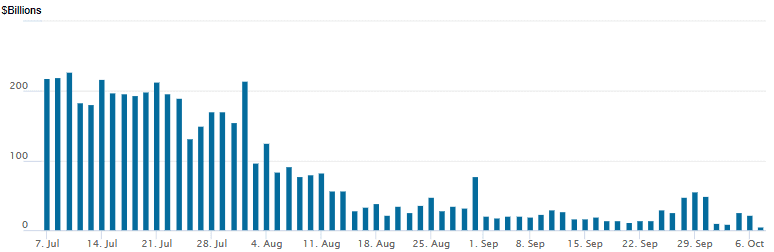

FED Reverse Repo Operation

RRP usage retreats to new multi-year low of $4.622B (lowest level since early April 2021) with 14 counterparties this afternoon from $21.776B on Monday. Compares to this year's high usage of $460.731B on June 30.

US SOFR/TREASURY OPTION SUMMARY

Option desks report light SOFR/Treasury call option trade overnight, leaning towards low delta puts as the US Gov shutdown continues. Underlying Tsy futures firmer, off late session highs after climbing steadily off this morning's lows (TYZ5 112-09 low, September 28 level). Projected rate cut pricing has gained slightly vs. early morning levels (*): Oct'25 at -23.7bp (-23.1bp), Dec'25 at -45.1bp (-44.2bp), Jan'26 at -55.7bp (-54.6bp), Mar'26 at -66.4bp (-65.4bp).

SOFR Options:

+10,000 SFRZ5 96.62/96.75 call spds 0.5 ref 96.32

+15,000 SFRZ5 96.62/96.68 call spds, cab vs. 96.30/0.05%

Update, +12,500 SFRZ5 96.43/96.50/96.56 call flys, 0.25

+15,000 SFRZ5 96.50/96.62 call spds, 1.0

1,000 SFRZ5 96.18/96.37/96.56 2x3x1 put flys

+1,500 0QV5 96.87/97.06 strangles, 1.5 vs. 96.91/0.20%

1,750 0QV5 96.62/96.75/96.87 put flys, 0.5 vs. 96.955/0.08%

+3,000 SFRZ5 96.50/96.62 call spds, 1

-4,100 SFRV5 96.31 puts, 1.25 ref 96.315

Treasury Options:

4,400 USZ5 115 puts, 51 ref 116-26

-15,000 FVX5 108.5/110 call over risk reversals, 0.5

10,000 USX5 109 puts, 2 ref 116-17

2,000 FVX5/FVZ5 110 put spds

7,500 FVX5 110 calls 3, ref 109-05.5

3,225 TYX5/TYZ5 111/111.5 put spd spd

+5,000 TYX5 112.5/113.5 call spds 7 over 111.25 put vs. 112-05.5/0.41%

-1,000 TYX5 111.25/113.5 strangles, 11 vs. 112-07/0.02%

-2,000 TYX5 112.5 calls, 24 vs. 112-12.5/0.44%

4,000 Tue/wkly 10Y 111.5 puts ref 112-11 (exp 10/14)

-5,500 wk2 US 115 puts, 4 ref 116-07

+1,000 wk3 FV 109.25/109.75 4x5 call spds, 27 vs. 109-04/0.92%

-5,400 TYZ5 109.5 puts, 4 ref 112-14 to -14.5

MNI BONDS: EGBs-GILTS CASH CLOSE: Curves Reverse Some Of Prior Steepening

Core European yields pulled back slightly Tuesday, with bull flattening across most curves partially reversing Monday's steepening.

- Yields started off on the ascent in morning trade, following on from Monday's weakness (triggered by apprehension over Japanese fiscal expansion following the LDP leadership elections).

- But tthey fell steadily over the course of the European afternoon however, with a sharp pullback in global equities boosting core instruments into the cash close.

- In data, German August factory orders were very weak, driven by softer foreign demand.

- On the day, the German curve leaned bull flatter, with Gilts more clearly bull flattening and outperforming German counterparts.

- Periphery/semi-core EGB spreads widened again, though this time OATs weren't the underperformers, with French spreads steadying after being sent higher after Monday's surprise resignation by PM Lecornu. Instead, Spain and Portugal 10Y/Bund widened 1+bp each.

- Wednesday's calendar includes an appearance by BOE's Pill and ECB's Muller, Elderson and Escriva, and German industrial production data (following on from factory orders).

- However most attention will be on France where ex-PM Lecornu will attempt to break a political deadlock ahead of telling President Macron whether a sustainable coalition government is workable or other alternatives (eg snap elections) should be pursued.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 0.3bps at 2.004%, 5-Yr is down 0.7bps at 2.298%, 10-Yr is down 1bps at 2.709%, and 30-Yr is down 0.3bps at 3.293%.

- UK: The 2-Yr yield is down 0.9bps at 3.983%, 5-Yr is down 0.5bps at 4.148%, 10-Yr is down 1.7bps at 4.719%, and 30-Yr is down 2.1bps at 5.534%.

- Italian BTP spread up 0.6bps at 82.7bps / Spanish up 1.1bps at 54.8bps

MNI OPTIONS: Euro Rate Call Condor Buying Continues

Tuesday's Europe rates/bond options flow included:

- DUZ5 107.10/107.00/106.90p Ladder, bought for 1.5 in 7.6k

- ERM6 98.1875/98.25cs 1x1.75 with ERH6 98.00/97.9375ps sold as a strip at 1 in 4k

- ERM6 98.37/98.50/98.75/98.87c condor, bought for 1 in 5k (also bought Monday in 14k)

- ERM6 98.50/98.625/98.750/98.875 call condor, bought for 0.5 in 18k

- 0RH6 98.12/98.37cs, bought for 3.5 in 4k

- 2RZ5 97.6875/97.8125cs vs 3RZ5 97.5625/97.6875cs, bought for 2.75 in 10k

MNI FOREX: NZD Slides Into RBNZ Decision, BoJ Hike Patterns in Focus

- Through the London close JPY printing fresh pullback lows, helping trigger a new all-time high for EURJPY for a second session at 176.36. The JPY leg remains dominant for now, and Takaichi's ability to quell concern among junior coalition partners should prove key to any near-term JPY bounce

and challenge to the JPY weakening bias. - BoJ rate hike timing should also prove key here: the fading odds for an October hike have worked against JPY near-term, but more assertive messaging

for a December hike may mean JPY weakness is limited here on out. We flagged earlier today the rising risk of a correction lower in JPY

crosses, which now screen overbought in many crosses on the 14-day RSI for the first time since mid-September. - The medium-term run higher in gold has continued, helping spot to new record highs of 3985.7 (although in futures space, COMEX gold has now shown above $4,000 for the first time), but the strength in gold looks pretty isolated: silver, oil prices and base metals are all seen lower, which may be limiting the bounce off lows for AUD/USD, which is yet to bounce back above 0.6600. NZD remains the underperformer into the RBNZ rate decision, and with 36bps of easing priced for Wednesday's meeting and a cumulative 63bps by November, markets may be erring in favour of a more sizeable rate cut this week.

- A return lower for NZD would re-open upside in AUD/NZD through to 1.1355-67 resistance, clearance above which returns focus to the bull trigger and cycle high at 1.1418.

- Despite a strong start to Tuesday trade, equity futures slipped sharply following the opening bell, opening a decent gap with the alltime highs posted across a number of markets in recent weeks. Small cap names underperformed, evident in the Russell 2000 slipping faster than the S&P 500. The government shutdown extended into a 7th day, and a lack of breakthrough by the end of this week will begin to prompt furloughed workers to miss paycheques, adding pressure to lawmakers to come to a resolution. House Dem Leader Jeffries painted a bleak picture of the hopes of near-term talks, suggesting there remains a very large gap between lawmakers on resolving the government shutdown - he noted a proposal to extend ACA credits for one year as "laughable" and unacceptable.

- German industrial production data is the data highlight Wednesday, while the FOMC minutes are set to follow, providing the FOMC's latest views on policy ahead of the government shutdown from one week ago. Several central bank speakers are due, including ECB's Escriva, Muller & Elderson, BoE's Pill and Fed's Musalem, Barr & Kashkari.

MNI OPTIONS: Expiries for Oct08 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1650(E698mln), $1.1700(E1.1bln), $1.1770-80(E1.2bln), $1.1800(E1.5bln), $1.1850-60(E1.0bln)

- USD/JPY: Y146.50($1.2bln), Y147.00($1.5bln), Y149.00($980mln), Y150.00($562mln), Y151.00($799mln)

MNI US STOCKS: Late Equities Roundup: SPX, Nasdaq Remain Off Record Highs

- Stocks are holding weaker levels on narrow ranges after SPX and the Nasdaq indexes retreated from new record highs on Tuesday's open. No obvious block or headline driver as rates climbed to new session highs.

- Currently, the DJIA down 137.43 points (-0.29%) at 46,558.86, S&P E-Minis down down 28.5 points (-0.42%) at 6,760.75 (6,802.75 high), Nasdaq down 143 points (-0.6%) at 22797.43 (23,006.07).

- Consumer Discretionary and Information Technology sector shares continue to lead the decline late Tuesday, a mix of auto, home and travel related shares weighed on the Discretionary sector: Ford Motor Co -5.98%, DR Horton Inc -5.95%, PulteGroup -4.64%, Deckers Outdoor -4.38% and Expedia Group -4.00%.

- Technology stocks underperformed in the second half: Seagate Technology -7.24%, Teradyne -5.11%, Lam Research -4.81% and NXP Semiconductors -4.72%.

- On the positive side, Consumer Staples and Utility sector shares led gainers in late trade: Kenvue +2.68%, Kroger +2.50%, Colgate-Palmolive +1.83% and Mondelez International +1.59%.

- Meanwhile, American Water Works +2.12%, Exelon +2.04%, American Electric Power +2.01% and NextEra Energy +1.55% led gainers in the Utility sector.

MNI EQUITY TECHS: E-MINI S&P: (Z5) Fresh Cycle High

- RES 4: 6831.38 2.500 proj of the Aug 20 - 28 - Sep 2 price swing

- RES 3: 6819.25 1.500 proj of the Aug 1 - 15 - 20 price swing

- RES 2: 6812.29 2.382 proj of the Aug 20 - 28 - Sep 2 price swing

- RES 1: 6802.75 Intraday high

- PRICE: 6759.00 @ 1503 ET Oct 7

- SUP 1: 6694.17 20-day EMA

- SUP 2: 6624.25 Low Sep 25

- SUP 3: 6575.48 50-day EMA

- SUP 4: 6506.50 Low Sep 5

A bull cycle in S&P E-Minis remains intact. The contract has again traded to a fresh cycle high to confirm a resumption of the uptrend and maintain the positive price sequence of higher highs and higher lows. Sights are on 6812.29, a Fibonacci projection. Initial support to watch is at the 20-day EMA, at 6694.17. It has recently been pierced, a clear break of it would signal scope for a deeper pullback, potentially towards the 50-day EMA, at 6575.48.

MNI COMMODITIES: Gold Hits Another Record High, Silver Pulls Back, Crude Steady

- Spot gold rose to another record high at $3,991/oz earlier in Tuesday’s session, despite a stronger US dollar, as safe-haven flows continue to push bullion higher amid ongoing government instability in the US, Japan and France.

- Spot is currently up by 0.5% at $3,980, just short of psychological round number resistance at $4,000.

- Citing ETF inflows and central-bank buying, Goldman Sachs has raised its end-2026 gold price forecast to $4,900, from $4,300.

- From a technical perspective, a bull cycle in gold remains in play, reinforced by today’s fresh cycle high. A break of the $4,000 handle would open $4,035.6 next, a Fibonacci projection. Support to watch lies at $3,775.0, the 20-day EMA.

- In contrast, silver has pulled back sharply today, falling by 1.8% to $47.6/oz, having hit its highest level since April 2011 yesterday.

- Trend signals in silver remain bullish, with sights on $48.838 next, a Fibonacci projection. Clearance of this level would pave the way for a climb towards the $49.00 handle. Initial firm support to watch lies at $45.038, the 20-day EMA.

- Meanwhile, crude prices are steady following a slight rise yesterday after a smaller than anticipated OPEC+ supply hike and soft Saudi OSPs.

- WTI Nov 25 is broadly unchanged at $61.7/bbl.

- WTI futures remain in a bear-mode condition, and gains are considered corrective. Initial support is at $60.40, the Oct 2 low, while initial firm resistance has been defined at $66.42, the Sep 29 high.

WEDNESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 08/10/2025 | 0500/1400 | Economy Watcher's Survey | ||

| 08/10/2025 | 0600/0800 | ** | Industrial Production | |

| 08/10/2025 | 0600/0800 | *** | Flash Inflation Report | |

| 08/10/2025 | 0600/0800 | *** | Flash Inflation Report | |

| 08/10/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 08/10/2025 | 1030/1230 | ECB Elderson In Panel at Finance Conference | ||

| 08/10/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 08/10/2025 | 1320/0920 | St. Louis Fed's Alberto Musalem | ||

| 08/10/2025 | 1330/0930 | Fed Governor Michael Barr | ||

| 08/10/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 08/10/2025 | 1430/1030 | ** | US DOE Petroleum Supply | |

| 08/10/2025 | 1500/1600 | BOE Pill Speech at University of Birmingham | ||

| 08/10/2025 | 1600/1800 | ECB Lagarde Video Message at Werner Report Event | ||

| 08/10/2025 | 1700/1300 | ** | US Note 10 Year Treasury Auction Result | |

| 08/10/2025 | 1800/1400 | FOMC Minutes | ||

| 08/10/2025 | 1915/1515 | Minneapolis Fed's Neel Kashkari | ||

| 08/10/2025 | 2145/1745 | Fed Governor Michael Barr |