MNI ASIA MARKETS ANALYSIS: Risk Off Raises Rates Ahead FOMC

HIGHLIGHTS

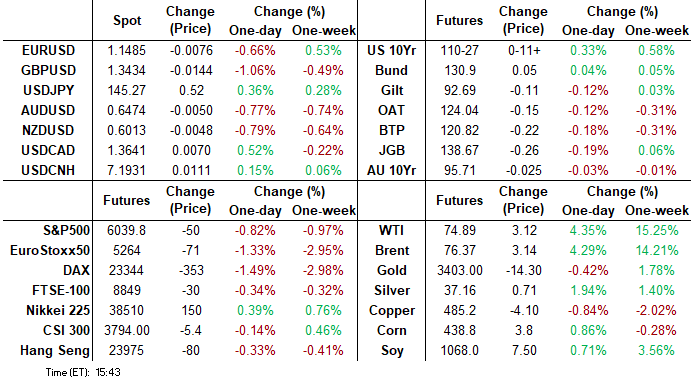

- Treasuries look to finish near highs as Middle East tensions continue to heat up, Pres Trump social media posts raised chances the US will join the war.

- Despite tensions, overall ranges were rather constrained as markets await Wednesday's FOMC policy announcement including a Summary of Economic Projections (Dots).

- Due to Thursday's "Juneteenth" holiday, Wednesday will accommodate additional data: weekly jobless & continuing claims, house starts, build permits, TIC flows and three US Treasury bill auctions (4, 8- and 17W bills).

US TSYS

MNI US TSYS: Safe Haven Raises Rates in Lead-Up to FOMC Policy Annc

- Rising Middle East tensions included chances the US will join the war lent to the second half risk-off support for Treasuries Tuesday. Otherwise, markets await Wednesday's FOMC policy announcement including a Summary of Economic Projections (Dots).

- Pres Trump: "We know exactly where the so-called “Supreme Leader” is hiding. He is an easy target, but is safe there - We are not going to take him out (kill!), at least not for now. But we don’t want missiles shot at civilians, or American soldiers. Our patience is wearing thin. Thank you for your attention to this matter!"

- We expect that the June FOMC meeting communications will reflect an increasingly patient attitude since May and certainly since March’s projections.

- Cross asset update: stocks ebbed in the second half (SPX eminis -44.75 at 6045.0), West Texas crude climbed to early July 2024 highs (WTI +3.39 at 75.16), while Bbg US$ index climbed to June 11 highs (BBDXY +6.43 at 1209.02).

- Tsy Sep'25 10Y futures trades +12.5 at 110-28 vs. 111-00 high, below key resistance and its recent high of 111-14+, a Fibonacci retracement and the Jun 5 high. Clearance of this hurdle would be bullish and highlight a stronger reversal. This would open 111-30, a Fibonacci retracement.

- Curves flatter, 2s10s -4.250 at 43.309, 5s30s -1.837 at 90.209. 10Y yield at 4.3849% vs. 4.3770% low.

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.32% (+0.04), volume: $2.697T

- Broad General Collateral Rate (BGCR): 4.30% (+0.03), volume: $1.090T

- Tri-Party General Collateral Rate (TCR): 4.30% (+0.03), volume: $1.065T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $101B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $273B

FED Reverse Repo Operation

RRP usage bounces to $168.939B this afternoon from $140.759B yesterday, total number of counterparties at 37. Usage had fallen to $54.772B on Wednesday, April 16 -- lowest level since April 2021. Conversely, usage had surged to the highest level since December 31, 2024 on Monday, March 31: $399.167B.

US SOFR/TREASURY OPTION SUMMARY

SOFR & Treasury option flow leans bullish Tuesday as Middle East tensions spurred risk-off support in rates. Breadth of moves rather modest as markets also await Wednesday's FOMC policy annc. Despite the rally, curves bull flattened while projected rate cut pricing retreated from morning's levels (*) as follows: Jun'25 at 0.0bp, Jul'25 steady at -3.6bp, Sep'25 at -17.7bp (-19.5bp), Oct'25 at -29.6bp (-32.6bp), Dec'25 at -45.2bp (-48.8bp).

SOFR Options

-10,000 SFRZ5 95.56/95.68/95.81 put trees, 2.125

+5,000 SFRZ5 96.25/96.50/96.75 call flys, 2.0 ref 96.11

-15,000 SFRU5 95.75/95.87 2x1 put spds 2.0 over SFRZ5 95.62/95.75 2x1 put spds

+10,000 0QZ5 96.75/97.00/97.50/97.75 call condors, 6.0 ref 96.695

Block: -9,000 SFRZ5 97.00/97.25/97.75/98.00 call condors, 0.75 ref 96.09.5

-10,000 0QZ5 97.50/97.62 call spds, 1.75 vs. 96.73/0.05%

+2,500 SFRZ5 96.37/96.75 call spds vs. 0QZ5 97.25/97.50 call spd, 1.5 net/steepener

+2,500 SFRN5 95.37/95.68 put spds, .37

*-4,000 SFRU5 95.68/95.81/96.25/96.37 call condors, 5.25 ref 95.875

2,000 0QU5 96.75/97.00/97.25 call flys ref 96.68 to -.675

3,000 SFRN5 96.00/96.12/96.75 broken call trees ref 95.885

+13,500 SFRQ5 95.62/95.75 put spds 2.5

2,000 SFRZ5 96.37/96.75 call spds vs. 0QZ5 97.25/97.50 call spds

+1,250 SFRZ5 96.25/96.37/96.62/96.75 call condors, 1.75 ref 96.13

+2,000 0QZ5 97.00/97.31 call spds, 8

Treasury Options

-5,250 TYN5/TYQ5 111.5 put spds, 35 (Aug over) ref 110-28

8,000 TYN5 110.75/111 call spds, 6 ref 110-25

10,000 TUQ5/TUU5 104 call spds, 4.5 ref 103-20.25

3,500 TYN5 111/111.5 call spds ref 110-25

5,000 wk4 TY 110.75 straddles, 56 ref 110-25.5 (exp 6/27)

3,000 TUN5/TUQ5 103.75 call spds 8 ref 103-20.88

2,000 TYN5 110.5 straddles, 38.0

+2,000 FVN5 108.5 calls, 5 vs 108-03/0.24%

+5,000 TUQ5 103/104.125 call over risk reversals, 4 ref 103-20

+3,000 FVQ5 107.25/109 call over risk reversal, 1 ref 108-01.5

+2,500 TYU5 111.5 calls, 54 vs. 110-22/0.22%

+3,000 Wed wkly 111/111.25 call spds, 3 ref 110-18.5 (exp tomorrow)

+2,000 FVN5 108.25 calls, 7 vs. 107-31.25/0.30%

MNI BONDS: EGBs-GILTS CASH CLOSE: Flatter Curves With Geopolitics Front Of Mind

European yields rose modestly Tuesday, with curves mostly flattening.

- Yields gapped higher on the open, catching up with the weakness in global bonds after Monday's cash close. Geopolitical and related inflation (energy)-related risk weighed on sentiment throughout amid the ongoing Israel-Iran conflict.

- Yields moved lower and hit session lows in a safe haven bid as the Israeli Defence Minister pointed to further attacks on Iran, a move that extended after weaker-than-expected US retail sales data.

- Core EGBs and Gilts would pull back again over the afternoon, with oil and gas prices moving higher, and some consideration given to robust US core retail data and firm import prices.

- German ZEW expectations jumped in June, with current conditions also improving.

- The German curve twist flattened, with the 2Y-5Y segment underperforming the UK which saw bear steepening and longer-end underperformance ahead of Wednesday's UK CPI data.

- Periphery / semi-core EGB spreads widened steadily through a broadly risk-off session.

- MNI's Markets Team sees downside risks to the headline UK CPI and services readings Wednesday - our preview is here.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 2.7bps at 1.868%, 5-Yr is up 2.1bps at 2.141%, 10-Yr is up 0.8bps at 2.535%, and 30-Yr is down 0.1bps at 2.985%.

- UK: The 2-Yr yield is up 1.7bps at 3.923%, 5-Yr is up 1.3bps at 4.053%, 10-Yr is up 1.7bps at 4.55%, and 30-Yr is up 2.9bps at 5.283%.

- Italian BTP spread up 2.4bps at 95.2bps / Spanish up 1.3bps at 63bps

MNI EGB OPTIONS: Notable Bobl Put, Euribor Call Ladder Buying

Tuesday's Europe rates/bond options flow included:

- OEQ5 117p, bought for 18.5 in ~11.2k

- RXN5 130/129.50ps, sold at 9.5 in 2k

- ERU5 98.25/98.37cs, bought for 1 in 10k

- ERZ5 98.25/98.50/98.625c ladder, bought for 3.75 in 3.5k

- ERZ5 98.25/98.375/98.50c ladder, bought for half in 2k

- ERZ5 98.25/98.50cs vs 98.00p, bought the cs for 2.25 in 5k

- 2RU5 97.93/97.75ps 1x2, bought for 0.75 in 2.5k

- SFIZ5 96.50/96.70cs, bought for 4 in 5.3k

- SFIH6 95.70/95.40ps 1x2, sold the 1 at -0.25 in 4k

MNI FOREX: USD Strength Extending as Middle-East Tensions Rise

- Headlines surrounding the Israel-Iran conflict, paired with President’s Trump escalatory rhetoric, have dented risk sentiment in currency markets, which has filtered through into a steady move higher for the US dollar across the US session.

- GBPUSD is notably underperforming in G10 as the pair currently tracks 0.87% lower on the session as we approach the APAC crossover, comfortably back below the 1.35 mark.

- This has coincided with a breach of the 20-day exponential moving average, of which spot has not closed below since May 12. A sustained break would be a bearish development, signalling scope for a deeper retracement below 1.3456 (Jun 10 low) and targeting the 50-day EMA at 1.3346.

- The likes of EUR, AUD and NZD have fallen over half a percent against the greenback. Price action has seen EURUSD slip back below 1.15, in what is deemed as a corrective selloff for now.

- USDJPY has risen 0.3%, evidence of the broad dollar strength on display. The pair is narrowing the gap to last week’s highs at 145.46. Key short-term resistance remains further out at 146.28, the May 29 high.

- Wednesday’s data calendar kicks off with UK CPI. US jobless claims & housing starts will precede the June FOMC decision later in the session.

MNI FX OPTIONS: Expiries for Jun18 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1500(E2.2bln), $1.1600-04(E1.0bln), $1.1645-50(E1.2bln)

- USD/JPY: Y144.00($725mln)

- NZD/USD: $0.5760(N$1.2bln)

- USD/CAD: C$1.3600($1.4bln)

- USD/CNY: Cny7.3000($858mln)

MNI US STOCKS: Late Equities Roundup: Risk-Off on Middle East Tension, Will US Join?

- Still off early Monday lows, stocks are retreating late Tuesday as Middle East tensions heat up. Following a series of social media posts around midday, wires said Pres Trump is considering joining Israel on striking Iran. Markets currently await a state Department press briefing.

- Currently, the DJIA trades down 320.42 points (-0.75%) at 42195.11, S&P E-Minis down 51.25 points (-0.84%) at 6038.5, Nasdaq down 185.9 points (-0.9%) at 19515.53.

- A mix of Health Care, Materials and Consumer Discretionary sectors underperformed in the first half, but it was a handful of Tech stocks led laggers: Enphase Energy -22.82%, First Solar -17.95% and AES -9.12% as the Senate looks to end wind & solar tax credits.

- Pharmaceuticals traded weaker as the WH considers cracking down on drug company advertising: Charles River Laboratories -4.56%, Bio-Techne -3.78%, IQVIA Holdings -3.15%, Thermo Fisher Scientific -2.93% and AbbVie -2.73%.

- The Energy sector outperformed as said geopol risk buoyed crude prices (WTI +2.804 at 74.57) in turn supported oil and gas stocks: Valero Energy +2.32%, APA Corp +2.17%, Diamondback Energy +2.15% and Chevron +1.92%.

MNI EQUITY TECHS: E-MINI S&P: (U5) Trend Condition Remains Bullish

- RES 4: 6200.00 1.500 proj of the Apr 7 - 10 - 21 price swing

- RES 3: 6172.50 High Feb 24

- RES 2: 6134.00 High Feb 26

- RES 1: 6128.75 High Jun 11 and the bull trigger

- PRICE: 6037.25 @ 1505 ET Jun 17

- SUP 1: 5979.00/5890.99 Low Jun 13 / 50-day EMA

- SUP 2:5811.50 Low May 23

- SUP 3: 5645.75 Low May 7

- SUP 4: 5500.00 Low Apr 30

The trend condition in S&P E-Minis is unchanged, it remains bullish and the contract traded to a fresh cycle high last Wednesday, reinforcing current bullish conditions. For now, the most recent pullback is considered corrective. The contract has pierced support at 6000.18, the 20-day EMA. A clear breach of this average would expose the 50-day EMA, at 5890.99. Key short-term resistance has been defined at 6128.75, the Jun 11 high.

MNI COMMODITIES: Crude Extends Gains Amid Mounting Geopolitical Tensions

- Crude has extended gains after US administration rhetoric late in the day raised the prospects of US direct involvement in the Iran-Israel conflict.

- WTI Jul 25 is up by 4.9% at $76.8/bbl, taking gains over the last week to over 15%.

- Several military analysts and reporters have interpreted VP JD Vance's recent social media post as laying the groundwork for President Trump to authorise the use of 'bunker buster' bombs to strike Iran's Fordow nuclear facility.

- The sharp rally in WTI futures marks an acceleration of the current bull phase. Price action is likely to remain volatile near-term, and from a technical standpoint, the trend is currently in an extreme overbought position.

- A continuation higher would expose the $80.00 handle, followed by $81.93, a Fibonacci projection.

- Meanwhile, spot gold is little changed at $3,383/oz.

- A bullish theme in gold remains intact, with initial resistance at $3,451.3, the Jun 16 high. Initial key support to monitor is $3,271.7, the 50-day EMA.

- By contrast, silver has rallied by 2.0% today to $37.0/oz, taking the precious metal to a new multi-year high. As a result, the gold-silver cross has fallen to 91.4, close to recent 2-month lows.

- A bull wave in silver remains in play, with sights on $37.195 next, a Fibonacci projection, which was pierced earlier. A clear break would open $37.478, the March 2012 high.

WEDNESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 18/06/2025 | 0600/0700 | *** | Consumer inflation report | |

| 18/06/2025 | 0730/0930 | *** | Riksbank Interest Rate Decison | |

| 18/06/2025 | 0730/0930 | ECB Elderson At SRB Legal Conference 2025 | ||

| 18/06/2025 | 0800/1000 | ** | EZ Current Account | |

| 18/06/2025 | 0900/1100 | *** | HICP (f) | |

| 18/06/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 18/06/2025 | 1230/0830 | *** | Housing Starts | |

| 18/06/2025 | 1230/0830 | *** | Jobless Claims | |

| 18/06/2025 | 1230/0830 | *** | Housing Starts | |

| 18/06/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 18/06/2025 | 1500/1700 | ECB Lane At Macroprudential Conference | ||

| 18/06/2025 | 1515/1115 | BOC Governor speaks in Newfoundland. | ||

| 18/06/2025 | 1600/1200 | ** | Natural Gas Stocks | |

| 18/06/2025 | 1800/1400 | *** | FOMC Statement | |

| 18/06/2025 | 1800/2000 | ECB de Guindos at Osservatorio Permanente Giovani-Editori | ||

| 18/06/2025 | 2000/1600 | ** | TICS | |

| 19/06/2025 | 2245/1045 | *** | GDP | |

| 19/06/2025 | - | NorgesBank Meeting | ||

| 19/06/2025 | - | Swiss National Bank Meeting | ||

| 19/06/2025 | 0130/1130 | *** | Labor Force Survey |