MNI ASIA MARKETS ANALYSIS: Reevaluating Middle East Conflict

HIGHLIGHTS

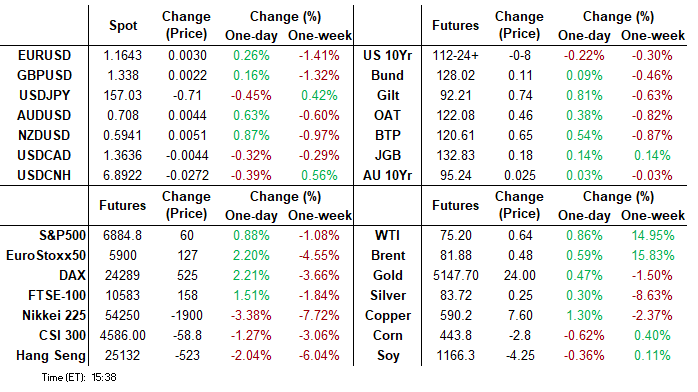

- Treasuries look to finish moderately lower, inside a rather narrow session range as markets continued to weigh the magnitude of risks tied to Saturday's US/Israel attack on Iran.

- Still up approximately 14%-15% vs. week ago levels, West Texas and Brent Crude prices traded near flat in late trade even as Iran is reported to have begun implementing an “emergency plan” to run the country under a prolonged war, semi-official Fars news reports.

- It has been a considerably more stable session for G10 FX, although perhaps surprisingly, the USD index sits just 0.2% lower on the session and is consolidating much of the week’s prior advance.

- The White House has officially nominated former Fed Governor Kevin Warsh as the next Fed chair (four-year term) for when Jerome Powell’s Chair role ends in May, along with a fourteen-year Governor role.

US TSYS

MNI US TSYS: Midweek Markets Calmer While Middle East Risks Remain

- Treasuries look to finish weaker Wednesday, 2s-10s extending lows after the bell as Pres Trump discusses the conflict with Iran from the WH, saying the US "will continue forward" and "doing well on the war front."

- TYM6 currently -8 at 112-24.5 vs. 112-23.5 low, 10Y yield +.0249 at 4.0843%. Initial technical support at 112-16+ (Low Mar 03) followed by 112-16 (50-day EMA).

- Markets continued to weigh the magnitude of risks tied to Saturday's US/Israel attack on Iran - while West Texas and Brent Crude prices traded near flat in late trade even as Iran is reported to have begun implementing an “emergency plan” to run the country under a prolonged war, semi-official Fars news reports.

- The White House has officially nominated former Fed Governor Kevin Warsh as the next Fed chair (four-year term) for when Jerome Powell’s Chair role ends in May, along with a fourteen-year Governor role. The nomination heads to the Senate but progress isn’t clear cut.

- Private payrolls rose by 63k in February, per the ADP Employment Report. This was the strongest initial reading since July 2025 and a beat vs the 50k expected, but its impact was offset by some mitigating factors that pointed to relatively subdued labor market conditions.

- Nonfarm payrolls are expected to increase 58k in February with gains coming entirely from the private sector, pulling back from a surprisingly strong January. One temporary impact known in advance was an additional 31k of striking workers over the payrolls reference period, the highest rise since late 2024. 32k workers will return in the March payrolls count.

REFERENCE RATES

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 3.70% (-0.01), volume: $3.310T

- Broad General Collateral Rate (BGCR): 3.67% (-0.02), volume: $1.381T

- Tri-Party General Collateral Rate (TCR): 3.67% (-0.02), volume: $1.338T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 3.64% (+0.00), volume: $101B

- Daily Overnight Bank Funding Rate: 3.64% (+0.01), volume: $175B

FED Reverse Repo Operation

RRP usage slips to $0.877B with 8 counterparties this afternoon vs. $1.203B Tuesday. Compares to last year's highest excess liquidity measure: $460.731B on June 30.

US SOFR/TREASURY OPTION SUMMARY

SOFR & Treasury options turned mixed, two-way repositioning Wednesday as underlying futures retreated to a narrow range as markets continued to evaluate risks tied to Saturday's US/Israel attack on Iran. Curves reversed course, bear flattening by the close while projected rate cut pricing slipped vs. late Tuesday (*): Mar'26 at -.7bp, Apr'26 at -3.5bp (-4.1bp), Jun'26 at -9.4bp (-12.3bp), Jul'26 at -16.5bp (-20.6bp), Sep'26 at -27.3bp (-32.2bp).

SOFR Options:

-5,000 0QU6 97.50 calls, 8.5 vs. 96.86/0.05%

+5,000 0QM6 96.75 puts, 11.5 vs. 96.875/0.38%

-7,500 SFRH7 96.50/96.87 2x1 put spds, 5.5 vs. 96.83/0.06%

+10,000 SFRN6 96.18/96.31 put spds, 5.0 rev 96.645

+5,000 0QH7 99.00/99.75 call spds, 2.5

+20,000 0QH6 96.87/97.00 call spds, 3.25-3.5 ref 96.85

+2,500 0QH6 96.62/97.00 call over risk reversals, 1.0 vs. 96.825/0.30%

+3,000 SFRM6 96.31 puts, 2

3,000 SFRM6 96.68/96.81 call spds ref 96.455

2,000 SFRZ6 96.12/96.25/96.31 put trees ref 96.755

8,000 SFRK6 96.25/96.31 put spds ref 96.455

+4,000 SFRM6 96.25/96.31 put spds, .75

over -29,500 0QJ6 96.50 puts, 1.5 ref 96.875

-9,000 SFRM6 96.25/96.31/96.43/96.56 put condors, 8.25 ref 96.445/0.11%

+4,000 SFRM6 96.50/96.62 call spds, 2.75 ref 96.455

+6,000 SFRN6 96.43/96.56 2x1 put spds, 1.75 vs. 96.635/0.08%

2,000 SFRM6 96.25/96.31/96.37 put fly vs. SFRJ6 96.37 put

-6,000 0QK6 96.81/96.93/97.06 put trees, 5 vs. 96.875/0.35%

5,000 SFRK6 96.31/96.43/96.56 2x3x1 put flys ref 96.445

Treasury Options:

+8,200 TYJ6 112.5/113.25 strangles, 43 ref 112-27

-7,000 FVJ6 108.5 puts, 3

-7,500 TYJ6 112/113.75 strangles, 24

+9,000 FVK6 108.25/108.5/109/109.25 put condors, 4 vs. 109-16.75/0.05%

over 7,000 FVM6 109.5 straddles, 120

Block, -12,000 TYJ6 113/113.75 strangles, 51 ref 112-31/0.20%

-3,000 TYJ6 113.5 calls, 19 vs. 112.265/0.31%

-2,000 TYJ6 112.5 puts, 24 vs. 112-26.5/0.39%

over 6,200 TYJ6 113.5 calls, 22 ref 112-26.5

over 10,700 TYJ6 112.5 puts, 24 ref 112-27

+4,000 wk1 TY 113/113.25 call spds, 5 ref 112-28

over -10,000 wk1 TY 112.75/113 put spds, 9 ref 112-27 to -26.5 (exp Fri)

+3,000 TYJ6 112.5 straddles, 107-109

+5,100 TYJ6 112 puts, 15 ref 112-24

+10,000 TYJ6 114.75 calls, 8 ref 112-27.5

2,000 FVJ6 108/108.5 put spds ref 109-16.75

2,000 FVJ6 108.25/108.75/109.25 put flys ref 109-16.25

MNI BONDS: EGBs-GILTS CASH CLOSE: Geopolitical Relief Rally

European yields mostly fell Wednesday, with Gilts outperforming Bunds.

- Nascent signs of de-escalation in the Middle East conflict helped yields pull back sharply in early trade.

- There was notable outperformance at the front end of curves in contrast to the prior two sessions' energy price related bear-flattening sell-off across EGBs and Gilts.

- Various geopolitical headlines buffeted energy prices (and thus FI) throughout, though on net Gilts would see more relief than Bunds given the former's underperformance earlier in the week, particularly at the front-end.

- In data, final February PMIs largely confirmed flashes; in new data, Italian Composite PMI hit a 3-month high while Spain's report was indicative of fading growth momentum.

- Yields would close near the lows, with the German curve twist steepening on the day while the UK's bull steepened.

- Periphery/semi-core EGB spreads tightened 2-4bp, reversing the prior session's risk-off move.

- On Thursday's calendar are Spanish and French industrial production data and Italian and Eurozone retail sales, in addition to the UK DMP survey. There are also appearances by ECB's Rehn, Nagel, and Lagarde.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 2.5bps at 2.13%, 5-Yr is down 1bps at 2.369%, 10-Yr is down 0.2bps at 2.75%, and 30-Yr is up 1.5bps at 3.401%.

- UK: The 2-Yr yield is down 2.9bps at 3.705%, 5-Yr is down 3.1bps at 3.93%, 10-Yr is down 3bps at 4.441%, and 30-Yr is down 1.7bps at 5.157%.

- Italian BTP spread down 2.5bps at 67.8bps / French OAT down 3.4bps at 60.7bps

MNI OPTIONS: Large Flow Continues To Go Both Ways In Volatile Week

Wednesday's Europe rates/bond options flow included:

- DUK6 106.70/106.80/106.90/107.10c condor, bought for 0.75 in 5k

- ERM6 97.93/98.06/98.12c fly 1x3x2, bought for 1.25 in 10k

- ERU6 97.93/98.00/98.06c fly, bought for 0.75 in 23k total

- ERU6 98.06/98.00/97.87/97.81p condor, sold at 3 in 22k

- SFIK6 96.40/96.50/96.60c fly, bought for 1.25 in 5k

- SFIU6 96.80/96.90/97.00c fly Bought for 0.75 in 10k

- SFIZ6 96.80/96.90/97.00c fly Bought for 0.5 in 25k

- SFIH7 96.80/96.90cs, bought for 2.75 in 10k

- SFIH7 98.00c, bought for 1.75 in 10k

MNI FOREX: USD Only Slightly Lower Despite Risk Recovery, AUD and NZD Outperform

- Risk sentiment has stabilised on Wednesday, with crude prices comfortably off their most recent extremes and major equity indices rallying back strongly. Resultingly, it has been a considerably more stable session for G10 FX, although perhaps surprisingly, the USD index sits just 0.2% lower on the session and is consolidating much of the week’s prior advance.

- Understandably, the likes of AUD and NZD are recovering well and stand around 1.8% and 1.6% above their Tuesday lows respectively.

- For AUDUSD, bullish conditions remain intact after support at the 50-day EMA held yesterday, intersecting at 0.6925. Short-term parameters are well defined, with a cluster of significant resistance building between 0.7125-50. Overnight, AU GDP came in slightly above expectations. At face value this keeps March RBA tightening risks in play, as the central bank may view it needs to hike more to curb growth momentum, however, the detail showed slowing in private domestic demand versus Q3 outcomes.

- Several aspects have helped provide a moderate reprieve for the Japanese yen on Wednesday, allowing USDJPY to edge further away from yesterday’s 157.97 high. These include hawkish tilting remarks from BOJ Governor Ueda, lingering FX intervention risks and stalling momentum above the post-election highs above 157.75. Initial firm support for USDJPY lies much lower at 154.00, the Feb 23 low.

- Elsewhere, EUR, GBP and CHF all kept very narrow ranges against the dollar. Swiss CPI did little to move the needle, although it is worth noting that despite the Swiss Franc unwind from earlier in the week, EURCHF currently resides within 50 pips of the 0.9025 cycle lows – with the potential to test the SNB’s resolve.

- Second-tier European data will precede the ECB minutes on Thursday, before US jobless claims. All focus will then turn to Friday’s Us employment report.

MNI OPTIONS: Expiries for Mar05 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1565(E894mln), $1.1600(E2.0bln), $1.1650-55(E2.3bln), $1.1685(E1.8bln), $1.1700(E1.0bln), $1.1700-20(E1.1bln)

- USD/JPY: Y157.00-05($1.4bln), Y158.00($818mln)

- EUR/GBP: Gbp0.8725(E698mln)

- AUD/USD: $0.7000(A$1.5bln), $0.7150(A$1.4bln)

- NZD/USD: $0.5950(N$895mln)

- USD/CAD: C$1.3600($1.9bln)

MNI US STOCKS: Late Equities Roundup: Broader Sentiment Improved, Oil Near Flat

- U.S. stock indexes continued to cling to firmer levels Wednesday, SPX eminis and Nasdaq back to pre-conflict levels while the DJIA is still off Monday's highs - let alone last week's as markets continue to weigh the magnitude of risks tied to Saturday's US/Israel attack on Iran.

- Despite the overall benign reaction in markets, geo-political risk remains fluid and sentiment can reverse quickly. Speaking of fluid markets - oil and gas shares led the midweek declines as the surge in crude prices has halted, WTI near flat on the day but still up over 14% vs. week ago levels.

- A mix of technology, financial services and health care sector shares continued to lead advances in the second half, semiconductor and defense related technology stocks continued to gain: Palantir up over 4.5% while Seagate, Micron and Western Digital held over 6% gains in late trade.

- Financial shares tied to cryptocurrencies remained supported as Bitcoin rallied over 7.9%, Coinbase Global rallying over 15.8% in the second half. Meanwhile Moderna rallied over 15.75% after settling a $950M covid vaccine patent with Arbutus & Genevant.

MNI EQUITY TECHS: E-MINI S&P: (H6) Range Base Holds For Now

- RES 4: 7066.70 1.000 proj of the Feb 6 - 11 - 17 price swing

- RES 3: 7043.00 High Jan 28 and bull trigger

- RES 2: 6983.75 High Feb 25

- RES 1: 6908.89 50-day EMA

- PRICE: 6888.00 @ 1450 ET Mar 4

- SUP 1: 6751.50/6718.72 Low Feb 6 and range base / Low Mar 3

- SUP 2: 6733.00 Low Nov 25 ‘25

- SUP 3: 6691.56 76.4% retracement of the Nov 21 - Jan 28 bull leg

- SUP 4: 6583.00 Low Nov 21 ‘25 and a key medium-term support

A bearish short-term tone in S&P E-Minis remains intact. For now, the contract is trading inside a range. Attention is on the base of the range at 6751.50, the Feb 6 low. This level has been pierced, a clear break would highlight a stronger bear threat. On the upside, a resumption of gains and a breach of 6983.75, the Feb 25 high, would instead refocus attention on key resistance and the range top at 7043.00, the Jan 28 high.

MNI COMMODITIES: Crude Steady, Precious Metals Rise As Risk Sentiment Stabilises

- Crude is little changed on the day as the market starts to stabilise while it waits for further indicators regarding the duration and impact of the conflict in the Middle East.

- WTI Apr 26 is down by 0.1% at $74.5/bbl.

- A NYT report earlier today noted that US officials are sceptical in the short term that either the US or Iran is ready for an offramp. Indeed, further reports later in the day suggested that the Iranian regime is preparing for a long war.

- The Strait of Hormuz is under wartime conditions and vessels sailing through it "could be at risk from missiles or rogue drones", Iran's IRGC said.

- A volatile bull cycle in WTI futures remains intact. The move higher this week paves the way for a climb towards $78.05 next, a Fibonacci projection, ahead of the $80.00 handle.

- The first key support to monitor is $66.74, the 20-day EMA. A pullback would allow the overbought condition to unwind.

- Meanwhile, precious metals have edged higher as risk sentiment has stabilised today and the USD index has consolidated much of the week’s prior advance.

- Spot gold is up by 0.8% at $5,131/oz, while silver has risen by 1.8% to $83.5/oz.

- For now, a short-term bullish theme in gold remains intact following recent gains, with scope for an extension towards key resistance and the bull trigger at $5,595.5, the Jan 29 high.

- Initial firm support to watch lies at $5,081.9, the 20-day EMA.

THURSDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 05/03/2026 | 0700/0800 | *** | Flash Inflation Report | |

| 05/03/2026 | 0700/0800 | *** | Flash Inflation Report | |

| 05/03/2026 | 0745/0845 | * | Industrial Production | |

| 05/03/2026 | 0800/0900 | ** | Industrial Production | |

| 05/03/2026 | 0800/0900 | ** | Unemployment | |

| 05/03/2026 | 0830/0930 | ** | S&P Global Final Italy Construction PMI | |

| 05/03/2026 | 0830/0930 | ** | S&P Global Final Germany Construction PMI | |

| 05/03/2026 | 0830/0930 | ** | S&P Global Final Eurozone Construction PMI | |

| 05/03/2026 | 0850/0950 | ECB de Guindos in Conversation at IIF European Investment Summit | ||

| 05/03/2026 | 0900/1000 | * | Retail Sales | |

| 05/03/2026 | 0930/0930 | ** | S&P Global/CIPS Construction PMI | |

| 05/03/2026 | 0930/0930 | *** | BOE Decision Making Panel | |

| 05/03/2026 | 1000/1100 | ** | EZ Retail Sales | |

| 05/03/2026 | 1000/1000 | ** | Gilt Outright Auction Result | |

| 05/03/2026 | - | National People's Congress | ||

| 05/03/2026 | 1330/0830 | ** | WASDE Weekly Import/Export | |

| 05/03/2026 | 1330/0830 | *** | Jobless Claims | |

| 05/03/2026 | 1330/0830 | ** | Import/Export Price Index | |

| 05/03/2026 | 1330/0830 | ** | Preliminary Non-Farm Productivity | |

| 05/03/2026 | 1530/1030 | ** | Natural Gas Stocks | |

| 05/03/2026 | 1630/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 05/03/2026 | 1630/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 05/03/2026 | 1700/1800 | ECB Lagarde Lecture on Global Risk | ||

| 05/03/2026 | 1815/1315 | Fed's Michelle Bowman |