COMMODITIES: Crude Steady, Precious Metals Rise As Risk Sentiment Stabilises

Mar-04 19:45

- Crude is little changed on the day as the market starts to stabilise while it waits for further indicators regarding the duration and impact of the conflict in the Middle East.

- WTI Apr 26 is down by 0.1% at $74.5/bbl.

- A NYT report earlier today noted that US officials are sceptical in the short term that either the US or Iran is ready for an offramp. Indeed, further reports later in the day suggested that the Iranian regime is preparing for a long war.

- The Strait of Hormuz is under wartime conditions and vessels sailing through it "could be at risk from missiles or rogue drones", Iran's IRGC said.

- A volatile bull cycle in WTI futures remains intact. The move higher this week paves the way for a climb towards $78.05 next, a Fibonacci projection, ahead of the $80.00 handle.

- The first key support to monitor is $66.74, the 20-day EMA. A pullback would allow the overbought condition to unwind.

- Meanwhile, precious metals have edged higher as risk sentiment has stabilised today and the USD index has consolidated much of the week’s prior advance.

- Spot gold is up by 0.8% at $5,131/oz, while silver has risen by 1.8% to $83.5/oz.

- For now, a short-term bullish theme in gold remains intact following recent gains, with scope for an extension towards key resistance and the bull trigger at $5,595.5, the Jan 29 high.

- Initial firm support to watch lies at $5,081.9, the 20-day EMA.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

LOOK AHEAD: Tuesday Data Calendar: JOLTS Report Likely Delayed, Fed Speakers

Feb-02 19:37

- US Data/Speaker Calendar (prior, estimate). All times ET

- 02/03 0800 Richmond Fed Barkin on economy (text, Q&A)

- 02/03 0940 Fed VC Bowman WSJ moderated discussion, live event

- 02/03 1000 JOLTS report likely delayed due to the US Gov shutdown

- 02/03 1130 US Tsy $90B 6W bill auction

- Source: Bloomberg Finance L.P. / MNI

USDJPY TECHS: Gains Considered Corrective For Now

Feb-02 19:30

- RES 4: 159.45 High Jan 14 and the bull trigger

- RES 3: 159.23 High Jan 23

- RES 2: 157.43 Low Jan 23

- RES 1: 155.76 50-day EMA

- PRICE: 155.54 @ 16:11 GMT Feb 2

- SUP 1: 152.10 Low Jan 27 and the bear trigger

- SUP 2: 151.98 38.2% of the Apr 22 ‘25 - Jan 14 bull cycle

- SUP 3: 151.54 Low Oct 29 ‘25

- SUP 4: 150.99 Trendline support drawn from the Apr 22 ‘25 low

Short-term trend conditions in USDJPY are unchanged and a bear cycle remains intact. However, a corrective cycle is in play and the latest recovery is allowing a recent oversold condition to unwind. Firm resistance to watch is at 155.76, the 50-day EMA. A clear break of this average would signal a possible bullish reversal. Key short-term support has been defined at 152.10, the Jan 27 low. A break would resume the recent downtrend.

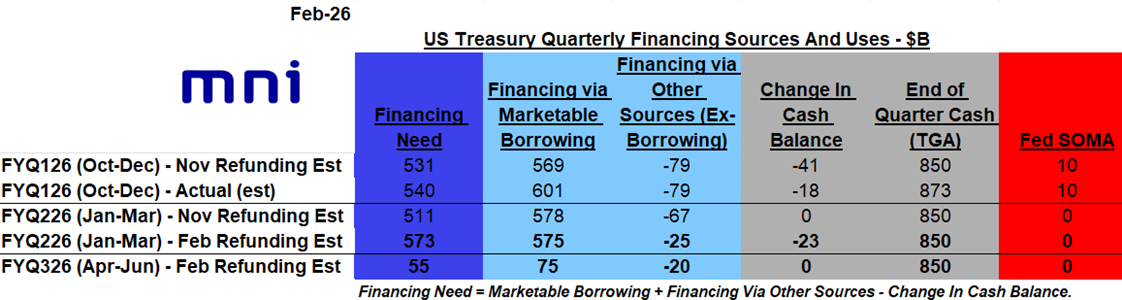

US TSYS/SUPPLY: Quarterly Financing Estimates Set To Come In Largely Steady

Feb-02 19:13

The February Refunding round starts at 1500ET today with the US Treasury’s update on financing requirements for the current (Jan-Mar) and next (Apr-Jun) quarters, at which is expected to largely maintain its borrowing projections for the current quarter.

- MNI’s expectations are in the table below. We would say that risks to our estimates are largely to the downside, i.e. Treasury expects to borrow/finance less than we have penciled in.

- Oct-Dec marketable borrowing will have been around $600B, not far from the original $569B estimate made in the November refunding round, and that is set to fall to around $575B in the Jan-Mar quarter (basically unchanged from the previous estimate; we’ve seen estimates ranging from $450-650B).

- The April-June quarter sees the lowest borrowing of the year as usual, which we estimate to come in at $75B (we’ve seen ranges from slightly negative, to over $200B).

- These figures assume that Treasury continues to target a $850B end-quarter TGA cash pile.

- Below are some sell-side expectations.

- CIBC: $640B borrowing requirement Jan-Mar, $96B Apr-Jun (assuming $850B end-quarter TGA).

- Deutsche: Net borrowing of $555B in Jan-Mar, $25B in Apr-Jun (assuming $850B cash end quarter TGA).

- Goldman Sachs: marketable borrowing of $640bn for Q1. Assuming a $850bn TGA target, for Q2 expect marketable borrowing of $290bn

- JPMorgan: $498B in marketable borrowing in Q1, $102B in Q2, assuming $850B TGA

- TD: $561bn in marketable borrowing for Q1 and $19bn in Q2. We assume a TGA target at $850bn for both quarters.

- Wells Fargo: Marketable borrowing $609B in Q1, $228B in Q2