US TSYS: Midweek Markets Calmer While Middle East Risks Remain

Mar-04 20:33

- Treasuries look to finish weaker Wednesday, 2s-10s extending lows after the bell as Pres Trump discusses the conflict with Iran from the WH, saying the US "will continue forward" and "doing well on the war front."

- TYM6 currently -8 at 112-24.5 vs. 112-23.5 low, 10Y yield +.0249 at 4.0843%. Initial technical support at 112-16+ (Low Mar 03) followed by 112-16 (50-day EMA).

- Markets continued to weigh the magnitude of risks tied to Saturday's US/Israel attack on Iran - while West Texas and Brent Crude prices traded near flat in late trade even as Iran is reported to have begun implementing an “emergency plan” to run the country under a prolonged war, semi-official Fars news reports.

- The White House has officially nominated former Fed Governor Kevin Warsh as the next Fed chair (four-year term) for when Jerome Powell’s Chair role ends in May, along with a fourteen-year Governor role. The nomination heads to the Senate but progress isn’t clear cut.

- Private payrolls rose by 63k in February, per the ADP Employment Report. This was the strongest initial reading since July 2025 and a beat vs the 50k expected, but its impact was offset by some mitigating factors that pointed to relatively subdued labor market conditions.

- Nonfarm payrolls are expected to increase 58k in February with gains coming entirely from the private sector, pulling back from a surprisingly strong January. One temporary impact known in advance was an additional 31k of striking workers over the payrolls reference period, the highest rise since late 2024. 32k workers will return in the March payrolls count.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

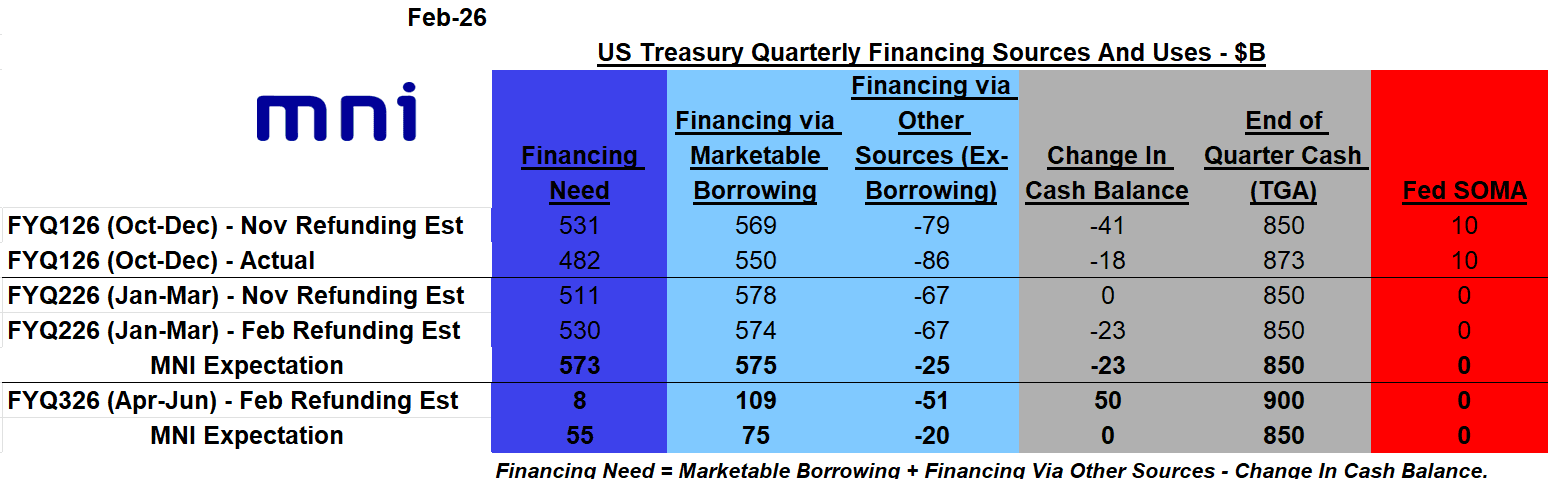

US TSYS/SUPPLY: Borrowing Ests Close To MNI Estimates, With End-FYQ3 Cash Twist

Feb-02 20:20

US Treasury publishes its latest quarterly financing estimates - see image below for sources/uses table vs the November refunding's estimates and MNI's expectations.

- For the Jan-Mar quarter, Treasury expects to borrow $574B (prior estimate was $578B; MNI's expectation was $575B) with a financing need of $530B (prior estimate was $511B; MNI's expectation was $573B, with the main difference being Treasury's estimate of non-borrowing financing which often rests on technical factors).

- For the Apr-Jun quarter, Treasury expects to borrow $109B, on financing needs of $8B. MNI had expected a borrowing estimate of $75B on a financing need of $55B.

- These are largely as expected though here was a surprise here in that Treasury targets its cash pile to rise to $900B by end FYQ3 vs the standard $850B, raising borrowing requirements by $50B than they otherwise would have been.

- This is suggestive of more bill issuance for borrowing purposes than had been expected, though Treasury doesn't explain its reasoning. It's possibly related to expectations for further Fed bill reserve management purchases though that may remain unsaid, and we await any official guidance.

US STOCKS: Late Equities Roundup: IT & Travel Shares Outperforming

Feb-02 20:19

- Stocks rebounded from early losses - drifting at or near near session highs late Monday as Consumer Discretionary and IT sector shares continued to outperform. Currently, the DJIA trades up 505.01 points (1.03%) at 49396.02, S&P E-Minis Future up 42 points (0.6%) at 7008, Nasdaq up 162.6 points (0.7%) at 23625.15.

- Leading advances in the second half include multiple hardware and semiconductor makers that rebound from last week's selling: Sandisk Corp +15.12%, Western Digital +8.90%, Intel Corp +5.94%, Seagate Technology +5.26% and Micron Technology +5.12%.

- Consumer Discretionary shares included luxury travel stocks: Carnival Corp +8.28%, Norwegian Cruise Line +7.19%, United Airlines Holdings +5.26% and Las Vegas Sands +5.16%.

- On the flipside, Energy shares led declines with crude prices off sharply (WTI -3.1 at 62.11) as middle east tensions cooled with Pres Trump's tone on Iran softening (while the carrier battle group remains in the region): EQT Corp -5.60%, Expand Energy -5.04%, ONEOK -4.17%, Diamondback Energy -3.41%, Coterra Energy -3.12% and Occidental Petroleum -3.06%.

AUDUSD TECHS: Off Last Week’s Trend High

Feb-02 20:00

- RES 4: 0.7208 61.8% of the Feb 25 ‘21 - Apr 9 ‘25 bear leg

- RES 3: 0.7158 High Feb 2 2023

- RES 2: 0.7123 2.000 proj of the Nov 21 - Dec 10 - 18 price swing

- RES 1: 0.7094 High Jan 29 ,and the bull trigger

- PRICE: 0.6963 @ 16:18 GMT Feb 2

- SUP 1: 0.6909 Intraday low

- SUP 2: 0.6835 20-day EMA

- SUP 3: 0.6727 50-day EMA

- SUP 4: 0.6660 Low Dec 31

A bull cycle in AUDUSD remains in play and last week’s gains reinforce current trend conditions. However, the latest pullback highlights the start of a corrective phase. If correct, it suggests potential for an extension towards support around the 20-day EMA, at 0.6835. This would also confirm an unwinding of the recent overbought trend condition. Key short-term resistance and the bull trigger has been defined at 0.7094, the Jan 29 high.