EQUITY TECHS: E-MINI S&P: (H6) Range Base Holds For Now

- RES 4: 7066.70 1.000 proj of the Feb 6 - 11 - 17 price swing

- RES 3: 7043.00 High Jan 28 and bull trigger

- RES 2: 6983.75 High Feb 25

- RES 1: 6908.89 50-day EMA

- PRICE: 6827.00 @ 14:50 GMT Mar 4

- SUP 1: 6751.50/6718.72 Low Feb 6 and range base / Low Mar 3

- SUP 2: 6733.00 Low Nov 25 ‘25

- SUP 3: 6691.56 76.4% retracement of the Nov 21 - Jan 28 bull leg

- SUP 4: 6583.00 Low Nov 21 ‘25 and a key medium-term support

A bearish short-term tone in S&P E-Minis remains intact. For now, the contract is trading inside a range. Attention is on the base of the range at 6751.50, the Feb 6 low. This level has been pierced, a clear break would highlight a stronger bear threat. On the upside, a resumption of gains and a breach of 6983.75, the Feb 25 high, would instead refocus attention on key resistance and the range top at 7043.00, the Jan 28 high.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

MNI: US ISM JAN MANUF PURCHASING MANAGERS INDEX 52.6

- MNI: US ISM JAN MANUF PURCHASING MANAGERS INDEX 52.6

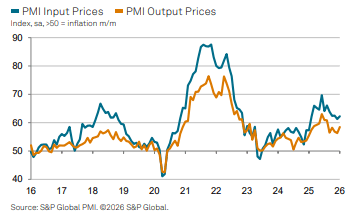

- US ISM JAN MANUF PRICES PAID INDEX 59.0

- US ISM JAN MANUF EMPLOYMENT INDEX 48.1

CROSS ASSET: USD Off Highs & E-minis Further Off Lows

Overnight weakness in e-minis further countered after the Wall St. opening bell, which helps the broader USD (BBDXY) trade away from session highs, preventing USD bulls from closing the Jan 26 opening gap lower in the index (located at 1,192.92).

- No headlines of note to flag for the initial move (final S&P global PMI revised higher in the time since), manufacturing ISM data due at 10:00 NY/15:00 London.

- Our macro team notes that the impending ISM is expected to reflect an improvement in activity indices from a surprisingly weak December, with inflation sub-metrics remaining stubbornly high.

- FOMC-dated OIS pricing pretty much bang on 50bp of easing through year-end ahead of the release, with ~80% odds of a cut priced through June and the next 25bp step fully discounted through the July FOMC, as the recovery in wider risk sentiment and (to a much lesser degree) final S&P Global PMI print helps promote some hawkish repricing on the day (’26 FOMC-dated OIS 0.5-3.0bp less dovish on the day).

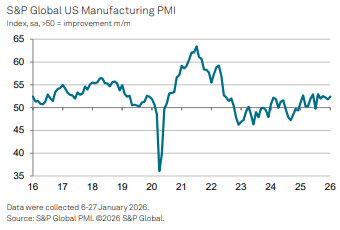

US DATA: Inventory Build Helps Surprise Upward Revision In January Mfg PMI

The S&P Global US manufacturing PMI saw a sizeable upward revision in January from 51.9 in the flash to 52.4 in the final (cons 52.0) after 51.8 in Dec, for its highest since October. The press release notes strong production but also a contribution from inventory build. Highlights from the full release (link):

- “A solid and stronger improvement in US manufacturing sector operating conditions was signaled by January’s S&P Global PMI® data amid the joint-sharpest upturn in production since May 2022.

- “However, growth was in part driven by inventory building as new orders, despite returning to expansion in January, increased only modestly.”

- “Tariffs remained a notable theme from the latest survey, driving up input costs to a greater degree and limiting demand gains, especially from international markets.”

- Output prices tell a similar story to that first reported in the flash: “Input cost inflation increased from December, while manufacturers’ own charges rose to the greatest extent since last August.”