MNI ASIA MARKETS ANALYSIS: Rate Cuts Gather Momentum Post NFP

HIGHLIGHTS

- Treasuries gapped higher following softer than expected August jobs gain (+22k vs. +75k est) Friday, while effective rates quickly projected over -70bp in rate cuts by year end.

- Chicago Fed Pres Goolsbee is "undecided" on a rate cut at next FOMC, wants "to get more information" while playing down the signal from payrolls slowdown, due to a potentially softer labor force growth dynamics.

- Stocks initially climbed to new record highs on optimism over increased rate cut pricing - but reversed course, trade weaker as focus turned back to soft labor data as market negative.

- Both the US and Canada printed weaker-than-expected jobs reports Friday, sending both the USD and CAD lower against all others in G10.

US TSYS

MNI US TSYS: Projected Rate Cut Pricing Near -75bp by Year End After Soft Jobs Data

- Treasuries look to finish broadly higher after key employ data showed less job gains than expected for August. The Fed enters communication blackout tonight.

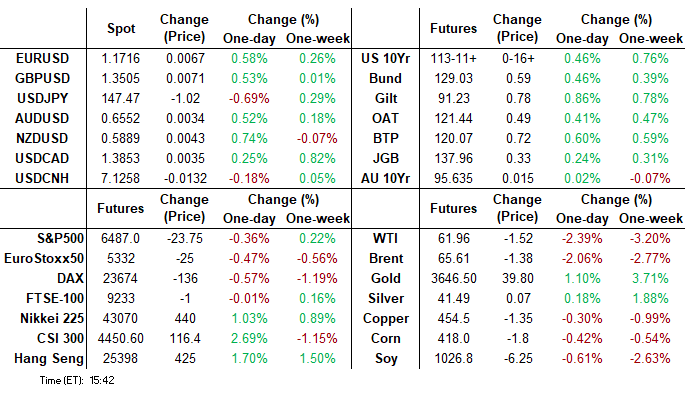

- Payrolls surprised lower in August (22k vs BBG cons 75k) and the u/e rate was on the dovish side at a new recent high of 4.324% (cons 4.3% but with a skew to a 4.2% print) after 4.25%. The downward revisions were concentrated in May (-27k vs +6k in June), offering no offset to last month’s huge downward revisions.

- Rate have gradually pared gains in the second half (TYZ5 +16.5 at 113-11.5 vs. 113-21.5 high) as markets continued to digest the labor data. Projected rate cuts remained well off pre-data (*) levels: Sep'25 at -28bp (-24.7bp), Oct'25 at -47.3bp (-38.6bp), Dec'25 at -69.7bp (-59bp), Jan'26 at -83.5bp (-71.1bp).

- Chicago Fed President Goolsbee, a 2025 FOMC voter, tells Bloomberg TV that he is "undecided" on a rate cut at the Sep 17 FOMC, saying he wants "to get more information", playing down the signal from the recent nonfarm payrolls slowdown, due to a potentially softer labor force growth dynamics. He suggests one of the things he will be looking at in the meantime is the August inflation report out next week - and in particular, whether services inflation looks tame.

- The USD fell sharply in tandem with yields, putting the USD Index to new September lows and within range of first support into the late July lows of 97.109 and the bear trigger into the July 1st print at 96.377.

- Generally slow start to next week - focus on PPI and CPI net Wed-Thu respectively.

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.41% (+0.02), volume: $2.834T

- Broad General Collateral Rate (BGCR): 4.38% (+0.02), volume: $1.131T

- Tri-Party General Collateral Rate (TCR): 4.38% (+0.02), volume: $1.108T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $118B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $231B

FED Reverse Repo Operation

RRP usage inches up to $20.997B with 15 counterparties this afternoon from $20.128B yesterday. Compares to $17.923B on Wednesday, Sep 3 - the lowest levels since early April 2021. This year's high usage of $460.731B occured on June 30.

US SOFR/TREASURY OPTION SUMMARY

SOFR & Treasury options saw decent two-way trade after this morning's jobs data, some chunky call unwinds and repositioning after underlying Tsy futures surged higher after this morning's lower than expected August employment data. Rate have gradually pared gains in the second half (TYZ5 +16.5 at 113-11.5 vs. 113-21.5 high) as markets continued to digest the labor data. Projected rate cuts remained well off pre-data (*) levels: Sep'25 at -28bp (-24.7bp), Oct'25 at -47.3bp (-38.6bp), Dec'25 at -69.7bp (-59bp), Jan'26 at -83.5bp (-71.1bp).

SOFR Options:

-10,000 0QZ5 97.00 calls, 27.5 vs. 97.135/0.60%

+20,000 SFRU5 95.81/96.06 call spds 17.0-17.25

-8,000 SFRU5 96.00/96.12 call spds 1.25-1.5 ref 95.9925

-10,000 SFRV5 96.25 calls 1.0 over 0QV5 97.12 calls

+4,000 SFRU5 95.87/96.12 call spds, 10.0

+10,000 SFRZ5 96.25/96.31/96.50/96.56 call condors, 2.25 ref 96.355

+10,000 SFRX5 96.00 puts, 1.25

over 25,000 SFRU5 96.18/96.25 call spds ref 95.925

5,600 3QU5 97.00/97.12 call spds ref 96.83

1,500 SFRU5 95.87/95.75/95.81/95.87 put condor vs. 95.87/95.93/96.00/96.06 put condor

4,500 SFRU5 95.87/95.93 call spds ref 95.9275

over 20,000 SFRU5 96.06/96.12 call spds ref 95.93

+4,000 SFRZ5 96.25/96.37/96.44/96.50 broken call condors, 3.5

10,000 SFRZ5 96.00 calls, 29.5

2,000 SFRU5 95.81/95.93 put spds vs. 95.93/96.06 call spd ref 95.93

2,500 0QU5 96.75 puts ref 96.955

1,000 2QF6 97.18/97.62/97.75 broken call flys

+2,000 0QX5 96.43/96.62/96.75/96.87 put condors, 2.5 ref 97.015

3,000 0QH6 97.00 puts vs. 97.00/97.37 call spd ref 97.08

Treasury Options:

-37,500 TYV5 113.25/114/114.75 call flys, 8 vs. 113-12.5/0.04%

Block, -40,000 TYV5 113/114/114.25/115.25 call condors, 17 ref 112-27

+29,000 109/109.25 put spds, 3 ref 109-22.25 (another 29k on screen - potential unwind)

+6,400 wk2 TY 112.25 puts, 15 vs. 112-28.5/0.30%

Block, +9,000 wk2 TY 112 puts, 10 ref 112-27

-1,000 FVV5 110.5 calls, 12.5 vs. 109-22/0.25%

-2,000 TUV5 104.12/104.37/104.62 call flys, 2.5

-2,000 FVV5 109.25/109.75 3x2 combo, 3.5 net vs. 109-21.5

over 9,400 TYV5 112.5 puts, 29-30

3,250 TYX5 110/111 put spds ref 112-30

7,450 wk2 FV 109.75 calls, 12 ref 109-21.5 to -21.75 (exp today)

8,000 wk2 FV 111 calls ref 109-21.75 to -22 (exp 9/12)

+2,000 TYV5 112.5/113.5 call over risk reversal, 6 vs. 112-27/0.77%

+40,000 TYV5 111 puts, 6 (late Thursday print)

2,000 TYV5 112.75/113.75/114 broken call trees ref 112-30.5

MNI BONDS: EGBs-GILTS CASH CLOSE: Weak US Jobs Data Helps Bull Flattening Continue

European curves bull flattened again Friday, with a downside surprise in US employment driving the rally.

- This was the third consecutive day of gains led by the long-end. While the session started constructively, ranges were relatively narrow, with weaker-than-expected German factory orders helping set a bullish tone for Bunds.

- In the UK, retail sales data were firmer-than-expected (but only due to downward revisions, which made for a marginally dovish report overall), but the big news was the resignation of deputy PM Rayner and a broader cabinet reshuffle, raising further uncertainty over the fiscal policy outlook.

- The main event of the day - the US employment report for August - showed weaker-than-expected job gains along with downward revisions and a slightly higher-than-anticipated unemployment rate, boosting Fed cut pricing and extending gains across global core curves.

- Gilts outperformed Bunds on the day. That's also true for the week: UK 2Y yield -3.3bp, 10Y -6.6bp; German 2Y yield -1.1bp, Germany -6.2bp.

- Periphery/semi-core EGB spreads were mixed on the day, with earlier tightening reversing toward the close as equities pulled back.

- Next week's highlights include Monday's expected confidence vote in the French government, and the ECB decision on Thursday.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 3.5bps at 1.929%, 5-Yr is down 5.1bps at 2.219%, 10-Yr is down 5.7bps at 2.662%, and 30-Yr is down 4bps at 3.297%.

- UK: The 2-Yr yield is down 3.9bps at 3.91%, 5-Yr is down 6.2bps at 4.048%, 10-Yr is down 7.4bps at 4.646%, and 30-Yr is down 7bps at 5.504%.

- Italian BTP spread down 0.8bps at 84.2bps / French OAT up 1bps at 78.6bps

MNI OPTIONS: Week Ends With Mixed Bund, Euribor Midcurve, And Sonia Plays

Friday's Europe rates/bond options flow included:

- RXV5 128.50/127.50/125.00 broken put fly paper paid 12 on 2.5K

- 2RZ5 97.75/98.00 call spread vs 3RZ5 97.625/97.875 call spread. Paper pays 2.5 to 2.75 in 5k, buying the 2RZ5 spread

- SFIZ5 96.30/96.55/96.80 call fly 10K given at 1.5

MNI FOREX: CAD Outdoes USD on Twin Jobs Market Weakness

- Both the US and Canada printed weaker-than-expected jobs reports Friday, sending both the USD and CAD lower against all others in G10. The US reported job gains of just 22k across August, resulting in both a higher unemployment rate as well as slower average hourly earnings. Compounding the bad news, the two-month net revision came in negative, pointing to persistent economic weakness into Q3.

- Resultantly, Fed rate cut pricing into year-end firmed aggressively. Markets added close to half a 25bps rate cut by for the December 2025 meeting, making 3x25bps rate cuts more likely than not. The USD fell sharply in tandem, putting the USD Index to new September lows and within range of first support into the late July lows of 97.109 and the bear trigger into the July 1st print at 96.377.

- We noted earlier Friday that the deterioration of the USD net position had stalled over Summer (potentially triggered by fragile European, UK politics), but today's payrolls number may provide the impetus for fresh shorts - a lacking driver since the post-tariffs downleg.

- CAD/JPY broke to new September lows and is now testing the 200-dma of 106.12 on the poor Canadian jobs numbers. The net change in employment dropped 65k, led by part-time employment and making for a new post-COVID high unemployment rate. Markets saw little reprieve in Carney detailing an extension of loan programmes for companies hit by US tariffs.

- Focus for the coming week shifts to the LDP meeting in Japan, at which party members will determine whether to trigger an early leadership election against PM Ishiba, which may introduce further political uncertainty. USD/JPY traded through the 50-dma into the Friday close, as the JPY benefited from a return lower for US stock markets.

- A busy week for US data next week, as both CPI and PPI prints are set to further inform the Fed's views on policy. CPI is expected to re-accelerate to 2.9% from 2.7% - complicating the policy mix as the central bank come under further scrutiny from the White House. Treasury Secretary Bessent called for an independent review into the Bank, which he sees as having lost public trust and credibility.

- The ECB rate decision is also due, at which markets expect little change on headline policy. EUR/GBP remains inside a nascent short-term uptrend, with 0.8713 representing the first upside trigger.

MNI OPTIONS: Expiries for Sep08 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1600(E1.2bln), $1.1620-30(E1.0bln), $1.1690-00(E1.3bln), $1.1750(E1.2bln), $1.1835(E873mln)

- USD/JPY: Y146.00($1.1bln), Y146.45-55($945mln)

- USD/CAD: C$1.4000($517mln)

MNI US STOCKS: Remain Off Early Highs, Banks & Energy Shares Underperforming

- Major indexes retreated early Friday after climbing to new record highs following the lower than expected August employment data. While the soft data initially spurred buying on hopes of increased rate cuts by year end, focus quickly shifted back to the data being market negative.

- While effective funds did project a -25bp cut at the September 17 FOMC (and nearly -75bp by year end), officials are less convinced. Chicago Fed President Goolsbee stated on Bbg TV he is "undecided" on a rate cut at the September FOMC, saying he wants "to get more information" while playing down the signal from the recent nonfarm payrolls due to a potentially softer labor force growth dynamics.

- Currently, the DJIA trades down down 247.99 points (-0.54%) at 45372.09 (*45770.20 high), S&P E-Minis down 33 points (-0.51%) at 6478.0 (*6541.75 high), Nasdaq down 47.5 points (-0.2%) at 21660.14 (*21878.81 high).

- A combination of Financials, Energy and Industrials sector shares continued to lead decliners in the second half. Banks and services weighed on the former: Interactive Brokers Group -6.07%, Charles Schwab -5.82%, Ameriprise Financial -4.51% and Raymond James Financial -4.20%.

- Weaker Energy and Industrial sectors partially tied to a late week decline in crude (WTI -1.70 at 61.78) weighed down by: Diamondback Energy -3.57%, ConocoPhillips -3.49%, Fastenal -5.29%, GE Vernova -2.86% and CH Robinson Worldwide -2.80%.

- One negative standout that carried through to the second half: Lululemon fell appr 18.25% on downgrades and guidance cuts. Information Technology sector shares traded mixed: Broadcom +10.42%, Enphase Energy +7.17%, Micron Technology +3.60% and Oracle +3.40%. On the flipside: Advanced Micro Devices -6.45%, NVIDIA Corp -3.18% and Microsoft Corp -2.93%.

- On the positive side, Real Estate and Materials sectors outperformed in the first half, the former buoyed by: Weyerhaeuser +2.19%, SBA Communications +1.94%, American Tower Corp +1.90% and Public Storage +1.82%. Leading gainers in the Materials sector included: Albemarle Corp +2.56%, Sherwin-Williams +2.52%, Newmont Corp +2.27% and Steel Dynamics +1.94%.

MNI EQUITY TECHS: E-MINI S&P: (U5) Fresh Cycle High

- RES 4: 6600.00 Round number resistance

- RES 3: 6585.83 2.0% 10-dma envelope

- RES 2: 6543.75 2.00 proj of the Apr 7 - 10 - 21 price swing

- RES 1: 6541.75 Intraday high

- PRICE: 6480.50 @ 1435 ET Sep 5

- SUP 1: 6447.06/6371.75 20-day EMA / Low Sep 2

- SUP 2: 6347.53 50-day EMA

- SUP 3: 6313.25 Low Aug 6

- SUP 4: 6239.50 Low Aug 1 and a key support

A bull cycle in S&P E-Minis remains intact and the latest pullback has once again proved to be a shallow correction. The contract has traded to a fresh cycle high, breaching the Aug 28 high of 6523.00. This confirms a resumption of the uptrend and maintains the price sequence of higher highs and higher lows. Sights are on 6543.75 next, a Fibonacci projection. Initial support to watch is 6447.06, the 20-day EMA.

COMMODITIES

MNI AMERICAS OIL: Americas End of Day Oil Summary: Crude Lower

Crude has fallen further today and is on track for a net decline on the week amid concerns that this weekend's OPEC+ meeting could result in further supply. US total rigs 537 as of Sep 5, oil rigs up 2 to 414. Canadian rigs rose by 6 to 181; oil rigs were up 3 to 123.

- Bloomberg report that Saudi Arabia wants to consider reviving another tranche of 1.66m b/d of halted supplies at the Sunday meeting.

- Russia’s Deputy PM Novak said that OPEC+ is not currently discussing a hike and that OPEC+ will look at the situation as a whole before making a decision at the meeting on Sunday.

- Bloomberg’s Javier Blas said a supply increase seems more likely to be approved when the full OPEC group meets in October/November, rather than on Sunday.

- President Donald Trump yesterday warned of consequences for Russia if President Vladimir Putin doesn't agree to a meeting with Ukrainian President Volodymyr Zelenskyy. He also pushed European leaders to stop purchases of Russian oil.

- WTI Oct futures were down 2.5% at $61.87

- WTI Nov futures were down 2.5% at $61.46

MONDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 08/09/2025 | 0500/1400 | Economy Watcher's Survey | ||

| 08/09/2025 | 0600/0800 | ** | Trade Balance | |

| 08/09/2025 | 0600/0800 | ** | Industrial Production | |

| 08/09/2025 | - | *** | Trade | |

| 08/09/2025 | 1500/1100 | ** | NY Fed Survey of Consumer Expectations | |

| 08/09/2025 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 08/09/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 08/09/2025 | 1900/1500 | * | Consumer Credit | |

| 09/09/2025 | 2301/0001 | * | BRC-KPMG Shop Sales Monitor |