MNI ASIA MARKETS ANALYSIS - Post-Downgrade Comeback

MNI (NEW YORK) - Highlights:

- Treasuries And Equities recover from losses post-Moody's downgrade of the US's AAA credit rating

- Fed officials sent their clearest signals yet that they weren't considering a rate cut until after summer

- The RBA decision announcemen is in focus Tuesday with a 25bp cut expected

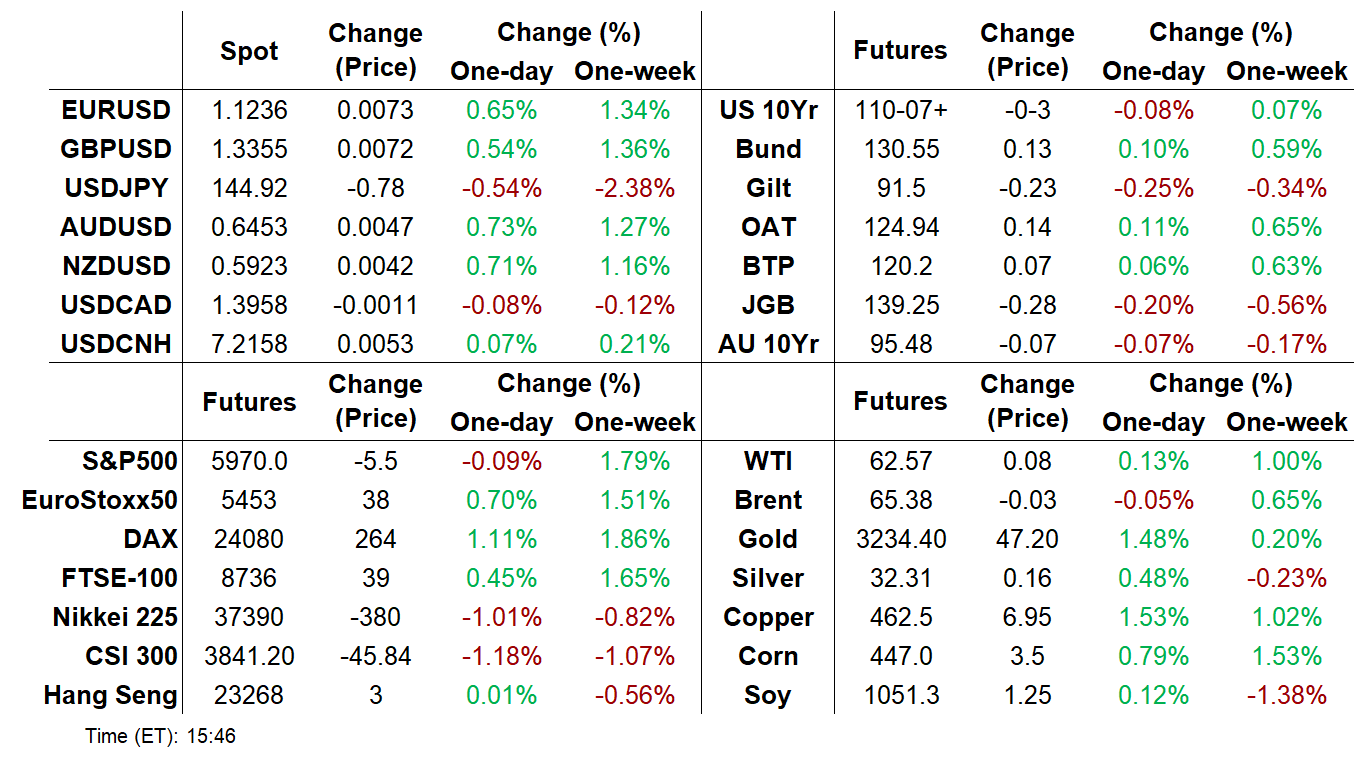

US TSYS: 30Y Holds 5% Level Amid Broad Post-Downgrade Rally

Treasuries recovered from early weakness to close flat/stronger Monday, with bull steepening in the curve.

- Following on from Friday's post-close surprise downgrade of the US's AAA credit rating by Moody's, yields rose sharply in the early going.

- While over the weekend White House officials shrugged off Moody's decision, there was significant attention on the apparently deteriorating fiscal trajectory overnight as House Republicans cleared a procedural hurdle to get the "Big, Beautiful" tax bill closer to completion.

- 30Y yields notably touched their highest since Nov 1 2023 (5.0353%) - up 13.5bp from Friday's ratings downgrade announcement - before an impressive reversal lower on the day (just 1+bp up from pre-downgrade).

- Despite little in the way of headline catalysts - China expressed displeasure with the US's guidance against the use of some Huawei chips, bringing a brief risk-off reaction - Treasuries rallied alongside equities for the rest of the session (the TY upturn started with the equity cash open).

- We heard from multiple Fed speakers, including Bostic, Jefferson, Williams, and Kashkari, all of whom reiterated the FOMC's patient approach on cuts amid economic uncertainty, and Williams and Bostic in particular suggesting that the next cut wouldn't seriously be contemplated until after the summer. Reaction was limited however given the market's already-low implied probability of a cut before September.

- Data was relatively thin - Conference Board leading economic index had its sharpest drop since 2023 but avoided an outright recession signal.

- Latest levels: the 2-Yr yield is down 3.1bps at 3.9681%, 5-Yr is down 3.2bps at 4.0611%, 10-Yr is down 2.2bps at 4.4553%, and 30-Yr is down 2.6bps at 4.9183%.

- Jun 10-Yr futures (TY) down 2.5/32 at 110-08 (L: 109-20 / H: 110-09)

- Tuesday's schedule includes the Philly Fed nonmanufacturing survey along with another slew of Fed speakers, including Collins, Barkin, Musalem, Kugler, Hammack and Daly.

MNI RBA Preview-May 2025: 25bp Cut, Will CPI Reach 2.5%?

- The RBA decision is announced on May 20 and a 25bp rate cut to 3.85% is widely expected (31/33 analysts on Bloomberg are forecasting -25bp with two expecting -50bp) after Q1 trimmed mean CPI fell within the 2-3% target band with activity, especially consumption, remaining lacklustre.

- The economy has broadly developed in line with the RBA's February expectations and thus forecast revisions this month are likely to be minimal.

- After stronger-than-expected Q1 wages and April employment data, the central bank is likely to retain its cautious tone though regarding the data-dependence of future easing and reiterate that uncertainty is very high.

- RBA-dated OIS pricing has a 95% probability of a 25bp rate cut in May, with a cumulative 75bps of easing priced by year-end.

FED: FOMC Officials Appear To Defer Next Cut Decision To Post-Summer

NY Fed President WIlliams and Fed Governor Jefferson - both permanent FOMC voters - on Monday reiterated a desire to be patient on cutting rates. Williams was even more explicit than usual in offering a rough timetable, with broader FOMC communications continuing to suggest that a cut before the end of summer is not in the frame.

- Williams appeared to put a timeframe on when the Fed would have sufficient clarity to decide on rates: "It's not going to be that in June, we're going to understand what's happening, or July... it's going to be a process of collecting data, getting a better picture, and watching those things develop."

- This follows Atlanta's Bostic this morning saying "I think we’ll have to wait three to six months to start to see where this settles out" (he sees just 1 cut this year), and recall last month Gov Waller - who may be the biggest dove on the Committee - also said that we won't see the tariffs in the hard data "until July" given the April 2 tariffs have been postponed. Indeed the other biggest dove on the FOMC (and a 2025 voter), Chicago's Goolsbee, suggested that uncertainty may actually have grown as a result of the latest tariff climbdown and the bar to cuts remains high.

- This would seem to align with current market pricing: there's under 10% probability implied of a June cut, with under 40% cumulative through July - and even a cut by September is not quite a 100% proposition (closer to 90%).

- It also brings September's FOMC meeting back into focus as has been the case in previous years, including September 2024 when the Fed kicked off the easing cycle. The late August Jackson Hole Fed symposium will likely remain a key focus in setting the stage.

- Both Jefferson and Williams said policy is in a "good place" (Jefferson said it was in a "very" good place), with both eyeing risks from tariffs to both sides of the dual mandate with potential for slower growth and upped inflation. Williams called policy "slightly restrictive" (earlier this month he similarly categorized policy as "modestly restrictive").

- Jefferson's key comments: “I believe it’s important that monetary policy make sure that any increase in the price level is not converted into a sustained increase in inflation...We’re going to keep our policy in a position to keep expectations anchored, and we’re going to wait and see the eventual impact of the totality of policies... given the level of uncertainty that we’re facing right now, I believe that it is appropriate that we wait and see how the policies evolve over time and their impact."

INFLATION: Expectations Anchored In US & EU, But With Opposing Forces [1/2]

- US market-based inflation expectations remain a story of one where short-term elevated expectations on the back of US tariff policy aren’t spilling over to longer duration measures, even when comparing just 1Y vs 1Y1Y metrics (left chart).

- 1Y inflation swaps have been helped lower by last week’s de-escalation in China-US trade policy, and at 3.24% today are below the 3.25% seen the day before Apr 2 Liberation Day announcements. They are however still elevated by the standards of the past two and a half years having pushed higher ahead of reciprocal tariffs.

- In contrast, the 1Y1Y inflation swap of 2.525% is back at Apr 1 levels. That’s high compared to pre-pandemic levels averaging closer to 2% but it’s very much in line with recent averages away from the 2021-22 peak of the post-pandemic inflation episode.

- With FOMC participants frequently talking on the need to keep inflation expectations anchored, this should continue to please them.

- Looking cross country, the opposite is true in Europe where negative near-term growth implications of US trade policy are deemed most acute.

- 1Y EUR inflation swaps at 1.43% are ~25bp lower than pre-Liberation Day levels and ~50bp lower than late March levels (right chart). The 1Y1Y at 1.75% meanwhile is 12bp and 14bp lower respectively.

INFLATION: Expectations Anchored In US & EU, But With Opposing Forces [2/2]

- Much of the EU and German fiscal push over the past two and a half months has been in defense spending and infrastructure investment with longer-term horizons.

- There have been increasing question marks over the extent to which this fiscal support will be inflationary, with 5Y5Y EUR CPI swaps holding most of the reversal from their initial spike higher on the early March announcements. Indeed, US-EU inflation swap differentials have at +38bps have fully reversed the initial drop to as low as +17bps.

EGBs-GILTS CASH CLOSE: Bunds Outperform In Broader Intraday Recovery

European curve steepened Monday, with Bunds outperforming Gilts.

- Global core FI was under some pressure coming out of the weekend, catching up to Friday's post-close downgrade of the US's AAA credit rating by Moody's.

- With headline and data flow relatively light for the most part Monday, the recovery in Treasuries that started roughly with the US equity open led a rally in Europe.

- One flashpoint that saw yields continue lower was China's statement that the recent U.S. guidance warning against the use of Huawei’s chips undermines the recent trade entente.

- The EC lowered growth projections, while final HICP pointed to the April uptick in services inflation as being largely a calendar effect.

- The German curve bull steepened, with the UK's bear steepening.

- Periphery spreads were mixed. PGBs closed flat to Bunds after the centre-right AD-PSD/CDS Coalition of PM Luis Montenegro, in line with expectations, emerged as the largest party following the 18 May legislative election.

- Tuesday's data schedule includes eurozone consumer confidence. BoE hawkish dissenter Pill is due to deliver comments on his monetary policy views, while ECB speakers include Wunsch, Knot and Cipollone.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 1.2bps at 1.843%, 5-Yr is down 0.6bps at 2.149%, 10-Yr is down 0.2bps at 2.588%, and 30-Yr is down 0.2bps at 3.038%.

- UK: The 2-Yr yield is up 0.2bps at 4.007%, 5-Yr is up 1.1bps at 4.157%, 10-Yr is up 1.5bps at 4.664%, and 30-Yr is up 2.5bps at 5.419%.

- Italian BTP spread up 0.3bps at 100.9bps / Portuguese PGB spread down 0.1bps at 50.3bps

EUROPE OPTIONS: Plenty Of Call Structure Trade In Sonia Ahead Of UK CPI This Week

Monday's Europe rates/bond options flow included:

- OEM5 116.00/117.75/117.25/118.75 put condor vs. 120.00/121.50 call spread, paper sells the put condor, buys the call spread for 32 on 13.5K.

- RXN5 132.00/133.50 call spread paper paid 20 on 3K

- SFIM5 95.90/96.00/96.10 call fly, paper pays 1 for 5k

- SFIU5 96.15/96.35/96.55 call fly paper paid 2.75 on 5K

- SFIU5 96.00/96.10 call spread sold at 5 in 8k

- SFIZ5 96.20/96.30 call spread vs. SFIZ5 95.75 puts, paper bought the call spread to sell the puts, paying 0.5 on 4K.

FX OPTIONS: Expiries for May20 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1015(E1.1bln), $1.1070-75(E1.8bln), $1.1100-05(E780mln), $1.1195-00(E1.5bln), $1.1245-50(E1.2bln), $1.1300(E1.1bln)

- USD/JPY: Y145.00($795mln), Y145.50($1.0bln), Y146.00($621mln)

- USD/CAD: C$1.3900-15($807mln)

US STOCKS: S&P Futures Reverse Moody’s Hit With Dip Buying, 6000 Next Resistance

- ESM5 has hit highs of 5986.75 to push above Friday’s high of 5977.50 seen an hour ahead of the Moody’s US downgrade, via an overnight low of 5892.75.

- Next up is the round 6000 after which lies 6057.00 (Mar 3 high). Support at 5837.25 (Mar 25 high) wasn’t troubled overnight.

- Within the S&P 500, health care (+0.7%, led by UnitedHealth +7.4%), consumer staples (+0.4%) and materials (+0.3%) lead.

- Within consumer staples, Walmart has pared losses to -0.1% after an intraday recovery of 2.5%. Trump said Saturday: “Walmart should STOP trying to blame Tariffs as the reason for raising prices throughout the chain” and that it should "EAT THE TARIFFS", adding, "I'll be watching”.

- Losses are seen in energy (-1.5% despite WTI +0.8%) and consumer discretionary (-0.2%).

- Apple (-1.3%) and Tesla (-2.9%) weigh on IT and consumer discretionary. App Store legal discussions and Alphabet-linked revenues are in focus for the former.

- E-mini summary; S&P 500 (+0.1%), Nasdaq 100 (+0.1%), Dow Jones (+0.4%) and Russell 2000 (-0.6%)

EQUITY TECHS: E-MINI S&P: (M5) Trend Needle Points North

- RES 4: 6080.75 High Feb 26

- RES 3: 6057.00 High Mar 3

- RES 2: 6000.00 Round number resistance

- RES 1: 5977.50 High MAy 16

- PRICE: 5916.75 @ 07:25 BST May 19

- SUP 1: 5681.27 50-day EMA

- SUP 2: 5455.50 Low Apr 30

- SUP 3: 5355.25 Low Apr 24

- SUP 4: 5127.25 Low Apr 21 and a key support

A bullish trend condition in S&P E-Minis remains intact and last week’s appreciation reinforces current conditions. The contract has cleared an important resistance at 5837.25, the Mar 25 high and a bull trigger. This strengthens the bullish theme, paving the way for a continuation near-term. Sights are on the 6000.00 handle next. Initial firm support to watch lies at 5681.27, the 50-day EMA.

FOREX: USD Dip Stabilises, RBA Policy Statement Key

- Headed through the European close, the greenback is holding the bulk of the day's losses having backtracked around 0.5% on the back of the Moody's downgrade late on Friday. Through APAC hours, JPY and CHF were the original outperformers, but a notable step higher in EGB/Gilt yields, a general steepening of the curve hindered progress and outperformance switched to EUR and GBP into the NY crossover.

- The RBA rate decision is a focus Tuesday. The Bank are expected to cut rates a further 25bps to 3.85%, but AUD/USD's range trade since the beginning of the month signals a market with little concern over easier policy. The policy statement will be watched carefully as markets priced a further 2 x 25bps cuts beyond assumed easing tomorrow, despite tariff uncertainty and the prospect of further stimulus from China.

- Canadian CPI for April is due Tuesday, ahead of which USD/CAD remains in a consolidation pattern after correcting higher to trade either side of 1.40. 1.4022 marks notable resistance ahead, the 200-dma, above which markets trade the best levels since mid-April. The 50-dma will imminently form a death cross, indicating strong short-term downward momentum.

- GBP/USD traded as high as 1.3404 through the initial phase of USD sales this morning, but has backtracked to clock only a ~75 pip gain on the day. CPI stats on Wednesday should prove pivotal here as the BoE's MPC remain divided on near-term rates strategy without hard data on wages through April.

| Date | GMT/Local | Impact | Country | Event |

| 20/05/2025 | 0430/1430 | *** | RBA Rate Decision | |

| 20/05/2025 | 0600/0800 | ** | PPI | |

| 20/05/2025 | 0800/1000 | ** | EZ Current Account | |

| 20/05/2025 | 0800/0900 | BOE's Pill At Barclays Briefing | ||

| 20/05/2025 | 0900/1100 | ** | Construction Production | |

| 20/05/2025 | 1000/1200 | ECB's Cipollone pre-rec video at Sustainability Festival | ||

| 20/05/2025 | - | ECB's Lagarde and Cipollone at G7 Meeting | ||

| 20/05/2025 | 1230/0830 | *** | CPI | |

| 20/05/2025 | 1230/0830 | ** | Philadelphia Fed Nonmanufacturing Index | |

| 20/05/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 20/05/2025 | 1300/0900 | Richmond Fed's Tom Barkin | ||

| 20/05/2025 | 1400/1600 | ** | Consumer Confidence Indicator (p) | |

| 20/05/2025 | 2100/1700 | Fed Governor Adriana Kugler |