MNI ASIA MARKETS ANALYSIS: Nasdaq New Highs, Focus on the FOMC

HIGHLIGHTS

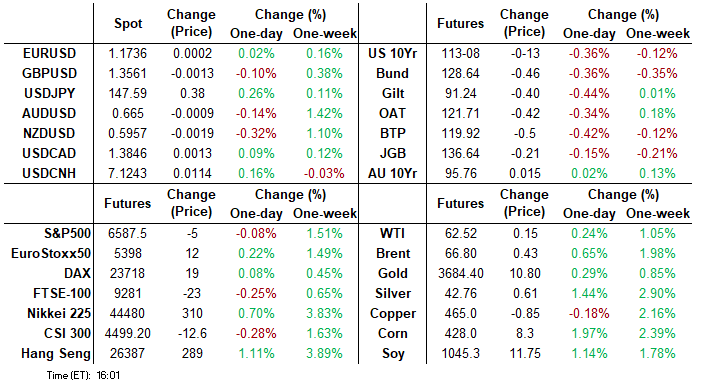

- Treasuries more than reversed the prior session's post-weekly claims/CPI related rally Friday, Dec'25 10Y futures briefly traded through Wednesday's low of 113-05 before drifting back to 113-07 in the second half.

- Little reaction to UoM data - sentiment lower than expected, 1Y inflation steady while 5-10Y inflation expectation rises, with Treasuries taking cues from lower EGBs into the European close

- Rates drifted off lows in the second half as participants set sights on next Wednesday's FOMC policy announcement, effective funds rate pricing in a 25bp cut with near two more by year end.

- The tech-heavy Nasdaq extending record highs in the second half while the DJIA continues to retreat from Thursday's record high of 46,137.20.

US TSYS

MNI US TSYS: Treasury Yields Rise, Focus on FOMC Rate Decision Next Week

- Treasuries look to finish lower Friday, off lows after tracking a decline in German Bunds heading into the European close. Rates held near lows (TYZ5 113-08) after UoM data - a muted reaction to lower than expected sentiment, 1Y inflation steady while 5-10Y inflation expectation rose: 3.9% (cons 3.4) in Sep prelim after 3.5% in Aug.

- Previously, such an upside for long-term inflation expectations would have sparked a market reaction but not this time. We suspect that’s after August and less so July preliminary readings were marked lower in the final.

- Consumer sentiment surprised lower in the U.Michigan preliminary September report, at 55.4 (cons 58) after 58.2 in Aug. The press release (https://www.sca.isr.umich.edu/) notes more pronounced easing in lower and middle income consumers along with unprompted comments about tariffs.

- Currently, the Dec'25 10Y trades -12 at 113-09 (yld 4.0586% +.0380) vs. 113-04 low - briefly testing initial technical support at 113-05.5/112-215 (Low Sep 10 / 20-day EMA); resistance above at 113-29 (High Sep 5). Curves are mixed: 2s10s +2.595 at 49.879, 5s30s -.898 at 104.744.

- USD fades slightly on the back of the weaker headline - stalling the fade in EUR/USD through early US hours. GBP/USD similarly improves, rising back above 1.3550 to 1.3564.

- Focus in the coming week shifts to the Fed rate decision. A 25bps rate cut remains fully priced, with not insignificant pricing for a 50bps step. This week's inflation data endorsed easing at this juncture, but there remains uncertainty around the magnitude of this rate cut step. Either way, the FOMC will be well aware of the scrutiny over their decision in the Oval Office.

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.41% (+0.02), volume: $2.828T

- Broad General Collateral Rate (BGCR): 4.38% (+0.01), volume: $1.147T

- Tri-Party General Collateral Rate (TCR): 4.38% (+0.01), volume: $1.120T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $117B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $214B

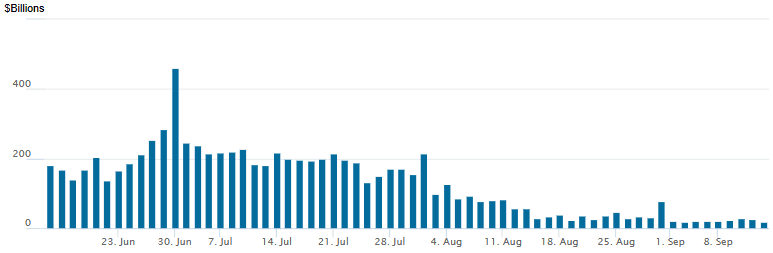

FED Reverse Repo Operation

RRP usage retreats to new lowest levels since early April 2021: $17.331B with 16 counterparties this afternoon from $26.897B Thursday. Compares to prior low of $17.923B on Wednesday, Sep 3. This year's high usage of $460.731B occurred on June 30.

US SOFR/TREASURY OPTION SUMMARY

SOFR & Treasury options turned mixed Friday, aside from unwinding Sep options that expire today, SOFR options leaned toward downside put structures while Treasury options included some large 10Y call unwinds. Underlying futures look to finish off lows after completely unwinding yesterday's post data rally. Projected rate cut pricing has consolidated vs. morning levels (*): Sep'25 at -26.5bp (-26.8bp), Oct'25 at -47.8bp (-48.8bp), Dec'25 at -70.3bp (-71.2bp), Jan'26 at -83.3bp (-84.3bp).

SOFR Options: (Sep'25 options expire today)

+6,000 0QV5 97.25/97.50 call spds, 2.75

+10,000 SFRZ5 95.81/95.93/96.06 put flys, 0.75

3,000 SFRZ5 95.50/95.87 put spds ref 96.37

+6,000 SFRV5 96.50/96.62 call spds, 1.5 vs. 96.395/0.05%

+/-8,000 SFRU5 96.00 combo - unwind

+2,500 SFRZ5 95.87/96.00 put spds, 0.5

+8,000 SFRX5 95.93/96.06/96.18 put flys, 1.5 ref 96.37

+6,000 SFRZ5 96.25/96.37/96.50 put trees, 2.75 ref 96.365

-1,500 SFRV5 96.31 straddles, 13.0 ref 96.365

-2,000 SFRZ5 95.87/96.00 2x1 put spds w/ SFRZ5 95.81/95.93/96.06 put trees, 1.25

Block, 5,000 0QZ5 97.56 calls, 4.5 ref 97.08

4,000 SFRV5 96.37/96.50 call spds ref 96.37

5,000 SFRV5 96.50/96.62/96.75 call flys ref 96.37

4,150 SFRV5 96.62 calls ref 96.37 to -.375

5,000 0QH6 97.50 calls ref 97.07

-2,000 SFRH6 96.37 puts, 8.5 vs. 96.60/0.31%

3,460 SFRZ5 96.00/96.12/96.25/96.37 call condors, 3.25

+2,000 SFRV5 96.43/96.50 call spds, 1.5 ref 96.375

2,000 SFRZ5 95.75/95.87/96.00/96.18 broken put condors, 2.5 ref 96.375

4,500 SFRZ5 96.50/96.62 call spds ref 96.375

20,000 0QZ5 97.31 calls vs. 2QZ5 97.25/97.75 call spds, 3.5

Block/screen, over -31,000 SFRU5 96.00/96.12/96.25 call flys, 0.0 ref 95.9875

Treasury Options:

5,000 TYV5 111 puts, 16 ref 113-08

2,700 FVV5 108/108.5/109 put flys ref 109-23.5

-40,000 TYV5 114.25 calls, 7

+5,000 TYZ5 111 puts, 16

5,000 TYV5 114.5/115 call spds, 3 ref 113-11.5

4,170 USX5 115/120 strangles, 127

1,200 FVV5 109/109.25 put spds ref 109-22.75

over 3,400 TYV5 111.5 puts ref 113-14.5

over 9,600 wk2 TY 113.75 calls ref 113-14 (exp today)

over 7,300 wk2 TY 113.5 calls, 4 last ref 113-13.5

5,500 TYV5 112.5 puts, 7 last

+2,000 TYV5 112.75 puts, 11 ref 113-12.5

+3,000 TYV5 113 puts, 16 red 113-12.5

2,000 FVV5 109.25/109.5 2x1 put spds

MNI BONDS: EGBs-GILTS CASH CLOSE: Soft Close Cements Bear Flattening For The Week

Gilts underperformed Bunds across respective curves Friday.

- Gilts picked up where Bunds left off post-ECB with some bear flattening early, with oil prices ticking up and BOE/TNS inflation expectations coming in on the high side (UK GDP data was largely in line but brought little reaction).

- BTPs underperformed across periphery/semi-core EGBs, but OATs lead a selloff in afternoon trade, amid concerns about a possible ratings downgrade from Fitch after the cash close.

- Final inflation data for France / Spain / Germany was uneventful. Multiple ECB speakers appearing Friday didn't have much market impact, largely echoing Thursday's hawkish-leaning tone from Lagarde (with the usual exception of Villeroy).

- For the week, there was bear flattening in both the UK (2Y +7.4bp, 10Y +2.5bp) and German (2Y +8.9bp, 10Y +5.3bp) curves.

- UK developments highlight next week's calendar, including labour market and inflation data, and the BOE meeting.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 3.2bps at 2.018%, 5-Yr is up 5bps at 2.307%, 10-Yr is up 5.8bps at 2.715%, and 30-Yr is up 4.3bps at 3.298%.

- UK: The 2-Yr yield is up 5.3bps at 3.984%, 5-Yr is up 5.3bps at 4.096%, 10-Yr is up 6.5bps at 4.671%, and 30-Yr is up 5.8bps at 5.496%.

- Italian BTP spread up 1.3bps at 80.8bps / French OAT up 0.5bps at 79.3bps

MNI OPTIONS: Upside Plays Bought In Euribor After Hawkish-Leaning ECB

Friday's Europe rates/bond options flow included:

- DUZ5 107.30/107.50 call spread paper paid 2.75 on 10K

- ERU5 98.00 calls paper paid 0.5 on 15K all day

- ERZ5 98.06/98.18 call spread vs. 98.00 puts, paper paid -2.0 for the call spread on 5K

- ERZ5 98.0625/97.9375/97.8125 put fly 5K given at 7.5

- ERH6 98.25/98.50^^ paper paid up to 25 on 10K vs. ERM6 98.375/98.25/97.9375 put ladder 8K sold down to 5.75

- ERM6 98.25/98.37 call spread paper paid 2.0 on 15K

- ERU6 98.125/98.375/98.50/98.75 call condor, paper sells for 4-4.25 in 9k

MNI FOREX: USD Rally Backed Up by Yields, But Conviction Low into Fed Meeting

- The USD rallied against all others Friday as markets backtracked a small part of the spell of weakness that followed Thursday's weekly jobless claims print. While equity markets were generally stable outside of a phase of selling through the European open, Treasuries faltered throughout Friday trade, providing a further tailwind to the greenback.

- That said, EUR/USD weakness failed to make any headway back below the 1.1700 handle as markets saw the first ECB governing council members speak after the Thursday rate decision. The divide among the council was clear, with Villeroy raising the possibility of further easing measures ahead, while both Kazaks and Simkus were less convictive in their approach.

- USD/JPY rallied well, while EUR/JPY remained inside the broader uptrend. A Kyodo news poll showed Thatcherite MP Takaichi leading opinion polling for the leadership race in the LDP (and thereby next PM of Japan). Her well known stance for fiscal spending as well as her recent criticism of the BoJ's rate hiking plans worked against the currency, keeping resistance into 173.91-97 intact for the EUR/JPY cross.

- Focus in the coming week shifts to the Fed rate decision. A 25bps rate cut remains fully priced, with not insignificant pricing for a 50bps step. This week's inflation data endorsed easing at this juncture, but there remains uncertainty around the magnitude of this rate cut step. Either way, the FOMC will be well aware of the scrutiny over their decision in the Oval Office.

- Outside of the Fed decision, UK inflation data and the Bank of England rate decision cross. Markets expect CPI to remain stubborn - keeping the MPC on hold into year-end. Just 9bps of easing are now priced through December, a series low, which is helping GBP/USD hold above the 1.35 handle. Horizontal resistance is seen layered between 1.3590-00, clearance above which will conclude the early September corrective move lower.

MNI OPTIONS: Expiries for Sep15 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1650(E794mln), $1.1690-10(E1.7bln), $1.1750(E548mln), $1.1800(E731mln)

- USD/JPY: Y147.70($501mln), Y150.00($1.0bln)

- GBP/USD: $1.3500(Gbp776mln)

- USD/CAD: C$1.3500($899mln)

MNI US STOCKS: Late Equities Roundup: Nasdaq Extends Record Highs

- Major US equity indexes continued to trade near steady (SPX eminis) to mixed late Friday, the tech-heavy Nasdaq extending record highs in the second half while the DJIA continues to retreat from Thursday's record high of 46,137.20.

- A relatively subdued end to the week as traders set their sights on next Wednesday's FOMC policy announcement.

- Currently, the DJIA trades down 161.78 points (-0.35%) at 45946.34, S&P E-Minis up 8.25 points (0.13%) at 6600.75, Nasdaq up 115.4 points (0.5%) at 22158.36 vs. 22164.01 high.

- A mix of Communication Services, Information Technology and Consumer Discretionary sector shares continued to lead gainers in the second half: Warner Bros Discovery +17.53% amid ongoing buyout chatter from Paramount Skydance which itself was up +5.96%.

- Separately: Tesla +6.93%, Micron Technology +4.35%, NRG Energy +3.50%, Super Micro Computer +3.3%, Palantir Technologies +3.74% and Corning +2.04%.

- On the flipside, Materials, Financials and Health Care sector shares led decliners: Moderna -7.76%, Incyte -3.75%, Fair Isaac -3.67%, Charles River Laboratories -3.66%, Pfizer -3.66%, F5 Inc -3.45%, Bio-Techne -3.42% and Freeport-McMoRan -3.42%.

MNI EQUITY TECHS: E-MINI S&P: (U5) Fresh Cycle High

- RES 4: 6706.00 2.236 proj of the Apr 7 - 10 - 21 price swing

- RES 3: 6673.37 2.236 proj of the May 23 - Jun 11 - 23 price swing

- RES 2: 6633.42 2.0% 10-dma envelope

- RES 1: 6600.00/6606.00 Round number resistance, intraday high

- PRICE: 6595.50 @ 1528 ET Sep 12

- SUP 1: 6481.60 20-day EMA

- SUP 2: 6380.81 50-day EMA

- SUP 3: 6313.25 Low Aug 6

- SUP 4: 6239.50 Low Aug 1 and a key support

A bull cycle in S&P E-Minis remains intact and Thursday’s gains reinforce current conditions. The contract again traded to a fresh cycle high Thursday. This confirms a resumption of the uptrend and maintains the bullish price sequence of higher highs and higher lows. Sights are on the 6600.00 handle where a break would strengthen the bull theme and open 6673.37, a Fibonacci projection. Initial support to watch is 6481.60, the 20-day EMA.

COMMODITIES

US OIL: September 12 - Americas End of Day Oil Summary: Crude Rises -- WTI crude prices are seeing some support from the anticipation of sanctions on Russian energy, set against looming oversupply expectations.

- The Baker Hughes US rig count rose 2 to 539 w/w while the oil rig count rose 2 to 416. Canadian rigs were up 2 this week including 4 oil rigs.

- The European Commission is expected to present a proposal for the 19th Russia sanctions package on Wednesday, Reuters reports.

- The global oil market faces a surplus of ~3m b/d in Q1 2026, according to Macquarie Group analyst Vikas Dwivedi cited by Bloomberg.

- A Ukrainian drone strike on the Russian Baltic export hub of Primorsk Sep 12 which set fire to a tanker at berth, is bullish for near-term crude oil and diesel price sentiment, Platts said.

- Saudi Arabia’s oil exports are set to jump this month as the twin impact of higher production and easing local demand from peak summer levels frees up supply, Bloomberg reports.

- WTI Oct futures were up 0.5% at $62.69

- WTI Nov futures were up 0.5% at $62.40

MONDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 15/09/2025 | 0900/1100 | * | Trade Balance | |

| 15/09/2025 | 1230/0830 | ** | Monthly Survey of Manufacturing | |

| 15/09/2025 | 1230/0830 | ** | Wholesale Trade | |

| 15/09/2025 | 1230/0830 | ** | Empire State Manufacturing Survey | |

| 15/09/2025 | 1300/0900 | * | CREA Existing Home Sales | |

| 15/09/2025 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 15/09/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 15/09/2025 | 1810/2010 | ECB Lagarde at Institut Montaigne Paris | ||

| 15/09/2025 | - | FOMC Meetings with S.E.P. |