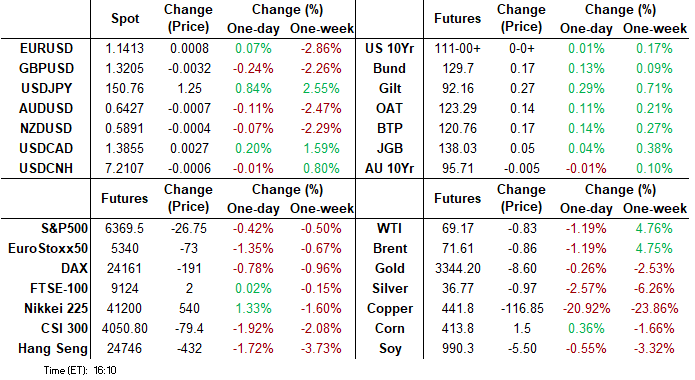

MNI ASIA MARKETS ANALYSIS: Mexico Granted 90 Day Tariff Extnsn

HIGHLIGHTS

- Late month-end rebalancing appeared to be in play a couple dealer desks said as Tsys and stocks looked to extend lows after the bell, US$ climbing higher (BBDXY +2.49 at 1221.74).

- Treasury futures extend gains ahead midday after Pres Trump's Mexico tariff 90 day extension tweet: "We have agreed to extend, for a 90 Day period"

- Focus on Friday's employment report for July, is expected at 104k in July per the broad Bloomberg consensus.

US TSYS

MNI US TSYS: Rates & Stocks Reverse Early Support, Extend Late Lows Ahead NFP

- Treasuries had a moderately volatile session Thursday, retreating from midday highs to near late session lows after the bell.

- Tsy Sep'25 10Y futures currently trades +1 at 111-01 (110-31 low, 111-10 high). Treasury futures faced resistance yesterday and pulled back from a key short-term hurdle at 111-14+, the high on Jul 22 and 30. A clear break of this level would highlight a stronger reversal and open 111-28, the Jul 3 high.

- Treasury futures had pared gains/rebounded after flurry of morning data: lower than expected weekly & continuing jobless claims, personal income/spending (priors up-revised slightly) and employ cost index largely in-line.

- Initial jobless claims were lower than expected at 218k (sa, cons 224k) in the week to Jul 26 after an unrevised 217k. Continuing claims were also lower than expected at 1946k (sa, cons 1953k) in the week to Jul 19 after a downward revised 1946k (initial 1955k).

- Treasury futures extend gains ahead midday after Pres Trump's Mexico tariff 90 day extension tweet: "We have agreed to extend, for a 90 Day period, the exact same Deal as we had for the last short period of time, namely, that Mexico will continue to pay a 25% Fentanyl Tariff, 25% Tariff on Cars, and 50% Tariff on Steel, Aluminum, and Copper. Additionally, Mexico has agreed to immediately terminate its Non Tariff Trade Barriers, of which there were many."

- Late month-end rebalancing appeared to be in play a couple dealer desks said as Tsys and stocks looked to extend lows after the bell, US$ climbing higher (BBDXY +2.49 at 1221.74).

- Focus on Friday's employment report for July, is expected at 104k in July per the broad Bloomberg consensus. The Bloomberg Whisper currently stands at 115k with little movement after Wednesday’s better than expected ADP report. Fed speakers are out of blackout tomorrow as well.

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.32% (-0.04), volume: $2.727T

- Broad General Collateral Rate (BGCR): 4.31% (-0.03), volume: $1.130T

- Tri-Party General Collateral Rate (TCR): 4.31% (-0.03), volume: $1.098T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $105B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $275B

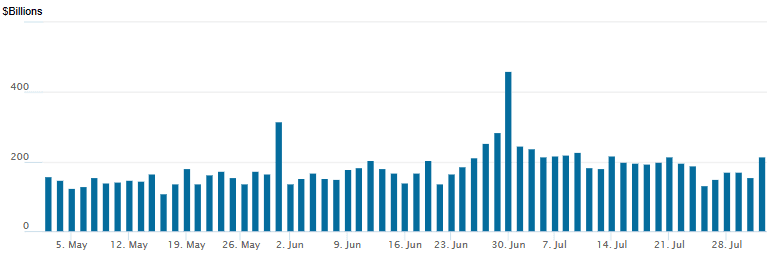

FED Reverse Repo Operation

RRP usage rebounds to $214.445B this afternoon from $155.481B yesterday, total number of counterparties at 52. Usage had fallen to $54.772B on Wednesday, April 16 -- lowest level since April 2021 - compares to July 1: $460.731B highest usage since December 31.

US SOFR/TREASURY OPTION SUMMARY

Heavy two-way SOFR & Treasury option trade reported Thursday, position adjusts to drop in rate hike projections in the second half of the year after yesterday's steady FOMC rate annc. Projected rate cut pricing vs. early morning (*) levels: Sep'25 at -9.9bp (-10.5bp), Oct'25 steady at -18.9bp, Dec'25 at -34bp (-34.4bp), Jan'26 at -42.9bp (-43.4bp). Year end projection well off early July level of appr -65.0bp.

SOFR Options:

-5,000 SFRZ5 96.25/96.62 call strip, 10.25 vs. 95.985/0.36%

Block/pit, +15,000 SFRU5 95.68/95.75/95.81 put trees, 2.0 net ref 95.775

Block, 6,550 SFRH6 96.18/2QH6 96.62 straddle spd, 11.0 net. Green March over

4,220 3QX5 96.25/96.75 strangles, 19.0 ref 96.50

4,200 3QX5 96.25/96.75 strangles, ref 96.50

+10,000 0QU5 97.25/3QU5 96.87 call spds, 0.75 net flattener (blue Aug over)

+20,000 SFRH6 95.62/96.00 put spds 0.5-0.75 over 0QH6 96.12/96.50 put spds (flattener)

+9,000 SFRQ5 95.75/95.87 straddle spds 5.0 ref 95.77

-2,500 SFRZ5 95.56 puts, 0.5 ref 95.975

-20,000 SFRZ5 95.37/95.62 put spds, 0.75 ref 95.98

+2,000 SFRZ5 96.0/SFRH6 96.25 put strip, 42.0

+30,000 0QU5 98.37 calls, cab ref 96.35

+10,000 SFRZ5 95.75/95.87 2x1 put spds, 0.75

+10,000 SFRH6 95.37/96.62 2x1 put spds, 0.5 ref 96.21

Block, 2,500 SFRZ5 96.37/96.75 call spds, 3.0 ref 96.02

+2,000 SFRU5 95.62/95.75 put spds, 5.5

+3,000 SFRZ5 96.25/96.50 call spds, 3.0 ref 95.99

2,500 SFRX5 96.18/96.50/97.00 broken call flys ref 95.99

2,000 SFRQ5 95.62/95.68 put spds ref 95.76

3,000 SFRZ5 96.25/96.50 call spds ref 95.985

3,000 SFRU5 95.75/95.81/95.87 put flys ref 95.755

1,500 SFRV5 95.75/95.81/95.93 2x3x1 put flys ref 95.98

12,000 SFRZ5 95.75/95.87/96.25/96.37 put condors, 6.0

Blocks, 9,800 SFRU5 95.25/95.75 put spds, 5.5-6.0 ref 95.76

over 10,000 SFRU5 95.81/95.93 call spds, 3.75-4.0 ref 95.775

2,000 SFRU5 97.00/97.5 call spds vs. 96.12 puts on 4x3 ratio

4,000 SFRZ6 97.00 puts ref 96.745

1,100 SFRU5 95.75 straddles, 13.5

+5,000 SFRZ5 96.12/96.37 call spds, 5.5 ref 96.00

+2,000 SFRZ5 96.25/96.37/96.62/96.75 call condors, 1.25

6,000 SFRZ5 96.25/96.37/96.75/96.87 call condors, 1.50

5,000 0QZ5 96.75 calls

2,600 SFRU5 95.75 puts ref 95.775

Treasury Options:

3,000 TYU5 111.5 calls, 27 ref 111-07.5

2,100 TYU5 111 straddles, 112

over 14,500 TYU5 108/109/110 put flys ref 111-04

+10,000 TYU5 110 puts, 13

2,000 TYZ5 107/109 put spds ref 111-03

1,800 UXYV5 114/116 call spds vs. 111.5 puts ref 112-31.5

12,000 TUV5 104.12/104.37 call spds ref 103-24.62

-1,500 TYU5 112.25 calls, 14

1,700 wk1 TY 110/110.5/110.75 put trees, 2 ref 111-04.5 (exp 8/1)

-2,500 wk1 TY 110 puts, 1

+1,000 wk1 TY 111.25 straddles, 37 vs. 111-03.5/0.13%

MNI BONDS: EGBs-GILTS CASH CLOSE: Curve Flattening Continues

Curves flattened for a third consecutive session Thursday.

- Longer-end yields moved lower at the open, with 10Y Bund yields touching their lowest intraday level since July 24 and Gilts July 7.

- The rest of the session was largely range-bound in nature, with weakness in European equities keeping yields contained amid solid-leaning US data.

- The short-end lagged, following Wednesday's hawkishly-perceived Federal Reserve meeting outcome.

- Reaction to European data was limited, including slight upside in German state-level, French and Italian flash July inflation readings.

- The German curve twist flattened, with the UK's bull flattening. Periphery/semi-core EGB spreads were mixed but little changed on the whole.

- Friday's schedule includes final July manufacturing PMIs and Eurozone flash July HICP.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 1bps at 1.964%, 5-Yr is down 0.1bps at 2.295%, 10-Yr is down 1.1bps at 2.695%, and 30-Yr is down 2.8bps at 3.176%.

- UK: The 2-Yr yield is down 1.5bps at 3.861%, 5-Yr is down 3.4bps at 4.007%, 10-Yr is down 3.4bps at 4.569%, and 30-Yr is down 3.9bps at 5.376%.

- Italian BTP spread down 0.1bps at 81.3bps / French up 0.4bps at 65.7bps

MNI EGB OPTIONS: Busy Session For Bund Options, Large CS vs PS In Euribor Continues

Thursday's Europe rates/bond options flow included:

- RXU5 130/132/134c fly, sold at 34 in 4.5k

- RXU5 128.50/127.50/126.50p fly sold at 10 in 2k.

- RXU5 129.5/129ps vs 132c, bought the ps for 13.5 in 5k

- RXU5 127p, bought for 6 in 3k

- RXU5 133c, bought for 4 in ~4k

- ERH6 98.3125/98.4375cs vs 97.9375/97.8125ps, bought the cs for 1 in 33k total (also bought Yesterday for 1.5 in 8k)

- ERU6 98.6875/98.875cs, bought for 1.25 in 36k vs +2k ERU6 98.25p

- SFIX5 96.30/96.45 call spread paper paid 4.5 on 5K

- SFIH6 96.90/97.10 call spread paper paid 1.75 on 6K

MNI FOREX: BoJ Give Greenlight to Further USD/JPY Gains

- Markets were broadly in consolidation across Thursday trade: EUR/USD held inside the recent range, propped up just above yesterday's lows at 1.1401. With both the July ECB and Fed rate decisions now cleared - it's left to the US data to further curtail expectations of a rate cut from the Fed at the September meeting - particularly as the mid-week press conference with Powell pressured assumed policy rates through the end of the year and into the first half of 2026.

- While EUR trade was contained, GBP/USD edged to a new pullback low. This marks a sixth consecutive session of lower lows for the pair, and a clean break of the 100-dma at 1.3338. This week's weakness exposes key support into the 1.3140 level, a break below which extends the sharp correction off the early July high.

- The standout Thursday was JPY. USD/JPY rallied sharply throughout the day despite the weakness in core equity futures. The recent rally in USD/JPY and EUR/JPY was given another tailwind following the BoJ decision and the board's decision to play down the risk of inflation through this year and into the next - pressuring BoJ hike expectations this year.

- AUDUSD has seen little in the way of a recovery rally after breaking lower this week. Rate has traded through both the 20- and 50-day EMAs. This undermines a recent bullish theme and signals the likely start of a corrective cycle. Note that support 0.6455 the Jul 17 low, has also been cleared.

- Focus Friday notably switches to the July NFP print. Street looks for job gains of 104k, while the household survey's unemployment rate will continue to be watched closely as a barometer of broad labor market tightness amidst significant immigration curbs. Powell stressed in Wednesday's FOMC press conference that the reduction in labor demand has been in tandem with reduced supply.

MNI OPTIONS: Expiries for Aug01 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1400-05(E1.7bln), $1.1425-30(E956mln), $1.1440-60(E2.2bln), $1.1500(E845mln)

- USD/JPY: Y146.00($1.4bln), Y147.00($1.6bln), Y148.15-35($729mln), Y149.00($574mln), Y150.00($932mln), Y151.00($627mln)

- USD/CAD: C$1.3450-70($1.2bln), C$1.3780-00($592mln), C$1.3930-50($540mln)

- USD/CNY: Cny7.3000($819mln)

MNI US STOCKS: Late Equities Roundup: Tech Heavy Nasdaq Continues to Outperform

- Stocks are near steady (SPX eminis) to mixed in late Thursday trade, tech-heavy Nasdaq outperforming modestly lower DJIA going into month end. Eminis and Nasdaq index had climbed to record highs before support waned after Pres Trump announced a 90 day tariff extension to Mexico, injecting uncertainty ahead of the August 1 deadline.

- Currently, the DJIA trades down 104.04 points (-0.23%) at 44357.73, S&P E-Minis up 2.5 points (0.04%) at 6398.75 (6468.50 high), Nasdaq up 66.4 points (0.3%) at 21195.11 (21457.48 high).

- Communication Services, Industrials and Information Technology sectors continued to lead gainers: Meta Platforms +11.92%, Western Digital +9.54%, Seagate Technology Holdings +5.50%, AMETEK +5.39% and Microsoft +4.03% and climbing past $4 trillion market value.

- Other gainers included: eBay +18.45%, CH Robinson Worldwide +18.05%, Xylem Inc +9.95%, Huntington Ingalls Industries +8.77%, Generac Holdings +8.19% and Allstate +7.07%.

- Conversely, Health Care, Estate Management and Materials sectors led decliners: following lower than expected earnings, job cuts and several large downgrades Align Technology cratered 36.72%, Baxter International -21.75%, International Paper -12.57%, Dexcom -9.35%, Cigna Group -8.63%, Moderna -6.56%, Paramount Global-5.79% and Smurfit WestRock -5.62%

- Additional earnings expected after the close include: Stryker Corp, Edison International, Arthur J Gallagher & Co, Ingersoll Rand Inc, Reddit Inc, Coinbase Global, Amazon, Roku Inc, First Solar Inc, Lumen Technologies Inc, Monolithic Power Systems Inc and Apple Inc.

MNI EQUITY TECHS: E-MINI S&P: (U5) Bulls Remain In The Driver’s Seat

- RES 4: 6523.63 1.764 proj of the May 23 - Jun 11 - 23 price swing

- RES 3: 6500.00 Round number resistance

- RES 2: 6477.31 1.618 proj of the May 23 - Jun 11 - 23 price swing

- RES 1: 6468.50 Intraday high

- PRICE: 6395.00 @ 1508 ET Jul 31

- SUP 1: 6366.75/6329.36 Low Jul 30 / 20-day EMA

- SUP 2: 6288.25 Low Jul 17

- SUP 3: 6241.00 Low Jul 16

- SUP 4: 6181.96 50-day EMA

The trend set-up in S&P E-Minis remains bullish. A fresh cycle high today confirms a resumption of the uptrend and maintains the price sequence of higher highs and higher lows. Note that moving average studies are in a bull-mode position highlighting a clear dominant uptrend. Sights are on 6477.31, a Fibonacci projection. Key support is at the 50-day EMA, at 6181.96. Support at the 20-day EMA is at 6329.36.

COMMODITIES

MNI AMERICAS OIL: WTI crude has come under pressure today amid trade uncertainty

July 31 - Americas End-of-Day Oil Summary: WTI crude has come under pressure today amid trade uncertainty, though remains near its highest since late-June given Trump’s threats of secondary tariffs on Russia.

- The market is watching for any signs of progress towards a peace agreement that could see Russia avoid Trump’s threat of sanctions/secondary tariffs as part of his 10-day deadline.

- Trump on Wednesday announced tariffs of 15% on imports from South Korea that matched the rate for Japan, while India faces 25%. Trump on Thursday extended the tariff deal with Mexico for 90 days.

- U.S. Treasury Secretary Scott Bessent said on Tuesday he warned Chinese officials that continuing to buy Russian oil would lead to big tariffs due to legislation in Congress.

- U.S. crude oil inventories rose by 7.7 million barrels in the week ending July 25 to 426.7 million barrels, driven by lower exports, the Energy Information Administration said on Wednesday.

- WTI Sep futures were down 1% at $69.26

- WTI Oct futures were down 1% at $68.24

FRIDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 01/08/2025 | 0715/0915 | ** | S&P Global Manufacturing PMI (f) | |

| 01/08/2025 | 0745/0945 | ** | S&P Global Manufacturing PMI (f) | |

| 01/08/2025 | 0750/0950 | ** | S&P Global Manufacturing PMI (f) | |

| 01/08/2025 | 0755/0955 | ** | S&P Global Manufacturing PMI (f) | |

| 01/08/2025 | 0800/1000 | * | Retail Sales | |

| 01/08/2025 | 0800/1000 | ** | S&P Global Manufacturing PMI (f) | |

| 01/08/2025 | 0830/0930 | ** | S&P Global Manufacturing PMI (Final) | |

| 01/08/2025 | 0900/1100 | *** | HICP (p) | |

| 01/08/2025 | - | *** | Domestic-Made Vehicle Sales | |

| 01/08/2025 | 1230/0830 | *** | Employment Report | |

| 01/08/2025 | 1345/0945 | *** | S&P Global Manufacturing Index (final) | |

| 01/08/2025 | 1400/1000 | *** | ISM Manufacturing Index | |

| 01/08/2025 | 1400/1000 | * | Construction Spending | |

| 01/08/2025 | 1400/1000 | *** | U. Mich. Survey of Consumers | |

| 01/08/2025 | 1400/1000 | ** | University of Michigan Surveys of Consumers Inflation Expectation | |

| 01/08/2025 | 1400/1000 | * | Construction Spending | |

| 01/08/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 01/08/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly |