FOREX: BoJ Give Greenlight to Further USD/JPY Gains

- Markets were broadly in consolidation across Thursday trade: EUR/USD held inside the recent range, propped up just above yesterday's lows at 1.1401. With both the July ECB and Fed rate decisions now cleared - it's left to the US data to further curtail expectations of a rate cut from the Fed at the September meeting - particularly as the mid-week press conference with Powell pressured assumed policy rates through the end of the year and into the first half of 2026.

- While EUR trade was contained, GBP/USD edged to a new pullback low. This marks a sixth consecutive session of lower lows for the pair, and a clean break of the 100-dma at 1.3338. This week's weakness exposes key support into the 1.3140 level, a break below which extends the sharp correction off the early July high.

- The standout Thursday was JPY. USD/JPY rallied sharply throughout the day despite the weakness in core equity futures. The recent rally in USD/JPY and EUR/JPY was given another tailwind following the BoJ decision and the board's decision to play down the risk of inflation through this year and into the next - pressuring BoJ hike expectations this year.

- AUDUSD has seen little in the way of a recovery rally after breaking lower this week. Rate has traded through both the 20- and 50-day EMAs. This undermines a recent bullish theme and signals the likely start of a corrective cycle. Note that support 0.6455 the Jul 17 low, has also been cleared.

- Focus Friday notably switches to the July NFP print. Street looks for job gains of 104k, while the household survey's

unemployment rate will continue to be watched closely as a barometer of broad labor market tightness amidst significant immigration curbs. Powell stressed in Wednesday's FOMC press conference that the reduction in labor demand has

been in tandem with reduced supply.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

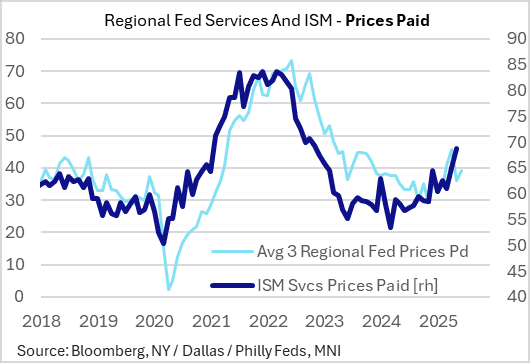

US OUTLOOK/OPINION: ISM Services Prices Should Have Steadied In June (2/2)

The ISM Services Prices Paid gauge is seen moderating to 68.4 from 68.7, which would be the first drop since March but still keep the index above 60 for a 7th consecutive month.

- Part of this expectation for a moderation derives from June's flash S&P Global PMI report which noted that while service sector prices "rose sharply...often attributed to tariffs but also reflecting higher financing, wage and fuel costs", "service sector input costs and selling prices nonetheless rose at slower rates than in May, in part reflecting more intense competition."

- Conversely, across regional Fed surveys, we saw a pickup overall in June, with rises of varying magnitudes in each of the Philadelphia, Dallas, and New York surveys, with the Richmond Fed's 1-year % change rising to 5.2% from 5.0%.

- That said, the rapid rise in the ISM Services prices paid gauge wasn't reflected by the pullback in Fed surveys in May and June vs April's recent peak.

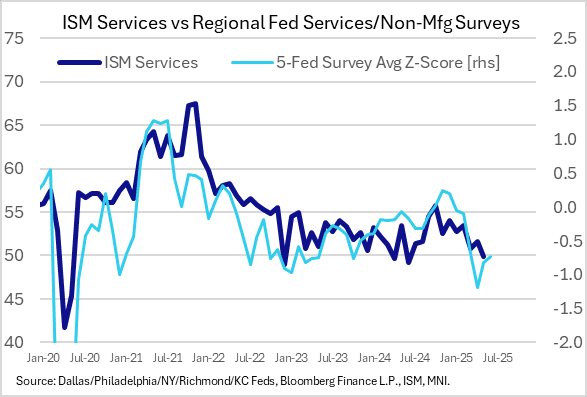

US OUTLOOK/OPINION: ISM Services Activity Expected To Pick Up Modestly (1/2)

The June ISM Services Index (released Thursday at 1000ET) is expected by Bloomberg consensus to see a rise to 50.8 (range of 49.0 to 51.8) from 49.9 prior.

- May's was the first sub-50 reading in the index since June 2024, and came amid pronounced weakness in New Orders (46.4, down 5.9 points).

- There are no consensus expectations for New Orders or Employment (was 50.7 in May, a 1.7 point rise from April), both of which unexpectedly weakened in the ISM manufacturing report.

- The S&P Global flash June PMI moderated to a still-solid 53.1 from 53.7 in May, with the wide gap between the two surveys expected to narrow slightly this month.

- Current / general activity readings in regional Fed services/non-manufacturing surveys broadly improved in June vs May, including New York, Philadelphia, Richmond, and Dallas, with Kansas City's weakening (the Chicago Fed's nonmanufacturing index also reversed lower from a jump in May).

- Each remained in negative territory on a normalized basis, though the average z-score (5-year lookback) ticked slightly higher (-0.7 from -0.8) suggesting slight improvement in overall contractionary territory for activity.

US TSYS: Late SOFR/Treasury Option Roundup: Projected Cut Pricing Eases

Option desks reported chunky two-way SOFR & Treasury option trade Tuesday, upside call interest evaporating into midday as underlying futures retreated after this morning's ISM Mfg and JOLTS job data. Projected rate cut pricing retreated from early morning (*) levels: Jul'25 steady at -5.3bp, Sep'25 at -28.0bp (-29.3bp), Oct'25 at -44.8bp (-47.3bp), Dec'25 at -63.9bp (-68.4bp).

- SOFR Options:

- +5,000 SFRU5 95.68/95.87/96.00 put flys, 0.75 ref 95.975

- +10,000 SFRZ5 98.00 calls, 2.0

- +5,000 SFRH6 96.12/96.50 2x1 put spds, 5.5

- 5,000 0QQ5 97.18 calls, ref 96.925

- Block, 10,000 SFRH6 96.00/96.50 put spds, 18.0

- over +45,000 SFRU5 95.87/95.93/96.00/96.12 broken call condors, 0.0 ref 96.00

- 2,000 0QN5 96.68/96.87 put spds ref 96.94

- 2,000 SFRN5 96.00/96.25 call spds ref 96.005

- Block, 12,000 SFRQ5 96.00/96.12/96.25/96.37 call condors, 2.5 ref 96.005

- Block/screen 6,000 SFRU5 95.68/95.75/95.87 2x3x1 put flys, 1.25 net

- 4,000 0QN5 97.06/97.18 call spds vs. 96.68/96.81 put spds, 0.5 net - call spd over

- +4,000 SFRZ5 96.00 straddles, 48.0 vs. 96.35/0.52%

- +2,000 SFRQ5 95.81/95.87/96.00 broken put trees, 4

- +8,000 SFRU5 96.00/96.12 put spds, 8.5 ref 96.00

- +2,000 SFRZ5 96.00/96.25 2x1 put spds, 3.25 ref 96.325

- Treasury Options:

- +10,000 TUU5 105.12 calls, 3

- 3,500 TYQ5 112.75/113.25 call spds vs. 111.75/112.25 put spds, 5.0 net/puts over

- Block, 18,900 wk1 TY 111.5/112 put spds, 11.0

- -4,000 wk2 TY 112.25 straddles, 48 vs. 112-05.5/0.09%

- 10,000 TYU5 108/110 put spds, 12 ref 112-07.5

- -15,000 wk1 FV 109.25/109.5/109.75/110 call condors, 3.5 vs. 109-03.5/0.10%

- +2,500 FVU5 105/106.5 put spds, 2.5 vs. 109-01.25/0.04%

- +5,000 TYQ5 112.5 calls, 39 vs. 112-10/0.46%

- +2,000 TYQ5 110.5/112 call spds vs. 109.5/111.5 put spds, 50 net vs. 112-10/0.54%

- +2,000 TYQ5 109 puts, 3 ref 112-04/0.08%

- +2,500 TYU5 109.5 puts, 13

- -1,500 FVQ5 108.5 puts, 14.5 vsd. 109-01.5/0.29%

- +5,000 TYU5 107/108 put spds, 2 ref 112-10.5

- +10,000 FVQ5 108 puts, 6.5 ref 109-03.25

- +2,000 TYQ5 113.25 calls, 23 vs. 112-10/0.60%

- +5,000 wk1 TY 111.25/111.5 put spds, 3 vs. 112-04.5/0.10