MNI ASIA MARKETS ANALYSIS: June FOMC Minutes: July on Hold

HIGHLIGHTS

- Treasuries look to finish near late session highs, little new from the June FOMC minutes with members signaling a July hold while keeping futures policy options open.

- Overall, Fed "participants noted that the progress in returning inflation to target had continued even though that progress had been uneven"

- Pres Trump issued a raft of new tariff letters, imposing unilateral tariff rates on six trading partners: Algeria (30%), Libya (30%), Moldova (25%), Iraq (30%), Brunei (25%), and the Philippines (20%).

US TSYS

MNI US TSYS: June FOMC Minutes Signal July Hold, Forward Options Open

- Treasuries look to finish near late session highs, little new from the June FOMC minutes with members signaling a July hold while keeping futures policy options open. The June meeting minutes captured a Committee that was leaning in a slightly more hawkish direction than earlier in the year, though probably no more than should have been expected.

- The Dot Plot released at the meeting already captured most of the story: a divided Committee retains its overall easing bias but needs varying degrees of certainty before supporting a resumption of the easing cycle.

- Overall, "participants noted that the progress in returning inflation to target had continued even though that progress had been uneven" (and in a nod to the hawks and perhaps a little surprising given decent inflation readings, "a few participants noted that there had been limited progress recently in reducing core inflation.").

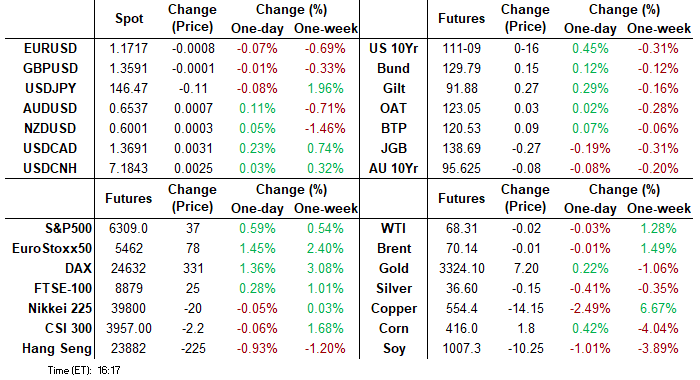

- Tsy Sep'25 10Y futures are currently +15.5 at 111-08.5 vs. 111-10 session high (below 111-12 high on Monday) technical resistance to watch is at 111-28, the Jul 3 high. Curves mixed with the short end flatter: 2s10s -2.616 at 47.838.

- Projected rate cut pricing has gained momentum vs morning (*) levels: Jul'25 at -1.7bp (-1.2bp), Sep'25 at -18.6bp (-17.3bp), Oct'25 at -33.7bp (-31.7bp), Dec'25 at 52bp (-49.3bp).

- Cross asset roundup: USD inching lower, Bbg index BBDXY -0.11 at 1196.53; US stocks firmer but off early session highs: SPX eminis +35.5 at 6307.5, Gold firmer (+13.19 at 3315.11), crude mildly lower (WTI -0.07 at 68.26).

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.34% (+0.01), volume: $2.765T

- Broad General Collateral Rate (BGCR): 4.32% (+0.01), volume: $1.118T

- Tri-Party General Collateral Rate (TCR): 4.32% (+0.01), volume: $1.088T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $117B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $262B

FED Reverse Repo Operation:

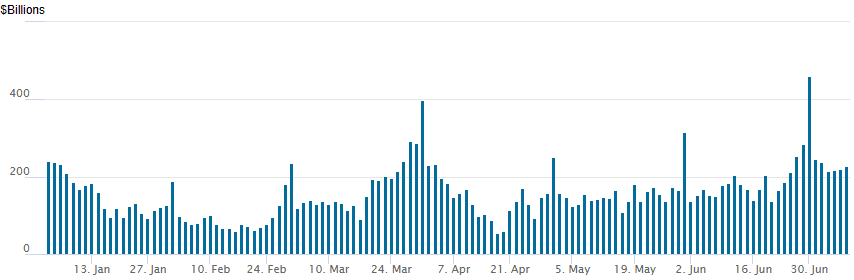

RRP usage climbs to $227.273B this afternoon from $219.415B yesterday, total number of counterparties at 37. Usage had fallen to $54.772B on Wednesday, April 16 -- lowest level since April 2021 - compares to yesterday's (July 1) $460.731B highest usage since December 31.

US SOFR/TREASURY OPTION SUMMARY

SOFR & Treasury options took advantage of the rebound in underlying futures to buy puts/put spreads (Dec SOFR put tree looking at year end Fed on hold), unwind calls with a few exceptions. Projected rate cut pricing has gained momentum vs morning (*) levels: Jul'25 at -1.7bp (-1.2bp), Sep'25 at -18.6bp (-17.3bp), Oct'25 at -33.7bp (-31.7bp), Dec'25 at 52bp (-49.3bp).

SOFR Options:

Update, +12,000 SFRZ5 95.62/95.75/95.81 broken put trees, 0.5 ref 96.17

+2,000 SFRU5 96.00/96.25 1x2 call spds 1.0 vs. 95.90/0.05%

+2,000 SFRU5 96.00/96.25 call spds, 2.75

-2,000 SFRH6 96.37/96.87 call spds, 15.0 ref 96.40/0.26%

+2,500 SFRU5 95.62/95.75 put spds, 3.0

-15,000 0QU5 97.12/98.12 call spds, 5.25 ref 96.745

+5,000 SFRU5 96.00 calls, 4.75 ref 95.88

+20,000 SFRU5 96.06/96.12 call spds, 0.75

+6,000 SFRU5 95.75/96.00/96.25 call trees, 9.0 ref 95.865

+4,000 SFRZ5 95.87/96.62 call over risk reversals, 1.0 vs. 96.15/0.40%

+1,000 SFRZ5 96.25 straddles, 38.5

over +20,000 SFRQ5 95.68/95.75 put spd, 1.25 (more on a 2x3 ratio)

+2,000 SFRQ5/SFRU5 95.75 put spd, 2.0

3,000 SFRU5 95.62/95.75 put spd, 3.0

Treasury Options:

Block, 9,000 wk2 TY 111.5 calls, 3

2,000 USQ5 110/112 put spds 14 ref 113-18

10,000 TYQ5 110.5/111.5 put spds 33 vs. 111-00/0.34%

-5,000 TYU5 111 calls, 46 vs 110-24/0.44%

+2,250 TYU5 110/110.5/111/111.5 call condor, 7 vs 110-30/0.05%

3,950 TYQ5 111.75/112.25 call spds ref 110-28

-5,000 wk2 TY 111 put, 15

+5,000 wk2 TY 111 straddle, 26 vs 110-28.5 to -29/0.20%

MNI EGB BONDS: EGBs-GILTS CASH CLOSE: Gilt Curve Flattens As BOE Mulls QT

The multi-session rise in yields took a breather Wednesday, with Gitls outperforming Bunds.

- Yields dipped slightly at the open, picking up through the morning in contained fashion as market participants digested overnight tariff rate announcements from the US.

- But the rally proved short lived, with German and UK supply and upside in equities and oil prices capping gains.

- The Gilt curve edged flatter as BoE Governor Bailey reaffirmed the idea that the recent curve steepening will factor into the BoE's decision on QT.

- US Treasuries led a modest rally through the afternoon, as President Trump renewed calls to call for the Federal Reserve to cut rates.

- 10Y instruments remained confined within the prior session's ranges throughout. The UK curve twist flattened, with the German curve leaning bull steeper.

- Periphery/semi-core EGB spreads widened slightly, with OATs underperforming.

- Thursday's calendar includes varying industrial production data and final June inflation for some Eurozone countries, with appearances by ECB's Cipollone, Escriva, and Villeroy, and BOE's Breeden scheduled.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 1.2bps at 1.86%, 5-Yr is down 1.5bps at 2.239%, 10-Yr is down 1.4bps at 2.673%, and 30-Yr is down 1bps at 3.162%.

- UK: The 2-Yr yield is up 0.8bps at 3.88%, 5-Yr is down 0.1bps at 4.041%, 10-Yr is down 2.1bps at 4.612%, and 30-Yr is down 3.2bps at 5.422%.

- Italian BTP spread up 0.1bps at 85.1bps / French OAT up 1bps at 68.8bps

MNI EGB OPTIONS: Sonia Call Structure Buying Picks Up

Wednesday's Europe rates/bond options flow included:

- RXQ5 128.5/127.5ps, bought for 11.5 in 4.5k

- SFIU5 96.00p with SFIZ5 96.05p, sold the strip at 5.5 in 4k

- SFIZ5 95.85/96.25/96.05c fly, bought for 3.75 in 11k

- SFIZ5 96.85c, bought for 2 in 4k vs selling SFIU5 96.00p at 2.5 in 1k

- ERU5 97.9375/97.75ps, bought for 0.25 in 7.5k

- ERU5 97.9375/97.8125ps, bought for 0.25 in 20.5k (ref 98.15).

- ERZ5 98.31/98.43cs, sold at 2.75 in 16k

- ERH6 98.0625/98.1875/98.375/98.625 broken c condor vs ERH6 97.8125/97.6875/97.5625 p fly, bought the condor for 2.5 in 5k

MNI FOREX: USD Index Consolidates Corrective Move Higher

- A relatively subdued session for foreign exchange has allowed the greenback to consolidate its most recent recovery from multi-year trendline support, with the DXY hovering around 1.25% above the July 01 cycle lows.

- EURUSD tilts lower on the session, with the pair slipping back to the 1.1700 handle. The latest pullback in appears corrective, given the underlying bullish trend condition. Note too that corrections have been shallow so far, reinforcing the trend condition. Key short-term support to watch lies at 1.1646, the 20-day EMA.

- NZDUSD has also consolidated its recent pull lower, having printed below 0.5980 overnight following the RBNZ’s decision to hold the OCR at 3.25%. The pair continues to exert pressure on the 50-day EMA, of which spot has not closed below since April 09. Continued weakness would signal scope for a move towards 0.5883 and 0.5847 (double bottom seen in mid-May and an important pivot level).

- AUDNZD has also extended its recovery to a seven-week high above 1.0900. Trendline support drawn from the April lows has helped underpin the latest bounce for the cross, targeting 1.0922 (May 15 high) initially, before the early April highs just above 1.10.

- Separately, USDJPY is a touch lower on Wednesday, having notably reversed from the overnight highs of 147.18 and tracking around 146.45 as we approach the APAC crossover. USDJPY has lost all downside momentum for now and trending back towards the upper bound if its broader 142.00 - 148.00 range. The Market is long JPY and should the USD manage to extend its correction higher, this will further challenge the conviction of Yen longs.

- Thursday’s data calendar is highlighted by US jobless claims, before the focus turns to Canadian employment data on Friday.

MNI FX OPTIONS: Expiries for Jul10 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1650(E2.5bln), $1.1685-00(E1.5bln), $1.1710-20(E616mln), $1.1735-50(E1.5bln), $1.1800(E1.3bln)

- USD/JPY: Y143.95-15($1.0bln), Y144.70-90($1.3bln), Y146.50-55($681mln), Y147.00($832mln)

- GBP/USD: $1.3490-10(Gbp529mln), $1.3570(Gbp540mln)

- EUR/GBP: Gbp0.8595-00(E815mln)

- AUD/USD: $0.6440-55(A$954mln), $0.6500(A$599mln), $0.6415-25(A$589mln), $0.6600(A$634mln)

- NZD/USD: $0.6000(N$517mln)

- USD/CAD: C$1.3625-35($1.0bln)

MNI US STOCKS: Late Equities Roundup: Moderate Support Post June FOMC Minutes

- Stocks are drawing some support following the June FOMC minutes release late Wednesday, Treasuries extend highs, curves flatter as markets digested uneven tariff-tied inflation progress. Currently, the DJIA trades up 163.08 points (0.37%) at 44403.01, S&P E-Minid up 28 points (0.45%) at 6300, Nasdaq up 163.8 points (0.8%) at 20582.09.

- Communication Services and Information Technology sectors continued to lead gainers in late trade, interactive media and entertainment shares buoyed the former with Meta Platforms +2.08, Alphabet +1.39%, Match Group +1.11% and Warner Bros Discovery +0.92%.

- Tech sector shares were supported by Enphase +4.37%, Arista Networks +3.55%, Broadcom +2.04%, Palantir Technologies +1.80% and NVIDIA +1.74% (fist company to reach $4T market cap).

- On the flipside, Consumer Staples and Energy sectors underperformed in late trade, The Hershey Co -4.30%, Altria Group -3.65%, Monster Beverage -3.58% and Mondelez Int -1.92% weighed on the Consumer Staples sector while Targa Resources -1.61%, EOG Resources -1.56%, Devon Energy -1.42% and Kinder Morgan -1.33% kept pressure on the Energy sector.

MNI EQUITY TECHS: E-MINI S&P: (U5) Bull Cycle Remains In Play

- RES 4: 6402.44 1.382 proj of the May 23 - Jun 11 - 23 price swing

- RES 3: 6381.00 1.764 proj of the Apr 7 - 10 - 21 price swing

- RES 2: 6356.12 1.236 proj of the May 23 - Jun 11 - 23 price swing

- RES 1: 6333.25 High Jul 3

- PRICE: 6301.50 @ 1520 ET Jul 9

- SUP 1: 6235.50 Low Jul 2

- SUP 2: 6163.03/6021.72 20- and 50-day EMA values

- SUP 3: 5811.50 Low May 23

- SUP 4: 5645.75 Low May 7

The trend condition in S&P E-Minis remains bullish and the contract is holding on to the bulk of its recent gains. Resistance at 6128.75, the Jun 11 high, has recently been breached. The break confirmed a resumption of the uptrend that started Apr 7. This was followed by a breach of key resistance and a bull trigger at 6277.50, the Feb 21 high. Sights are on 6356.12, a Fibonacci projection. Key support is at the 50-day EMA, at 6021.72.

MNI COMMODITIES: Copper Trend Condition Remains Bullish, Gold, WTI Rangebound

- After spiking sharply higher yesterday following President Trump’s 50% tariff threat, copper futures have pulled back today, with the red metal currently 2.6% lower on the session at $554/lb.

- Copper remains more than 10% up from yesterday, however, having broken key resistance at $546.15, the Mar 26 high.

- The breach is seen as a key bullish development and reinforces the current primary uptrend. Sights are on a retest of yesterday’s high at $589.55. Clearance of this level would open the $600.00 handle.

- Price action is likely to remain volatile, however. Key short-term support has been defined at $497.25, the Jul 8 low.

- Meanwhile, spot gold has edged up by 0.3% to $3,311/oz, as the yellow metal has struggled for direction today.

- Recent weakness in gold resulted in a breach of the 50-day EMA, and a trendline drawn from the Dec 30 ‘24 low and connected to the Feb 28 low. A clear break of both trend tools would signal scope for a deeper correction, and open $3,245.5, the May 29 low.

- However, the recovery from the Jun 30 low also highlights a possible false trendline break. A resumption of gains would refocus attention on $3,451.3, the Jun 16 high.

- WTI has also been largely rangebound as the market continues to monitor US trade policy and any impact on demand.

- WTI Aug 25 is up 0.1% at $68.4/bbl.

- Support to watch is the 50-day EMA, at $65.22. Initial resistance is at $71.20.

THURSDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 10/07/2025 | 0600/0800 | *** | CPI Norway | |

| 10/07/2025 | 0600/0800 | ** | Private Sector Production m/m | |

| 10/07/2025 | 0600/0800 | *** | HICP (f) | |

| 10/07/2025 | 0700/0900 | ECB Cipollone Digital Euro Lecture | ||

| 10/07/2025 | 0800/1000 | * | Industrial Production | |

| 10/07/2025 | - | *** | Money Supply | |

| 10/07/2025 | - | *** | New Loans | |

| 10/07/2025 | - | *** | Social Financing | |

| 10/07/2025 | 1230/0830 | *** | Jobless Claims | |

| 10/07/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 10/07/2025 | 1400/1000 | St. Louis Fed's Alberto Musalem | ||

| 10/07/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 10/07/2025 | 1500/1600 | BOE Breeden On Climate Change | ||

| 10/07/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 10/07/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 10/07/2025 | 1700/1300 | *** | US Treasury Auction Result for 30 Year Bond | |

| 10/07/2025 | 1715/1315 | Fed Governor Christopher Waller | ||

| 10/07/2025 | 1830/1430 | Fed's Mary Daly at MNI |