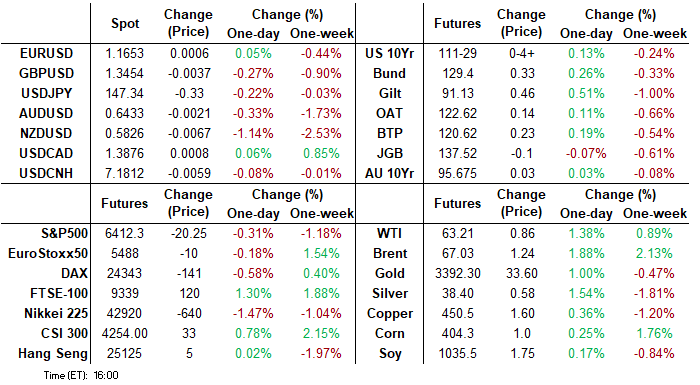

MNI ASIA MARKETS ANALYSIS: July FOMC Minutes Mixed Messaging

HIGHLIGHTS

- Treasuries look to finish modestly higher Wednesday, off midday highs after slightly mixed messages from the July FOMC minutes regarding the inflation outlook, labor market, and ultimately policy.

- A majority of participants judged the upside risk to inflation as the greater of these two risks, while several participants viewed the two risks as roughly balanced

- DJIA index staged a late session rebound while Nasdaq traded weaker - weighed by chip stocks amid reports the Trump admin "may seek equity in any such firms awarded federal grants under the Biden-era CHIPS Act."

- The Greenback see-sawed lower apparently adopting a more neutral position headed into Friday's Jackson Hole appearance from Chair Powell.

US TSYS

MNI US TSYS: Digesting Mixed Messaging From July FOMC Minutes

- Treasuries look to finish modestly higher Wednesday, off midday highs after slightly mixed messaging from the July FOMC minutes regarding the inflation outlook, labor market, and ultimately policy.

- Tsy Sep'25 10Y contract trades +4 at 111-28.5 after the bell vs. 112-00.5 high, Initial technical support well below at 111-11 (50-day EMA); resistance above at 112-15.5 (High Aug 5 and the bull trigger). Curves mixed: 2s10s -1.699 at 53.911, 5s30s +.196 at 108.438.

- A majority of participants judged the upside risk to inflation as the greater of these two risks, while several participants viewed the two risks as roughly balanced. "Almost all participants viewed it as appropriate to maintain the target range for the federal funds rate at 4.25% to 4.5%".

- Limited data: MBA composite mortgage applications edged -1.4% (sa) lower last week to hold onto most of its refi-driven 11% increase the week prior. Indeed, new purchase applications increased 0.1% after 1.4% whilst refis dipped -3.1% after 23.0%.

- DJIA index staged a late session rebound while Nasdaq traded weaker - weighed by chip stocks amid reports the Trump admin "may seek equity in any such firms awarded federal grants under the Biden-era CHIPS Act."

- The Greenback see-sawed lower (BBDXY -.35 at 1206.64) adopting a more neutral position headed into Friday's Jackson Hole appearance from Chair Powell.

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.33% (-0.01), volume: $2.760T

- Broad General Collateral Rate (BGCR): 4.31% (-0.02), volume: $1.144T

- Tri-Party General Collateral Rate (TCR): 4.31% (-0.02), volume: $1.118T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $109B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $260B

FED Reverse Repo Operation

RRP usage rebounds to $34.999B this afternoon from $22.344B yesterday - lowest since April 5, 2021. Total number of counterparties at 29. This week's retreat compares this year's high usage of $460.731B on June 30.

US SOFR/TREASURY OPTION SUMMARY

Various upside call structures targeting more rate cuts than currently priced traded Wednesday, SOFR outpacing Treasury options for the most part - though paper bought over 100k TYV5 113 calls earlier, adding to some 78k Tuesday. Underlying futures trade modestly higher after the bell - paring gains slightly after mixed messaging in the July FOMC minutes. Projected rate cuts consolidate from midday high to near steady vs. early morning (*) levels: Sep'25 at -20.6bp (-21.1bp), Oct'25 at -34.1bp (-34.9bp), Dec'25 at -54.0bp (-54.1bp), Jan'26 at -65.4bp (-65.1bp).

SOFR Options:

Block, 5,000 SFRH6 96.25/97.25 call spds, 26.5

+50,000 SFRH6 97.25 calls, 6.0-6.5 covered

+50,000 SFRZ5 96.18/96.31/96.50/96.62 call condors, 3.0-3.125 ref 96.205

+15,000 SFRU6 96.00/96.25/96.50 put flys, 3.25

+5,000 SFRU5 95.81 puts, 3.25 vs. 95.90/0.30%

3,500 SFRU5 96.00/96.12/96.25 call flys ref 95.8975

-20,000 SFRU5 95.81/SFRZ5 95.87 put spds, 0.75 net/Sep over

+4,000 SFRU5 95.62/96.31 call over risk reversals, 0.25 ref 95.9025

8,000 SFRU6 96.75/97.25 2x1 put spds ref 96.805

1,400 SFRZ5 96.25/96.37/96.50/96.62 call condors ref 96.21

Block, 4,500 SFRZ5 96.25/96.50/96.75/97.00 call condors, 6.0 ref 96.21

6,000 SFRU5 96.00/96.12/96.25 call flys ref 95.90

6,000 SFRU5 95.87/95.93 put spds ref 95.90

Treasury Options: (reminder Sep options expire Friday)

+10,000 USV5 119 calls, 16

Block: -5,000 WNU5 117.5 puts 20 over the WNV5 116/119 put over risk reversal

-8,000 TYV5 111.5 puts, 34 vs. 111-30.5/0.40%

1,700 FVU5 108.5 puts, 3.5 total volume over 6k

5,000 wk5 TU 103.75/103.87/104 put trees vs. TUU5 103.75 puts

Block/screen, over 10,800 TYU5 111 puts, 2 vs. 111-22.5/0.08%

over 5,600 TYU5 112 calls, 8 last

over 5,300 TYU5 112.5 calls, 2 last

over 103,600 TYV5 113 calls, 20-23 ref 111-24.5 to -25.5 (78k trade Tuesday)

MNI BONDS: EGBs-GILTS CASH CLOSE: Gilts Gain, Shrugging Off Firm UK CPI

EGBs and Gilts rallied Wednesday.

- Gilts outperformed despite UK inflation data coming out on the firmer side of expectations. MNI's Markets Team saw little in the way of "game-changing" information in the report in terms of the BOE's approach to policy, with headline inflation just 7 hundredths above the BOE's forecast at 3.83%Y/Y in July (MNI median 3.7%, BOE 3.76%, 3.58% in June) and much of the upside surprise driven by volatile airfares/accommodation prices.

- Yields descended through much of the session from there, with a further firming notable in Bunds in mid-afternoon as US tech stocks dipped sharply (albeit without any headline trigger).

- In other data, Eurozone final HICP showed marginal upward revisions to the core and services measures.

- Meanwhile, ECB's Lagarde said that uncertainty has been "alleviated, but certainly not eliminated" though this had little impact on rate pricing.

- On the day, the belly outperformed on the German curve, while the UK curve bull flattened. Periphery/semi-core spreads to Bunds closed little changed.

- Thursday's schedule includes flash August PMIs and UK public finance data.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 2.5bps at 1.933%, 5-Yr is down 3.3bps at 2.273%, 10-Yr is down 3.3bps at 2.717%, and 30-Yr is down 2.9bps at 3.294%.

- UK: The 2-Yr yield is down 5.8bps at 3.922%, 5-Yr is down 6.2bps at 4.076%, 10-Yr is down 6.8bps at 4.672%, and 30-Yr is down 7.1bps at 5.531%.

- Italian BTP spread up 0.3bps at 80.8bps / French OAT up 1.2bps at 69.5bps

MNI OPTIONS: Put Condors Bought Across Euribor, Bunds

Wednesday's Europe rates/bond options flow included:

- RXU5/RXV5 129.5c spread, bought the Oct for 20.5 in 5k

- RXV5 127.5/126.5/125.5/123p condor vs 130/131.5 cs, bought the Condor for 2 and 3 in 10k

- ERH6 97.9375/97.8125/97.6875/97.5625p condor, bought for half in 7.5k

- 0RX5 98.25/98.375cs, bought for 2 in 4k

- SFIH6 95.50/60/70/80c condor, bought for 1.5 in 3k

MNI FOREX: NZD Consolidates Sharp Move Lower Following Dovish RBNZ

- The New Zealand dollar has been under significant pressure Wednesday, after the RBNZ committee voted to reduce the OCR by 25bps to 3.00% and two members voted for a larger 50bp interest rate cut. NZDUSD extended the week’s depreciation, extending down to a four-month low of 0.5815.

- Exponential moving average studies have moved into a bear-mode position and today’s move through the May lows bolsters the short-term bearish momentum. The 50% and 61.8% retracements of the April-July price swing are the next notable support levels, located at 0.5803 and 0.5728 respectively.

- Additionally, EURNZD has risen back above the psychological 2.00 mark to trade at its highest level since 2010. A previous attempt above this level in April provided an abrupt top for the cross, before a swift 6% reversal ensued. Given the longer-term significance of current chart levels, EURNZD may be at an important inflection point. Should spot close above 2.00, momentum demand could signal scope for a much stronger rally, potentially targeting 2.1249, the 61.8% retracement of the 2009-2015 range.

- Higher-than-expected inflation data in the UK provided only momentary support for GBP, which then reversed steadily lower across the session. Leaving the UK with one of the highest core rates of inflation in the G10, market sentiment appeared to sour towards sterling. As such, GBPUSD looks set to extend its losing streak to three sessions, sliding back towards 1.3450 as we approach the APAC crossover.

- After creeping to a new weekly high at 98.44 overnight, the USD index slipped back into moderate negative territory on Wednesday. Markets appear to be adopting a more neutral position headed into Friday's Jackson Hole appearance from Chair Powell, while headlines from Trump calling for Fed Governor Cook’s resignation represent a developing risk to monitor.

MNI FX OPTIONS: Expiries for Aug21 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1600(E1.4bln), $1.1625-30(E629mln), $1.1650-70(E1.4bln), $1.1700(E1.6bln), $1.1750(E2.0bln), $1.1800(E3.0bln)

- USD/JPY: Y145.95-00($1.2bln), Y146.70-80($1.8bln), Y151.00($2.5bln)

- AUD/USD: $0.6590-00(A$1.8bln)

- NZD/USD: $0.5975-80(N$820mln)

- USD/CAD: C$1.3775($580mln), C$1.3820($625mln)

MNI US STOCKS: Late Equities Roundup: Tech Stocks Weigh on Broader Market

- Stocks remain weaker but off session lows Wednesday, markets digesting the slightly hawkish July FOMC minutes. Participants generally pointed to risks to both sides of the Committee’s dual mandate, emphasizing upside risk to inflation and downside risk to employment," the report said.

- Currently, he DJIA trades down 10.73 points (-0.02%) at 44911.47, S&P E-Minis down 28.5 points (-0.44%) at 6404.75, Nasdaq down 203.6 points (-1%) at 21111.06.

- Information Technology sector stocks led decliners on the day after Forbes reported the Trump administration "may seek equity in any such firms awarded federal grants under the Biden-era CHIPS Act. Lutnick said the government want to acquire an equity stake in Intel in exchange for grants earmarked under the CHIPS Act."

- Intel led the decline -7.45%, followed by Dell Technologies -6.03%, Micron Technology -5.71%, Keysight Technologies -5.27%, Palantir Technologies -3.01% and Super Micro Computer -2.73%.

- Consumer Discretionary sector share followed close behind: DoorDash -3.62%, Pool Corp -2.76%, Norwegian Cruise Line Holdings -2.74%, Tesla -2.71% and Best Buy Co -2.70%.

- On the positive side, Energy sector shares led gainers as crude prices rose (WTI +0.86 at 63.21): Valero Energy +1.86%, Exxon Mobil +1.41%, EQT Corp +1.23%, Phillips 66 +1.00%, EOG Resources +0.93% and Marathon Petroleum +0.92%.

MNI EQUITY TECHS: E-MINI S&P: (U5) Retracement Mode

- RES 4: 6600.00 Round number resistance

- RES 3: 6554.98 2.0% 10-dma envelope

- RES 2: 6523.63 1.764 proj of the May 23 - Jun 11 - 23 price swing

- RES 1: 6508.75 High Aug 15 and Alltime High

- PRICE: 6405.00 @ 1455 ET Aug 20

- SUP 1: 6402.75 20-day EMA

- SUP 2: 6313.25 Low Aug 6

- SUP 3: 6282.00 50-day EMA

- SUP 4: 6239.50 Low Aug 1

The dominant uptrend in S&P E-Minis remains intact and the latest shallow retracement is considered corrective. Moving average studies are in a bull-mode position, highlighting a clear uptrend. A resumption of gains would pave the way for a climb towards 6523.63, a Fibonacci projection. On the downside, supports to watch are; 6402.75, the 20-day EMA, and 6282.00, the 50-day EMA.

MNI COMMODITIES: Crude Rises Following Inventory Draw, Gold Rallies

- Crude has gained ground today following EIA data showing crude inventory draws, coupled with added hopes of an end to the Russia-Ukraine war.

- WTI Sep 25 is up by 1.4% at $63.2/bbl.

- Bloomberg reports that Italian PM Giorgia Meloni is pushing for security guarantees for Ukraine that, under the scenario of a peace deal or ceasefire being in place, would see its allies decide within 24 hours of a renewed Russian attack whether to provide military support to Kyiv.

- Despite today’s gains, WTI futures remain in a clear bear cycle, with initial support at $61.99, the Jun 30 low, which has been pierced. A continuation lower would open $57.71, the May 30 low.

- Initial resistance to watch is $64.72, the 50-day EMA, while key short-term resistance has been defined at $69.36, the Jul 30 high.

- Elsewhere, spot gold has risen by 0.9% to $3,345/oz, as markets remain cautious ahead of Friday's Jackson Hole appearance from Chair Powell, while headlines from Trump calling for Fed Governor Cook's resignation represent a developing risk to monitor.

- A bull cycle in gold remains intact, with sights on $3,439.0, the Aug 23 high. On the downside, first support to watch lies at $3,268.2, the Jul 30 low.

- Meanwhile, silver has also rallied by 1.1% to $37.8/oz, narrowing the gap to initial resistance at $39.655, a Fibonacci projection.

THURSDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 21/08/2025 | 0600/0700 | *** | Public Sector Finances | |

| 21/08/2025 | 0600/0800 | ** | Norway GDP | |

| 21/08/2025 | 0715/0915 | ** | S&P Global Services PMI (p) | |

| 21/08/2025 | 0715/0915 | ** | S&P Global Manufacturing PMI (p) | |

| 21/08/2025 | 0730/0930 | ** | S&P Global Services PMI (p) | |

| 21/08/2025 | 0730/0930 | ** | S&P Global Manufacturing PMI (p) | |

| 21/08/2025 | 0800/1000 | ** | S&P Global Services PMI (p) | |

| 21/08/2025 | 0800/1000 | ** | S&P Global Manufacturing PMI (p) | |

| 21/08/2025 | 0800/1000 | ** | S&P Global Composite PMI (p) | |

| 21/08/2025 | 0830/0930 | *** | S&P Global Manufacturing PMI flash | |

| 21/08/2025 | 0830/0930 | *** | S&P Global Services PMI flash | |

| 21/08/2025 | 0830/0930 | *** | S&P Global Composite PMI flash | |

| 21/08/2025 | 0900/1100 | ** | Construction Production | |

| 21/08/2025 | 1000/1100 | ** | CBI Industrial Trends | |

| 21/08/2025 | 1130/0730 | Atlanta Fed's Raphael Bostic | ||

| 21/08/2025 | 1230/0830 | *** | Jobless Claims | |

| 21/08/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 21/08/2025 | 1230/0830 | * | Industrial Product and Raw Material Price Index | |

| 21/08/2025 | 1230/0830 | ** | Philadelphia Fed Manufacturing Index | |

| 21/08/2025 | 1345/0945 | *** | S&P Global Manufacturing Index (Flash) | |

| 21/08/2025 | 1345/0945 | *** | S&P Global Services Index (flash) | |

| 21/08/2025 | 1400/1000 | *** | NAR existing home sales | |

| 21/08/2025 | 1400/1000 | * | Services Revenues | |

| 21/08/2025 | 1400/1600 | ** | Consumer Confidence Indicator (p) | |

| 21/08/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 21/08/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 21/08/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 21/08/2025 | 1700/1300 | ** | US Treasury Auction Result for TIPS 30 Year Bond | |

| 22/08/2025 | 2301/0001 | ** | Gfk Monthly Consumer Confidence | |

| 22/08/2025 | 2330/0830 | *** | CPI |