MNI ASIA MARKETS ANALYSIS: Focus on Thu's Data and Fed Speak

HIGHLIGHTS

- Treasuries see-sawed off early Wednesday lows to steady/mixed in late trade, focus on Thursday's heavy data (weekly claims, CPI, regional Fed and Tsy TICS) and Riksbank, Norges, Bank of England and ECB policy announcements.

- Intra-day swings for the US$ continued to reflect the limited appetite ahead of the busy central bank docket and the key US CPI data release on Thursday.

- Merger/acquisitions continued to make headlines as Paramount Skydance trade down -4.08% after Jared Kushner's private equity firm pulled out of the hostile takeover bid for Warner Brothers.

US TSYS

MNI US TSYS: Focus on Thursday's Data & Four Central Bank Policy Announcements

- Treasuries see-sawed off early Wednesday lows to steady/mixed in late trade, focus on Thursday's heavy data (weekly claims, CPI, regional Fed and Tsy TICS) and Riksbank, Norges, Bank of England and ECB policy announcements. Fed speakers are absent tomorrow.

- We won't get aggregate CPI levels for October tomorrow, but as part of the November report's unprecedented format, the BLS will include data for some but not all subcomponents for October.

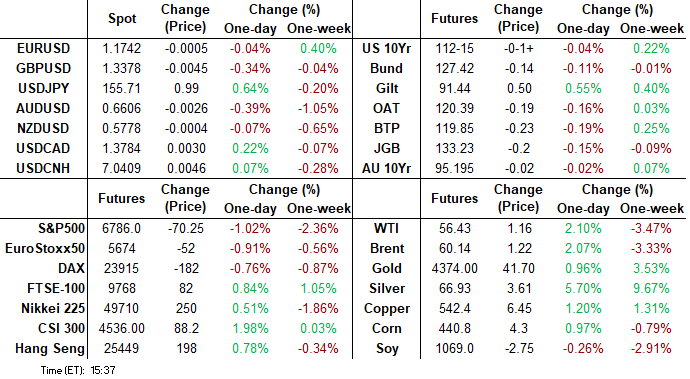

- Currently, TYH6 trades -1 at 112-15.5, yielding 4.1509% (+.0059). Curves mildly steeper, 2s10s +.995 at 66.588, still well off yesterday's 69.086% high.

- The short-term technical condition in Treasuries is bearish and near-term resistance points remain. A continuation lower would refocus attention on key support at 111-29, the Dec 10 low. Clearance of this level would confirm a resumption of the bear leg and open 111-19, a Fibonacci projection.

- On the upside, a clear breach of 112-23, the Dec 12 high would instead strengthen a short-term bull cycle.

- Gov Waller indicates in Q&A earlier that he's forecasting GDP growth of 1.6% this year and 2.5% in 2026 (vs FOMC medians 1.7% / 2.3%), and that supply-side improvements mean that stronger growth will not translate into stronger inflation (an argument advanced by the Trump administration as well as some of Waller's FOMC colleagues such as Gov Miran).

REFERENCE RATES

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 3.69% (-0.06), volume: $3.319T

- Broad General Collateral Rate (BGCR): 3.64% (-0.09), volume: $1.336T

- Tri-Party General Collateral Rate (TCR): 3.64% (-0.09), volume: $1.296T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 3.64% (+0.00), volume: $95B

- Daily Overnight Bank Funding Rate: 3.64% (+0.00), volume: $169B

FED Reverse Repo Operation:

RRP usage rises to $10.361B with 17 counterparties this afternoon, vs. Tuesday's $1.554B. Compares to last Thursday's $0.838B (lowest level since mid-March 2021); this years highest excess liquidity measure: $460.731B on June 30.

US SOFR/TREASURY OPTION SUMMARY

SOFR & Treasury options remained mixed, two-way on directional and vol structures on net ahead Thursday's heavy data (claims, CPI, TICS) and policy docket 4 central banks: Riksbank, Norges, BOE and EU. Underlying futures off early lows - near steady in 10s to mildly weaker in the short and long ends. While rates pared losses - projected rate cut pricing has gained some momentum vs. early morning levels (*): Jan'26 at -6.1bp (-5.5bp), Mar'26 at -15.2bp (-14.4bp), Apr'26 at -21.6bp (-20.5bp), Jun'26 at -35bp (-33.7bp).

SOFR Options:

+6,000 SFRG6 96.31/96.37 put spds, 1.25

-5,000 SFRM6 95.87 calls, 74.5 vs. 96.62/0.99%

-6,000 SFRU6 96.12/96.50 3x1 put spds, 1.5 ref 96.835

+4,000 SFRF6/SFRG6 96.31/96.37/96.43 call fly strip, 3.5 total

Block, +10,000 SFRZ6 97.00/98.00, 16.75 net vs. 96.87/0.32%

-15,000 SFRM6 97.00/97.50 call spds, 4.0 ref 96.685

over 12,500 SFRF6 96.62 calls, 1.75 last

8,476 SFRF6 96.50/96.56/96.81 broken call trees

Block, 2,500 0QG6 96.68/96.81/96.87/96.93 put condors ref 96.87

over 4,000 SFRH6 96.25/96.37/96.43/96.50 broken put condors

1,500 SFRH6 96.56 calls ref 96.465

+2,500 SFRU6 97.00/97.25/97.50 call flys, 2.25 ref 96.83

Treasury Options:

-10,000 TYG6 111.5/113.5 strangles, 28

Block/screen +17,100 TYF6 112.5 straddles, 32

+5,000 TYG6 114/115 call spds, 5

+5,000 wk1 TY/TYG6 112.5 call spds, 17

-10,000 TYF6 112 puts, 8

-5,000 wk3 TY 112.75/113.25/113.5 broken call fly seller, 2

+5,000 TYF6 113.5 calls, 3 ref 112-11

+2,500 TYG6 114 calls, 10

-2,500 TYF6 111.25/112.75 put spds, 26

+1,500 TYF6 112/112.5 2x1 put spds, 7 ref 112-11.5

+1,500 TYG6 113/114.5 call spds, 17 ref 112-12

over 5,300 TYF6 113 calls, 6 (*large buyers in low delta calls over last week)

over +12,300 TYF6 113.5 calls, 2-3*

+3,000 TYF6 110.5 puts, cab-7

2,500 TYF6 112.25 puts, 12 ref 112-13

MNI BONDS: EGBs-GILTS CASH CLOSE: Gilts Boosted By Soft UK CPI Ahead Of BOE, ECB

Gilts easily outperformed peers Wednesday as UK CPI came in on the soft side of expectations.

- The UK CPI miss was broad-based, with downside surprises in services, core goods and food inflation contributing to outperformance in the short-end/belly of the curve in early trade.

- Bunds were boosted only briefly by UK developments but weakened throughout most of the session, including a small leg lower on confirmation that the German Bundestag approved a defence procurement package worth E50bln.

- In other data, German IFO Business Climate unexpectedly fell for a second consecutive time in December.

- The UK curve bull steepened on the day, with Germany's bear steepening. Periphery/semi-core spreads closed little changed overall.

- Thursday's focus will be the ECB (MNI preview) and BOE (MNI preview) decisions.

- For the BOE, a 5-4 vote split in favor of a 25bp cut is expected but analysts are split over what happens after December. The ECB is set to hold rates, with attention on the updated macroeconomic projections and the balance of risks to inflation and growth.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 0.3bps at 2.137%, 5-Yr is up 1.4bps at 2.466%, 10-Yr is up 1.9bps at 2.864%, and 30-Yr is up 1.9bps at 3.485%.

- UK: The 2-Yr yield is down 5.8bps at 3.708%, 5-Yr is down 4.7bps at 3.913%, 10-Yr is down 4.3bps at 4.475%, and 30-Yr is down 3.5bps at 5.223%.

- Italian BTP spread up 0.7bps at 70.5bps / French OAT up 0.5bps at 71bps

MNI OPTIONS: Sizeable Sonia Call Structure Buying Before And After UK CPI

Wednesday's Europe rates/bond options flow included:

- DUG6 106.90/107.00/107.10/107.20c condor, bought for 1.5 in 2k

- OEG6 117.5 ^, bought for 142 in 2k

- RXF6/H6 129.5^ spread, sold the March at 73 in 2.25k

- RXG6 129.5/131cs, sold at 9.5 in 4k

- ERU6 98.1875/98.3125 call spread, paper pays 1.75 in 10k

- SFIF6 96.50/96.60/96.70c fly, bought for 1.5 in 5k

- SFIG6 96.45/96.55/96.65c fly, bought for 2.25 up to 2.50 in 15k

- SFIG6 96.60/96.70 call spread paper paid 1.25 on 25K

- SFIH6 96.65/70/75/80 call condor paper paid 0.5 on 12.8K

MNI FOREX: USDJPY Consolidates 0.5% Gains, Markets Await US CPI

- It was a tale of two halves for the broad dollar index on Wednesday, with early recovery strength slowly dissipating through the US session. Intra-day swings continue to reflect the limited appetite ahead of the busy central bank docket and the key US CPI data release on Thursday. The DXY stands just 0.15% in the green as we approach the APAC crossover.

- Greenback gains have been most notable against the Japanese Yen, with USDJPY consolidating towards the upper end of the day’s range around 155.55. The post-NFP bounce totals around 1.1% as we approach Friday’s BOJ meeting, where a 25bp hike to the policy rate remains priced in.

- GBP also had significant swings on the session following the below-expectation CPI data earlier today. While the data cements the likelihood of a 25bp rate cut from the BOE tomorrow, the figures place particular emphasis for a dovish surprise on the vote split and the potential for dovish developments regarding 2026 pricing.

- GBPUSD briefly extended losses to around 0.8% to 1.3312 before the general dollar turnaround prompted spot to rise back to around current levels of 1.3390. Initial firm support is 1.3290, the 50-day EMA, of which a breach would highlight a possible technical reversal.

- For USDCAD, it is worth highlighting that yesterday’s dip following the US jobs data essentially matched the first primary target for the selloff, trading to within 3 pips of the September lows at 1.3727. Subsequently, price has been consolidating below the 1.38 mark, keeping short-term bearish trend conditions in place following the technical breakdown earlier in the month.

- In emerging markets, mounting political uncertainty is continuing to dominate short-term sentiment in Brazil, with price action today extending the USDBRL bounce from cycle lows to around 5%.

- Interest rate decisions from the Riksbank, Norges Bank, BOE and ECB highlight tomorrow’s docket, alongside the eagerly awaited release of US CPI.

MNI FX OPTIONS: Expiries for Dec18 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1550(E1.9bln), $1.1600(E1.3bln), $1.1700(E1.4bln), $1.1735(E1.2bln), $1.1745-50(E3.3bln), $1.1797-00(E1.2bln), $1.2000(E1.9bln)

- USD/JPY: Y155.00($3.4bln), Y156.00($3.1bln), Y156.25($2.3bln), Y157.00($4.2bln), Y158.00($5.0bln), Y158.50($1.9bln), Y159.00($6.5bln)

- GBP/USD: $1.3600(Gbp570mln)

- AUD/USD: $0.6540-50(A$1.6bln), $0.6665-75(A$1.3bln)

- AUD/NZD: N$1.1410(A$1.5bln)

MNI US STOCKS: Late Equities Roundup: IT, Communication Services, Industrials Lag

- Stocks extend lows late Wednesday - the Nasdaq leading the decline as longs took profits ahead of the Christmas & New Years holidays. Currently, the DJIA trades down 153.34 points (-0.32%) at 47956.34, S&P E-Mini Futures down 65.75 points (-0.96%) at 6791, Nasdaq down 339.6 points (-1.5%) at 22771.63.

- Information Technology, Communication Services and Industrials sector shares continued to lead declines in the second half: Lam Research -5.10%, Oracle -5.04%, Broadcom -4.95%, Advanced Micro Devices -4.86%, Super Micro Computer -4.71%, Palantir Technologies -4.64%, Western Digital -4.51% and Dell Technologies -4.27%.

- Merger/acquisitions continued to make headlines as Paramount Skydance trade down -4.08% after Jared Kushner's private equity firm pulled out of the hostile takeover bid for Warner Brothers, the latter also down 2.04%. Warner executives implored investors to reject the $108B Paramount bid, calling it "illusory" in favor of Netflix's superior offer.

- GE Vernova -8.80%, Quanta Services -5.55%, EMCOR Group -4.84%, Generac Holdings -4.78%, Caterpillar -4.77% and Eaton Corp -4.68% weighed on the Industrials sector.

- On the positive side, Energy and Consumer Staples sector shares outperformed in the first half:

- Texas Pacific Land +6.05% after signing an agreement with Bolt Data to build data centers, followed by: ConocoPhillips +3.96%, Devon Energy +3.85%, Occidental Petroleum +3.37%, Targa Resources +2.60% and Diamondback Energy +1.94%.

- Meanwhile, General Mills +2.87%, Church & Dwight Co +2.64%, Kroger +2.38%, Clorox +1.99%, Procter & Gamble +1.88% and Hormel Foods +1.48% buoyed the Consumer Staples sector in the first half.

MNI EQUITY TECHS: E-MINI S&P: (H6) Pierces Support

- RES 4: 7100.00 Round number support

- RES 3: 7048.21 2.0% Upper Bollinger Band

- RES 2: 7014.00 High Oct 30 and the bull trigger

- RES 1: 6932.25/6988.00 High Dec 15 / 12

- PRICE: 6857.00 @ 14:36 GMT Dec 17

- SUP 1: 6831.93/6817.50 50-day EMA / Low Dec 16

- SUP 2: 6785.50 50.0% retracement of the Nov 21 - Dec 11 rally

- SUP 3: 6737.71 61.8% retracement of the Nov 21 - Dec 11 rally

- SUP 4: 6684.50 Low Nov 24

A bull cycle in S&P E-Minis remains intact and the latest pullback - for now - is considered corrective. Initial support to watch is 6831.93, the 50-day EMA. It has been pierced, a clear break of this average would signal scope for a deeper retracement. Note that the key support and reversal trigger lies at 6583.00, the Nov 21 low. For bulls, a resumption of gains would refocus attention on the key resistance and bull trigger at 7014.00, the Oct 30 high.

MNI COMMODITIES: Crude Rises Amid Sanction Threat, Silver Extends Gains

- Crude markets have found support from US plans to introduce further Russia sanctions if Putin does not agree to a peace deal, alongside a US move to blockade all sanctioned tankers from leaving and entering Venezuela.

- WTI Jan 26 is up by 1.4% at $56.1/bbl.

- The US is considering options such as targeting shadow fleet vessels used to transport Russian oil, as well as traders who facilitate the transactions, Bloomberg reports.

- The Venezuela blockade comes amid an escalating campaign by the Trump administration that has included a ramped-up military activity in the Caribbean.

- Despite today’s gains, a bearish theme in WTI futures remains intact. A key support and the bear trigger at $55.99, the Oct 20 low has been breached, opening $53.53.

- On the upside, initial resistance is at $59.14, the 50- day EMA.

- Elsewhere, precious metals have also risen today amid the escalating tensions between the US and Venezuela. While gold is up by 0.7% at $4,333/oz, silver has notably outperformed, with price currently 4.1% higher at $66.3/oz.

- Silver remains supported by a continued squeeze in physical markets, which has seen price rise ~10% since Nov 4 lows.

- From a technical perspective, a bullish theme in gold remains intact, with attention on key resistance and the bull trigger at $4,381.5, the Oct 20 high.

- For silver, today’s extension reinforces the current bull theme, with sights on $68.397 next, a Fibonacci projection.

THURSDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 18/12/2025 | 0745/0845 | ** | Manufacturing Sentiment | |

| 18/12/2025 | 0830/0930 | *** | Riksbank Interest Rate Decison | |

| 18/12/2025 | 0900/1000 | *** | Norges Bank Rate Decision | |

| 18/12/2025 | 1000/1100 | ** | EZ Construction Output | |

| 18/12/2025 | 1200/1200 | *** | Bank Of England Interest Rate | |

| 18/12/2025 | 1200/1200 | *** | Bank Of England Interest Rate | |

| 18/12/2025 | 1315/1415 | *** | ECB Deposit Rate | |

| 18/12/2025 | 1315/1415 | *** | ECB Main Refi Rate | |

| 18/12/2025 | 1315/1415 | *** | ECB Marginal Lending Rate | |

| 18/12/2025 | 1330/0830 | *** | Jobless Claims | |

| 18/12/2025 | 1330/0830 | ** | WASDE Weekly Import/Export | |

| 18/12/2025 | 1330/0830 | * | Payroll employment | |

| 18/12/2025 | 1330/0830 | ** | Philadelphia Fed Manufacturing Index | |

| 18/12/2025 | 1330/0830 | *** | CPI | |

| 18/12/2025 | 1330/0830 | *** | CPI | |

| 18/12/2025 | 1330/0830 | *** | CPI | |

| 18/12/2025 | 1330/0830 | *** | CPI | |

| 18/12/2025 | 1345/1445 | ECB Press Conference | ||

| 18/12/2025 | 1445/1545 | ECB Staff Macroeconomic Projections | ||

| 18/12/2025 | 1515/1615 | ECB Lagarde Presents Rate Decision on ECB Podcast | ||

| 18/12/2025 | 1530/1030 | ** | Natural Gas Stocks | |

| 18/12/2025 | 1600/1100 | ** | Kansas City Fed Manufacturing Index | |

| 18/12/2025 | 1630/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 18/12/2025 | 1630/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 18/12/2025 | 1800/1300 | ** | US Treasury Auction Result for TIPS 5 Year Note | |

| 18/12/2025 | 1900/1400 | *** | Mexico Interest Rate | |

| 18/12/2025 | 2100/1600 | ** | TICS | |

| 19/12/2025 | 2330/0830 | *** | CPI | |

| 19/12/2025 | 0001/0001 | ** | Gfk Monthly Consumer Confidence | |

| 19/12/2025 | 0300/1200 | *** | BOJ Policy Rate Announcement |