US TSYS: Focus on Thursday's Data & Four Central Bank Policy Announcements

- Treasuries see-sawed off early Wednesday lows to steady/mixed in late trade, focus on Thursday's heavy data (weekly claims, CPI, regional Fed and Tsy TICS) and Riksbank, Norges, Bank of England and ECB policy announcements. Fed speakers are absent tomorrow.

- We won't get aggregate CPI levels for October tomorrow, but as part of the November report's unprecedented format, the BLS will include data for some but not all subcomponents for October.

- Currently, TYH6 trades -1 at 112-15.5, yielding 4.1509% (+.0059). Curves mildly steeper, 2s10s +.995 at 66.588, still well off yesterday's 69.086% high.

- The short-term technical condition in Treasuries is bearish and near-term resistance points remain. A continuation lower would refocus attention on key support at 111-29, the Dec 10 low. Clearance of this level would confirm a resumption of the bear leg and open 111-19, a Fibonacci projection.

- On the upside, a clear breach of 112-23, the Dec 12 high would instead strengthen a short-term bull cycle.

- Gov Waller indicates in Q&A earlier that he's forecasting GDP growth of 1.6% this year and 2.5% in 2026 (vs FOMC medians 1.7% / 2.3%), and that supply-side improvements mean that stronger growth will not translate into stronger inflation (an argument advanced by the Trump administration as well as some of Waller's FOMC colleagues such as Gov Miran).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Late SOFR/Treasury Option Roundup: Holding Ranges

Treasury & SOFR option volumes were rather light Monday, underlying futures firmer - but off early session highs. Projected rate cut pricing appears steady to mixed vs late Friday levels (*): Dec'25 at -10.2bp (-10.8bp), Jan'26 at -20.1bp (-20.9bp), Mar'26 at -30.9bp (-30.8bp), Apr'26 at -37.6bp (-37.4bp).

- SOFR Options:

- +20,000 SFRZ5 96.18/96.25/96.31 call flys, 0.5 vs. 96.19/0.05%

- 4,000 SFRZ5 96.31/96.43 call spds

- Block 2,500 2QH6 97.12 calls, 8.0 vs. 96.755

- 5,000 SFRZ5 96.18/96.25/96.31 put flys ref 96.183

- 2,000 SFRZ5 96.18/96.31 call spds vs. 0QZ5 97.00/97.12 call spds

- 1,125 SFRZ5 96.00/96.06/96.12 put flys ref 96.183

- Treasury Options:

- +40,000 wk4 US 106 puts, cab-7

- 16,800 TUZ5 104 puts, 2.5 ref 104-03

- 2,000 USF6 111/116 2x1 put spds

- 7,100 TYZ5 113/113.5 call spds

- 5,300 TYF6 113/114/115 1x3x2 call spds

- 10,300 TYZ5 113/TYF6 113.5 call spds, 17 net/Jan over

- 2,100 USF6/USG6 116 put spds ref 116-19

- 1,600 FVF6 108/108.75 put spds ref 109-09.25

- 3,500 TYF6 110/112 put spds ref 112-20

- 1,700 TYF6 114.5/115.5 call spds ref 112-18

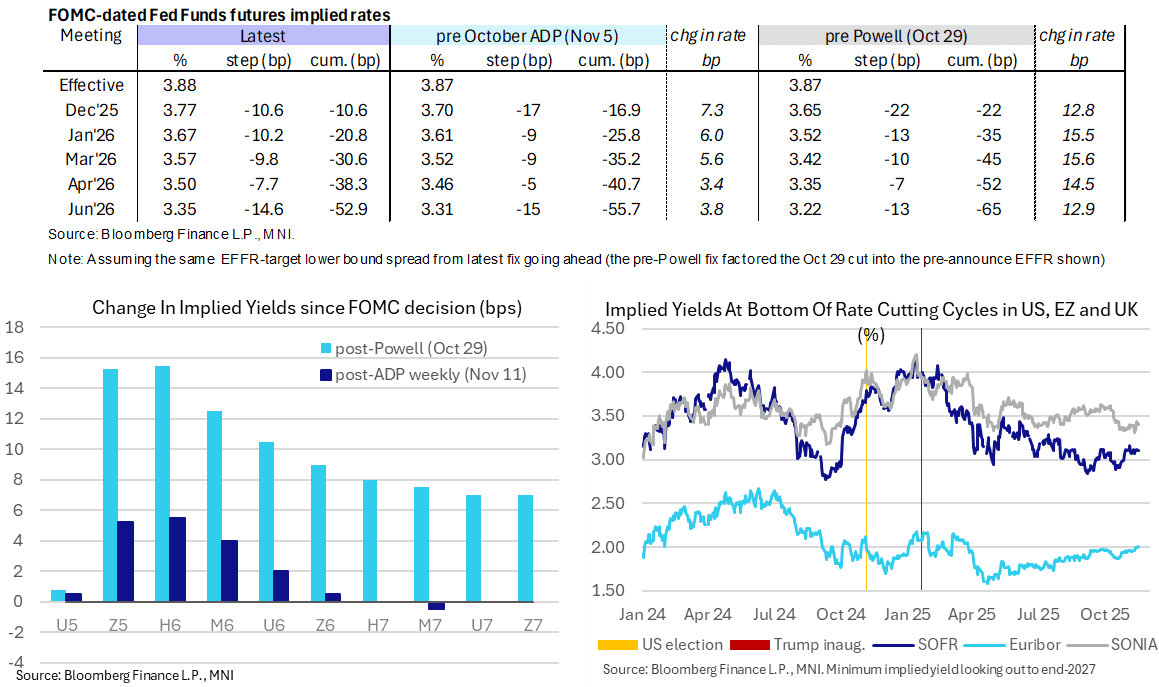

STIR: Fed December Pause Seen As Slightly More Likely, A Dovish Waller Ahead

- US rates at the very front end of the curve have given back some of today's further losses, with SFRZ5 back at 96.175 (-0.01) and the Fed Funds implied rate for the Dec FOMC limited to a 0.5bp increase from Friday’s close.

- The move has come within the past hour with little clear driver, but equally it pares what had been further momentum from last week’s hawkish Fedspeak rather than stronger data earlier.

- It maintains the recent development of a December pause being seen as slightly more likely.

- FF cumulative cuts from an assumed 3.88% effective: 10.5bp Dec, 21bp Jan, 30.5bp Mar, 38.5bp Apr and 53bp Jun.

- SOFR futures are -0.01 (Z5 and H6) to +0.02 (most 2027 contracts), with gains seen from U6 onwards.

- The terminal implied yield at 3.10% (H7) is unchanged since the start of the US session and between the 3.06-3.16% recent range that has been defined primarily by labor data and a strong ISM services report.

- Vice Chair Jefferson earlier today reiterated his increasingly cautious stance, seeing a need to proceed slowly on rates. If forced to guess we would think he is still marginally in favor of a December cut.

- Coming up at 1535ET, Fed Gov. Waller (voter, dove) speaks on the economic outlook (text + Q&A), having driven some gyrations in rates over the past six weeks by sounding a little more patient ahead of the October meeting before reverting to a more dovish stance since then.

- He made clear on Oct 31 that he still supports a rate cut in December and we expect more of the same today. "The fog might tell you to slow down. It doesn't tell you to pull over to the side of the road. You still have to go. You may want to be careful, but it doesn't mean to stop, and … the right thing to do with policy is to continue cutting."

- Tomorrow then sees weekly ADP data at 0815ET for what will be a closely watched update after last week’s abrupt weakness.

EURJPY TECHS: Trend Needle Points North

- RES 4: 181.70 1.764 proj of the Jul 31 - Sep 29 - Oct 2 price swing

- RES 3: 181.01 1.618 proj of the Jul 31 - Sep 29 - Oct 2 price swing

- RES 2: 180.37 1.500 proj of the Jul 31 - Sep 29 - Oct 2 price swing

- RES 1: 180.02 High Nov 14

- PRICE: 179.88 @ 16:15 GMT Nov 17

- SUP 1: 177.72/175.99 20- and 50-day EMA values

- SUP 2: 174.82 Low Oct 17

- SUP 3: 174.30 Bull channel support drawn from the Feb 28 low

- SUP 4: 173.92 Low Oct 6 and a gap high on the daily chart

The trend in EURJPY remains bullish and the cross is holding on to its latest gains. Recent strength has resulted in a break of the bull trigger at 178.82, the Oct 30 high, confirming a resumption of the medium-term uptrend. Note too that moving average studies are in a bull-mode position, highlighting a dominant uptrend. Sights are on 180.37, a Fibonacci projection. First support lies at 177.72, the 20-day EMA.