MNI ASIA MARKETS ANALYSIS: Fed Holds Steady, Two Govs Dissent

HIGHLIGHTS

- Tsys pared losses after the FOMC kept funds target rate steady at 4.25-4.50%, Fed Govs Waller and Bowman dissented in favor of a 25bp rate cut.

- Stronger than expected US data (ADP, GDP and Core PCE figures higher than expected) weighed on Treasuries early Wednesday.

- Bank of Canada holds 2.75% rate for third time in a row as expected by all economists.

- Pres Trump wants to impose 25% tariff on Idia in addition to unspecified penalty for buying Russian oil, final announcement this Friday.

US TSYS

MNI US TSYS: Fed Holds Steady, No Decision on Next Meeting

- Treasury futures are near late session lows, curves bear flattening as projected rate cuts into year end continue to cool after Chairman Powell said the FOMC has not yet made a decision on what it will do at its next policy meeting in September, adding that current policy is appropriate and there is lots of data between now and then.

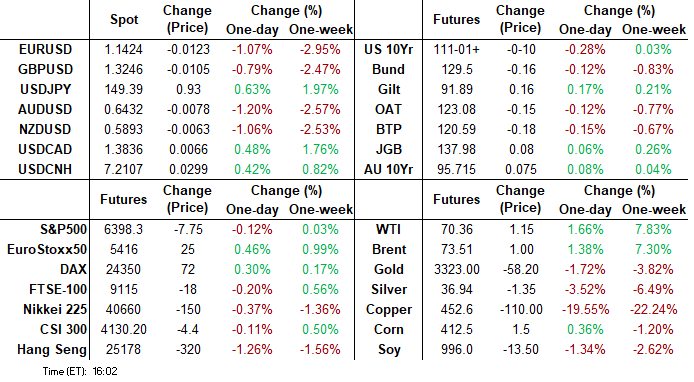

- Projected rate cut pricing retreated vs. this morning/pre-data (*) levels: Sep'25 at -11.8bp (-16.9bp), Oct'25 at -21.4bp (-29.1bp), Dec'25 at -37.1bp (-46.6bp), Jan'26 at -45.6bp (--55.6bp). Year end projection well off early July level of appr -65.0bp.

- Treasury futures had pared losses after the FOMC kept rate steady as Fed Govs Waller & Bowman dissented in favor of a 25bp cut. "The majority of the Committee was of the view that inflation is a bit above target, maximum employment is at target" Powell said. "That calls for modestly restrictive, in my way of thinking, modestly restrictive stance right now."

- Futures extended well past this morning's ADP/GDP/Core-PCE lows: Sep'25 10Y futures currently trades -10 at 111-01.5 vs. 110-30.5 low (111-14.5 high). Key support is 110-08+, the Jul 14 and 16 low. Clearance of this level would reinstate a bearish theme. First support is at 110-19+, the Jul 24 low. Curves shift to flatter: 2s10s -1.814 at 43.131, 5s30s -1.397 at 94.131.

- Cross asset: Stocks retreating (SPX eminis -20.0 at 6386.0), Gold weaker at 3271.82, Bbg US$ index remains well bid: 1218.99 (+9.01).

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.36% (+0.00), volume: $2.754T

- Broad General Collateral Rate (BGCR): 4.34% (-0.01), volume: $1.137T

- Tri-Party General Collateral Rate (TCR): 4.34% (-0.01), volume: $1.098T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $112B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $264B

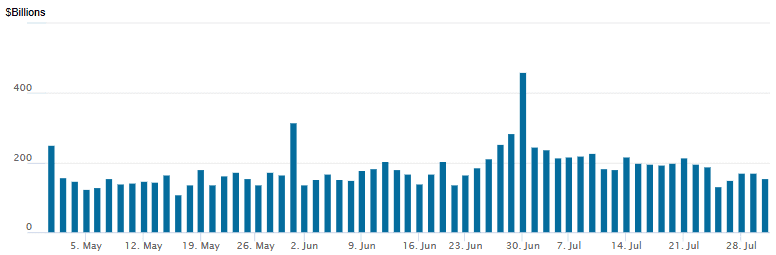

FED Reverse Repo Operation

RRP usage retreats to $155.481B this afternoon from $171.018B yesterday, total number of counterparties at 27. Usage had fallen to $54.772B on Wednesday, April 16 -- lowest level since April 2021 - compares to July 1: $460.731B highest usage since December 31.

US SOFR/TREASURY OPTION SUMMARY

Moderate two-way SOFR & Treasury option volumes Wednesday, some put unwinds/profit taking as underlying futures extend lows post-FOMC. Projected rate cut pricing retreated vs. this morning/pre-data (*) levels: Sep'25 at -11.8bp (-16.9bp), Oct'25 at -21.4bp (-29.1bp), Dec'25 at -37.1bp (-46.6bp), Jan'26 at -45.6bp (--55.6bp). Year end projection well off early July level of appr -65.0bp.

SOFR Options:

-8,000 0QQ5 96.62 puts, 5.5-6.0 ref 96.675

-6,000 0QU5 96.37 puts, 2.5 vs. 96.685/0.12%

-3,000 SFRH6 96.25 straddles, 44.75

+5,000 SFRZ5 96.62/97.75 call spds 2.75

+2,500 SFRU5 95.87 straddles 13.5 over 96.12 calls

+10,000 SFRH6 95.68 puts, 2.5 vs. 96.275/0.10%

-3,000 SFRZ5 96.00/96.37/96.75 call flys, 8.75

-4,000 0QV5 97.00/97.50/98.00 call flys, 5.25

4,000 SFRU5 95.75/95.81/95.93/96.00 call condors, 2.75

4,300 SFRZ5 96.12 straddles ref 96.105

2,000 SFRU5 95.75/95.68 put spds ref 95.845

Block/screen, 5,500 SFRV5 95.81/SFRZ5 95.62 put spds, 1.0 +Oct

Block, +8,000 SFRV5 95.68/95.81 2x1 put spds, 1.0

over 5,000 SFRZ5 95.62/96.87 strangles ref 96.105

4,000 SFRZ5 95.50/95.62/95.75 put flys, 1.5 ref 96.105 to -.11

2,000 0QQ5 96.93/97.06 call spds

+1,000 SFRU5 96.12/96.25 call spds, 0.75 vs. 95.90/0.04%

Block/screen, +12,000 SFRV5 96.12/96.25 call spds 1.0 over 95.81/95.93 put spds ref 96.105

Treasury Options:

+25,000 Wednesday wkly US 107 puts, 1 (exp 8/6)

+10,000 TYU5 109.5 puts, 8

+6,500 TYV5 111 straddles, 160

over +53,000 wk5 Wednesday FV 108 puts, 1, OI 1,545, expire today

+7,500 TYU5 114 calls, 5 ref 111-10

+1,500 TYU5 111 straddles, 118 vs. 111-14.5/0.16%

5,450 USU5 116 calls, 49 last

2,500 USU5 117 calls

2,000 Wednesday wkly TY 110.75 puts, 1 ref 111-14, expire today, OI 12,561

1,200 FVU5 110.25 calls ref 108-14

+3,000 TYX5 112/116 1x2 call spds vs. 110 puts, 5-6/call spd ovr

over 4,200 TYU5 110.5 puts, 19 ref 111-11 to -10

2,000 wk1 TY 110.25/110.5 put spds, 2 ref 111-11.5 (exp 8/1)

appr +3,000 TYU5 111.5/112.5 1x2 call spds

MNI BONDS: EGBs-GILTS CASH CLOSE: Flatter Curves Amid Heightened Data Flow

European curves flattened Wednesday.

- Early trade was constructive for EGBs and Gilts, stemming from the prior session's late strength in US Treasuries.

- A solid long-end Gilt tender and potentially some month-end dynamics also assisted. 10Y Gilt yields briefly hit their lowest intraday level since Jul 22; for Bunds Jul 24.

- Above-expected US data including private payrolls and GDP triggered a selloff in Treasuries that weighed across the Atlantic, seeing yields finish off their lows.

- Earlier, a slew of Eurozone data didn't really move the needle for markets: Euro Q2 GDP and July consumer confidence were slightly stronger than expected, while Spanish flash July inflation was slightly above-consensus and Belgian HICP decelerated. The ECB's forward looking wage tracker points to a continued decline in negotiation wage growth in Q1 2026.

- The German curve twist flattened, with the UK's bull flattening. Periphery/semi-core EGB spreads were mixed.

- The Federal Reserve decision will be a focus overnight, with Thursday bringing French, Italian, and German flash July inflation data (MNI's preview is here).

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 1.2bps at 1.954%, 5-Yr is up 0.3bps at 2.296%, 10-Yr is down 0.2bps at 2.706%, and 30-Yr is unchanged at 3.204%.

- UK: The 2-Yr yield is down 1.8bps at 3.876%, 5-Yr is down 2.6bps at 4.041%, 10-Yr is down 3bps at 4.603%, and 30-Yr is down 2.5bps at 5.416%.

- Italian BTP spread up 0.4bps at 81.4bps / French OAT down 0.3bps at 65.3bps

MNI EGB OPTIONS: Sonia Leans To Upside, Euribor To Downside Wednesday

Wednesday's Europe rates/bond options flow included:

- ERZ5 98.12/98.06/98.00 put fly paper paid 0.5 (vs. 98.13) on 5K

- ERZ5 97.87 puts paper paid 1.0 on 18K

- SFIQ5 96.15/96.20cs, bought for 0.6 in 5k

MNI FOREX: Fed Tips Greenback into Rally Mode, Clearing Key Levels

- After a shakier start to the European session, the USD soon recovered through NY hours, with strong GDP and ADP Employment Change numbers shortly followed by a resolutely patient outlook from the Fed Chair Powell following the Fed rate decision. Resultantly, the USD Index made light work of resistance into the mid-June highs, testing the 100-dma to the upside for the first time since October 2024.

- Powell's patient approach on policy came despite renewed pressure from the White House to cut interest rates, as he stressed that the FOMC see modestly restrictive policy as "appropriate", despite two dissents at the meeting (Bowman and Waller). The chair also talked down any decisions about the September meeting - stressing that the FOMC is still a ways from seeing where things settle down. As a result, rates pricing through year-end and into the second half of 2026 tightened, helping underpin the dollar rally.

- Markets remained content to sell the EUR through phases of USD strength, resulting in EUR/USD showing well through the late-June lows. This week’s bearish price action has resulted in a move through key support at the 50-day EMA, at 1.1560 - which highlights a stronger reversal and opens 1.1431, a Fibonacci retracement.

- Soft Australian CPI data remained a weight for AUD throughout the day - AUD/JPY is again testing Y96.00, while AUD/USD has shown through the bottom-end of the up-trend channel drawn through the April-July range.

- With the Fed decision now cleared for markets, focus shifts to China's manufacturing and non-manufacturing PMI prints for July, regional German inflation metrics and the Bank of Japan rate decision.

- The BoJ is widely expected to keep its policy rate unchanged at 0.5% for a fourth consecutive meeting, amid signs of easing trade-related uncertainty since its June meeting. Markets will pay close attention to Governor Ueda’s tone during the post-meeting press conference. Ueda has maintained a cautious stance since May, but if the forecasts and risk assessments are revised higher, there’s a high likelihood his tone may shift.

MNI FX OPTIONS: Expiries for Jul31 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1475-90(E1.3bln), $1.1490(E986mln), $1.1600-10(E2.6bln), $1.1650-70(E2.0bln), $1.1745-50(E1.1bln), $1.1800(E2.0bln)

- USD/JPY: Y146.00-20($1.5bln), Y147.40-50($728mln), Y148.00($522mln)

- AUD/USD: $0.6465(A$1.0bln), $0.6600(A$1.4bln)

- NZD/USD: $0.5965(N$505mln)

- USD/CAD: C$1.3670-75($1.0bln), C$1.3740($602mln)

- USD/CNY: Cny7.0700($1.4bln), Cny7.1500($897mln)

MNI US STOCKS: Late Equities Roundup: Retreating As Rate Cuts Cool

- Stocks sold off, extended lows after projected rate cuts into year end cooled (Dec'25 at -37.6bp vs. -46.6bp on the open) as Fed Chairman Powell continued to answer journals questions. Powell said it's "really hard to say" whether there will be enough information to cut in September."

- Currently, the DJIA trades down 298.93 points (-0.67%) at 44336.2, S&P E-Minis down 27 points (-0.42%) at 6379.75, Nasdaq down 17.5 points (-0.1%) at 21082.38.

- Leading decliners included IDEX -10.47%, Freeport-McMoRan -9.96%, Old Dominion Freight Line -9.36%, Trane Technologies -8.19%, Garmin -7.08%, Palo Alto Networks -5.58%, BXP Inc -5.48%, Verisk Analytics -5.45% and Carrier Global -5.30%.

- On the positive side, Teradyne still up +19.19% after reporting better than expected earnings this morning, Generac Holdings +19.14%, Humana +9.68%, Electronic Arts +7.19%, Bunge Global +5.46%, CVS Health +4.42%, Super Micro Computer +4.21% and American Electric Power Co +4.15%.

- Expected earnings after the close include: Ford Motor Co, Carvana Co, Albemarle Corp, Meta Platforms Inc, Robinhood Markets, QUALCOMM, Guardant Health Inc, Western Digital Corp, Cognizant Technology Solutions, Lam Research Corp, Microsoft, eBay and Allstate.

MNI EQUITY TECHS: E-MINI S&P: (U5) Bulls Remain In The Driver’s Seat

- RES 4: 6523.63 1.764 proj of the May 23 - Jun 11 - 23 price swing

- RES 3: 6500.00 Round number resistance

- RES 2: 6477.31 1.618 proj of the May 23 - Jun 11 - 23 price swing

- RES 1: 6457.75 High Jul 28

- PRICE: 6372.00 @ 1520 ET Jul 30

- SUP 1: 6322.32 20-day EMA

- SUP 2: 6241.00 Low Jul 16

- SUP 3: 6173.21 50-day EMA

- SUP 4: 6130.75 Low Jun 25

The trend set-up in S&P E-Minis remains bullish. Recent cycle highs once again confirm a resumption of the uptrend and maintain the price sequence of higher highs and higher lows. Note that moving average studies are in a bull-mode position highlighting a clear dominant uptrend. Sights are on 6477.31, a Fibonacci projection. Key support is at the 50-day EMA, at 6173.21. Support at the 20-day EMA is at 6322.32.

MNI OIL: WTI crude has reversed earlier declines and is slightly higher on the day

July 30 - Americas End-of-Day Oil Summary: WTI crude has reversed earlier declines and is slightly higher on the day, supported by the potential for further US action against Russia amid Trump’s 10-day deadline. The Fed left rates unchanged as expected with two dissents, and there was little market reaction.

- Polish PM Tusk said he had seen ‘signals’ that the Russia-Ukraine war might be ‘suspended.'

- The market is watching for any signs of progress towards a peace agreement that could see Russia avoid Trump’s threat of sanctions/secondary tariffs as part of his 10-day deadline.

- Focus is also on the risk of supply disruption from further sanctions on Russian oil, but President Trump doesn’t appear concerned about supply suggesting the US will increase its oil output.

- U.S. Treasury Secretary Scott Bessent said on Tuesday he warned Chinese officials that continuing to buy Russian oil would lead to big tariffs due to legislation in Congress.

- OPEC is also expected to increase its production target for September at its August 3 meeting.

- WTI Sep futures were up 1.2% at $70.00

- WTI Oct futures were up 1% at $68.97

THURSDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 31/07/2025 | 0600/0800 | ** | Import/Export Prices | |

| 31/07/2025 | 0630/0830 | ** | Retail Sales | |

| 31/07/2025 | 0645/0845 | *** | HICP (p) | |

| 31/07/2025 | 0645/0845 | ** | PPI | |

| 31/07/2025 | 0755/0955 | ** | Unemployment | |

| 31/07/2025 | 0800/1000 | *** | Bavaria CPI | |

| 31/07/2025 | 0800/1000 | *** | North Rhine Westphalia CPI | |

| 31/07/2025 | 0800/1000 | *** | Baden Wuerttemberg CPI | |

| 31/07/2025 | 0900/1100 | ** | Unemployment | |

| 31/07/2025 | 0900/1100 | *** | HICP (p) | |

| 31/07/2025 | 1000/1200 | ** | PPI | |

| 31/07/2025 | 1200/1400 | *** | HICP (p) | |

| 31/07/2025 | 1230/0830 | *** | Jobless Claims | |

| 31/07/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 31/07/2025 | 1230/0830 | * | Payroll employment | |

| 31/07/2025 | 1230/0830 | *** | Personal Income and Consumption | |

| 31/07/2025 | 1230/0830 | *** | Employment Cost Index | |

| 31/07/2025 | 1230/0830 | *** | Gross Domestic Product by Industry | |

| 31/07/2025 | 1342/0942 | *** | MNI Chicago PMI | |

| 31/07/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 31/07/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 31/07/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 01/08/2025 | 2300/0900 | ** | S&P Global Manufacturing PMI (f) | |

| 01/08/2025 | 2330/0830 | * | Labor Force Survey | |

| 01/08/2025 | 0030/0930 | ** | S&P Global Final Japan Manufacturing PMI | |

| 01/08/2025 | 0130/1130 | * | Producer price index q/q | |

| 01/08/2025 | 0145/0945 | ** | S&P Global Final China Manufacturing PMI |