FOREX: Fed Tips Greenback into Rally Mode, Clearing Key Levels

Jul-30 19:18

- After a shakier start to the European session, the USD soon recovered through NY hours, with strong GDP and ADP Employment Change numbers shortly followed by a resolutely patient outlook from the Fed Chair Powell following the Fed rate decision. Resultantly, the USD Index made light work of resistance into the mid-June highs, testing the 100-dma to the upside for the first time since October 2024.

- Powell's patient approach on policy came despite renewed pressure from the White House to cut interest rates, as he stressed that the FOMC see modestly restrictive policy as "appropriate", despite two dissents at the meeting (Bowman and Waller). The chair also talked down any decisions about the September meeting - stressing that the FOMC is still a ways from seeing where things settle down. As a result, rates pricing through year-end and into the second half of 2026 tightened, helping underpin the dollar rally.

- Markets remained content to sell the EUR through phases of USD strength, resulting in EUR/USD showing well through the late-June lows. This week’s bearish price action has resulted in a move through key support at the 50-day EMA, at 1.1560 - which highlights a stronger reversal and opens 1.1431, a Fibonacci retracement.

- Soft Australian CPI data remained a weight for AUD throughout the day - AUD/JPY is again testing Y96.00, while AUD/USD has shown through the bottom-end of the up-trend channel drawn through the April-July range.

- With the Fed decision now cleared for markets, focus shifts to China's manufacturing and non-manufacturing PMI prints for July, regional German inflation metrics and the Bank of Japan rate decision.

- The BoJ is widely expected to keep its policy rate unchanged at 0.5% for a fourth consecutive meeting, amid signs of easing trade-related uncertainty since its June meeting. Markets will pay close attention to Governor Ueda’s tone during the post-meeting press conference. Ueda has maintained a cautious stance since May, but if the forecasts and risk assessments are revised higher, there’s a high likelihood his tone may shift.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

SOFR: Morgan Stanley Opinion: Buy Dec'25 SOFR Ahead May Jolts, June NFP Data

Jun-30 19:17

- Morgan Stanley strategists suggest buying SFRZ5 futures ahead of tomorrow's May Jolts and Thursday's June Non-Farm Payrolls release that may underpin rate cut projections that are over halfway between 50bp to 75bp in rate cuts by year end.

- "Downside risks to US labor market data remain underpriced, especially considering the potential for near 0k payroll prints starting as soon as July," MS suggested in a recent strategy piece.

- Projected rate cut pricing gains slightly vs. late Friday (*) levels: Jul'25 at -5.3bp (-4.8bp), Sep'25 at -28.6bp (-28.2bp), Oct'25 steady at -46.3bp, Dec'25 at -66.8bp (-66.2bp).

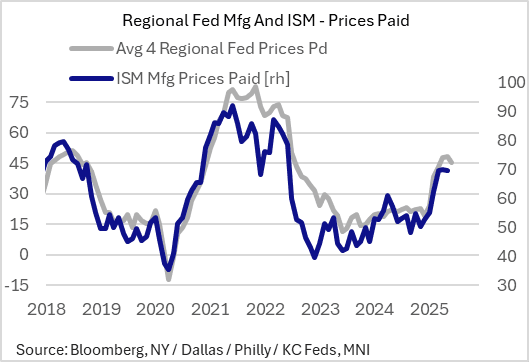

US OUTLOOK/OPINION: ISM Manufacturing Prices Paid Seen Steady (2/2)

Jun-30 19:14

The Prices Paid component of June's ISM Manufacturing survey, which will be closely watched for signs that tariffs are feeding into goods inflation, is expected by consensus to see a fairly flat reading of 69.5 vs 69.4 prior.

- Regional Fed surveys were extremely mixed though overall they point to flat or if anything slightly lower prices paid, but this could be dependent on when the question was asked. Empire State (New York) prices paid pulled back to a 3-month low, with Philly's at a 4-month low; however Kansas City prices pad rose to a 36-month high, with Dallas's ticking up to a 2-month high.

- The latter two regions are relatively impacted by energy sector developments so there may have been an element of the June oil price jump involved, particularly since this occurred in the latter half of the month before receding. For example Dallas's was collected June 17–25, with the high in oil prices right in the middle of those dates.

- Richmond's 12-month change meanwhile showed a sharp rise to a 26-month high (6.1%). though this is not really on a comparative basis with the index readings elsewhere.

- The S&P Global flash PMI noted a sharp rise in price pressures in the month :"Manufacturers’ input prices and selling prices both rose at rates not seen since July 2022, as higher costs were passed on to customers. Close to two-thirds of all manufacturers reporting higher input costs attributed

these to tariffs, whilst just over half of respondents linked increased selling prices to tariffs."

US TSYS: Lat SOFR/Treasury Option Roundup: SFOR Vol Spread, 10Y Calls

Jun-30 19:07

SOFR & Treasury option trade looked mixed on net, some chunky flows traded sporadically: Large Mar'26 SOFR Straddle buy vs. calls, while Treasury options say a pick-up in Sep & Aug 10Y call buying in the second half. Projected rate cut pricing gains slightly vs. late Friday (*) levels: Jul'25 at -5.3bp (-4.8bp), Sep'25 at -28.6bp (-28.2bp), Oct'25 steady at -46.3bp, Dec'25 at -66.8bp (-66.2bp).

- SOFR Options:

- -4,000 0QZ52QZ5 96.00 put spd, 2.0 net flattener

- +2,000 0QQ5 96.62/2QQ5 96.50/3QQ5 96.12 put fly, 1.5 net db

- +45,000 SFRH6 96.12 straddles vs. 97.00 calls, 28.5-29.0 vs. 97.00/0.20%

- +5,000 SFRN5 95.75/95.81 put spds, 0.25

- +2,000 SFRU5 95.75/95.81/95.87 put flys, .25 ref 95.985

- +4,000 2QZ5 96.25 puts, 9.0 vs. 96.785/0.20%

- Block/screen, 4,000 SFRU6 97.00/97.75 2x1 put spds, 4.0 net ref 96.91 to -.92

- -1,500 0QQ5 97.50 calls, 3.0 ref 96.92

- 2,000 SFRN5 95.87 puts

- -3,000 SFRU5 96.12/96.25 1x2 call spds, 5.5

- Treasury Options:

- +30,000 TYU5 112 calls, 1-04 ref 112-03

- 12,500 TYQ5 113 calls, 21 ref 112-02.5

- 3,500 TYQ5 110.75/111.25 put spds

- 10,000 TYU5 108/110 put spds ref 111-29

- -2,000 FVQ5 107.75 puts, 5

- over +11,300 FVQ5 108 puts, 7.5-8

- 6,000 TYQ5 110 puts

- +1,500 TYU5 109.5/111 put spds, 24 ref 111-31.5 vs. 111-29/0.10%

- +2,000 wk1 TY 111.25 puts, 6 vs. 111-28.5/0.10%

- +1,100 USQ5 116/119 2x3 call spds, 105 ref 114-30/0.36%