MNI ASIA MARKETS ANALYSIS: Fed Gov Miran Sees Dovish Data

HIGHLIGHTS

- Treasuries looked to finish near late Monday lows, narrow overall ranges and light volumes (TYH6 700k) at the start of the shortened Christmas holiday week: early close Wednesday at 1315ET, Thursday Closed, full session Friday.

- Fed Gov Miran on Bloomberg TV says that the incoming data have "come out in accordance with my view of the world", referring to last week's CPI and Employment Situation reports: "should push people into a dovish direction."

- The US dollar is notably weaker on Monday, with the USD index sliding roughly 0.35% as we approach the APAC crossover.

- Japanese finance minister Katayama ups the ante on language used toward the JPY, stating that they have a "free hand" to take bold action, and see speculative moves in currency markets, not based on fundamentals.

US TSYS

MNI US TSYS: Tsy Yld Gains Ahead Tue Data: Wkly ADP, GDP, IP/Cap-U, Tsy Note Sales

- Treasuries look to finish near late Monday lows, light volumes (TYH6 705k) on narrow ranges at the start of the shortened Christmas holiday week: early close Wednesday at 1315ET, Thursday Closed, full session Friday.

- Currently, TYH6 trades -4.5 at 112-11.5 (10Y yld 4.1667 +.0196) vs. 112-09.5 low, a continuation lower would refocus attention on 111-29, the Dec 10 low and a key short-term support. A breach of this support resumes the bear cycle that started Oct 17.

- Scant data today: Chicago Fed National Activity Index for September at -0.21 vs -0.31 in August, while Gov Miran on Bloomberg TV says that the incoming data have "come out in accordance with my view of the world", referring in particular to last week's CPI and Employment Situation reports.

- Focus is on tomorrow's busy morning data schedule: ADP Weekly, GDP, IP/Cap-U, while US Tsy auctions 2Y FRN and 5Y Notes.

- The Japanese finance minister Katayama provided the most forceful warning of intervention on Monday, stating that the MoF have a ‘free hand’ to take bold action on the currency. This kept pressure on USDJPY, which erased around 100 pips of the strong rally seen following the BOJ’s hike last Friday.

REFERENCE RATES

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 3.66% (+0.00), volume: $3.238T

- Broad General Collateral Rate (BGCR): 3.63% (+0.00), volume: $1.325T

- Tri-Party General Collateral Rate (TCR): 3.63% (+0.00), volume: $1.295T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 3.64% (+0.00), volume: $93B

- Daily Overnight Bank Funding Rate: 3.64% (+0.00), volume: $181B

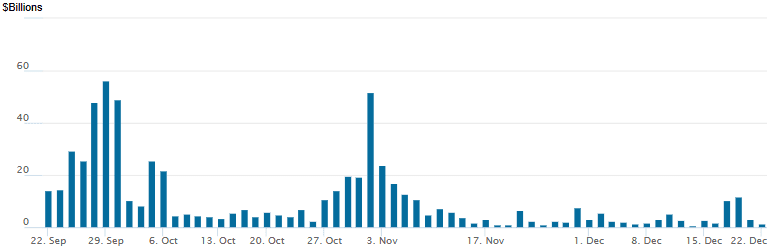

FED Reverse Repo Operation:

RRP usage slips to $1.523B with 7 counterparties this afternoon vs. Friday's $3.047B. Compares to December 12 low of $0.838B (lowest level since mid-March 2021); this years highest excess liquidity measure: $460.731B on June 30.

US SOFR/TREASURY OPTION SUMMARY

While downside puts made up the bulk of Monday's SOFR & Treasury option flow, scale buyer of low delta Mar'26 10Y calls carried over from last week. SOFR options included buyer of limited downside Jan'26 call fly targeting the 100.0 strike. Projected rate cut pricing cooled vs. early morning levels (*): Jan'26 at -5bp (-5.5bp), Mar'26 at -14.3bp (-15.1bp), Apr'26 at -21.5bp (-22.5bp), Jun'26 at -34.1bp (-35.3bp).

SOFR Options:

over +10,000 SFRF6 99.00/100.00/110.00 call flys, 1.75-1.62 vs. 96.92/0.05%

-2,000 SFRM6 96.43/96.56/96.62/96.68 put condors, 1.0 ref 96.685

+6,000 SFRH7 97.25 calls, 18.5 vs. 96.86

+4,000 SFRU6 96.12 puts, 1.75 vs. 96.83/0.06%

1,000 0QF6 96.75/97.06 strangles, 4.25 ref 96.885

+1,500 0QF6 96.87 straddles, 15.5 ref 96.88

1,000 0QH6 96.62/2QH6 96.56 2x1 put spds, 0.0

+2,500 SFRZ6 97.00/97.25 call spds 2.0 over SFRM6

+1,500 SFRH6 96.50 straddles, 16.75

+2,000 0QF6 99.75 puts, 2.5

-4,000 SFRH6 96.18/96.37/96.43/96.56 broken put condors, 5.0 ref 96.49

Treasury Options:

Over +62,200 TYH6 113 calls, 32-34

3,000 TYF6 112.25 puts, 5 ref 112-10.5

+6,000 TYF6 114 calls, 1 ref 112-11.5

1,450 FVG6 108.75/109.75 strangles, 19 ref 109-08

10,300 TYG6 113/114 call spds 11 ref 112-14.5

1,500 USH6 117/120/121 broken call flys

+1,200 TYG6 109.5 puts, 2 vs. 112-09/0.10%

+2,400 TYF6 112/112.5 2x1 put spds, 10 ref 112-12.5

1,000 TUH6 103.5/104/104.25/104.37 broken put condors ref 104-12.25

2,500 TYH6 112 put vs. USH6 114 puts on 2:1 ratio

+2,500 TYH6 110.5/111.5 put spds vs. TYG6 111.5 put, 3 net ref 112-14

over 5,700 wk2 TY 112.75 calls 15 ref 112-12.5 to -13

MNI BONDS: EGBs-GILTS CASH CLOSE: Bunds Enjoy Late Schnabel-Related Rally

Cash EGBs picked up a late bid Monday, mitigating an earlier rise in yields.

- Core FI started off the session on the back foot in a continuation of last week's BOE/ECB-influenced price action. 10Y German yields briefly moved above 2.90% for the first time since March and were above that level just 15 minutes before the close.

- ECB's Schnabel told a FAZ podcast released Monday that "at the moment, no interest rate increase is to be expected in the foreseeable future... I didn’t say that interest rates should be raised...but rather that they shouldn’t be lowered again. That’s a very important distinction" (as quoted by Bloomberg).

- Those comments were interpreted as tempering hawkish perceptions of her remarks from earlier in the month when she said she was "rather comfortable" with the market's modestly-implied 2026 hikes. They made headlines just before the cash close, depressing EGB yields across the curve.

- Gilts twist steepened on the day, with a slight uptick in long-end yields carrying on from Friday's trade but remaining within the month's ranges. Final Q3 UK GDP data met expectations.

- Periphery / semi-core EGB spreads mostly closed wider of Bunds, though OAT spreads held in, with a French official expressing confidence that a 2026 budget will be agreed after negotiations resume in January.

- This week's schedule is thin due to upcoming holidays, with only 2nd tier data this side of Christmas.

Closing Yields / 10-Yr EGB Spreads To Germany

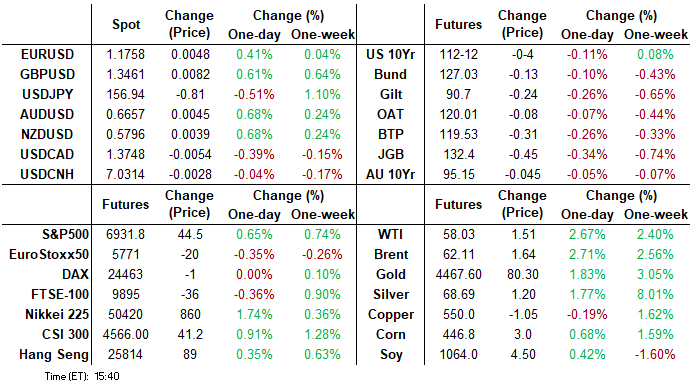

- Germany: The 2-Yr yield is down 0.6bps at 2.148%, 5-Yr is down 0.3bps at 2.485%, 10-Yr is up 0.2bps at 2.897%, and 30-Yr is down 0.4bps at 3.532%.

- UK: The 2-Yr yield is down 0.8bps at 3.745%, 5-Yr is up 0.5bps at 3.976%, 10-Yr is up 1.2bps at 4.536%, and 30-Yr is up 1.6bps at 5.271%.

- Italian BTP spread up 1.2bps at 70.2bps / French OAT down 0.1bps at 71.5bps

MNI OPTIONS: Continued Upside Buying In Sonia, Euribor Via Call Spreads

Monday's Europe rates/bond options flow included:

- RXG6 128/130cs, bought for 24 in 2k

- RXG6 126.00p, bought again for 29 in 7.2k total now

- RXG6 126.50/125.50 1x1.5 put spread paper paid 16.5 on 3K

- RXH6 126/129.5^^ vs 131c x6, bought the call for -24 (receive) in 500 x 3k

- ERU6 97.9375/98.0625cs, bought for 2.5 in 5k total

- SFIJ6 96.70/96.75cs, bought for 1.5 in 15k

- SFIJ6 96.55/96.65/9675/96.85c condor, bought for 3.5 in 10k

MNI FOREX: Softer USD Backdrop Prevailing, Katayama Sounds JPY Intervention Alarm

- The US dollar is notably weaker on Monday, with the USD index sliding roughly 0.35% as we approach the APAC crossover. This dynamic kept the focus on gold throughout the session, trading firmly to fresh all-time highs above $4,400/oz. Geopolitics remain in focus for FX markets with the US oil blockade of Venezuela continuing and US-European-Ukraine-Russia talks ended without a breakthrough with special envoy Witkoff saying that they were “productive and constructive".

- Firmer equity and oil/metal prices have boosted the likes of AUD and NZD to the top of the leaderboard, while GBP and JPY have also risen notably. NZDUSD has shrugged off the weakness from late last week and has returned to its medium-term pivot level of 0.5800, ahead of resistance which stands at 0.5831, the Dec 11 high.

- AUDUSD meanwhile remains in a bullish trend structure ahead of tomorrow's RBA minutes. The minutes will be scrutinised for more information around the board's degree of concern about upside inflation risks as well as how much this translates to the RBA's stance being skewed to the upside. AUDUSD is pressing towards resistance at 0.6686 December 10 high.

- An extension of GBPUSD strength was most notable during US hours, breaking above last week's 1.3456 highs, bolstering the ongoing bull theme and signalling scope for a move to 1.3527, the Oct 1 high.

- The Japanese finance minister Katayama provided the most forceful warning of intervention on Monday, stating that the MoF have a ‘free hand’ to take bold action on the currency. This kept pressure on USDJPY, which erased around 100 pips of the strong rally seen following the BOJ’s hike last Friday. Sights remain on key resistance at 157.89, the Nov 20 high and a bull trigger.

- In emerging markets, BRLMXN weakness continues to standout amid mounting political uncertainty in Brazil and ongoing Mexican peso resilience. The cross dropped another 1.2% today, closing in on 23 year lows just above 3.20.

MNI US STOCKS: Late Equities Roundup: Stock Gains a Nice Stocking Stuffer

- Stocks are holding decent gains at the start of the shortened Christmas holiday week, albeit amid generally light volumes on by late Monday.

- Currently, the DJIA trades up 209.24 points (0.43%) at 48339.18, S&P E-Mini Futures up 37.75 points (0.55%) at 6924.75, Nasdaq up 109.9 points (0.5%) at 23415.97.

- A mix of Energy, Materials, Pharmaceutical, Communication Services and Consumer Discretionary sector shares led advances in the second half: First Solar +6.67%, Moderna +6.04%, Huntington Ingalls +5.80%, Constellation Brands +5.09%, Norwegian Cruise Line +4.67%, Paramount Skydance +4.18% and Warner Bros Discovery +3.44%.

- Of note, Netflix trades 1.4% lower at the moment after they announced refinancing of a part of its $59B bridge facility with a $5B RCF and two $10B delayed-draw term loans. NFLX is expected to issue up to $25B senior unsecured notes on or before the closing date.

- Conversely, Consumer Staples, Utilities and Information Technology sector shares underperformed late Monday:

- Dollar Tree -3.97%, Target -2.86%, Lamb Weston Holdings -2.46% and Molson Coors Beverage -2.12%.

- Dominion Energy -5.35%, Eversource Energy -1.86% and Vistra Corp -0.49%.

- Seagate Technology -4.49%, Western Digital -2.48%, Zebra Technologies -1.08% and Apple -1.06%.

MNI EQUITY TECHS: E-MINI S&P: (H6) Trading Above Key Short-Term Support

- RES 4: 7021.79 0.618 proj Nov 21 - Dec 11 - 18 price swing

- RES 3: 7014.00 High Oct 30 and the bull trigger

- RES 2: 6988.00 High Dec 12

- RES 1: 6936.25 Intra-day high

- PRICE: 6931.00 @ 14:47 ET Dec 22

- SUP 1: 6771.50 Low Dec 18

- SUP 2: 6737.71 61.8% retracement of the Nov 21 - Dec 11 rally

- SUP 3: 6678.58 76.4% retracement of the Nov 21 - Dec 11 rally

- SUP 4: 6583.00 Low Nov 21

The recent pullback in S&P E-Minis appears corrective. A key short-term support has been defined at 6771.50, the Dec 18 low. A break of this level would signal scope for a deeper retracement of the recent bull phase between Nov 21 - Dec 11. This would open 6737.71, a Fibonacci retracement. For bulls a stronger resumption of gains would refocus attention on key resistance at 7014.00, the Oct 30 high.

COMMODITIES

MNI AMERICAS OIL: US OIL: December 22 - Americas End of Day Oil Summary: Crude Rises

US OIL: December 22 - Americas End of Day Oil Summary: Crude Rises

WTI Crude prices continue to rally following Friday’s gains supported by stronger risk appetite and geopolitical factors. The US blockage of Venezuelan oil and continued Ukrainian attacks on Russian energy infrastructure are providing support amid global oversupply fears.

- The US oil blockade of Venezuela continues with it boarding two shadow fleet tankers and continuing to seek a third. Venezuelan storage is approaching limits which could drive a reduction in production.

- SocGen sees a “full return to contango” for WTI early in the New Year despite the Venezuela situation, according to a note cited by Bloomberg.

- US-European-Ukraine-Russia talks continued in Florida on the weekend with special envoy Witkoff saying that they were “productive and constructive” with focus on aligning positions. Putin’s top foreign policy aide said on Sunday that proposal changes had not improved prospects for peace.

- WTI Feb futures were up 2.6% at $58.01

- WTI Mar futures were up 2.6% at $57.86

TUESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 23/12/2025 | 0700/0800 | ** | PPI | |

| 23/12/2025 | 0700/0800 | ** | Import/Export Prices | |

| 23/12/2025 | 0800/0900 | ** | PPI | |

| 23/12/2025 | 0800/0900 | *** | GDP (f) | |

| 23/12/2025 | 1200/0700 | ** | Brazil Preliminary CPI | |

| 23/12/2025 | 1330/0830 | *** | Gross Domestic Product by Industry | |

| 23/12/2025 | 1330/0830 | ** | Philadelphia Fed Nonmanufacturing Index | |

| 23/12/2025 | 1330/0830 | *** | GDP / PCE Quarterly | |

| 23/12/2025 | 1330/0830 | *** | GDP / PCE Quarterly | |

| 23/12/2025 | 1330/0830 | ** | Durable Goods New Orders | |

| 23/12/2025 | 1330/0830 | ** | Durable Goods New Orders | |

| 23/12/2025 | 1355/0855 | ** | Redbook Retail Sales Index | |

| 23/12/2025 | 1415/0915 | *** | Industrial Production | |

| 23/12/2025 | 1500/1000 | ** | Richmond Fed Survey | |

| 23/12/2025 | 1630/1130 | ** | US Treasury Auction Result for 52 Week Bill | |

| 23/12/2025 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 23/12/2025 | 1800/1300 | ** | US Treasury Auction Result for 2 Year Floating Rate Note | |

| 23/12/2025 | 1800/1300 | * | US Treasury Auction Result for 5 Year Note | |

| 23/12/2025 | 1830/1330 | Bank of Canada meeting minutes |