BONDS: EGBs-GILTS CASH CLOSE: Bunds Enjoy Late Schnabel-Related Rally

Cash EGBs picked up a late bid Monday, mitigating an earlier rise in yields.

- Core FI started off the session on the back foot in a continuation of last week's BOE/ECB-influenced price action. 10Y German yields briefly moved above 2.90% for the first time since March and were above that level just 15 minutes before the close.

- ECB's Schnabel told a FAZ podcast released Monday that "at the moment, no interest rate increase is to be expected in the foreseeable future... I didn’t say that interest rates should be raised...but rather that they shouldn’t be lowered again. That’s a very important distinction" (as quoted by Bloomberg).

- Those comments were interpreted as tempering hawkish perceptions of her remarks from earlier in the month when she said she was "rather comfortable" with the market's modestly-implied 2026 hikes. They made headlines just before the cash close, depressing EGB yields across the curve.

- Gilts twist steepened on the day, with a slight uptick in long-end yields carrying on from Friday's trade but remaining within the month's ranges. Final Q3 UK GDP data met expectations.

- Periphery / semi-core EGB spreads mostly closed wider of Bunds, though OAT spreads held in, with a French official expressing confidence that a 2026 budget will be agreed after negotiations resume in January.

- This week's schedule is thin due to upcoming holidays, with only 2nd tier data this side of Christmas.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 0.6bps at 2.148%, 5-Yr is down 0.3bps at 2.485%, 10-Yr is up 0.2bps at 2.897%, and 30-Yr is down 0.4bps at 3.532%.

- UK: The 2-Yr yield is down 0.8bps at 3.745%, 5-Yr is up 0.5bps at 3.976%, 10-Yr is up 1.2bps at 4.536%, and 30-Yr is up 1.6bps at 5.271%.

- Italian BTP spread up 1.2bps at 70.2bps / French OAT down 0.1bps at 71.5bps

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

RATINGS: Moody's Upgrades Italy To Baa2 From Baa3, Still A Notch Below Others

The Moody's upgrade to Italy's credit rating announced late Friday was the first from the agency since 2002 but shouldn't be considered a major surprise. Among the 3 major ratings agencies, Moody's had the lowest rating on Italy - by two notches (Fitch and S&P both BBB+).

- So this upgrade to Baa2 from Baa3 represents something of a closing of that gap rather than a major breakthrough for Italy.

- From the release:

- "The rating upgrade reflects a consistent track-record of political and policy stability which enhances the effectiveness of economic and fiscal reforms and investment implemented under the National Recovery and Resilience Plan (NRRP). It also points to prospects of further policy actions supporting growth and fiscal consolidation beyond the plan's deadline in August 2026. As a result, we expect that Italy's high government debt burden will gradually decline from 2027 onwards."

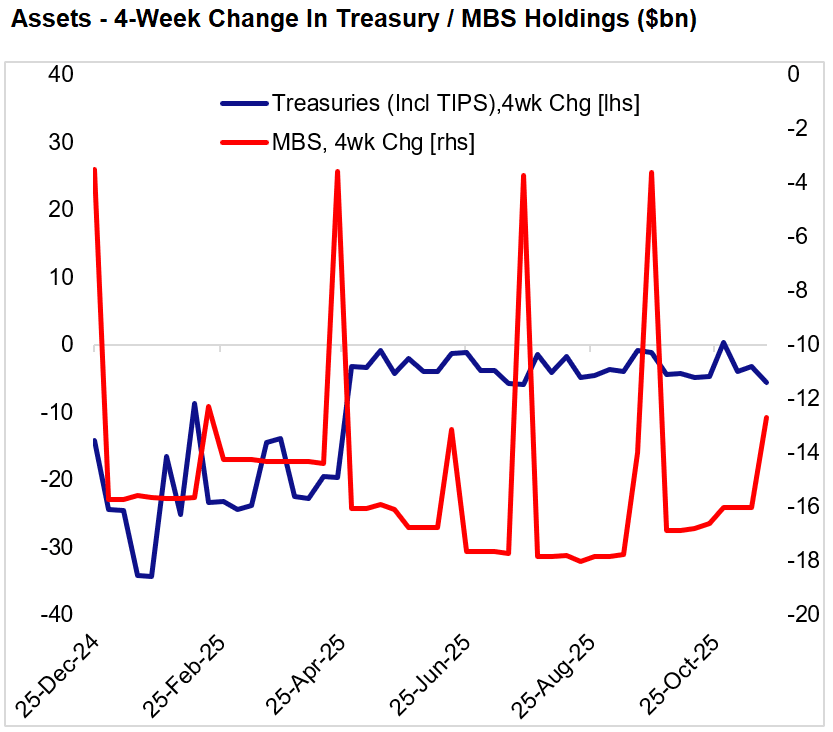

FED: Heading Into Its Final Weeks, QT Pace Remains At $20B/Month (2/2)

On the asset side of the Fed balance sheet, we saw a $25B drop in assets, of which just $2B could be attributed to QT in one of its final weeks (ends Dec 1).

- Instead it was a $6B drop in dealer repo operations vs a week earlier, and $17B in "other" areas that aren't related directly to monetary policy and typically don't have any significant impact on the size of the balance sheet (such changes are largely due to items such as bank premises, accrued interest, and other accounts receivable.)

- Discount window takeup edged up $0.3B to $6.1B but remains relatively low.

- QT has totaled just under $21B over the last month, around the expected pace, though as noted this will flatline in December with a pickup in net bills as MBS proceeds are rolled over into T-bills.

LOOK AHEAD: US Week Ahead: Retail Sales, PPI & Claims Headline Thanksgiving Week

A Thanksgiving-condensed week sees data highlights from delayed retail sales and PPI reports for September on Tuesday (Nov 25) before a Wednesday release for weekly jobless claims (Nov 26). Aside, the Fed’s Beige Book should also offer another important update on Wednesday for latest liaison reporting, with no Fedspeak currently scheduled around the holiday and the FOMC media blackout due to start on Saturday, Nov 29.

- As we regularly comment in this weekly publication, Redbook and Chicago Fed CARTS indicators point to solid nominal growth in retail sales, something broadly reflected in analyst consensus for the release.

- PPI inflation will offer a useful albeit not overly timely update on input cost pressures.

- Jobless claims will be watched particularly closely, both for latest initial claims for signs of layoffs and a notable update for continuing claims. The latter covers the payrolls reference period for November and will be an important reference point for FOMC members trying to get a sense of latest unemployment rate clues with the next payrolls reports coming after the Dec 9-10 FOMC decision (going into it with this week’s 0.12bp rise to 4.44% back in September).