MNI ASIA MARKETS ANALYSIS: Fed Delivers Third Consecutive Cut

HIGHLIGHTS

- Treasuries look to settle near late session highs after the FOMC delivered an expected 25bp rate cut, anticipation of hawkish guidance proved less-so.

- Stocks enjoyed the Fed messaging, the DJIA climbing to mid November highs while the tech-heavy Nasdaq reversed losses to finish higher as well.

- As the FOMC press conference progressed, negative sentiment towards the dollar has re-emerged, with the USD index extending session lows and now down a little more than 0.5%.

US TSYS

MNI US TSYS: Rates Rally, Fed Guidance Less Hawkish Than Anticipated

- Treasuries look to finish near late session highs after the FOMC delivered an expected 25bp rate cut, while anticipation for hawkish guidance proved less so - fueling bull curve steepening as Chairman Powell answered journalist questions.

- Currently, the TYH6 contract trades +10.5 at 113-13.5 vs. 113-14.5, initial key resistance is seen at 112-25+, the 20-day EMA. A break of this average would signal a possible reversal.

- Policymakers penciled in one more rate cut in 2026 and in 2027 on median, unchanged from the September Summary of Economic Projections. "In considering the extent and timing of additional adjustments to the target range for the federal funds rate, the Committee will carefully assess incoming data, the evolving outlook, and the balance of risks," the Fed said in its post-meeting statement.

- As the FOMC press conference progressed, negative sentiment towards the dollar has re-emerged, with the USD index extending session lows and now down a little more than 0.5%. Gains across the G10 have been broad based and are certainly more balanced than earlier on Wednesday.

- Earlier data - the ECI increased 0.79% non-annualized in Q3 (sa, cons 0.9) after an unrevised 0.94% in Q2 and 0.89% in Q1. It’s the softest quarter since 2Q21. The wages & salaries component also moderated to 0.79% after 1.01% in Q2 although that’s back close to the 0.77% in Q1.

REFERENCE RATES

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 3.93% (-0.02), volume: $3.244T

- Broad General Collateral Rate (BGCR): 3.90% (-0.03), volume: $1.315T

- Tri-Party General Collateral Rate (TCR): 3.90% (-0.03), volume: $1.285T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 3.89% (+0.00), volume: $85B

- Daily Overnight Bank Funding Rate: 3.89% (+0.00), volume: $161B

FED Reverse Repo Operation

RRP usage rises to $5.045B with 17 counterparties this afternoon from $3.211B Tuesday. Compares to Tuesday November 18: $0.905B - lowest level since mid-March 2021; this years highest excess liquidity measure: $460.731B on June 30.

US SOFR/TREASURY OPTION SUMMARY

Heavier 2-way SOFR & Treasury option flow throughout the session, making it difficult to summarize overall direction of flow. Underlying futures, however, continued to extend late session highs after the Federal Reserve delivered an expected 25bp rate cut while hawkish guidance proved less so. Projected rate cut pricing post FOMC: Jan'26 at -6.6bp, Mar'26 at -13.3bp, Apr'26 at -19.1bp, Jun'26 at -32.1bp.

SOFR Options:

-20,000 0QH6 97.25/97.50/97.75 call flys, 1.0 ref 96.77

+10,000 SFRH6 96.43/96.56/96.68 call flys, 1.75 ref 96.415

+10,000 0QF6 96.31/96.50 put spds, 1.5

+20,000 SFRF6 96.50 calls from 3.5-3.75 ref 96.415

2,600 SFRG6 96.31/96.37 put spds ref 96.415

+10,000 SFRH6 96.31/96.43/96.56 put flys, 1.5 ref 96.41

+3,000 SFRH6 96.43/96.56/96.68 put flys, 1.5 ref 96.41

+5,000 3QM6 97.50 calls, 2.0 vs. 96.39/0.04%

Block, 3,750 2QF6 96.12/96.25/96.37/96.50 put condors 2.5 vs. 96.635/0.12%

2,000 SFRZ6 96.25/96.50 put spds vs. 97.00/97.50 call spds

2,000 0QZ5 96.62/96.75/96.87 put flys ref 96.76

2,100 SFRZ5 96.25/96.31 combos vs. 96.76

2,000 SFRZ5 96.25 straddles ref 96.265

5,500 0QF6 96.50 puts ref 96.395

+14,000 SFRH6 96.31/96.37/96.43/96.50 put condors, 0.75 ref 96.395

over +10,000 SFRZ5 96.12 puts, 0.5

1,000 SFRU6 99.00/100.00 call spds ref 96.705

-6,500 SFRH6 96.25 puts, 2.0 ref 96.39/0.20%

1,500 SFRZ5 96.18/96.25/96.31 call flys ref 96.2625

4,000 SFRM6 96.37/97.00 risk reversals, 0.25 ref 96.58

Block, 2,500 2QH6 97.37/97.75 call spds 1.0

over 7,000 0QF6 96.25/96.50 put spds, 2.0-2.5

+2,250 2QF6 96.12/96.25/96.37/96.50 put condors, 2.5 ref 96.635/0.12%

Block, 4,000 0QF6 96.43/96.56 put spds, 2.5 vs. 96.74/0.10%

-8,500 SFRZ6 98.00/99.00 call spds, 3.5

+7,900 SFRH6 96.18/96.31/96.37 broken put flys, 2.0 ref 96.395

+2,960 0QF6 96.68 puts, 7.5 ref 96.77/0.37%

Treasury Options:

Block/screen, +24,000 TYG6 112.5/113 call spds, 12 vs. 112-07.5/0.10%

24,000 TYG6 114 calls, 12 ref 112-04.5

3,900 FVG6 109.5 calls, 17.5

7,000 FVH6 108/108.75 2x1 put spds

1,757 FVF6 109.25/109.5 call spds

+3,500 TYH6 114.5/115.5 1x2 call spds, 2 ref 111-31

4,000 TYH6 110/113.5 strangles ref 111-31.5

+6,666 wk3 TY 111.25/111.5 put spds, 5 vs. 111-30/0.08%

-1,500 TYF6 110.5/112.75 2x1 put spds, 54 ref 111-30/0.50%

-2,000 TYF6/TYG6 113 call spds, 15 ref 112-03.5/0.05%

+2,000 TYH6 111 puts, 37 vs. 112-01/0.30%

1,583 TUH6 103.5/103.75/104 put trees, ref 111-30

2,000 TYF6 112/112.5/113/114 broken call condors, 7 ref 112-03.5/0.03%

+5,000 wk2 111.5 puts, 6

+4,000 wk2 TY 111.75/112 put spds, 7 ref 111-31.5/0.08%

+2,000 TYF6 114 calls, 4

-2,100 FVF6 108/108.25/108.5/108.75 put condors, 3.5 ref 108-27

-1,400 FVF6 108.5/109 2x1 put spds, 3.5 ref 108-29.5

1,650 TYF6 112.5/TYG6 111.5 put spd ref 112-02.5

-2,850 TYG6 111/113.5 risk reversals, 4 ref 112-03.5

MNI BONDS: EGBs-GILTS CASH CLOSE: German Short-End Remains Under Light Pressure

European yields rose slightly Wednesday.

- The German curve saw light bear flattening with continued short-end underperformance as ECB hike pricing edging higher for 2026 despite some pushback against that notion by ECB's Villeroy and Simkus.

- That helped drag on the UK short-end/belly as well. Overall on the day though the German short-end underperformed its UK counterpart; vice-versa for the long-end.

- In a session limited on data and macro developments, softer-than-expected US employment cost data helped global core FI recover from early session lows. ECB's Kazaks told an MNI Connect event that monetary policy remains in a "good place" with no need to act in December.

- Periphery/semi-core EGB spreads were little changed on the day, with OAT spreads closing slightly wider despite the French National Assembly passing the 2026 Social Security budget after Tuesday's close.

- Attention after the cash close will be on the US Federal Reserve decision; Thursday's calendar includes the SNB decision.

Closing Yields / 10-Yr EGB Spreads To Germany

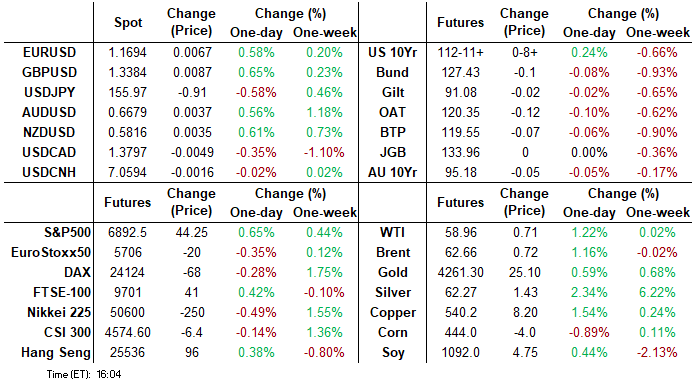

- Germany: The 2-Yr yield is up 2.3bps at 2.177%, 5-Yr is up 1bps at 2.476%, 10-Yr is up 0.1bps at 2.851%, and 30-Yr is down 0.6bps at 3.453%.

- UK: The 2-Yr yield is up 0.5bps at 3.79%, 5-Yr is up 1.1bps at 3.983%, 10-Yr is up 0.1bps at 4.506%, and 30-Yr is up 1bps at 5.205%.

- Italian BTP spread up 0.1bps at 69.6bps / French OAT up 0.3bps at 71.6bps

MNI OPTIONS: Large Euribor Call Condors Feature Wednesday

Wednesday's Europe rates/bond options flow included:

- DUG6 106.8/107/107.2c fly, bought for 2.5 in 4k

- DUH6 106.80/107.00/107.20c fly, bought for 3 in 10k

- DUH7 107c, bought for 5.75 in 5k

- RX (Week 2) 124.50p, bought for 1 in 3.5k

- RXG6 128.50/130cs vs 126/125ps, bought the cs for 11 and 11.5 in 5k

- RXG6 127.5/126.5ps vs 129.5/131/131.5/134.5c condor, bought the ps for 38.5 in 4.75k (ref 127.14)

- ERU6 98.00/98.50cs vs 97.87/97.62ps, bought the cs for -2 and -1.75 (receive) in 10k

- ERU6 98.125/98.375/98.4375/98.6875 call condor, bought for 2.5 & 2.75 in 10k

- ERZ6 98.375/98.625/98.75/99.00 call condor stripped with the 98.3125/98.4375/98.75/98.875 call condor paper paid 2 on 12.25K

MNI FOREX: USD Selling Resumes, DXY Extends Decline to 0.65%

- As the FOMC press conference progressed, negative sentiment towards the dollar has re-emerged, with the USD index extending session lows and now down a little more than 0.5%. Gains across the G10 have been broad based and are certainly more balanced than earlier on Wednesday.

- This dynamic has propelled the likes of EUR, AUD and NZD to fresh recovery highs, while the Japanese Yen has been eroding the week’s advance with USDJPY now trading back below the 156.00 handle. GBPUSD is also pressing towards 1.34, while the Swiss Franc and Swedish krona remain the day’s best performers.

- For EURUSD, spot is testing the 1.17 handle for the first time since October 17, keeping the technical bull cycle intact. The recent breach of key short-term resistance at 1.1656, the Nov 13 high and a bull trigger, and today’s extension higher strengthens the underlying bullish sentiment. 1.1728 and 1.1779 represent the next levels on the topside.

- AUDUSD has notably risen above the September 18 high of 0.6660, extending the impressive surge from the November lows to 4.12% amid the more hawkish RBA and firmer risk sentiment. A strong impulsive bull wave in AUDUSD remains intact, signalling scope for a continuation near-term. 0.6707 remains a key resistance point, the September 17 high.

- In similar vein, NZDUSD has extended above pivot resistance at 0.5800, registering a 0.5825 high on Wednesday, while USDSEK (-1.12%) has significantly narrowed the gap to recent cycle lows at 9.1936. A break below here would place the pair at the lowest level since February 2022.

MNI OPTIONS: Expiries for Dec11 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1595-00(E3.2bln), $1.1610(E3.9bln), $1.1710(E1.4bln), $1.1800(E1.7bln)

- USD/JPY: Y154.95-00($1.1bln), Y156.00($2.8bln)

- AUD/USD: $0.6550(A$1.6bln), $0.6640(A$732mln)

- USD/CAD: C$1.4000($968mln)

MNI US STOCKS: Late Equities Update: Extending Late Session Highs

- Stocks have staged a late session rally - well after the initial reaction to the anticipated FOMC 25bp rate cut, the DJIA continues to outperform, dragging the tech-heavy Nasdaq off session lows.

- Currently, the DJIA trades up 593.69 points (1.25%) at 48149.94, S&P E-Mini Futures up 54.25 points (0.79%) at 6902.75, Nasdaq up 116.2 points (0.5%) at 23693.05.

- Leading advances, Industrials, Consumer Discretionary and Materials sector shares led late advances

- GE Vernova +16.46%, Axon Enterprise +5.00%, Old Dominion Freight Line +4.53%, Stanley Black & Decker +4.20% and Cummins +4.03%.

- LKQ Corp +6.11%, Expedia Group +4.91%, Royal Caribbean Cruises +4.49% and NIKE +3.41%.

- Dow Inc +4.67%, Packaging Corp of America +4.47%, LyondellBasell Industries +3.74% and Smurfit WestRock +3.65%.

- On the flip side, Utilities, Consumer Staples and Communication Services sector shares led late declines:

- American Electric Power -1.63%, Southern Co -1.54%, PPL Corp -1.39%, Xcel Energy -1.15% and Public Service Enterprise -1.15%.

- Kroger Co -1.88%, Costco Wholesale -1.65%, Campbell's Company -1.33% and Walmart -1.27%.

- Netflix -3.57%, T-Mobile US -2.94%, Meta Platforms -1.39% and Match Group -1.35%.

MNI OUTLOOK: Price Signal Summary - S&P E-Minis Bull Intact

- In the equity space, a bull cycle in S&P E-Minis remains intact and price continues to trade above the 20- and 50- day EMAs. Note that recent gains signal the likely end of the corrective cycle between Oct 30 and Nov 21. A continuation higher would highlight potential for a move towards the key resistance and bull trigger at 6953.75, the Oct 30 high. Key support lies at 6525.00, the Nov 21 low. First support is at 6807.02, the 20-day EMA.

MNI COMMODITIES: Crude Rebounds On US-Venezuela Tensions, Precious Metals Edge Up

- Oil prices have rebounded following a Bloomberg headline that the US has seized an oil tanker off the coast of Venezuela, raising concerns for the country’s exports.

- Meanwhile, Trump and European leader see a ‘critical moment’ for Ukraine, but a final peace agreement still appears elusive.

- WTI Jan 26 is up 0.7% at $58.7/bbl.

- Looking ahead, the IEA and OPEC are due to publish updated projections for the future market balance on Thursday.

- Short-term gains in WTI futures appear corrective, for now, and a bear threat remains present.

- A stronger resumption of the bear leg would open key support and the bear trigger at $55.99, the Oct 20 low. Key short-term resistance to watch is $61.84, the Oct 24 high.

- Meanwhile, precious metals have edged higher today, despite a brief decline in the aftermath of the Fed rate decision.

- Spot gold has ticked up by 0.1% to session lows at $4,214/oz, while silver has risen by 0.5% to $61.0/oz.

- From a technical perspective, gold is now in consolidation mode. On the upside, sights are on key resistance and the bull trigger at $4,381.5, the Oct 20 high. Meanwhile, key support to watch is the 50-day EMA, at $4,049.8.

- For silver, trend signals remain bullish following yesterday’s surge to fresh cycle highs. Having traded through the psychological $60.00 handle, this paves the way for an extension towards $61.895, a Fibonacci projection.

THURSDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 11/12/2025 | 0700/0800 | *** | Final Inflation Report | |

| 11/12/2025 | 0700/0800 | *** | Final Inflation Report | |

| 11/12/2025 | 0830/0930 | *** | SNB Interest Rate Decision | |

| 11/12/2025 | 0950/0950 | BOE Bailey Pre-recorded Chat on Financial Stability | ||

| 11/12/2025 | 1000/1000 | BOE Bailey Gives Evidence At Covid-19 Inquiry | ||

| 11/12/2025 | 1100/0600 | *** | Turkey Benchmark Rate | |

| 11/12/2025 | - | *** | Money Supply | |

| 11/12/2025 | - | *** | Social Financing | |

| 11/12/2025 | - | *** | New Loans | |

| 11/12/2025 | - | ECB Lagarde and Cipollone at Eurogroup Meeting | ||

| 11/12/2025 | 1330/0830 | *** | Jobless Claims | |

| 11/12/2025 | 1330/0830 | ** | WASDE Weekly Import/Export | |

| 11/12/2025 | 1330/0830 | * | Household debt-to-income | |

| 11/12/2025 | 1330/0830 | ** | International Merchandise Trade (Trade Balance) | |

| 11/12/2025 | 1330/0830 | ** | Trade Balance | |

| 11/12/2025 | 1330/0830 | ** | Trade Balance | |

| 11/12/2025 | 1500/1000 | * | Services Revenues | |

| 11/12/2025 | 1500/1000 | ** | Wholesale Trade | |

| 11/12/2025 | 1500/1000 | ** | Wholesale Trade | |

| 11/12/2025 | 1530/1030 | ** | Natural Gas Stocks | |

| 11/12/2025 | 1630/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 11/12/2025 | 1630/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 11/12/2025 | 1800/1300 | *** | US Treasury Auction Result for 30 Year Bond | |

| 12/12/2025 | 0430/1330 | ** | Industrial Production |